Wireless LAN Security Market by Security Type (WPA2/WPA (Wi-Fi Protected Access), WEP (Wired Equivalent Privacy), No-Encryption), Technology (Dedicated Security Appliances, Mobile VPNs, Stand-Alone WLAN Security Software, Performance Monitoring and Intrusion Detection Systems), Deployment Type (On-Premises, On-Cloud), End User (Enterprises, Individual Consumers), and Region 2026-2034

Wireless LAN Security Market Size:

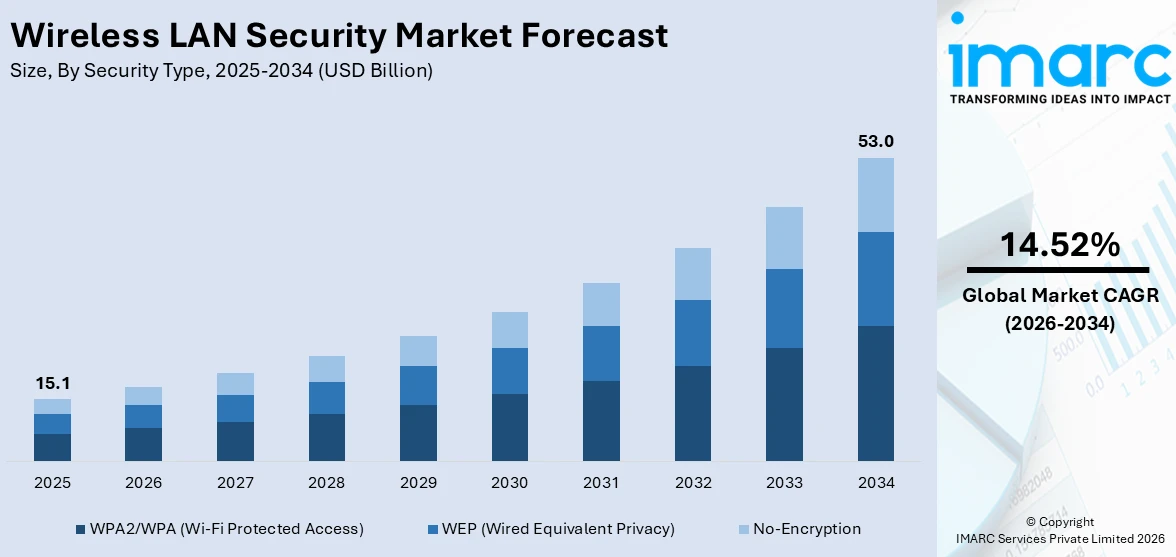

The global wireless LAN security market size reached USD 15.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 53.0 Billion by 2034, exhibiting a growth rate (CAGR) of 14.52% during 2026-2034. The market is experiencing steady growth driven by the rising reliance on wireless networks, the growing awareness about the importance of network security, and the rapid integration of advanced technologies.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 15.1 Billion |

| Market Forecast in 2034 | USD 53.0 Billion |

| Market Growth Rate 2026-2034 | 14.52% |

Wireless LAN Security Market Analysis:

- Market Growth and Size: The market is experiencing robust growth, driven by the escalating demand for secure wireless communication and the increasing prevalence of cyber threats. The market size continues to expand globally as organizations prioritize the implementation of advanced security measures to safeguard their wireless networks.

- Major Market Drivers: Key drivers for the market include the proliferation of wireless devices, rising cybersecurity concerns, and stringent regulatory compliance requirements. These factors propel the adoption of advanced security solutions, contributing to the market's sustained growth.

- Technological Advancements: Continuous technological advancements, such as the integration of artificial intelligence, machine learning, and encryption protocols, significantly impact the market. These innovations enhance the efficiency and effectiveness of security solutions, addressing evolving cyber threats and bolstering network defenses.

- Industry Applications: Wireless LAN security finds applications across various industries, including healthcare, finance, manufacturing, and government. The need to protect sensitive data and ensure secure communication channels drives the adoption of these solutions across diverse sectors.

