Wealth Management Platform Market Size, Share, Trends and Forecast by Advisory Model, Deployment Mode, Business Function, Enterprise Size, End Use Industry, and Region, 2026-2034

Wealth Management Platform Market Size and Share:

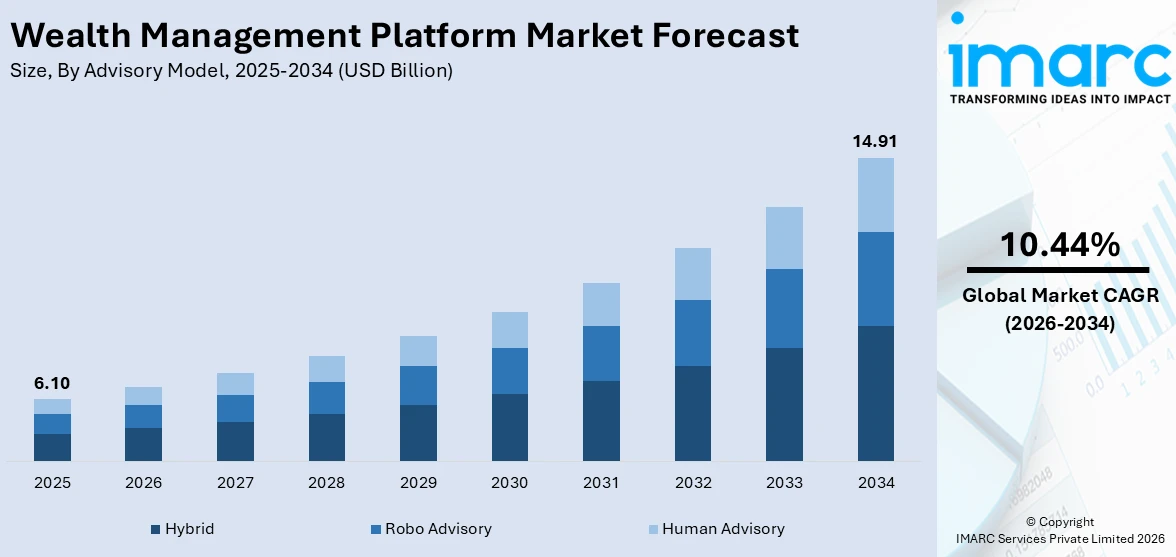

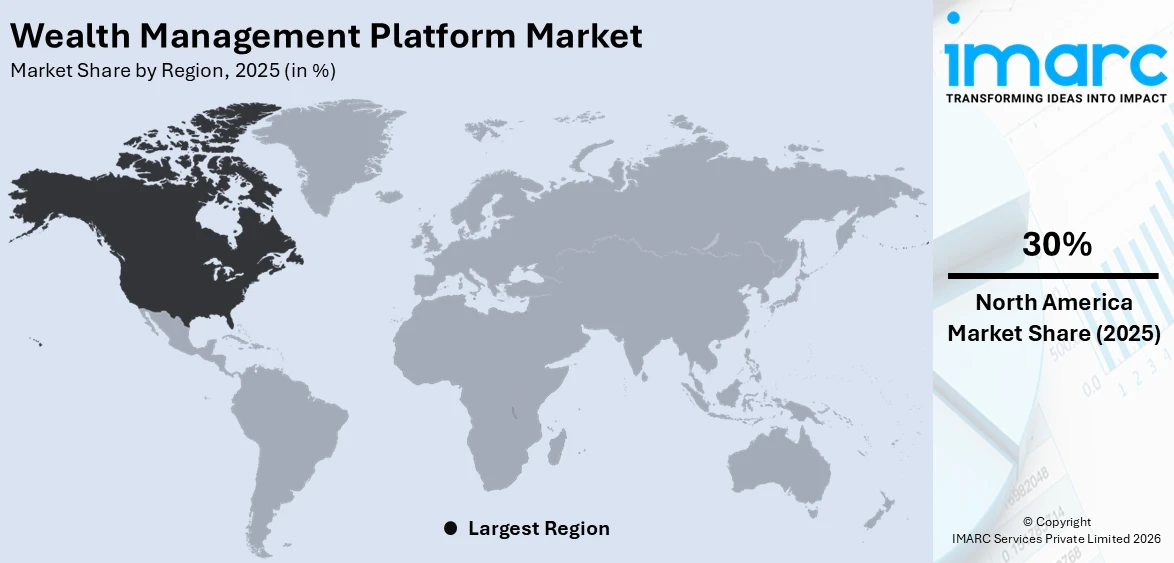

The global wealth management platform market size was valued at USD 6.10 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 14.91 Billion by 2034, exhibiting a CAGR of 10.44% from 2026-2034. North America currently dominates the market, holding a market share of 30% in 2025. The region benefits from a well-established financial services infrastructure, widespread adoption of advanced digital technologies among wealth management firms, and a growing demand for integrated advisory solutions that combine automated tools with personalized client engagement, all contributing to the wealth management platform market share.

The wealth management platform market growth is being primarily driven by the increasing digitization of financial services worldwide, as institutions seek to modernize their operations and deliver enhanced client experiences. The rising demand for personalized investment advisory solutions that cater to diverse client portfolios and risk profiles is further accelerating market expansion. Additionally, the growing need for real-time portfolio monitoring, automated rebalancing, and seamless integration with banking ecosystems is encouraging financial organizations to adopt advanced wealth management platforms. The ongoing shift toward fee-based advisory models, rather than commission-based structures, is also prompting wealth management firms to invest in comprehensive platform solutions that improve transparency and client trust.

The United States has emerged as a major region in the wealth management platform market owing to many factors. The country's mature financial services sector, characterized by a high concentration of registered investment advisors, broker-dealers, and wealth management firms, creates substantial demand for sophisticated platform solutions. In December 2025, U.S. fintech startup Nevis raised $35 million in a Series A round to expand its AI‑driven wealth management platform for registered investment advisors, underlining strong investor appetite for advisor‑focused technology and automation across RIAs. Moreover, the growing preference among American investors for hybrid advisory models that blend robo-advisory capabilities with human expertise is driving platform innovation and adoption. The wealth management platform market outlook is further strengthened by the rapid expansion of digital-first financial services providers and the rising expectations of tech-savvy investors who demand intuitive, mobile-accessible portfolio management tools and comprehensive real-time financial insights across all their investment accounts.

To get more information on this market Request Sample

Wealth Management Platform Market Trends:

