Toys Market Size, Share, Trends and Forecast by Product Type, Age Group, Sales Channel, and Region, 2026-2034

Global Toys Market Size, Share, Trends & Forecast (2026-2034)

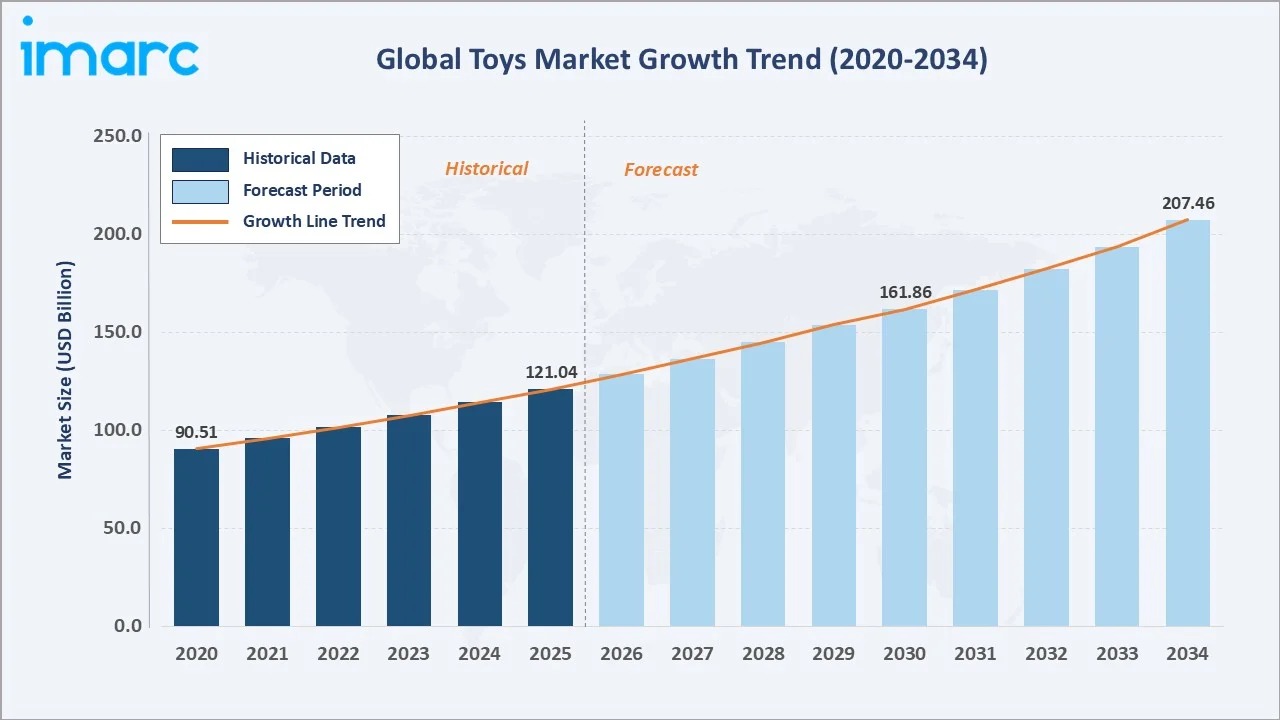

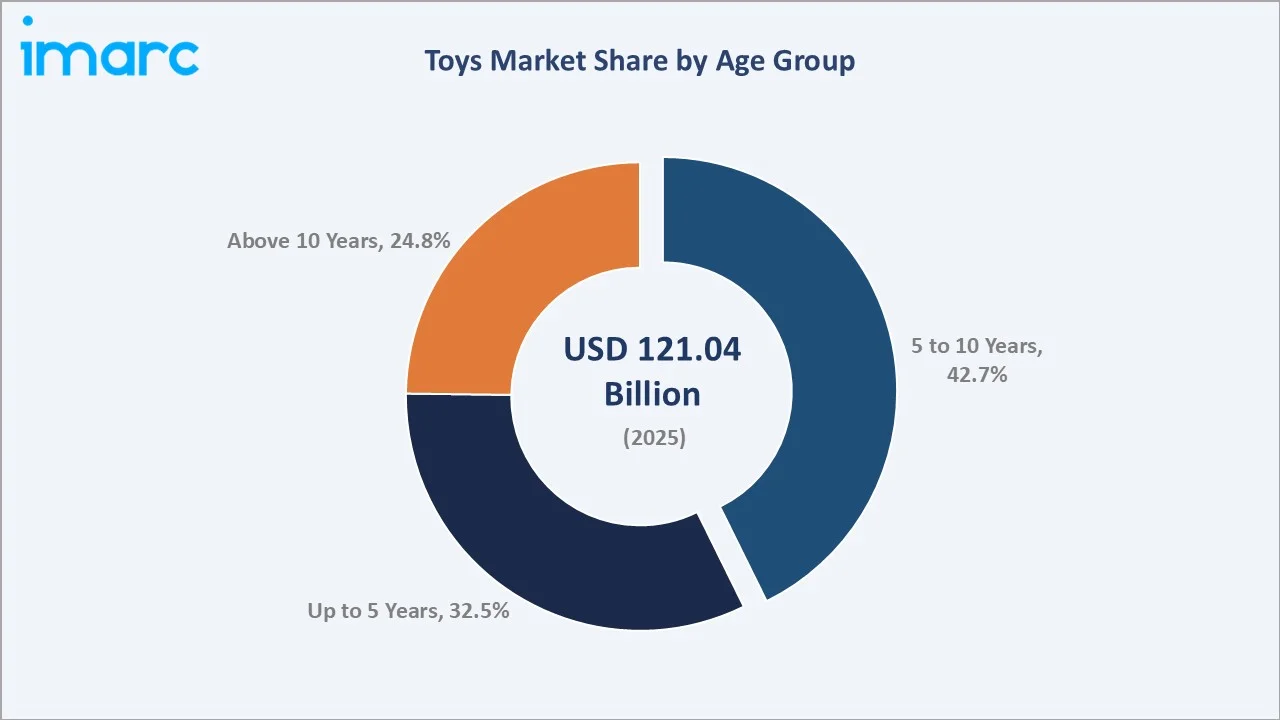

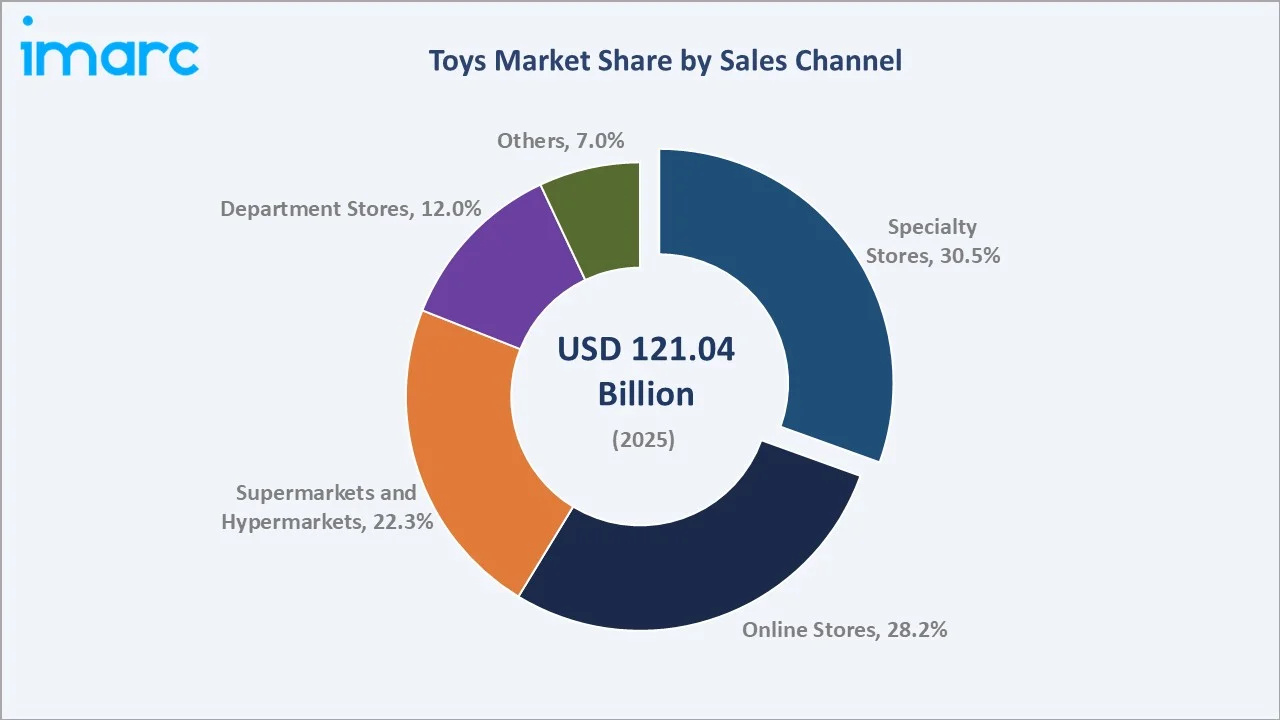

The global toys market size was valued at USD 121.04 Billion in 2025 and is projected to reach USD 207.46 Billion by 2034, exhibiting a CAGR of 5.98% during the forecast period 2026-2034. Rising disposable incomes, growing parental awareness of developmental benefits, and the rapid penetration of e-commerce platforms are driving the toys market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 121.04 Billion |