- Key Market Trends: Emerging trends in the market include the increasing adoption of cloud-based security solutions, the integration of IoT security measures, and the emphasis on user-centric security models to accommodate remote work and mobile connectivity.

- Geographical Trends: Geographical trends indicate significant market growth in regions with high technology adoption, such as North America and Asia-Pacific. These regions witness increased investments in cybersecurity infrastructure and a strong emphasis on data protection.

- Competitive Landscape: The market features a competitive landscape with key players engaging in strategic collaborations, mergers and acquisitions, and continuous product innovations to maintain their market position. Major companies focus on providing comprehensive security solutions to meet evolving customer needs.

- Challenges and Opportunities: Challenges in the market include the sophistication of cyber threats, compliance complexities, and the need for constant adaptation to emerging risks. Opportunities lie in the development of advanced security technologies, addressing specific industry requirements, and expanding market outreach.

- Future Outlook: The future outlook for the market is optimistic, driven by the increasing reliance on wireless networks, the continuous evolution of cyber threats, and the demand for scalable and adaptive security solutions. Anticipated advancements in technology and strategic collaborations are expected to shape the market's trajectory positively.

Wireless LAN Security Market Trends:

Increasing cybersecurity threats and attacks

The persistent rise in cybersecurity threats and attacks is a significant driving force behind the growth of the market. As organizations increasingly rely on wireless networks for seamless connectivity, they become more susceptible to various cyber threats, including unauthorized access, data breaches, and malicious intrusions. The evolving nature of cyber threats requires robust security measures to safeguard sensitive information and maintain the integrity of wireless communications. Factors such as phishing, ransomware, and sophisticated hacking techniques necessitate advanced security protocols, including encryption, authentication, and intrusion detection systems. The market responds to this escalating threat landscape by providing solutions that mitigate risks and fortify networks against cyber vulnerabilities, ensuring the confidentiality and privacy of transmitted data.

To get more information on this market Request Sample

Proliferation of wireless devices and IoT

The proliferation of wireless devices, coupled with the widespread adoption of Internet of Things (IoT) technologies, is a key driver for the market. With an increasing number of devices connecting to wireless networks, ranging from smartphones and laptops to IoT devices in smart homes and enterprises, the attack surface for potential security threats expands exponentially. The need to secure diverse endpoints and ensure the integrity of communication channels becomes paramount. These solutions address this challenge by offering scalable and comprehensive measures to authenticate devices, encrypt data transmissions, and detect anomalous activities. As the number of connected devices continues to grow, the demand for robust security solutions intensifies, making it an indispensable component of modern cybersecurity strategies.

Compliance requirements and data privacy regulations

Stringent compliance requirements and data privacy regulations play a pivotal role in driving the market, especially in sectors dealing with sensitive information such as healthcare, finance, and government. Regulatory frameworks, such as GDPR, HIPAA, and various industry-specific standards, mandate organizations to implement robust security measures to protect confidential data. Failure to comply with these regulations can result in severe legal and financial consequences. These security solutions, including encryption protocols and access controls, enable organizations to meet these compliance requirements by ensuring the confidentiality and integrity of data transmitted over wireless networks. The market experiences a rise in demand as organizations seek to align with regulatory mandates, mitigate legal risks, and uphold the trust of stakeholders by prioritizing the security of their wireless communications.

Wireless LAN Security Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on security type, technology, deployment type, and end user.

Breakup by Security Type:

- WPA2/WPA (Wi-Fi Protected Access)

- WEP (Wired Equivalent Privacy)

- No-Encryption

WPA2/WPA (Wi-Fi protected access) accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the security type. This includes WPA2/WPA (Wi-Fi protected access), WEP (wired equivalent privacy), and no-encryption. According to the report, WPA2/WPA (Wi-Fi protected access) represented the largest segment.

