Indian Advertising Market Size, Share, Trends and Forecast by Segments and Region, 2026-2034

Indian Advertising Market Size, Share, Trends & Forecast (2026-2034)

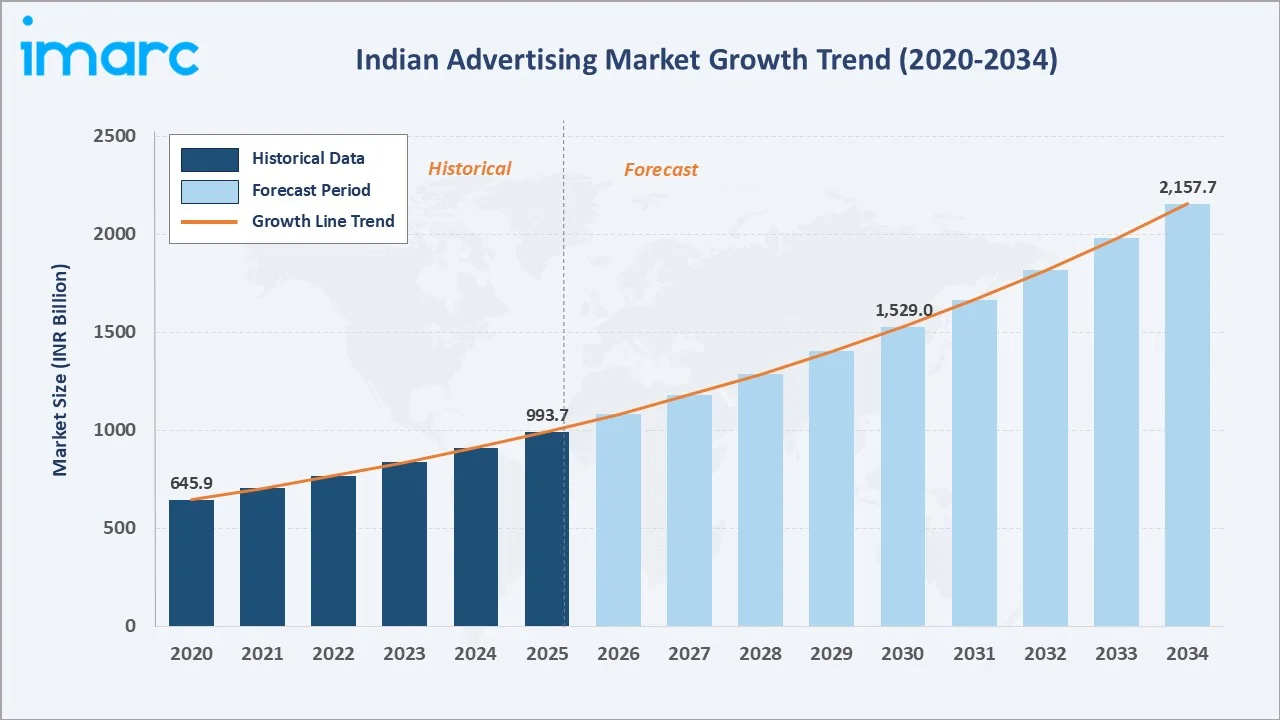

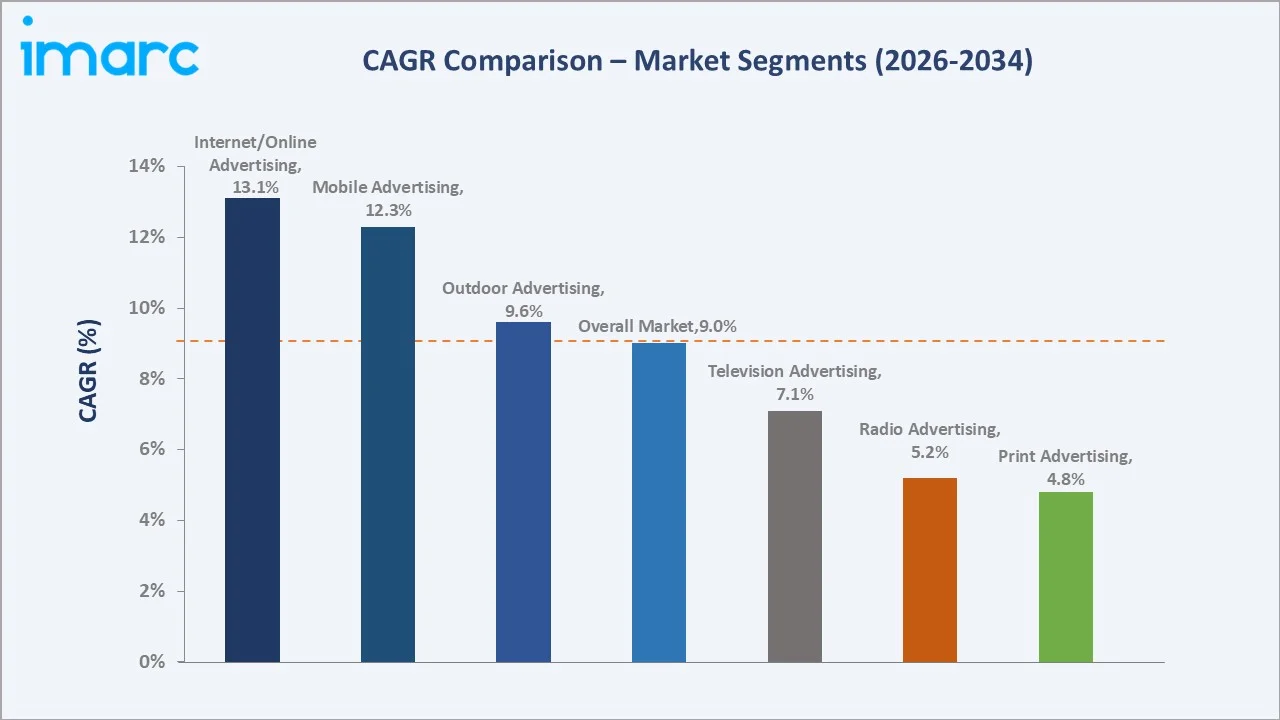

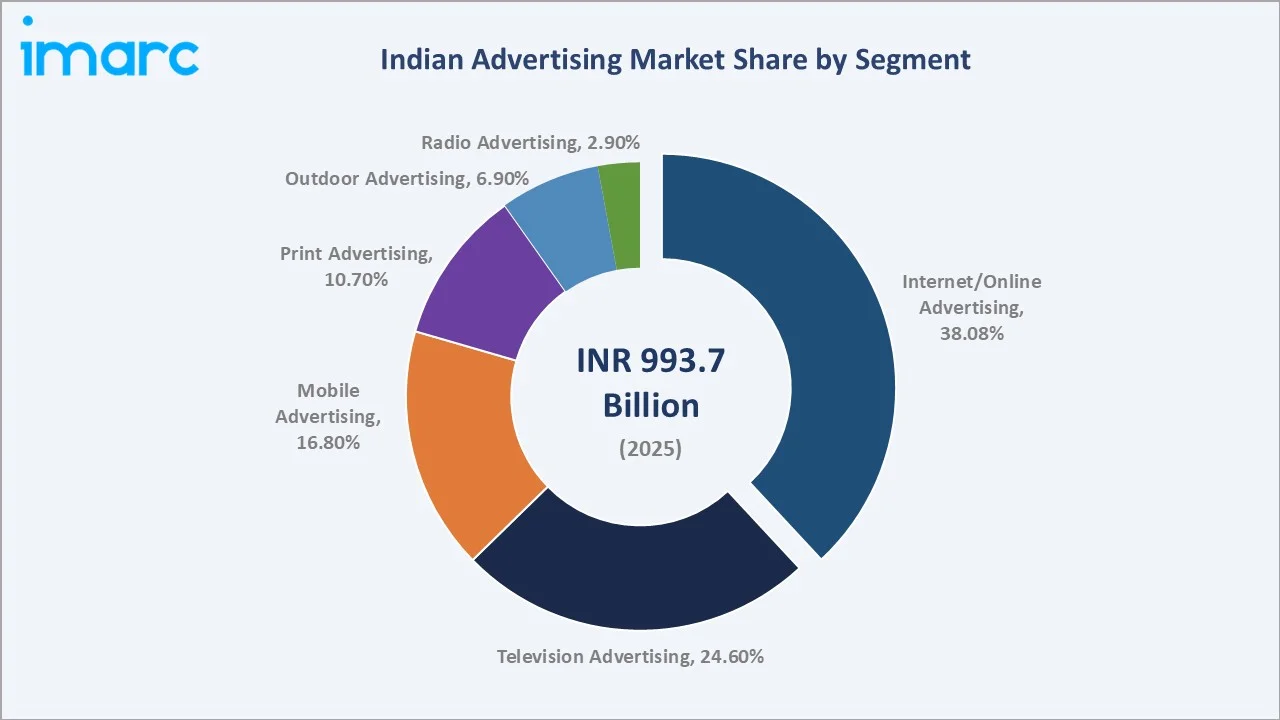

The Indian advertising market size was valued at INR 993.7 Billion in 2025 and is projected to reach INR 2,157.7 Billion by 2034, growing at a compound annual growth rate (CAGR) of 9.00% during 2026-2034. Rapid digital adoption, surging smartphone penetration, and the explosive growth of e-commerce platforms are driving robust expansion. Internet/Online Advertising dominates with a 38.08% share in 2025, reflecting the structural shift from traditional to digital channels.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

INR 993.7 billion |

|

Forecast Market Size (2034) |

INR 2,157.7 billion |

|

CAGR (2026-2034) |

9.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment |

Internet/Online Advertising (38.08%, 2025) |

|

Largest Region |

North India (28.0%, 2025) |

|

Fastest Growing Segment |

Internet/Online Advertising (~13.1% CAGR) |

|

Fastest Growing Region |

South India (Strong Digital Penetration) |

The chart below illustrates the Indian advertising market forecast trajectory from 2020 through 2034. Historical values (2020–2025) reflect compound expansion from INR 645.9 billion to INR 993.7 Billion, driven by digital adoption and rising advertiser spending

To get more information on this market, Request Sample

The forecast period (2026–2034) shows an accelerating growth curve supported by AI-driven ad technologies, programmatic adoption, and deeper penetration across emerging urban markets.

Executive Summary

The Indian advertising industry is undergoing a structural transformation, transitioning from traditional broadcast media toward data-driven digital ecosystems. The market was valued at INR 993.7 billion in 2025, up from INR 645.9 billion in 2020, representing consistent expansion driven by rising consumer internet engagement, mobile-first behavior, and brand budget reallocation toward digital platforms. This sustained Indian advertising market growth trajectory is anchored in strong macroeconomic fundamentals, India's youthful demographic, and accelerating 5G rollout enabling richer digital ad experiences.

Internet/Online Advertising commands the largest segment share at 38.08% in 2025, overtaking television as the dominant channel. Programmatic trading accounted for over 40% of digital ad spend in 2025. Mobile platforms command nearly 78% of digital advertising budgets, confirming the smartphone as the primary consumer touchpoint. The Indian advertising market outlook is further strengthened by the proliferation of OTT platforms, creator-led content, and AI-powered personalization tools that allow brands to deploy highly targeted, performance-driven campaigns at scale.

