Xerostomia (Dry Mouth Disease) Therapeutics Market Size, Share, Trends and Forecast by Type, Drug Type, Distribution Channel, and Region, 2025-2033

Xerostomia (Dry Mouth Disease) Therapeutics Market Size and Share:

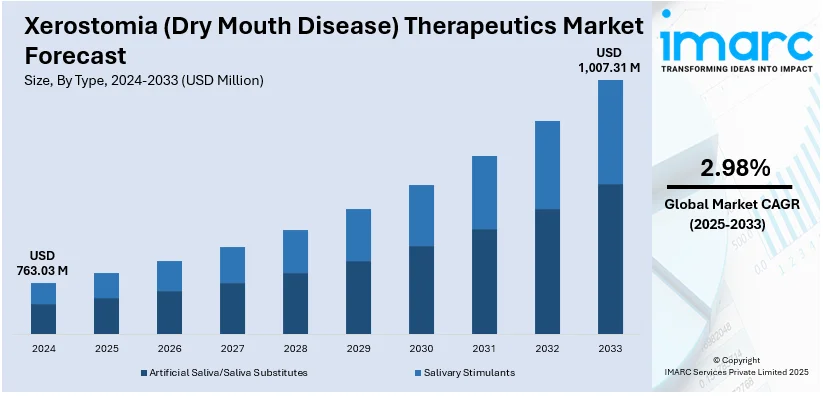

The global xerostomia (dry mouth disease) therapeutics market size was valued at USD 763.03 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 1,007.31 Million by 2033, exhibiting a CAGR of 2.98% from 2025-2033. North America currently dominates the market, holding a market share of over 36.8% in 2024, attributed to a well-established healthcare system, increased disease understanding, and growing incidence of dry mouth due to the elderly population and medications.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 763.03 Million |

|

Market Forecast in 2033

|

USD 1,007.31 Million |

| Market Growth Rate (2025-2033) | 2.98% |

The xerostomia (dry mouth disease) therapeutics market expands due to rising incidence of dry mouth conditions, involving Sjogren’s syndrome, diabetes, and radiation therapy for cancer patients. The effective treatment demand is witnessing a notable increase with lung cancer and an aging population. Additionally, healthcare professionals alongside patients are increasingly aware of dry mouth disease which drives their pursuit of therapeutic solutions. Moreover, improved drug formulations, including secretagogues and saliva substitutes, profilerating the market forward as these new formulations provide better effectiveness and comfort to patients. Technological advances in drug delivery systems with emphasis on personalized medicine also contribute to the market's growth.

In the United States, the xerostomia therapeutics market is growing with a high incidence of risk factors like aging, diabetes, and cancer therapy, especially head and neck radiation. The increasing use of targeted therapies and technological advancements in over-the-counter products are offering increased treatment choices for patients. For instance, as per industry reports, researchers from University of Wisconsin School of Medicine Public Health, in partnership with PACT, is performing a clinical trial to explore the potential of using a patient’s own enhanced stem cells to improve salivary gland function in Sjogren’s disease. This innovative approach involves extracting stem cells from the patient’s bone marrow, activating them, and injecting them into the salivary glands. Furthermore, as the understanding of xerostomia’s impact on health continues to evolve, demand for effective and accessible treatments in the U.S. is expected to rise steadily.

Xerostomia (Dry Mouth Disease) Therapeutics Market Trends:

Advancements in Salivary Stimulant Formulations

The xerostomia therapeutics market has some of the most significant advancements in the formulation of salivary stimulants. The demand for prolonged and effective treatment is, however, driving these changes. Most of the classical saliva substitutes provide only temporary relief, forcing researchers to seek newer or innovative drug delivery methods like mucoadhesive formulations, sustained-release gels, and nanoparticle-based therapies. Companies have also turned their attention to plant-derived compounds or regenerative medicine approaches to stimulate rather than replace this natural saliva production capability. Biologics are being developed targeting salivary gland function, like growth factors and gene therapy, that might offer some long-term benefits. This development improves patient compliance and the efficacy of the treatment through improved moisture retention and decreased frequency of reapplication. Prescription-based formulations with enhanced bioavailability further add to the market's growth. With over 30% of individuals aged 65 and older experiencing dry mouth, there is a growing need for innovative solutions that improve patient compliance and offer sustained relief, a research article stated. As a consequence, the industry is moving away from symptomatic relief products towards therapeutic interventions targeting the cause of dry mouth. This will ensure better patient outcomes.