|

Forecast Market Size (2034) |

USD 207.46 Billion |

|

CAGR (2026-2034) |

5.98% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

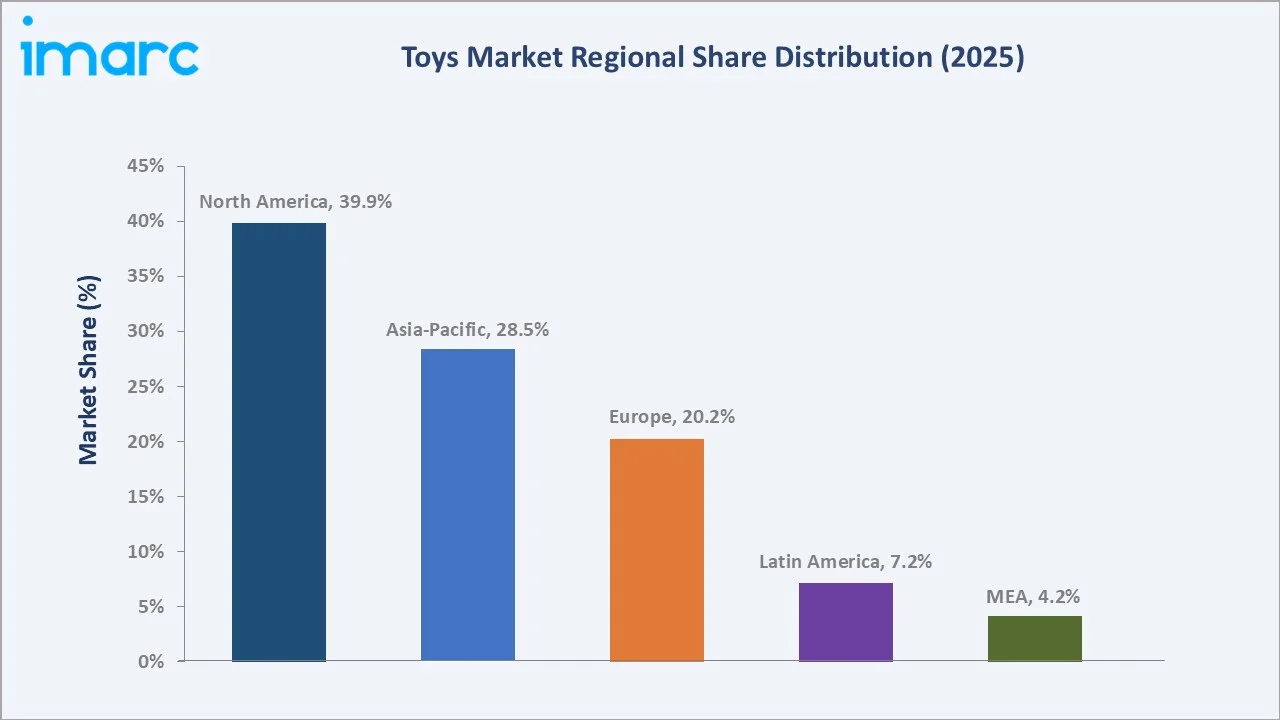

Largest Region |

North America (39.9% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~7.2% CAGR) |

|

Leading Age Group |

5 to 10 Years (42.7%, 2025) |

|

Leading Sales Channel |

Specialty Stores (30.5%, 2025) |

To get more information on this market, Request Sample

The global toys market growth trajectory from 2020 through 2034 contrasts historical expansion against a sustained forecast curve powered by innovation, rising incomes, and expanding digital commerce across all major regions.