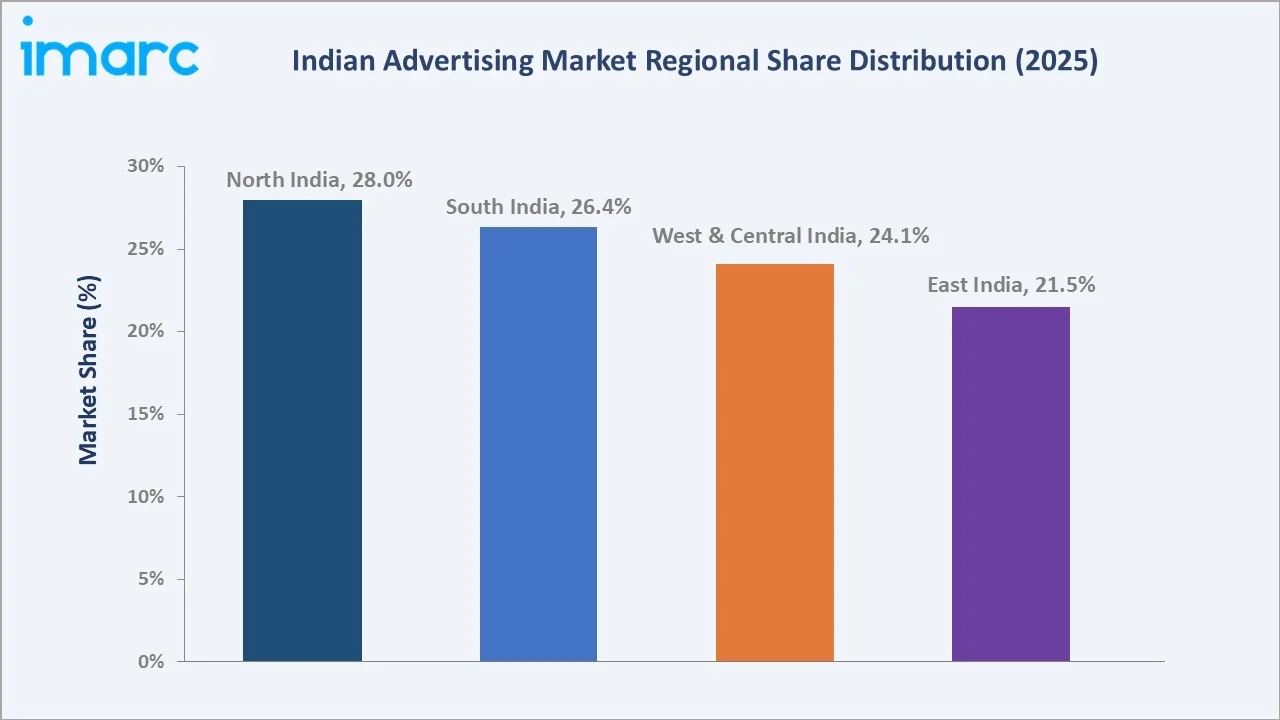

North India leads all regional markets with a 28.0% share in 2025, driven by concentration of corporate headquarters and extensive media infrastructure in Delhi NCR. South India follows at 26.4%, propelled by robust technology sector advertising and rapid digital adoption in major metros.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Internet/Online Advertising – 38.08% share (2025) |

|

Second Largest Segment |

Television Advertising – 24.60% share (2025) |

|

Fastest Growing Segment |

Internet/Online Advertising – ~13.1% CAGR (2026-2034) |

|

Leading Region |

North India – 28.0% revenue share (2025) |

|

Top Companies |

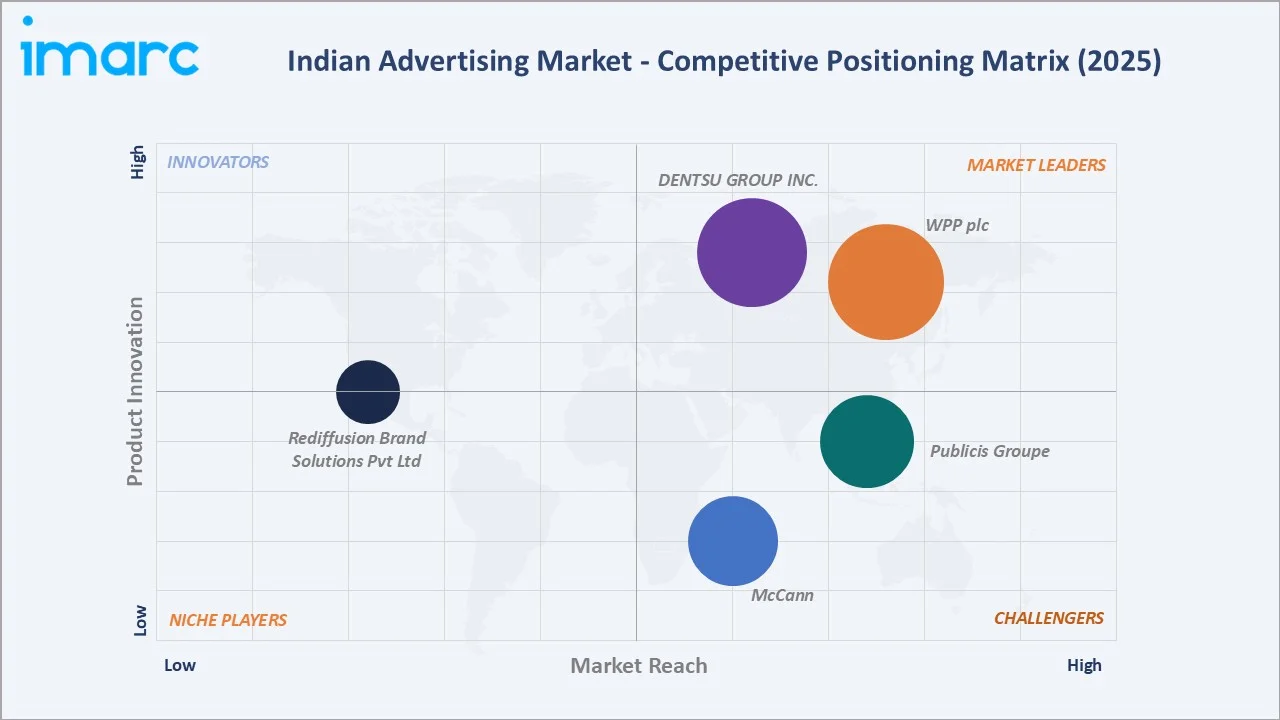

WPP plc, DENTSU GROUP INC., McCann, Publicis Groupe, Rediffusion Brand Solutions Pvt Ltd |

|

Market Opportunity |

India's internet user base |

Key Analytical Observations Supporting the Above Data:

- Internet/Online Advertising's 38.08% dominance in 2025 reflects a structural shift in media consumption, with digital advertising surpassing television as India’s largest advertising channel. Digital advertising has reached a historic milestone in scale, with mobile platforms accounting for the majority of digital ad budgets, underscoring the mobile-first nature of India’s digital ecosystem.

- Television Advertising holds a 24.6% share, retaining importance through marquee events including major sports leagues, national elections, and high-impact entertainment properties. Despite structural pressure from streaming platforms, television’s broad reach across rural India sustains its relevance for mass-market brands in FMCG, automotive, and consumer durables.

- Programmatic advertising contributed approximately INR 20,686 crore to total digital ad spending in India, representing a large portion of digital budgets. This automated approach enables real-time audience targeting and campaign optimization, making it the preferred methodology for performance-focused advertisers across e-commerce, fintech, and FMCG verticals.

- North India's 28.0% regional dominance reflects the concentration of major corporate subsidiaries, national broadcasters, and leading advertising agencies in the Delhi National Capital Region. The region benefits from high advertiser density, strong media infrastructure, and robust demand from government, FMCG, and technology-sector brands.