WPA2/WPA (Wi-Fi protected access) holds the majority of the market share. This security type is mostly preferred among individuals since it represents an advanced and widely adopted protocol designed to secure wireless networks. With robust encryption methods and enhanced security features, WPA2/WPA provides a more secure alternative to its predecessor, WEP. Organizations and individuals alike prioritize WPA2/WPA to safeguard their wireless communications, mitigating the risks associated with unauthorized access and data breaches.

On the other hand, wired equivalent privacy (WEP), although an earlier wireless LAN security protocol, still finds application in certain environments. However, due to its vulnerabilities and susceptibility to hacking techniques, WEP has become less prevalent in favor of more secure alternatives like WPA2/WPA. Organizations and individuals transitioning from WEP to more advanced security types contribute to the declining market share of WEP.

Additionally, while not a recommended security practice, a segment of the market may still deploy wireless LANs without encryption, represented by the category of No-Encryption. This segment is typically associated with open or public Wi-Fi networks where encryption may not be enforced. However, the increasing awareness of cybersecurity risks has led to a decreasing prevalence of no-encryption configurations, with organizations and users increasingly opting for more secure encryption protocols to protect their wireless communications.

Breakup by Technology:

- Dedicated Security Appliances

- Mobile VPNs

- Stand-Alone WLAN Security Software

- Performance Monitoring and Intrusion Detection Systems

Mobile VPNs hold the largest share of the industry

A detailed breakup and analysis of the market based on the technology have also been provided in the report. This includes dedicated security appliances, mobile VPNs, stand-alone WLAN security software, and performance monitoring and intrusion detection systems. According to the report, mobile VPNs accounted for the largest market share.

Mobile virtual private networks (VPNs) emerge as the leading technology segment, holding the largest share in the market. With the proliferation of mobile devices and the rise of remote work, Mobile VPNs play a crucial role in ensuring secure communication and data transmission over wireless networks. This technology facilitates secure access to corporate resources, protecting sensitive information and maintaining the privacy of mobile users, which results in a higher uptake of the product among the consumers.

On the other hand, dedicated security appliances are integral to the market, offering specialized hardware solutions for safeguarding networks. These appliances often include firewalls, intrusion prevention systems, and content filtering capabilities. Enterprises leverage dedicated security appliances to fortify their wireless networks against a spectrum of cyber threats, providing a robust first line of defense.

Moreover, stand-alone WLAN security software offers comprehensive solutions specifically designed to address wireless network vulnerabilities. These software solutions encompass encryption, authentication, and access control mechanisms, providing a holistic approach to security. They are crucial for enterprises aiming to fortify their networks against unauthorized access and data breaches.

Furthermore, performance monitoring and intrusion detection Systems (IDS) contribute significantly to the landscape. These systems continuously monitor network activities, identifying anomalies and potential security breaches. By providing real-time insights into network performance and detecting suspicious behavior, these technologies play a pivotal role in maintaining the integrity and security of wireless LANs.

Breakup by Deployment Type:

- On-Premises

- On-Cloud

On-premises represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the deployment type. This includes on-premises and on-cloud. According to the report, on-premises represented the largest segment.

On-premises deployment holds the dominant position in the market. Enterprises prefer on-premises solutions for their control, customization, and dedicated infrastructure. This deployment type allows organizations to manage and secure their wireless networks locally, ensuring a higher level of control over security policies and configurations. On-premises solutions are often favored by industries with strict regulatory compliance requirements, where maintaining data within the organization's physical premises is essential for security and compliance reasons. This deployment type provides a sense of data sovereignty and is well-suited for enterprises with established IT infrastructures seeking a high degree of autonomy in managing their wireless LAN security.

On the contrary, the adoption of on-cloud solutions is growing rapidly, driven by the advantages of scalability, flexibility, and reduced infrastructure costs. Cloud-based deployments are particularly appealing to organizations looking for agile and easily scalable security solutions. This model offers the benefit of outsourcing infrastructure management and maintenance, enabling businesses to focus on core competencies. As cloud technology matures and concerns about data security in the cloud diminish, the on-cloud segment is expected to gain further traction in the market.