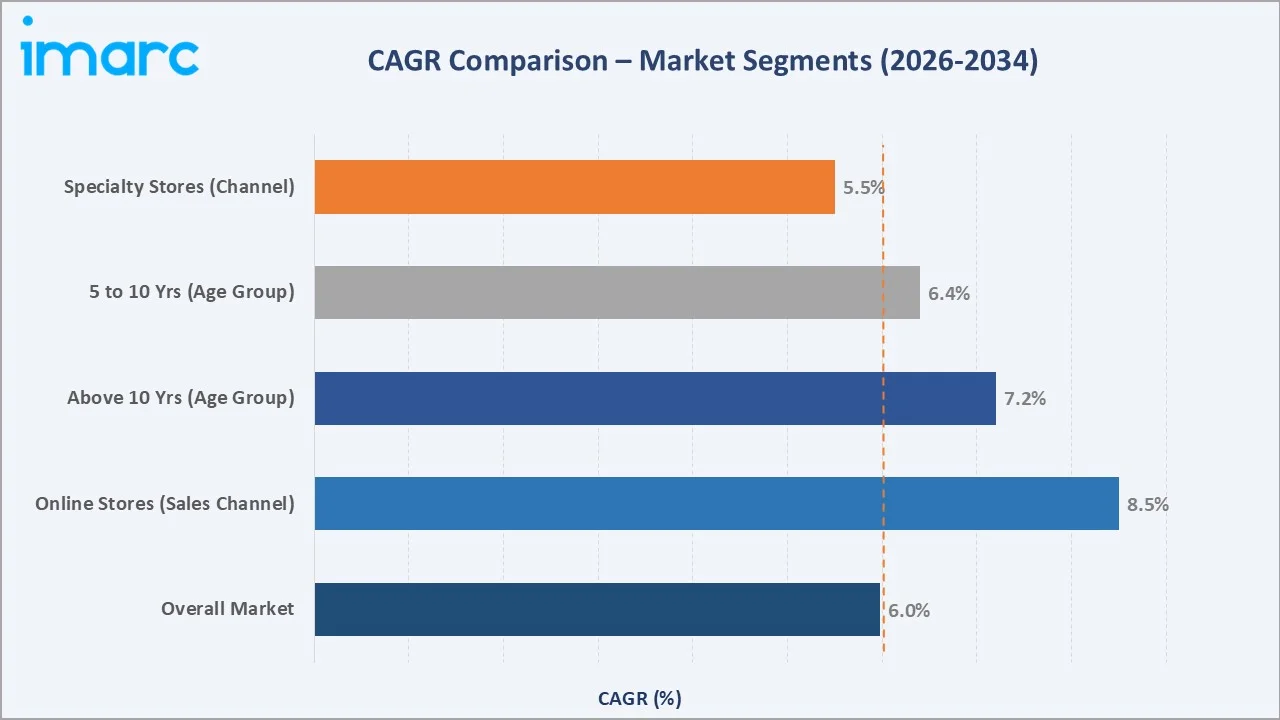

Segment-level CAGR comparisons highlight online channel adoption and the Above-10-Years age group as the fastest-growing sub-categories within the global toys market forecast through 2034.

Executive Summary

The global toys market is undergoing significant structural transformation. It is fuelled by rising consumer spending on premium and educational play products, accelerating digital-retail penetration, and growing demand for STEM-based and licensed character toys. Valued at USD 121.04 Billion in 2025, the market is forecast to reach USD 207.46 Billion by 2034 at a CAGR of 5.98%.

The 5-to-10-year age group commands 42.7% share in 2025, driven by educational, action, and building-set categories. The up-to-5-years segment represents 32.5% and is propelled by developmental toy innovation. Specialty stores lead at 30.5%, while online stores are the fastest-growing channel at an estimated CAGR of ~8.5% through 2030.

North America leads globally with 39.9% global revenue share in 2025. Asia-Pacific holds 28.5% and is forecast to be the fastest-growing region. The toys market outlook remains positive as digital integration, sustainability-led manufacturing, and licensing-driven demand converge across all major geographies.

Key Market Insights

|

Insight |

Data |

|

Largest Age Group Segment |

5 to 10 Years - 42.7% share (2025) |

|

Second Age Group |

Up to 5 Years - 32.5% share (2025) |

|

Leading Sales Channel |

Specialty Stores - 30.5% share (2025) |

|

Fastest Growing Channel |

Online Stores - ~8.5% CAGR (2026-2034) |

|

Leading Region |

North America - 39.9% revenue share (2025) |

|

Top Companies |

The LEGO Group, Mattel, Hasbro, Bandai Namco Holdings Inc, Spin Master, Funko, MGA Entertainment Inc, and VTech Holdings Limited |

|

Market Size in 2030 |

USD 161.86 Billion |

Key Analytical Observations Supporting the Above Data:

- The 5-to-10-years segment's 42.7% dominance in 2025 reflects strong demand for action figures, building sets, games, and STEM-learning products across developed and emerging markets.

- Specialty stores' 30.5% channel leadership reflects curated product ranges and knowledgeable in-store assistance, which remain preferred for considered toy purchases and gift occasions.