- India's advertising expenditure growth of 9.2% in 2025 exceeded the broader Asia-Pacific average, establishing the country as one of the fastest-growing major advertising markets globally. Retail media is a key growth driver in India through e-commerce and quick-commerce platforms.

Indian Advertising Market Overview

The Indian advertising market encompasses all paid forms of commercial communication designed to reach consumers across traditional and digital media channels. The ecosystem spans Internet/Online Advertising, Television, Mobile, Print, Outdoor/Out-of-Home (OOH), and Radio advertising, serving advertisers ranging from multinational FMCG companies to domestic startups and government entities. India's advertising-to-GDP ratio, while lower than mature markets like the United States.

The industry operates at the intersection of technology, media, and commerce. Macroeconomic drivers including India's nominal GDP growth of 10%+ annually, rising disposable incomes, the government's Digital India initiative expanding broadband connectivity, and the rapid scaling of domestic e-commerce ecosystems are collectively driving advertiser demand. India ranks ninth globally by advertising revenue as of 2025, ahead of Australia and positioned for continued rise. The Indian advertising industry analysis reveals accelerating convergence between performance marketing, content commerce, and AI-driven personalization.

Market Dynamics

To evaluate market opportunities, Request Sample

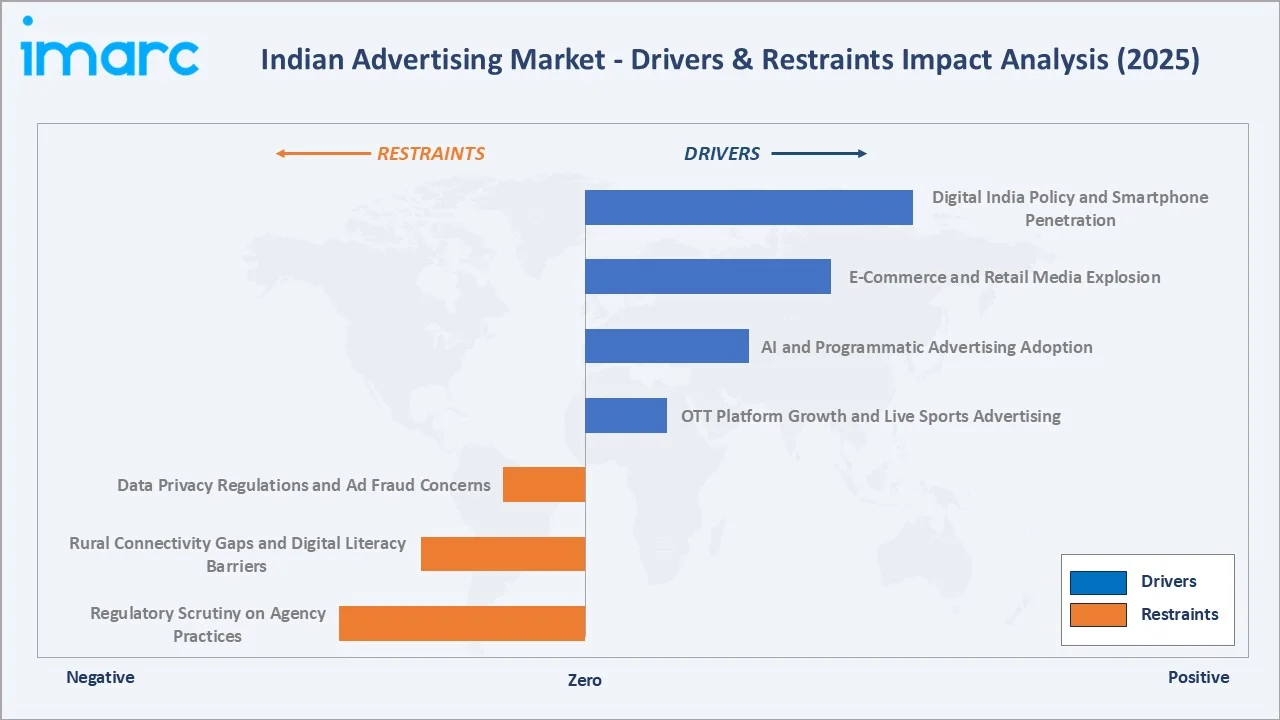

Market Drivers

- Digital India Policy and Smartphone Penetration: The Government of India’s Digital India initiative, combined with affordable data tariffs from telecom operators, has significantly increased internet penetration across the country. India’s 5G rollout, covering a wide network of districts across multiple states, has enabled faster mobile connectivity and supported richer advertising formats including video, augmented reality experiences, and live commerce. This infrastructure expansion is a key catalyst for growth in the Indian advertising market, particularly in Tier-II and Tier-III cities where advertiser spending was earlier constrained by connectivity limitations.

- E-Commerce and Retail Media Explosion: India's e-commerce market is projected to reach INR 345 billion by 2030, with platforms like Flipkart, Amazon India, Meesho, and Swiggy Instamart building powerful first-party data ecosystems. Indian retailers and quick-commerce platforms, including Amazon Now launched in December 2024 for 15-minute delivery, are creating vast, high-intent advertising inventory that brands can leverage for measurable, conversion-driven campaigns.

- AI and Programmatic Advertising Adoption: Programmatic trading accounted for a significant share of total digital ad spend in India, with AI-driven dynamic creative optimization, predictive audience targeting, and real-time bidding transforming campaign efficiency. Investments in AI and machine learning for advertising are expected to grow strongly, enabling hyper-personalized consumer experiences.

- OTT Platform Growth and Live Sports Advertising: India’s connected TV and OTT advertising market is expanding rapidly, with young adults more likely to choose OTT/CTV over social media platforms for premium content consumption. Live cricket advertising, particularly the Indian Premier League, generates substantial advertising revenue annually across both TV and digital streams. Brands advertising on OTT/CTV are perceived as significantly more premium by consumers compared to user-generated content platforms, making streaming a strategically important channel for brand building.

Market Restraints

- Data Privacy Regulations and Ad Fraud Concerns: India's Digital Personal Data Protection Act, 2023, and evolving regulatory frameworks governing data collection and targeting are creating compliance complexity for advertisers. Ad fraud, brand safety risks in user-generated content environments, and growing consumer adoption of ad-blocking software reduce effective reach and campaign measurement accuracy, challenging advertiser ROI expectations.

- Rural Connectivity Gaps and Digital Literacy Barriers: Despite significant progress, a large segment of the population still lacks reliable internet connectivity, limiting digital advertising reach in rural markets. Fragmented regional language requirements and varying levels of digital literacy across India’s diverse geography create operational complexity for national advertisers seeking uniform campaign reach.