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Enterprises

- Individual Consumers

Enterprises represent the leading market segment

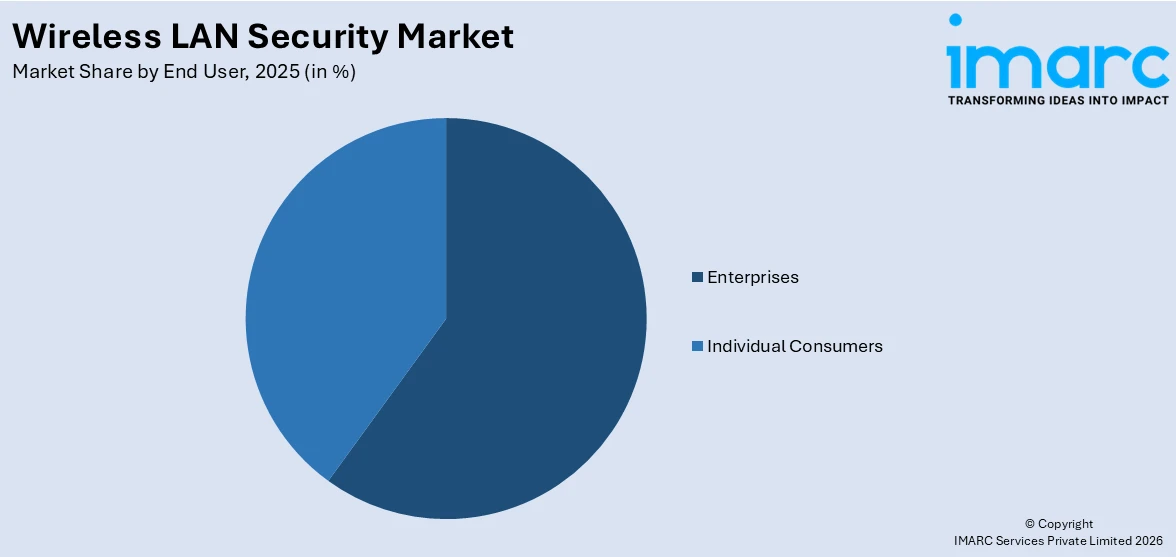

The report has provided a detailed breakup and analysis of the market based on the end user. This includes enterprises and individual consumers. According to the report, enterprises represented the largest segment.

Enterprises stand as the leading market segment in the landscape. The demand for robust security solutions is driven by the increasing reliance on wireless networks for business operations. Enterprises prioritize securing sensitive data, intellectual property, and communication channels, leading to substantial investments in advanced measures. With a focus on protecting corporate networks from evolving cyber threats, enterprises deploy comprehensive solutions encompassing encryption, intrusion detection, and authentication protocols. The adoption of this security is integral to ensuring the integrity, confidentiality, and availability of data in enterprise environments.

On the other hand, while individual consumers contribute significantly to the market, they do not represent the leading segment. The adoption of security measures by individual consumers is driven by the need to safeguard personal information, financial transactions, and online activities. Consumer-oriented solutions often focus on user-friendly interfaces and ease of use. Factors such as the rise in remote work, the proliferation of smart devices, and an increasing awareness of cybersecurity contribute to the growth of this segment. However, the enterprise sector's emphasis on comprehensive security solutions positions it as the primary driver in the market.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest wireless LAN security market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America leads the market, holding the largest market share. The region's dominance is attributed to widespread adoption of advanced technologies, high internet penetration, and a strong focus on cybersecurity measures. The presence of major players, coupled with robust IT infrastructure and stringent regulatory frameworks, fuels the demand for sophisticated LAN security solutions.

The Asia-Pacific region exhibits significant growth potential in the market. Rapid digitization, increasing internet connectivity, and a rise in cyber threats drive the adoption of robust security measures. Government initiatives to strengthen cybersecurity and the proliferation of smartphones contribute to the market's expansion in this dynamic and diverse region.