Growing Adoption of Prescription Therapies Over OTC Products

The market of xerostomia therapeutics is moving away from OTC dry mouth relief products to more prescription-based drugs based on the increasing awareness within the healthcare professional community and the patients' concern for complete long-term management. While OTC products such as artificial saliva sprays, lozenges, or mouth rinses provide mere symptom relief, it does not take into account the root causes of the dryness. On the other hand, prescription medications such as pilocarpine and cevimeline, muscarinic receptor agonists stimulate salivary gland function to produce long-lasting effects. In addition, promising drug candidates for clinical development involve enhancement of saliva flow and glandular regeneration that positions prescription treatments as a more viable option. The healthcare provider has increasingly become recommending prescription treatments to patients who suffer from chronic xerostomia secondary to Sjögren's syndrome, radiation therapy, or polypharmacy-induced dryness. This shift is expected to fuel market growth as pharmaceutical companies continue investing in the development of targeted treatments with improved efficacy and safety profiles. Studies suggest that up to 73.4% of patients undergoing chemotherapy report experiencing xerostomia, with the prevalence rising to 90% among those receiving radiation therapy for head and neck cancers. This trend is driving the adoption of prescription-based treatments targeting the underlying pathology.

Rising Prevalence of Xerostomia Due to Chronic Diseases and Medications

The principal reason for the rising rate of xerostomia cases is the increased number of chronic diseases and side effects from medication. Diseases like diabetes, Sjögren's syndrome, and other autoimmune diseases have a direct impact on salivary glands, causing symptoms of xerostomia to be felt for long durations. Similarly, cancer treatments through radiation therapy and chemotherapy often damage salivary glands, thereby resulting in xerostomia as a common side effect in cancer patients. Studies indicate that xerostomia affects 13-17% of the general population, with prevalence rates rising to 30-40% among the elderly due to polypharmacy. The widespread use of medications such as antihypertensives, antidepressants, and opioids further contributes to the rising number of cases, with over 400 commonly prescribed drugs known to cause dry mouth as a side effect. Demand for effective remedies against xerostomia will increase among the aging globe and the constantly growing burden of chronic diseases. As such, pharmaceutical companies are coming forward with the drugs that can offer symptomatic relief and address the underlying cause of dry mouth. The rising number of patients, thus, represents an important area for innovation and growth in the xerostomia therapeutics market.

Xerostomia (Dry Mouth Disease) Therapeutics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global xerostomia (dry mouth disease) therapeutics market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on type, drug type, and distribution channel.

Analysis by Type:

- Artificial Saliva/Saliva Substitutes

- Salivary Stimulants

Artificial saliva/saliva substitutes lead the market with around 65.7% of market share in 2024. due These products provide moisture, lubrication, and relief from dry mouth symptoms, improving patients' comfort and quality of life. Available in various forms, such as sprays, gels, and lozenges, artificial saliva products help alleviate discomfort caused by conditions like Sjögren's syndrome or medication-induced xerostomia. Their widespread use in both clinical settings and over-the-counter offerings, along with ongoing advancements in formulation, continues to drive demand, positioning them as a key treatment option for dry mouth management.

Analysis by Drug Type:

- OTC

- Prescription

OTC leads the market in 2024, driven by consumer preference for easily accessible, non-prescription solutions. OTC treatments, including mouthwashes, lozenges, gels, and sprays, offer immediate relief from dry mouth symptoms and are widely available in pharmacies and online. The growing trend of self-management and the increasing awareness of xerostomia contribute to the popularity of OTC products. Additionally, their affordability and convenience make them a preferred choice for patients seeking to manage mild to moderate cases of dry mouth without the need for a healthcare provider’s prescription.

Analysis by Distribution Channel:

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

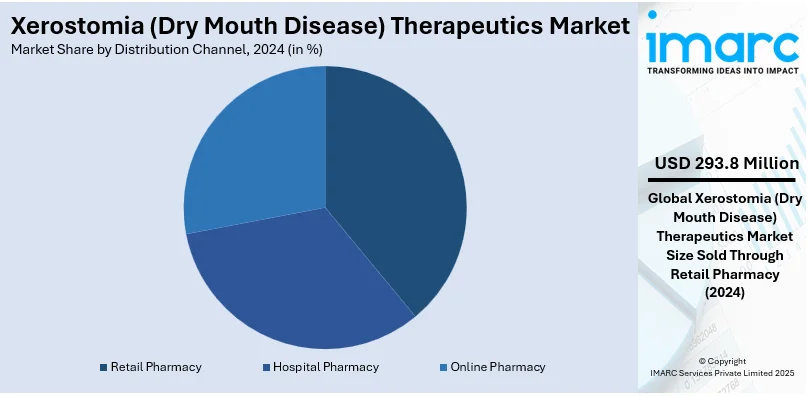

Retail pharmacy leads the market with around 38.5% of market share in 2024, due to their wide accessibility and convenience for consumers. Patients can easily obtain over-the-counter (OTC) products such as mouthwashes, lozenges, and gels, which are commonly used to manage dry mouth symptoms. The growing preference for self-management of xerostomia, along with the increasing number of retail pharmacy chains globally, has bolstered this segment. Retail pharmacies also benefit from strong relationships with pharmaceutical companies, enabling them to stock a diverse range of therapeutics. Additionally, their ability to provide personalized advice and quick access further drives their dominance in the market.