Growing Integration of Artificial Intelligence

The integration of artificial intelligence (AI) and machine learning (ML) technologies into wealth management platforms is reshaping how financial advisors interact with clients and manage portfolios. AI-powered tools enable predictive analytics, allowing advisors to anticipate market movements, identify investment opportunities, and personalize client recommendations with unprecedented accuracy. In October 2025, BlackRock’s Aladdin Wealth platform introduced an AI‑driven “Auto Commentary” feature, first implemented by Morgan Stanley Wealth Management, to help advisors deliver personalized, data‑based insights to clients. ML algorithms continuously analyze vast datasets, including market conditions, client behavior patterns, and macroeconomic indicators, to generate actionable insights that enhance decision-making processes. Additionally, natural language processing capabilities are being embedded into platforms to automate client communications, generate investment reports, and respond to routine inquiries efficiently.

Rising Demand for Cloud-Based Platforms

The shift toward cloud-based deployment models is transforming the wealth management platform industry, enabling firms of all sizes to access sophisticated tools without significant upfront infrastructure investments. Cloud-based platforms offer scalability, allowing wealth management firms to expand their operations seamlessly while maintaining cost efficiency and operational flexibility. In November 2025, UK investment manager 7IM partnered with Cloud Direct to build a new cloud‑based infrastructure using Microsoft technologies, aimed at improving scalability, accelerating feature delivery, and enhancing adviser and client experiences. The wealth management platform market trends indicate that cloud adoption is being driven by the need for real-time data accessibility, enabling advisors and clients to access portfolio information from anywhere using any internet-connected device.

Increasing Focus on Regulatory Compliance

The growing complexity of financial regulations across global markets is driving significant demand for wealth management platforms equipped with robust compliance management capabilities. Regulatory frameworks governing client suitability assessments, anti-money laundering protocols, know-your-customer requirements, and data privacy standards are becoming increasingly stringent, requiring firms to adopt platforms that automate compliance workflows and reduce operational risk. In January 2025, RIA Compliance Technology announced a dedicated compliance management software for registered investment advisors that automates critical tasks such as regulatory deadline tracking, documentation, and reporting to help firms stay current with evolving SEC requirements. The wealth management platform market forecast reflects the increasing emphasis on platforms that provide built-in regulatory reporting, audit trails, and real-time monitoring of compliance-related activities.