- Online stores are growing rapidly at ~8.5% CAGR through 2034, driven by e-commerce platforms such as Amazon, Flipkart, and dedicated toy retail websites offering broad SKU selection and convenience.

- North America's 39.9% global share is anchored by the United States - the world's largest individual toys market - where licensed merchandise, sports toys, and premium STEM products drive per-capita spending.

- Asia-Pacific at 28.5% reflects China's dominance as both the world's largest toy manufacturer and a rapidly growing consumer market, alongside India's rising middle-class household spending on children's education and play.

- The market in 2030 is estimated at USD 161.86 Billion, reflecting compounded annual expansion from the 2025 base of USD 121.04 Billion at a sustained 5.98% CAGR.

Global Toys Market Overview

Toys are play products designed to stimulate physical, cognitive, and social development across all childhood age groups. The global toys market encompasses a broad portfolio - including action figures, building sets, dolls, puzzles, STEM kits, sports and outdoor toys, plush items, and digitally integrated smart toys. Products are manufactured using materials such as plastic, wood, metal, fabric, and electronic components, serving consumers from infancy to adolescence and beyond.

The industry operates at the intersection of consumer spending trends, educational-value awareness, intellectual-property licensing, and retail channel evolution. Growth is supported by macroeconomic tailwinds such as rising disposable incomes in emerging markets, growing urbanization, and increased parental prioritization of toys industry products with developmental benefits. Simultaneously, the market is undergoing a structural shift toward smart, connected, and sustainable toys, driven by technology integration and evolving consumer values.

Market Dynamics

To evaluate market opportunities, Request Sample

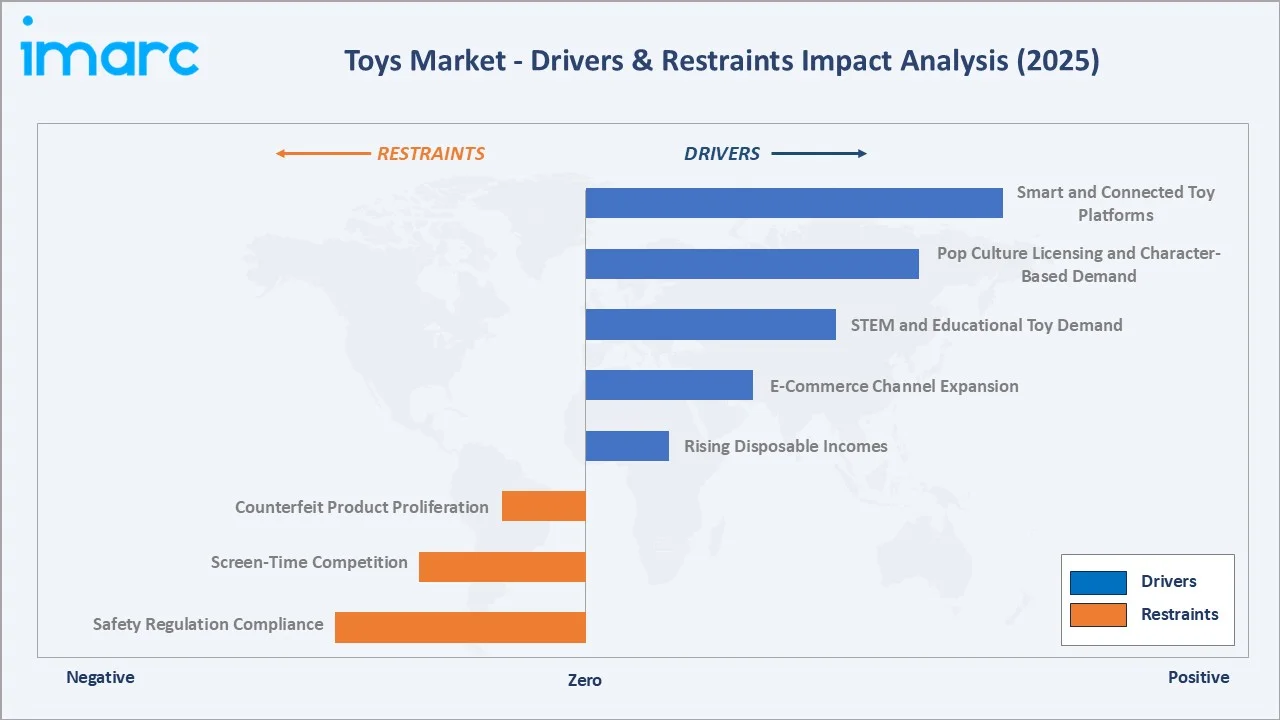

Market Drivers

- Rising Disposable Incomes: Growing household incomes - particularly in Asia-Pacific, Latin America, and the Middle East - are enabling families to allocate greater spending toward premium, licensed, and educational toys. The middle-class population in emerging markets is set to double over the next decade, expanding from 354 million households in 2024 to over 670 million households by 2035, directly expanding the addressable toys market.

- E-Commerce Channel Expansion: Rapid growth of digital retail platforms is broadening market access across underserved geographies. Online toy sales are growing at ~8.5% CAGR through 2034, as platforms offering wider SKU ranges, price comparison, and fast delivery displace traditional retail for routine toy purchases.

- STEM and Educational Toy Demand: Parental awareness of early developmental benefits is boosting demand for toys that promote learning. Educational toy categories - robotics kits, coding toys, and mathematics games - are among the fastest-growing segments, benefiting from government-backed STEM-in-education initiatives in the U.S., UK, India, and China.

- Pop Culture Licensing and Character-Based Demand: Box office franchises, streaming content, and social media influencers continuously generate demand for licensed merchandise. Major releases from Disney, Marvel, and major gaming studios drive multi-year product cycles for action figures, plush, and playsets tied to recognizable intellectual properties.

Market Restraints

- Safety Regulation Compliance: Stringent product safety standards - including ASTM F963 in the United States, EN 71 in Europe, and IS 9873 in India - impose significant compliance costs on toy manufacturers. Non-compliance risks product recalls, reputational damage, and market-access restrictions, particularly for smaller manufacturers.