- Regulatory Scrutiny on Agency Practices: The Competition Commission of India conducted raids on major global advertising agencies in March 2025, investigating alleged cartelization, price-fixing, and bid-rigging on commission and ad rates. This regulatory pressure is introducing compliance costs and potential penalties of up to 10% of global turnover, adding structural uncertainty to media buying operations.

Market Opportunities

- Vernacular and Regional Language Advertising: India's linguistic diversity, with 22 official languages and hundreds of regional dialects, represents a significant untapped opportunity. Brands that invest in localized vernacular content can reach audiences in states like Tamil Nadu, Maharashtra, West Bengal, and Telangana with far greater resonance than English-only campaigns. AI translation tools, including India's first Hindi AI design tool PixelYatra launched in May 2025, are reducing the cost barriers for multi-language content creation.

- Creator Economy and Influencer Marketing Scaling: India has a large base of active social media content creators, and influencer marketing is growing rapidly. Platforms including Instagram, YouTube, and Moj are building monetization ecosystems that enable brands to partner with nano, micro, and macro influencers for authentic and targeted campaigns. The education sector’s digital advertising has also grown significantly year-on-year, reflecting strong momentum in online learning promotion and student acquisition across platforms.

- Emerging Advertising Formats: Gaming advertising is emerging as one of the fastest-growing global content advertising channels, expanding rapidly as brands increase investment in interactive and immersive formats. India’s gaming user base is large and continues to expand, creating significant in-game and around-game advertising inventory. Additionally, connected TV, audio streaming, podcast advertising, and shoppable video formats represent nascent but fast-scaling channels within the evolving digital media ecosystem.

Market Challenges

- Attribution and Measurement Complexity: As consumer journeys span multiple devices, platforms, and channels, accurate attribution of advertising outcomes remains technically complex. The deprecation of third-party cookies and evolving identity solutions are requiring advertisers and agencies to rebuild measurement infrastructure around first-party data, contextual targeting, and privacy-preserving measurement methodologies.

- Agency Model Disruption from AI and Consulting Firms: Consultancies including Infosys, TCS, and Deloitte are positioning their AI capabilities to create campaigns, while technology platforms build their own creative tools. This convergence of tech, consulting, and advertising creates structural pressure on traditional creative agencies to demonstrate differentiated value beyond algorithmic execution.

Emerging Market Trends

1. Digital Dominance and Mobile-First Advertising

Digital advertising has emerged as India’s dominant channel, crossing a major milestone and surpassing television for the first time. Mobile platforms account for the majority of digital advertising budgets, driven by India’s large smartphone user base that consumes content across social media, OTT platforms, and messaging applications. This trend reflects a fundamental shift in consumer attention, pushing advertisers toward mobile-native formats such as short-form video, stories, and interactive ads. Indian advertising market trends indicate that this mobile-first shift will continue to intensify in the coming years as 5G penetration deepens and smartphone affordability improves.

2. AI-Powered Programmatic and Real-Time Bidding

Programmatic advertising accounts for a significant share of India’s digital ad spending, with AI-driven real-time bidding, dynamic creative optimization, and predictive audience modeling becoming standard tools for major advertisers. Generative AI is accelerating content production, enabling brands to quickly create and test multiple creative variants across demographic and regional segments. Retail media is emerging as a major driver of digital media spends, with strong growth momentum and increasing influence on incremental revenue compared to traditional channels like search and social. AI investment in advertising is expected to grow significantly in India in the near term, strengthening automation and personalization across the ecosystem.

3. Short-Form Video and Creator-Led Commerce

Short-form video advertising on platforms including Instagram Reels, YouTube Shorts, and Moj has become a fast-growing digital ad format in India, with brands shifting budgets from static display toward video-first strategies. Creator-led commerce, where influencers drive purchase decisions through shoppable content, is blurring the line between advertising and sales. India’s creator economy includes a large base of active content producers, and the influencer marketing segment is growing rapidly. This trend is accelerating as platforms expand creator monetization tools and brands increasingly seek authentic consumer engagement.

4. Connected TV (CTV) and OTT Premium Advertising

India’s OTT advertising market is experiencing rapid growth as platforms including JioCinema, Disney+ Hotstar, Netflix, and Amazon Prime Video expand their ad-supported offerings. Young Indian adults show a stronger preference for OTT/CTV over social media for premium content consumption, and brands advertising on these platforms are perceived as more premium compared to user-generated content environments. Live sports streaming, particularly cricket, represents a high-value advertising space due to its broad reach and strong audience engagement. The shift of premium advertising from linear television to streaming is emerging as a key structural transformation in India’s media ecosystem.

5. Vernacular Content and Regional Market Expansion

Advertising in regional Indian languages is growing faster than English-language digital advertising, as brands recognize the purchasing power and brand loyalty of non-metro consumers. The launch of AI-powered vernacular content tools is democratizing high-quality regional language content creation for brands of all sizes. Policy changes have also enabled digital platforms and OTT services to participate in government publicity campaigns, significantly expanding the addressable market for regional publishers. States including Uttar Pradesh, Maharashtra, Tamil Nadu, and Gujarat are emerging as key growth markets for regional advertising spend.