Europe is a key player in the market, characterized by a mature IT landscape and a strong emphasis on data protection regulations. The region experiences steady growth due to the increasing need for secure wireless communication in various sectors. Investments in cybersecurity infrastructure and rising awareness of potential threats contribute to market expansion.

Latin America is witnessing a growing demand for LAN security solutions as businesses and individuals embrace digital transformation. Increasing internet connectivity, coupled with a rising number of cyber threats, propels the adoption of robust security measures. Government initiatives and cybersecurity awareness campaigns further contribute to the region's market growth.

The Middle East and Africa region demonstrate a rising need for LAN security solutions amidst increasing digitalization. The adoption of advanced technologies, expanding internet connectivity, and a growing focus on cybersecurity measures drive market growth. Government initiatives and investments in securing critical infrastructure contribute to the region's significance in the wireless LAN security landscape.

Leading Key Players in the Wireless LAN Security Industry:

The key players in the market are driving growth through strategic initiatives focused on innovation, partnerships, and addressing evolving cybersecurity threats. These players, including major technology firms and cybersecurity specialists, invest significantly in research and development to create advanced security solutions. By introducing cutting-edge technologies like AI-driven threat detection, encryption protocols, and intrusion prevention systems, they enhance the robustness of LAN security. Collaborations and partnerships with other cybersecurity vendors or industry stakeholders contribute to a holistic approach to tackling security challenges. Key players actively participate in shaping industry standards and regulations, demonstrating thought leadership in the LAN security space. Additionally, awareness campaigns and educational initiatives help enterprises and end-users understand the importance of securing wireless networks, driving the adoption of advanced security solutions in a rapidly evolving digital landscape.

The market research report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- ALE International SAS

- Broadcom Inc.

- Cisco Systems Inc.

- Dell Inc.

- Fortinet

- Hewlett Packard Enterprise Company

- Huawei Technologies Co. Ltd.

- ZTE Corporation

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

Latest News:

- January 22, 2024: ALE International SAS announced the launch of its new Consultants Programme.

- January 17, 2024: Broadcom's End-User Computing Division has been recognized as a leader in Unified Endpoint Management (UEM) by global market research firm Forrester, according to The Forrester Wave™: Unified Endpoint Management, Q4 2023. The division, formerly a part of VMware and now under Broadcom, showcased excellence in balancing Digital Employee Experience (DEX), management, and security.

- January 24. 2024: Cisco Systems Inc. launched Smart Agent for Cisco AppDynamics, enabling agent lifecycle management, dramatically simplifying application instrumentation for full-stack observability through intelligent agent automation and management, and helping customers onboard new applications faster.

Wireless LAN Security Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Security Types Covered | WPA2/WPA (Wi-Fi Protected Access), WEP (Wired Equivalent Privacy), No-Encryption |

| Technologies Covered | Dedicated Security Appliances, Mobile VPNs, Stand-Alone WLAN Security Software, Performance Monitoring and Intrusion Detection Systems |

| Deployment Types Covered | On-Premises, On-Cloud |

| End Users Covered | Enterprises, Individual Consumers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ALE International SAS, Broadcom Inc., Cisco Systems Inc., Dell Inc., Fortinet, Hewlett Packard Enterprise Company, Huawei Technologies Co. Ltd., ZTE Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global wireless LAN security market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global wireless LAN security market?

- What is the impact of each driver, restraint, and opportunity on the global wireless LAN security market?

- What are the key regional markets?

- Which countries represent the most attractive wireless LAN security market?

- What is the breakup of the market based on the security type?

- Which is the most attractive security type in the wireless LAN security market?

- What is the breakup of the market based on technology?

- Which is the most attractive technology in the wireless LAN security market?

- What is the breakup of the market based on the deployment type?

- Which is the most attractive deployment type in the wireless LAN security market?

- What is the breakup of the market based on the end user?

- Which is the most attractive end user in the wireless LAN security market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global wireless LAN security market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the wireless LAN security market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global wireless LAN security market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the wireless LAN security industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)