- Screen-Time Competition: Increased time spent on smartphones, tablets, and gaming consoles is competing with traditional physical toy engagement, particularly among children aged 8 and above. This is moderating growth in non-digital toy categories for the Above-10-Years demographic.

- Counterfeit Product Proliferation: The global toy market faces persistent challenges from counterfeit products, particularly in emerging markets. Counterfeit toys undercut premium brand pricing and pose safety risks due to non-compliance with regulatory standards, affecting both revenue and consumer trust for established manufacturers.

Market Opportunities

- Smart and Connected Toy Platforms: IoT-enabled toys with app connectivity, AI-driven personalization, and augmented reality features represent a high-growth innovation frontier. Smart toy demand is expanding as parents seek engaging, technology-inclusive play products for digitally literate children, opening premium pricing opportunities.

- Emerging Market Penetration: India, Southeast Asia, and Africa represent under-penetrated markets with rapidly growing youth populations and rising consumer spending. India's toy imports and domestic manufacturing are expanding significantly, supported by the government's 'Make in India' initiative targeting toy production self-sufficiency.

- Sustainable and Eco-Friendly Toys: Growing consumer preference for environmentally responsible products is creating demand for toys made from recycled plastics, FSC-certified wood, and organic materials. Manufacturers adopting sustainable product lines are gaining brand differentiation in developed markets, were eco-labeling commands meaningful price premiums.

Market Challenges

- Raw Material and Supply Chain Volatility: Fluctuations in plastic resin, electronic component, and textile costs - combined with ongoing shipping cost variability - create margin pressure for toy manufacturers. The concentration of global toy manufacturing in China (80% of global production, 2021) creates supply chain concentration risk.

- Short Product Life Cycles: Toy trends driven by licensing deals, pop-culture cycles, and seasonal demand patterns create significant inventory management challenges. Products tied to specific IP releases can become obsolete rapidly, requiring manufacturers and retailers to manage markdown risks and overstocking effectively.

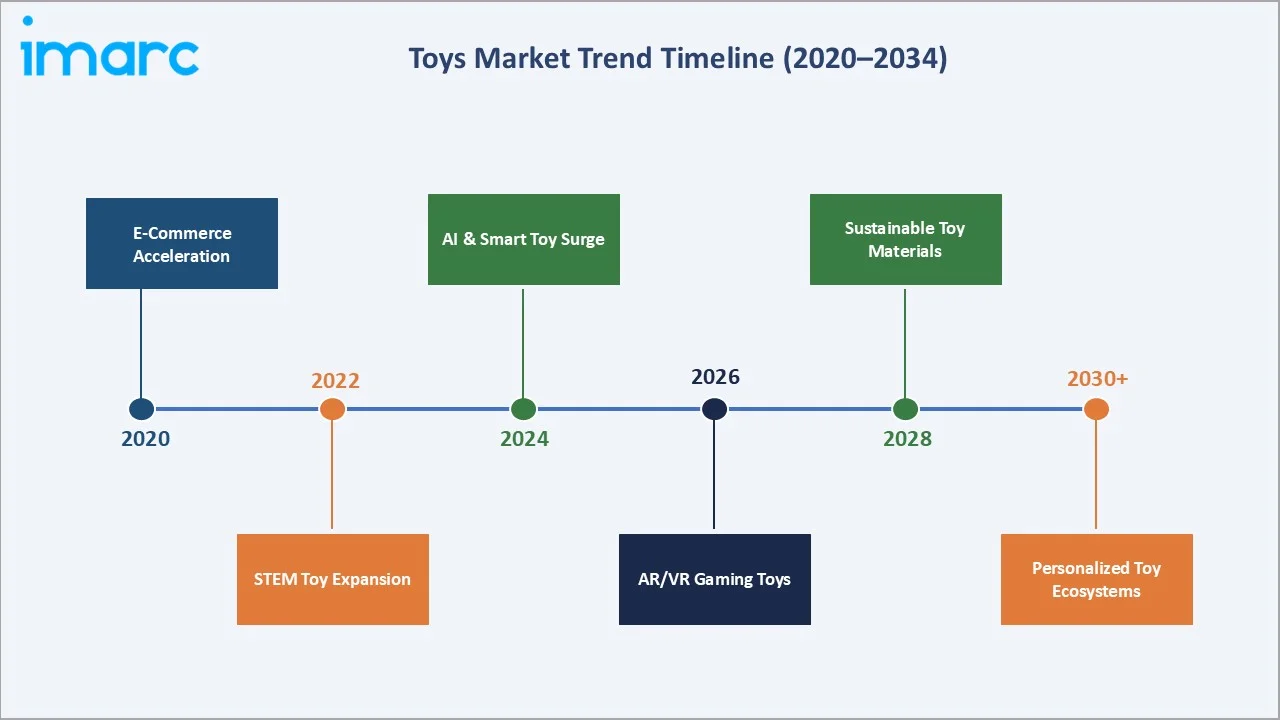

Emerging Market Trends

1. E-Commerce and Direct-to-Consumer Acceleration

Online toy sales are growing at approximately 8.5% CAGR through 2034, outpacing offline channels significantly. Home delivery convenience, subscription toy boxes, and platform algorithms recommending age-appropriate products are reshaping how parents discover and purchase toys globally.

2. STEM and Educational Toy Expansion

STEM-based toy categories - including robotics kits, coding games, and science experiment sets - are among the fastest-growing segments within the toys market. Government educational policies in the U.S., UK, and India are reinforcing school-adjacent demand for learning-focused play products in the 5-to-10-year demographic.

3. AI-Powered Smart and Interactive Toys

Artificial intelligence integration is enabling toys with personalized interaction, adaptive learning features, and voice-based engagement. Smart toy demand is expanding rapidly among premium consumer segments as parents seek engaging, technology-inclusive play options. AI-driven toy platforms represent a high-margin premium growth frontier through 2034.

4. Augmented Reality and Digital-Physical Convergence

AR-enabled toy sets, where physical figures interact with smartphone apps to create immersive digital experiences, are gaining traction across the 7-to-12-year demographic. This trend blurs the boundary between physical toys and gaming software, expanding average selling prices and consumer engagement duration.