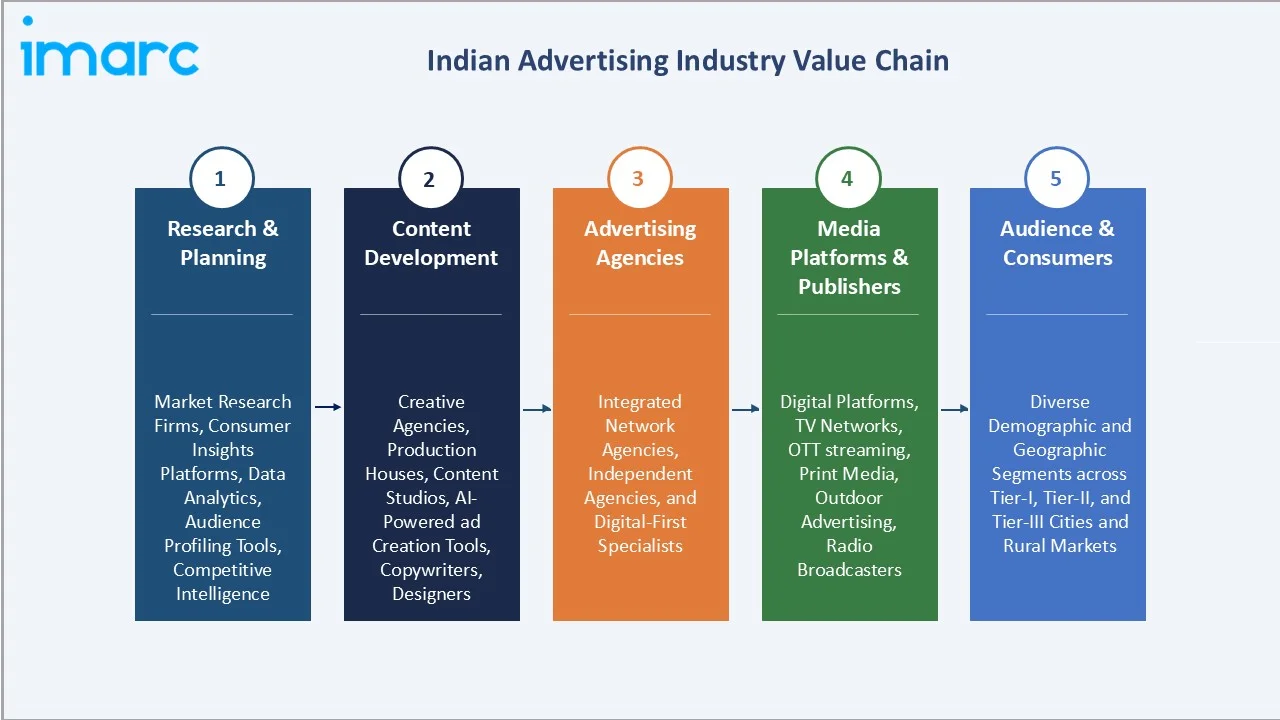

Industry Value Chain Analysis

The Indian advertising industry value chain spans five integrated stages, from initial market research and strategic planning through consumer audience engagement. Each stage presents distinct competitive dynamics, technology investment requirements, and value creation opportunities. The shift toward programmatic and data-driven advertising is reshaping value distribution across the chain, with technology platforms and data analytics providers capturing increasing margin share from traditional creative and media intermediaries.

|

Value Chain Stage |

Description |

|

Research & Planning |

Market research firms, brand strategy consultants, audience insight platforms. Consumer data analytics, competitive intelligence, and media planning inform campaign strategy and budget allocation across channels. |

|

Content Development |

Creative agencies, production houses, CGI studios, AI content generation platforms. Responsible for campaign ideation, scripting, visual design, film production, and multi-format creative adaptation for digital, TV, print, and OOH channels. |

|

Advertising Agencies |

Integrated network agencies, independent agencies, and digital-first specialists. Manage media planning, buying, programmatic execution, and performance analytics for advertiser clients. |

|

Media Platforms & Publishers |

Digital platforms television broadcasters, OTT services, print publishers, OOH network operators, and radio broadcasters. Provide advertising inventory, audience data, and measurement tools. |

|

Audience & Consumers |

Diverse demographic and geographic segments across Tier-I, Tier-II, and Tier-III cities and rural markets. Audience behavior data flows back to inform planning, completing the value chain cycle. |

Technology Landscape in the Indian Advertising Industry

Artificial Intelligence and Generative AI

AI has become the central technology reshaping India's advertising industry. Generative AI enables brands to produce multiple creative variants at scale, dramatically reducing production timelines and costs. Dynamic creative optimization (DCO) leverages AI to deliver personalized ad content in real time based on user behavior, device, location, and intent signals. Predictive analytics and machine learning-powered audience modeling allow advertisers to anticipate purchase behavior and optimize budget allocation across campaign lifecycle stages.

Programmatic Advertising and Ad Tech Infrastructure

India’s programmatic advertising ecosystem includes demand-side platforms (DSPs), supply-side platforms (SSPs), data management platforms (DMPs), and ad exchanges that automate media buying at scale. Programmatic advertising accounts for a significant share of total digital ad spend, with real-time bidding enabling precise audience targeting across large publisher networks and improving campaign efficiency.

Connected TV and Streaming Ad Technology

The rapid expansion of OTT and connected TV advertising requires advanced ad-serving technologies including server-side ad insertion (SSAI), addressable TV platforms, and live-stream monetization infrastructure. Major streaming platforms have demonstrated the ability to deliver large-scale live sports and entertainment events to massive audiences, showcasing India’s growing digital streaming capacity.

Measurement, Attribution, and Privacy Technology

As India's Digital Personal Data Protection Act creates new constraints on data usage, advertising measurement technology is evolving toward privacy-compliant methodologies. Multi-touch attribution models, media mix modeling (MMM), brand lift studies, and incrementality testing are increasingly used alongside traditional last-click attribution to provide holistic campaign effectiveness measurement. The Advertising Standards Council of India (ASCI) released an AI-ready regulatory roadmap in 2025 addressing generative content, deepfakes, synthetic influencers, and disclosure norms, positioning India among the first markets to proactively establish ethical AI advertising guardrails.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Internet Advertising | 38.08% | 2025 |

| Region | North India | 28.0% | 2025 |

By Segment

To access detailed market analysis, Request Sample

Internet/Online Advertising commands the largest share of the Indian advertising market at 38.08% in 2025, having surpassed television to become the dominant channel for the first time in fiscal year 2024–25. The segment encompasses search advertising, display and programmatic advertising, social media advertising, video advertising, content marketing, and native advertising formats.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Markets |

|

North India |

28.0% |

Corporate headquarters concentration, NCR media hub, strong FMCG and government advertising |

Delhi NCR, Uttar Pradesh, Punjab, Haryana, Rajasthan |

|

South India |

26.4% |

Technology sector advertising, digital adoption, FMCG demand, e-commerce penetration |

Bengaluru, Chennai, Hyderabad, Kerala, Tamil Nadu |

|

West & Central India |

24.1% |

Mumbai as financial and entertainment capital, FMCG brands, entertainment industry advertising |

Mumbai, Pune, Ahmedabad, Surat, Indore |

|

East India |

21.5% |

Rising digital penetration, vernacular language content demand, FMCG and retail growth |

Kolkata, Patna, Bhubaneswar, Guwahati, Jharkhand |

North India (28.0%)

North India accounts for 28.0% of India's total advertising market in 2025, maintaining its leadership position driven by the Delhi National Capital Region's concentration of corporate headquarters, government ministries, and national advertising agency offices. The rapid growth of e-commerce platforms serving Uttar Pradesh, Rajasthan, and Haryana is driving performance marketing investment in the region.