Regional Analysis:

-therapeutics-market.png2.webp)

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 36.8%, driven by a high prevalence of dry mouth conditions, advanced healthcare infrastructure, and significant investments in research and development. The region’s large aging population, particularly in the U.S., contributes to the rising incidence of xerostomia, often linked with medication use, autoimmune diseases, and radiation therapy for cancer treatment. For instance, industry reports state that the U.S. population aged 65 plus is projected to grow from 58 million in 2022 to 82 million by 2050, increasing from 17% to 23% of the total population. Additionally, the presence of key pharmaceutical companies, a robust pipeline of therapeutic products, and favorable reimbursement policies further support market growth. North America’s demand for innovative treatments and patient-centered care strategies ensures its leadership in this market.

Key Regional Takeaways:

United States Xerostomia (Dry Mouth Disease) Therapeutics Market Analysis

In 2024, United States accounted for 88.6% of the market share in North America. The U.S. Xerostomia (Dry Mouth Disease) therapeutics market is growing due to the increasing number of chronic patients, such as diabetes and Sjögren's syndrome, among others. According to CDC, in 2023, about 37.3 million Americans had diagnosed diabetes, accounting for a big portion of individuals with dry mouth. Moreover, the growing need for prescription dry mouth treatments by cancer patients after radiation therapy enhances the demand. New saliva substitutes, oral sprays, and regenerative therapies are creating advanced treatment avenues. Developed healthcare system in the United States ensures increased accessibility to xerostomia treatments for patients. Major pharmaceutical giants, GlaxoSmithKline and Colgate-Palmolive, are looking for expansion in their portfolios of oral health care. Government-aided health care, Medicare, and Medicaid continue to make treatments affordable for patients, and increasing awareness programs also facilitate timely diagnosis and adherence to treatments. The integration of AI in dental healthcare is also improving patient outcomes, positioning the U.S. as a key market for xerostomia therapeutics.

Europe Xerostomia (Dry Mouth Disease) Therapeutics Market Analysis

The European Xerostomia therapeutics market is experiencing growth due to the aging population and increasing diabetes and autoimmune cases. It is estimated by the World Health Organization (WHO) that about 74 million adults and 300,000 children and adolescents in Europe are suffering from diabetes, the greatest risk factor for xerostomia. In addition, an increase in the number of cancer patients treated using radiation therapy causes a boosted demand for saliva substitutes and prescription treatments. Germany and France lead the market in terms of adoption since their healthcare systems are well established. Unilever and Reckitt companies are taking a challenge to apply innovative oral hydration solutions and prescription medicines. European Union rules promoting access to advanced patient therapies support market expansion, as increased research and development result in novel treatment solutions, positioning Europe as a central market for xerostomia therapeutics.

Asia Pacific Xerostomia (Dry Mouth Disease) Therapeutics Market Analysis

Asia Pacific is experiencing a huge growth in the Xerostomia therapeutics market due to the increasing diabetic population and the increasing awareness of oral health. The International Diabetes Federation (IDF) states that by 2023, China had around 140 million people living with diabetes, significantly contributing to the prevalence of dry mouth. The elderly population in Japan, at about 29% of the total population, further fuels the demand for xerostomia treatments. The potential for the market increases in addition to government healthcare services in the form of various schemes, such as Ayushman Bharat by India, which encourages oral health awareness. Herbal and natural saliva substitutes are emerging nowadays, especially in countries like China and India. Pharmaceutical companies like Sun Pharma and Takeda are increasing their market presence both domestically and internationally. The increasing use of digital healthcare platforms is enhancing access to treatment, making Asia Pacific a key region for market growth.

Latin America Xerostomia (Dry Mouth Disease) Therapeutics Market Analysis

The Latin American Xerostomia therapeutics market is growing because of increased investments in healthcare and the rising prevalence of chronic diseases. According to an industry report, Brazil's healthcare spending has reached USD 161 billion in 2023, with a significant share spent on oral health care, as per reports. Increasing cases of xerostomia caused by diabetes and cancer treatments are pushing the demand for therapeutic solutions. Brazil and Mexico have the largest market share in that region, therefore, are shifting their focus toward increasing prescription-only dry mouth therapies. According to an industry report, more than 1.7 million aesthetic and dental operations were conducted within Mexico in the year 2023, contributing to the augmented demand for oral hydration solutions. Multinational companies are coming together with regional firms to create advanced saliva substitutes and prescription-only medications. The market growth in the region is likely to be sustained by government-backed healthcare programs and rising private investments in oral health care.