5. Sustainable and Eco-Friendly Toy Manufacturing

Consumer demand for environmentally responsible products is structurally reshaping toy manufacturing inputs. Recycled plastics, FSC-certified wood, organic textiles, and biodegradable packaging are increasingly standard in premium product lines. Eco-certification is becoming a meaningful purchase factor in North America, Europe, and Australia through 2030.

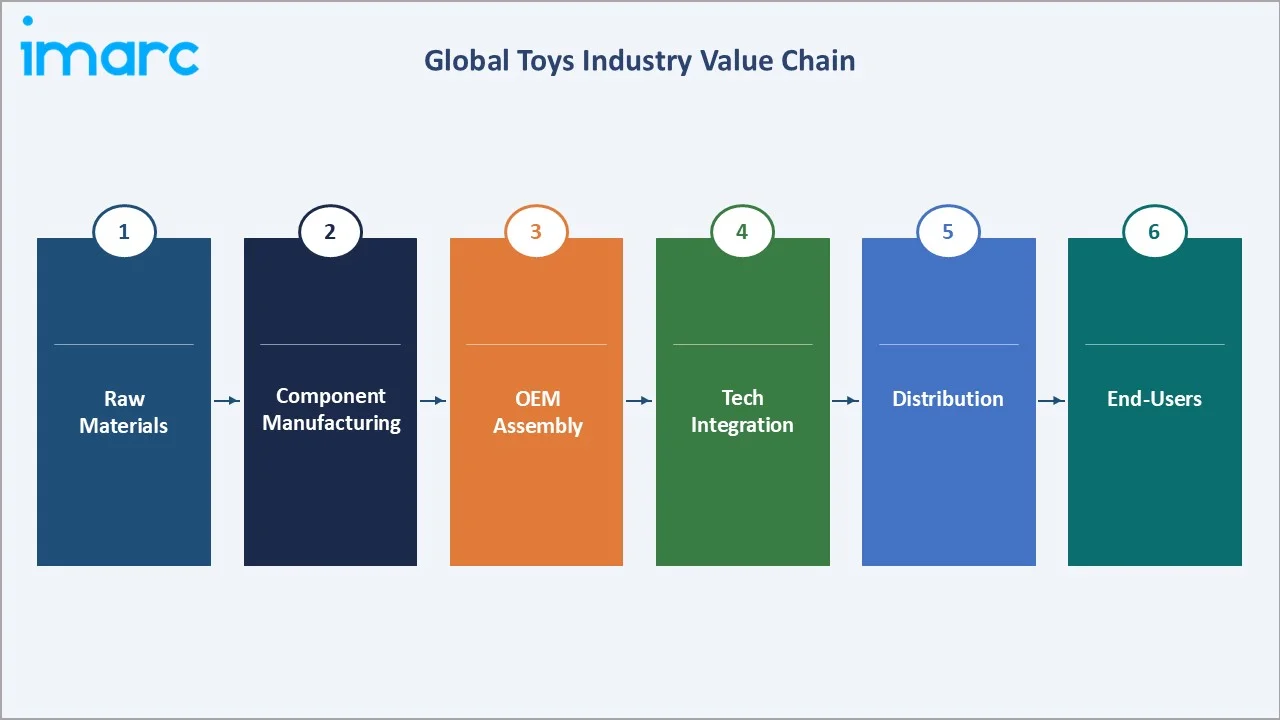

Industry Value Chain Analysis

The global toys industry value chain spans six integrated stages from raw material sourcing through end-consumer delivery. Each stage presents distinct competitive dynamics, cost structures, and innovation investment requirements relevant to the overall toys market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Plastic resins (ABS, PP, PS), textile fabrics, wood, metal components, electronic chips - sourced globally with manufacturing concentration in China, Vietnam, and India |

|

Component Manufacturing |

Injection-molded parts, electronic sub-assemblies, fabric components, and battery modules produced by Tier-2/Tier-3 suppliers across Asia |

|

OEM Manufacturing |

The LEGO Group, Mattel, Hasbro, Bandai Namco Holdings Inc - full product assembly, safety testing, and regulatory certification across major manufacturing hubs |

|

Technology Integration |

App-connected smart toy modules, AR platforms, AI-driven interactive features, IoT sensors, and voice-control components - growing segment integration |

|

Distribution Channels |

Specialty stores (30.5% share), online stores (28.2%), supermarkets & hypermarkets (22.3%), department stores (12.0%), others (7.0%) |

|

End Users |

Parents purchasing for children aged 0-15 years; gift buyers; institutional buyers for schools and daycare centres; collectors of premium licensed merchandise |

OEMs and brand owners hold the highest strategic value by integrating components, safety compliance, and brand IP into consumer-ready products. Meanwhile, e-commerce and direct-to-consumer channels are reshaping distribution dynamics, enabling manufacturers to bypass intermediaries and capture higher margins.

Technology Landscape in the Toys Industry

Smart and Connected Toy Technologies

Wi-Fi- and Bluetooth-enabled toys are transitioning from niche premium offerings to mainstream product features. Integration with smartphone apps enables interactive gameplay, progress tracking, and parental monitoring functions. Leading manufacturers including Mattel, Hasbro, and VTech are expanding connected toy portfolios across multiple age categories.

Artificial Intelligence and Adaptive Learning

AI-driven toys that adapt to a child's learning pace and preferences are gaining adoption in the educational toy segment. Natural language processing enables conversational interfaces, while machine learning algorithms personalize content delivery. This technology convergence is particularly relevant for the 4-to-8-year learning and development segment.

Augmented Reality and Gamification

AR features that overlay digital content onto physical toy play experiences are creating a new hybrid product category. Smartphone-based AR platforms require no additional hardware, enabling accessible integration at mid-price-tier products. Playsets incorporating AR story experiences represent one of the fastest-growing premium subcategories within the toys market trends landscape.