Competitive Landscape

|

Company |

Brand / Network |

Market Position |

|

WPP plc |

EssenceMediacom, Mindshare, Wavemaker |

Leader – Largest media group, ~18.5% estimated share |

|

DENTSU GROUP INC. |

Dentsu Creative, Carat, iProspect |

Leader – Digital-first, strong programmatic capabilities |

|

McCann |

McCann Worldgroup India |

Challenger – Strong FMCG and B2C client base |

|

Publicis Groupe |

Leo |

Challenger – Purpose-led creative approach |

|

Rediffusion Brand Solutions Pvt Ltd |

Rediffusion |

Emerging – India's largest independent full-service agency |

The Indian advertising market is characterized by a competitive landscape dominated by global holding company networks alongside strong independent players and emerging digital-native agencies.

Key Company Profiles

DENTSU GROUP INC

Dentsu Group Inc. is a leading global advertising and marketing services holding company headquartered in Tokyo, with a legacy dating back to 1901. The group operates across approximately 120 countries with a around 67,000 employees, positioning it among the top global agency networks by revenue.

- Product & Service Portfolio: Creative marketing, digital advertising, social media marketing, performance marketing, media planning and buying, content strategy, market research, programmatic advertising, and data analytics. Dentsu India operates multiple specialist brands including dentsu X, iProspect, Isobar, and others.

- Recent Developments: In 2026, Dentsu Group Inc has launched the 10th edition of its Digital Advertising Report titled “Next 10: Forces Shaping the Next Decade of Indian Media. The report highlights a shift in India’s media landscape from scale-driven growth to strategic maturity, where attention, trust, and outcomes are becoming key success factors.

- Strategic Focus: Dentsu India's strategic focus centers on building tech-enabled, data-driven marketing platforms that integrate creative, media, and digital capabilities. The agency is investing in AI-powered media planning tools, first-party data solutions, and integrated measurement frameworks to help clients navigate the digital advertising ecosystem's increasing complexity.

Publicis Groupe

Leo, a brand under Publicis Groupe, is a globally recognized advertising and communications agency founded in 1935. The agency has a strong international footprint with over 96 offices across nearly 85 countries and a workforce exceeding 9,000 employees.

- Product & Service Portfolio: Brand strategy, integrated advertising, digital marketing, content creation, social media, experiential marketing, performance marketing, and data-driven campaign management across mass market and premium brand categories.

- Recent Developments: Publicis Groupe's Leo is strengthening its creative strategy through a HI x AI (Human Intelligence × Artificial Intelligence) approach. The model combines human insight, creativity, and storytelling with AI, data, and technology to enhance campaign effectiveness and innovation.

- Strategic Focus: Publicis Groupe's Leo India's strategic focus is on creating culturally resonant, purpose-driven campaigns that demonstrate measurable business impact. The integration into the unified Leo network is accelerating AI-powered creative production capabilities and shared data infrastructure.

McCann

McCann is one of the world's most globally integrated marketing networks, bringing together advertising, digital, social media, direct marketing, public relations, and specialty services. McCann India has a strong track record of creating impactful campaigns for major multinational brands across FMCG, technology, financial services, and consumer goods categories.

- Product & Service Portfolio: Integrated marketing communications, creative strategy, digital advertising, performance marketing, McCann Health, MRM (data and CRM), and experiential services through a unified multi-disciplinary model.

- Recent Developments: In 2025, McCann Worldgroup India has won the creative mandate for Smart Bazaar, strengthening its position in India’s retail advertising space. As part of the mandate, McCann conceptualised and launched a new brand campaign built around the cultural shift from “making do” to living well.

- Strategic Focus: McCann India's strategic focus centers on the belief that "truth well told" drives brand effectiveness. The agency is investing in integrated data and analytics capabilities, performance measurement frameworks, and AI-assisted creative production to maintain leadership in creative effectiveness while growing its digital and performance marketing revenue streams.

Market Concentration Analysis

The Indian advertising market exhibits moderate-to-high concentration at the holding company level, with the top five global agency groups – WPP plc, DENTSU GROUP INC., McCann, Leo Burnett, Rediffusion Brand Solutions Pvt Ltd – controlling an estimated 65–70% of organized advertising agency revenues in India.

Despite holding-company concentration, the broader Indian advertising market remains fragmented across thousands of small and mid-sized independent agencies, digital marketing firms, performance marketing specialists, and emerging AI-native creative shops.

India’s advertising and marketing services landscape includes a large number of agencies spanning the full spectrum from boutique creative studios to large integrated networks. The digital advertising segment is particularly fragmented, with numerous agencies competing for performance marketing mandates from D2C brands, startups, and mid-market companies.

Consolidation trends are expected to continue through 2034, driven by client demand for integrated, data-driven agencies capable of managing complex multi-channel campaigns, and the economies of scale in AI and technology investment that favor larger entities. However, market observers note that consolidation carries the risk of reducing creative diversity and agility, potentially creating space for independent challenger agencies that can offer more innovative approaches and undivided senior leadership attention to emerging advertisers.

Investment & Growth Opportunities

Fastest Growing Segments

- Internet/Online and Mobile Advertising: With strong projected growth rates through the next decade, digital segments offer the highest growth potential within the advertising market. Programmatic technology, retail media networks, and AI-powered personalization are enhancing advertising effectiveness and attracting increasing brand investment.

- Retail Media Networks: India’s e-commerce and quick-commerce platforms are building high-margin advertising businesses by leveraging first-party purchase data. This segment mirrors global trends where retail media has emerged as a major revenue stream, creating strong opportunities for investment in ad tech infrastructure and data monetization platforms.

- Connected TV and OTT Advertising: As streaming platform subscriber bases expand and ad-supported tiers grow, CTV advertising is transitioning from a premium niche to a mainstream channel. Investment in streaming ad technology, live sports rights, and creator content infrastructure offers high-return opportunities.

Emerging Market Opportunities

- Tier-II and Tier-III City Expansion: India’s large base of non-metro internet users represents a massive, underserved advertising market. Brands that invest in vernacular content, regional language campaigns, and mobile-optimized ad experiences for smaller cities can capture significant share as digital penetration continues to deepen.

- AI and Ad Tech Infrastructure: India’s advertising technology ecosystem remains underdeveloped relative to its market size. Investment in domestic DSP, DMP, and measurement platforms, along with AI-powered creative generation tools tailored for Indian languages and cultural contexts, offers significant returns as the country’s advertising market continues to scale in the coming years.