Middle East and Africa Xerostomia (Dry Mouth Disease) Therapeutics Market Analysis

Middle East and Africa Xerostomia therapeutics market is also witnessing growth in this region as there is growing healthcare investment coupled with a higher incidence of chronic diseases such as diabetes. As per the UAE government data, the federal healthcare budget for 2022 was USD 1.16 billion. It allocated most of the healthcare budget to oral healthcare services. Diabetes is quite prevalent in this region, particularly in the gulf countries. The demand for prescription medication, such as pilocarpine, in Saudi Arabia is on the rise due to an incidence rate of over 18% for diabetes. In South Africa, increasing production by pharmaceutical companies contributes to increased oral hydration solution availability. Dental and oral healthcare awareness is further bolstering the market within the region. Investments in health infrastructure, along with collaborations between local and international pharmaceutical companies, are likely to boost the growth of advanced treatments for xerostomia.

Competitive Landscape:

The competition among the established pharmaceutical firms and emerging biotechnology companies drives the market for xerostomia (dry mouth disease) therapeutics. The key players are focused on the development and commercialization of some products, including saliva substitutes, secretagogues, and therapies focusing on the underlying causes of xerostomia. Companies are putting in substantial investments to create new drug formulations and sophisticated delivery systems to fill unmet needs in patient care. Besides, firms often take on strategic partnerships and acquisitions to base their portfolios of products and enhance market reach. Competition is further influenced by important aspects, such as regulatory approvals, pricing strategies, and clinical effectiveness. For instance, in December 2024, MeiraGTx Holdings announced that they received Regenerative Medicine Advanced Therapy (RMAT) designation from the FDA for their product AAV2-hAQP1 for the treatment of Grade 2/3 radiation-induced xerostomia. This designation highlights the therapy's potential to address unmet needs, expedite development, and enhance patient outcomes for those affected by radiation-induced dry mouth.

The report provides a comprehensive analysis of the competitive landscape in the xerostomia (dry mouth disease) therapeutics market with detailed profiles of all major companies, including:

- 3M Company

- Biotene (GSK plc)

- Parnell Pharmaceuticals Inc.

- Quest Products LLC

- Saliwell Ltd

- Sun Pharmaceutical Industries Limited

- West-Ward Pharmaceutical (Hikma Pharmaceuticals plc)

Latest News and Developments:

- November 2023: Researchers at the University of Leeds launched a new saliva substitute based on aqueous lubricant technology. Laboratory tests indicate that this new formulation is four to five times more effective than existing commercial products in hydrating the mouth and acting as a lubricant during chewing. This substance, termed a microgel, adheres to the oral surface and captures water, so it provides a long-lasting hydrating effect.

- October 2023: The efficacy of a new oral rinse containing sodium hyaluronate for individuals with xerostomia was evaluated in the context of a randomized crossover study. The results demonstrated that this oral rinse significantly decreased dry mouth symptoms and objectively measured improvements in oral health-related subjective measurements, indicating it could benefit patients in terms of quality of life.

Xerostomia (Dry Mouth Disease) Therapeutics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Artificial Saliva/Saliva Substitutes, Salivary Stimulants |

| Drug Types Covered | OTC, Prescription |

| Distribution Channels Covered | Hospital Pharmacy, Retail Pharmacy, Online Pharmacy |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3M Company, Biotene (GSK plc), Parnell Pharmaceuticals Inc., Quest Products LLC, Saliwell Ltd, Sun Pharmaceutical Industries Limited, West-Ward Pharmaceutical (Hikma Pharmaceuticals plc), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the xerostomia (dry mouth disease) therapeutics market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global xerostomia (dry mouth disease) therapeutics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the xerostomia (dry mouth disease) therapeutics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The xerostomia (dry mouth disease) therapeutics market was valued at USD 763.03 Million in 2024.

IMARC estimates the global xerostomia (dry mouth disease) therapeutics market to reach USD 1,007.31 Million in 2033, exhibiting a CAGR of 2.98% during 2025-2033.

The market is driven by rising awareness of dry mouth conditions, the increasing number of elderly individuals prone to the disease, and the growing prevalence of related disorders like Sjögren’s syndrome. Additionally, advancements in treatment options and improved patient outcomes are further stimulating market demand.

North America currently dominates the market, holding a market share of over 36.8% in 2024. This prominence is backed up by high disease awareness, advanced healthcare infrastructure, and strong demand for innovative treatments. The region benefits from a large patient population, favorable reimbursement policies, and significant investments in research and development.

Some of the major players in the xerostomia (dry mouth disease) therapeutics market include 3M Company, Biotene (GSK plc), Parnell Pharmaceuticals Inc., Quest Products LLC, Saliwell Ltd, Sun Pharmaceutical Industries Limited, West-Ward Pharmaceutical (Hikma Pharmaceuticals plc), etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)