Sustainable Materials Innovation

Bio-based plastics, recycled polyethylene terephthalate (rPET), and FSC-certified wood materials are increasingly replacing virgin plastic in toy construction. Life-cycle assessments are becoming standard in product development processes for major manufacturers, particularly those operating in the European market where Ecodesign and Extended Producer Responsibility regulations are tightening.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Sports and Outdoor Toys | 21.9% | 2025 |

| Age Group | 5 to 10 Years | 42.7% | 2025 |

| Sales Channel | Specialty Stores | 30.5% | 2025 |

| Region | North America | 39.9% | 2025 |

By Age Group

To access detailed market analysis, Request Sample

The 5-to-10-years age group leads the global toys market with a 42.7% share in 2025. This segment is the core consumer cohort for action figures, building sets, STEM kits, games, and puzzles. The segment is projected to maintain dominance through 2034 as educational toy demand and licensed merchandise tied to entertainment franchises sustain consistent volume growth.

By Sales Channel

Specialty stores are the dominant distribution channel at 30.5% of global revenue in 2025. Dedicated toy retailers, specialty gaming stores, and educational toy boutiques provide curated assortments and expert staff guidance that drive considered purchase decisions, particularly for premium-tier and developmental toy categories.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.9% |

U.S. premium toy demand, licensed merchandise, STEM adoption, strong e-commerce penetration |

|

Asia-Pacific |

28.5% |

China consumer market growth, India rising incomes, Southeast Asia urbanization |

|

Europe |

20.2% |

Educational toy emphasis, sustainability regulations, strong specialty retail network |

|

Latin America |

7.2% |

Brazil/Mexico middle-class expansion, growing e-commerce, licensing demand |

|

Middle East & Africa |

4.2% |

UAE/Saudi Arabia retail expansion, rising youth population, premium toy adoption |

North America commands 39.9% global revenue share in 2025. The United States is the world's single largest toys market by consumer spending, driven by strong per-capita toy expenditure, deep licensing culture, and high adoption of premium educational and smart toy categories. The U.S. National Retail Federation recorded toy and game sales as a consistently top-performing holiday retail category, with 2024 holiday toy spending exceeding USD 30 Billion.

Competitive Landscape

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

The LEGO Group |

LEGO |

Leader |

Building sets innovation, licensing partnerships, digital integration |

|

Mattel |

Barbie, Hot Wheels, Fisher-Price |

Leader |

Diversified portfolio, global distribution, blockbuster IP licensing |

|

Hasbro |

Nerf, Monopoly, Transformers |

Leader |

Entertainment-linked brands, STEM toys, e-commerce strength |

|

Bandai Namco Holdings Inc |

Gundam, Tamagotchi, Kamen Rider |

Leader |

Japan/Asia dominance, collectibles, anime licensing |

|

Spin Master |

PAW Patrol, Bakugan |

Challenger |

IP creation, preschool market, North America strength |

|

Funko |

Pop |

Challenger |

Licensed collectibles, broad IP portfolio, adult collector targeting |

|

MGA Entertainment Inc |

L.O.L. Surprise!, Bratz |

Challenger |

Surprise unboxing trend, viral marketing, girls category leadership |

|

VTech Holdings Limited |

Vtech, LeapFrog |

Emerging |

Electronic learning toys, infant-toddler segment leadership |

The global toys market's competitive landscape is moderately fragmented, with global powerhouses competing alongside regional specialists and high-volume manufacturers. Leading players compete on IP ownership, product innovation, e-commerce capabilities, and safety certification.

Key Company Profiles

The Lego Group

The LEGO Group is a globally recognized toy manufacturing company headquartered in Billund, Denmark. Founded in 1932 by Ole Kirk Christiansen, it operates across construction toy, digital gaming, and entertainment sectors with a presence in over 130 countries.

- Product & Platform Portfolio: Lego's portfolio includes Classic, Technic, City, Star Wars, Harry Potter, Minecraft, and Ideas lines.

- Recent Developments: In 2026, The LEGO Group announced its new LEGO SMART Play platform, an interactive system that combines physical play with embedded technology to bring LEGO creations to life. The platform features smart bricks, tags, and minifigures that respond in real time with sounds and actions.

- Strategic Focus: Lego's strategy centers on IP licensing expansion, digital-physical convergence through gaming platforms, and manufacturing sustainability - targeting 100% sustainable materials across its product range by 2030.

Mattel

Mattel is a leading global toy and entertainment company headquartered in El Segundo, California. Founded in 1945, Mattel has grown into one of the world’s largest toy manufacturers, known for its iconic brands and expanding presence in content-driven entertainment.

- Product & Platform Portfolio: Mattel's portfolio includes Barbie, Hot Wheels, Fisher-Price, American Girl, Masters of the Universe, UNO, and Matchbox

- Recent Developments: In 2026, Mattel introduced its first autistic Barbie doll as part of its inclusive Fashionistas line, developed in collaboration with the Autistic Self Advocacy Network. The launch highlights the company’s focus on representation, featuring sensory-friendly design elements and accessories to better reflect neurodiverse experiences in children’s play.

- Strategic Focus: Mattel's strategy focuses on transforming its IP portfolio into a multi-franchise entertainment ecosystem, expanding direct-to-consumer digital commerce, and recovering Barbie brand momentum following record 2023-2024 film-driven sales cycles.

Hasbro

Hasbro is headquartered in Pawtucket, Rhode Island, USA. Founded in 1923, it is one of the world's largest entertainment and toy companies, operating across toys, games, and licensed merchandise through owned and partnership brands.

- Product & Platform Portfolio: Hasbro's portfolio includes Nerf, Monopoly, My Little Pony, Transformers, Play-Doh, Magic: The Gathering, and Dungeons & Dragons - serving broad age groups from preschool through adult collector segments.

- Recent Developments: In 2026, Hasbro showcased a wide range of new products and franchise expansions at Toy Fair 2026, highlighting key brands such as Transformers, Nerf, Monopoly, and Play-Doh. The company emphasized innovation through pop culture collaborations and new product launches, reinforcing its strategy to blend entertainment, licensing, and interactive play experiences to drive future growth.

- Strategic Focus: Hasbro's focus is on brand-led premium toy growth, expanding Magic: The Gathering and D&D as entertainment IP platforms, and building its Hasbro Pulse direct-to-consumer e-commerce channel for collector and enthusiast segments.