- Gaming and Immersive Advertising: India’s large gaming user base represents one of the world’s biggest gaming audiences. In-game advertising, AR ad experiences, and gaming platform sponsorships are still in early stages of commercial development, representing a high-growth opportunity as ad monetization infrastructure continues to mature.

Venture and Strategic Investment Trends

Indian advertising technology and digital media companies attracted significant venture capital and strategic investment in 2025. AI-native creative platforms, influencer marketing marketplaces, regional language content networks, and retail media technology firms are among the most active investment categories. Global advertising holding companies are acquiring Indian digital agencies and technology firms to strengthen AI capabilities and data infrastructure. Government-backed Digital India initiatives are indirectly supporting advertising market growth by funding broadband infrastructure, digital payments, and e-government services that expand the advertising addressable market.

Future Market Outlook (2026-2034)

The Indian advertising market forecast through 2034 points to INR 2,157.7 billion, representing a sustained CAGR of 9.00% from the 2025 base of INR 993.7 billion. By 2030, the market is expected to reach INR 1,529.0 billion, reflecting the sustained compound impact of digital adoption, rising consumer spending, and advertiser budget expansion.

The structural shift from traditional to digital advertising will accelerate through the forecast period. Internet/Online Advertising is projected to command over 50% of total advertising expenditure by 2030 as mobile internet penetration approaches saturation in urban markets and deepens in rural areas. Television advertising will maintain relevance through live sports and premium content, but its share is expected to decline steadily as OTT and CTV platforms capture increasing fractions of total video viewing time. Print advertising will continue to stabilize in regional language markets while declining in metro English-language segments. Outdoor advertising will be transformed by digital OOH technology, enabling data-driven, programmatic outdoor campaigns that compete for digital-era budgets.

Technological disruptions will reshape how advertising is created, distributed, and measured. AI will automate substantial portions of creative production, media planning, and campaign optimization, requiring agencies to restructure operations and build new competencies. The convergence of advertising, commerce, and entertainment through shoppable content, live commerce, and interactive video will blur traditional channel boundaries. India's regulatory environment will evolve alongside global privacy frameworks, necessitating investment in privacy-preserving advertising methodologies. The overall Indian advertising market outlook remains robustly positive, supported by India's demographic dividend, rising urbanization, expanding middle class, and deepening integration of digital technology across all aspects of economic and social life.

Research Methodology

Primary Research

IMARC Group's primary research for the Indian advertising market report encompasses in-depth interviews with senior executives at advertising agencies, brand marketers, media platform representatives, technology vendors, and industry associations. Key informants include Chief Marketing Officers, Chief Media Officers, agency CEOs and Managing Directors, and digital marketing heads at leading Indian and multinational brands. Primary data collection also includes structured surveys with media planners, programmatic buyers, and creative directors to capture granular operational insights on channel allocation, technology adoption, and emerging advertising strategies.

Secondary Research

Secondary research sources include government databases including the Ministry of Information & Broadcasting, the Telecom Regulatory Authority of India (TRAI), and the Competition Commission of India. Industry association publications from the Advertising Agencies Association of India (AAAI), the Indian Society of Advertisers (ISA), and the Internet and Mobile Association of India (IAMAI) provide sector-level data. Research builds on reports from dentsu-e4m, FICCI-EY, PitchMadison, WPP Media's TYNY report, Bain & Company, and other credible industry intelligence sources. Financial filings and announcements from publicly listed advertising and media companies supplement agency-level market sizing.

Forecasting Methodology

Market forecasts are generated using a combination of bottom-up and top-down approaches. Bottom-up methodology aggregates segment-level advertising expenditure projections across Internet/Online, Television, Mobile, Print, Outdoor, and Radio channels, informed by channel-specific growth drivers, historical CAGR analysis, and primary research insights on advertiser budget plans. Top-down methodology cross-validates projections against India's nominal GDP growth trajectory, advertising-to-GDP ratio benchmarks, and comparable emerging market advertising market trajectories. CAGR projections are stress-tested under multiple macroeconomic scenarios to produce robust central-case forecasts.

Indian Advertising Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion |

| Scope of the Report Covered |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Television Advertising, Print Advertising, Newspaper Magazines, Radio Advertising, Internet/Online Advertising, Mobile Advertising, Outdoor Advertising Billboards, Street Furniture, Transit Advertising, Other Mediums. |

| Region Covered | North India, South India, West and Central India, East India |

| Companies Covered | WPP plc, DENTSU GROUP INC., McCann, Publicis Groupe, Rediffusion Brand Solutions Pvt Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Advertising Market Report

The Indian advertising market was valued at INR 993.7 billion in 2025, making it the ninth-largest advertising market globally by revenue, according to WPP Media's year-end 2025 global forecast.

The Indian advertising market is projected to exhibit a CAGR of 9.00% during 2026-2034, reaching INR 2,157.7 billion by 2034. An interim milestone of INR 1,529.0 billion is projected by 2030.

Key drivers include rapid digital adoption, accelerating smartphone penetration, AI-powered programmatic advertising, explosive e-commerce and retail media growth, OTT platform expansion, and the Government of India's Digital India policy creating digital infrastructure tailwinds.

Internet/Online Advertising dominates the Indian advertising market with a 38.08% share in 2025, having surpassed television as the largest channel for the first time in fiscal year 2024–25. Mobile platforms account for nearly 78% of digital advertising budgets.

North India leads the Indian advertising market with a 28.0% share in 2025, driven by the concentration of corporate headquarters, government advertising budgets, and national agency offices in the Delhi National Capital Region.

AI is reshaping content creation, media planning, measurement, and consumer engagement. Brands are deploying generative AI for dynamic creative optimization, predictive audience modeling, and campaign automation.

Key players include WPP plc, DENTSU GROUP INC., McCann, Publicis Groupe, and Rediffusion Brand Solutions Pvt Ltd.

The Indian advertising market is projected to grow at a CAGR of 9.00% during the forecast period 2026–2034, driven by digital adoption, programmatic growth, mobile-first consumer behavior, and expanding advertiser base in Tier-II and Tier-III cities.

Key trends include digital surpassing traditional media, mobile-first programmatic advertising growth, creator economy and influencer marketing expansion, OTT and CTV advertising growth, and vernacular content driving regional market development.

The market is segmented into Internet/Online Advertising (38.08%), Television Advertising (24.6%), Mobile Advertising (16.8%), Print Advertising (10.7%), Outdoor Advertising (6.9%), and Radio Advertising (2.9%) as of 2025.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)