Market Concentration Analysis

The global toys market exhibits moderate fragmentation. The top five players - The LEGO Group, Mattel, Hasbro, Bandai Namco Holdings Inc, Spin Master - collectively account for approximately 25-32% of global market revenue in 2025.

The market is experiencing a bifurcated dynamic. At the premium OEM tier, consolidation is occurring around brand equity, IP portfolio depth, and e-commerce platform capabilities. Simultaneously, Chinese and Indian domestic manufacturers are generating competitive challengers that are increasingly targeting international markets with cost-competitive, design-improved products. This dynamic is intensifying competition across all price tiers through 2034.

Large toy conglomerates are actively managing portfolio complexity - Mattel's IP monetization strategy reflect a trend toward brand-focused, asset-light business models that prioritize core toy and licensing revenue streams over vertical entertainment integration.

Investment & Growth Opportunities

Fastest-Growing Segments

Online channel sales are the highest-growth distribution sub-segment at approximately 8.5% CAGR through 2034. Smart and AI-integrated toys represent the premium technology growth opportunity, expanding as connected home ecosystems achieve mainstream adoption among young families. The Above-10-Years demographic is emerging as a rapidly growing segment driven by collectibles, hobbyist models, and gaming-adjacent toy categories.

Emerging Market Expansion

India represents the highest-potential emerging market, driven by youth population (about 65% of its people under the age of 35), rising middle-class toy spending, and the government's Make in India initiative targeting domestic toy manufacturing expansion. Southeast Asia's rapidly urbanizing consumer markets, along with Sub-Saharan Africa's growing youth population and expanding modern retail infrastructure, collectively represent significant volume growth opportunities through 2034.

Venture and Strategic Investment Trends

Strategic investments are increasingly targeting AI toy platform developers, sustainable materials innovators, and direct-to-consumer toy subscription services. IP acquisition remains a key value-creation lever, as entertainment franchise integration (gaming, streaming) creates multi-year licensed merchandise demand cycles. E-commerce infrastructure investment - including AR product visualization tools and subscription personalization algorithms - is a primary capital allocation area for leading toy companies.

Future Market Outlook (2026-2034)

The global toys market forecast projects sustained value expansion from USD 121.04 Billion in 2025 to USD 207.46 Billion by 2034 at a CAGR of 5.98%. North America will retain regional leadership while Asia-Pacific accelerates structurally, narrowing the revenue gap through the forecast period.

Three key shifts will reshape the toys market through 2034. First, smart-toy convergence will embed AI and connectivity into mainstream mid-tier products, making interactive digital features standard across most age categories by 2028-2030. Second, sustainability mandates in North America and Europe will make recycled and bio-based materials a baseline expectation rather than a premium differentiator. Third, Chinese and Indian manufacturers are expected to reach global quality and design benchmarks, intensifying competition across all price tiers and geographies through the forecast horizon.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with toys industry stakeholders - including product directors at leading OEM manufacturers, category buyers at specialty and mass-market retail chains, institutional investors in consumer goods, and educators involved in STEM curriculum development. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include U.S. Census Bureau consumer spending data, NPD Group global toy sales reports, Toy Industry Association annual market data, Euromonitor International consumer goods databases, company annual reports, trade publications including Toy World Magazine, The Toy Book, and PlayBack magazine, and regional retail association databases across North America, Europe, and Asia-Pacific.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, birth-rate trends, urbanization indices, consumer spending indices, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty and supply chain variability.

Toys Market Research Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Action Figures, Building Sets, Dolls, Games and Puzzles, Sports and Outdoor Toys, Plush, Others |

| Age Groups Covered | Up to 5 Years, 5 to 10 Years, Above 10 Years |

| Sales Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Department Stores, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered |

The LEGO Group, Mattel, Hasbro, Bandai Namco Holdings Inc, Spin Master, Funko, MGA Entertainment Inc, VTech Holdings Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the toys market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global toys market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the toys industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Toys Market Report

The global toys market was valued at USD 121.04 Billion in 2025, driven by rising disposable incomes, e-commerce growth, and increasing parental spending on educational and premium play products worldwide.

The market is projected to reach USD 207.46 Billion by 2034, growing at a CAGR of 5.98% during 2034, supported by smart toy innovation, emerging market expansion, and sustained licensed merchandise demand.

Children aged 5 to 10 years lead with a 42.7% share in 2025, driven by strong demand for action figures, building sets, STEM kits, and games and puzzles within this core play-engagement age cohort.

Online stores are the fastest-growing distribution channel, expanding at approximately 8.5% CAGR through 2034, driven by e-commerce platform growth, product discovery algorithms, and consumer preference for home-delivery convenience.

North America dominates with a 39.9% share in 2025. The United States is the world's largest individual toy market by consumer spending, anchored by strong per-capita expenditure on licensed merchandise and educational products.

Key drivers include rising household incomes, e-commerce channel expansion, STEM education awareness, entertainment IP licensing cycles, pop culture demand for character-based toys, and increasing parental prioritization of developmental play products.

Major players include The LEGO Group, Mattel, Hasbro, Bandai Namco Holdings Inc, Spin Master, Funko, MGA Entertainment Inc, and VTech Holdings Limited.

AI-powered and app-connected smart toys are the fastest-growing technology segment. Interactive learning toys with adaptive AI features are gaining adoption, particularly in the 4-to-8-year developmental segment in North America and Europe.

Key opportunities include AI and smart toy platforms, sustainable toy manufacturing, India and Southeast Asia market expansion, direct-to-consumer online channels, and licensed merchandise tied to major entertainment IP releases from streaming and gaming platforms.

The market is segmented into specialty stores (30.5%), online stores (28.2%), supermarkets and hypermarkets (22.3%), department stores (12.0%), and others (7.0%), based on 2025 revenue share distribution.

E-commerce is reshaping the toys market industry by broadening geographic access, enabling price comparison, and supporting subscription-based toy delivery models. Online channels are projected to capture an increasing share of global toy sales through 2034 as digital retail infrastructure matures globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)