Wealth Management Platform Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global wealth management platform market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on advisory model, deployment mode, business function, enterprise size, and end use industry.

Analysis by Advisory Model:

- Hybrid

- Robo Advisory

- Human Advisory

Hybrid holds 40% of the market share, which combines the efficiency of automated robo-advisory tools with the nuanced judgment of human financial advisors, creating a comprehensive service offering that appeals to a broad spectrum of investors. This model allows clients to benefit from algorithm-driven portfolio management for routine tasks such as asset allocation and rebalancing, while still having access to personalized guidance from experienced advisors for complex financial planning decisions. In 2025, a survey by Futu Private Wealth Management revealed that 80% of emerging high‑net‑worth investors preferred a hybrid service model integrating digital platforms with human advisory support, underscoring strong client demand for blended services. The increasing preference among high-net-worth and mass-affluent investors for a balanced approach that leverages both technology and human expertise is supporting the dominance of the hybrid model. Financial institutions are investing in hybrid platforms that seamlessly transition clients between digital and human interactions based on the complexity of their needs.

Analysis by Deployment Mode:

- On-premises

- Cloud-based

Cloud-based leads the market with a share of 63%, offering wealth management firms significant advantages in terms of scalability, cost efficiency, and operational agility, enabling organizations to access advanced platform capabilities without the burden of maintaining complex on-premises infrastructure. The growing demand for remote accessibility and real-time data synchronization across multiple devices and locations is further supporting the widespread adoption of cloud-based solutions. Financial firms benefit from automatic software updates, enhanced data security protocols managed by specialized cloud service providers, and the ability to rapidly integrate new features and third-party applications. Small and medium-sized wealth management firms, in particular, favor cloud deployment due to its lower initial capital expenditure and predictable subscription-based pricing models. Additionally, the increasing availability of cloud-native wealth management solutions designed specifically for the financial services industry is expanding the range of options available to firms seeking modern, flexible, and compliant platform environments.

Analysis by Business Function:

- Reporting

- Performance Management

- Financial Advice Management

- Risk and Compliance Management

- Portfolio, Accounting and Trading Management

- Others

Portfolio, accounting and trading management dominates the market, with a share of 25%. This business function encompasses the core operational activities of wealth management, including portfolio construction, trade execution, settlement processing, and accounting reconciliation, which are fundamental to the daily operations of advisory firms. The growing complexity of investment portfolios, which increasingly span multiple asset classes, geographies, and currencies, requires sophisticated platforms capable of managing diverse holdings while maintaining accurate accounting records. Wealth management firms rely on integrated portfolio and trading management tools to execute investment strategies efficiently, minimize operational errors, and ensure timely reconciliation of transactions. The demand for real-time portfolio analytics and automated trading capabilities is encouraging platform providers to develop advanced modules that support algorithmic trading, order management, and seamless connectivity with exchanges and custodians. Furthermore, regulatory requirements for accurate and transparent accounting practices are compelling firms to prioritize platforms that deliver comprehensive portfolio management functionalities.

Analysis by Enterprise Size:

- Large Enterprises

- Small and Medium-sized Enterprises

Large enterprises represent the leading segment, with a market share of 59%. Large enterprises, including major banks, global asset management firms, and multinational financial institutions, possess extensive client bases and complex operational requirements that necessitate comprehensive wealth management platform solutions. These organizations require platforms capable of managing high volumes of client accounts, supporting multi-jurisdictional regulatory compliance, and integrating with existing enterprise resource planning and customer relationship management systems. The significant financial resources available to large enterprises enable them to invest in customized, feature-rich platform implementations that address their specific operational workflows and client service requirements. Additionally, large firms prioritize platforms offering advanced analytics, robust security frameworks, and scalable architectures that can accommodate growing client portfolios and evolving market conditions. The increasing competitive pressure among large financial institutions to deliver superior digital client experiences is further driving their adoption of sophisticated wealth management platforms.

Analysis by End Use Industry:

Access the comprehensive market breakdown Request Sample

- Banks

- Brokerage Firms

- Investment Management Firms

- Trading and Exchange Firms

- Others

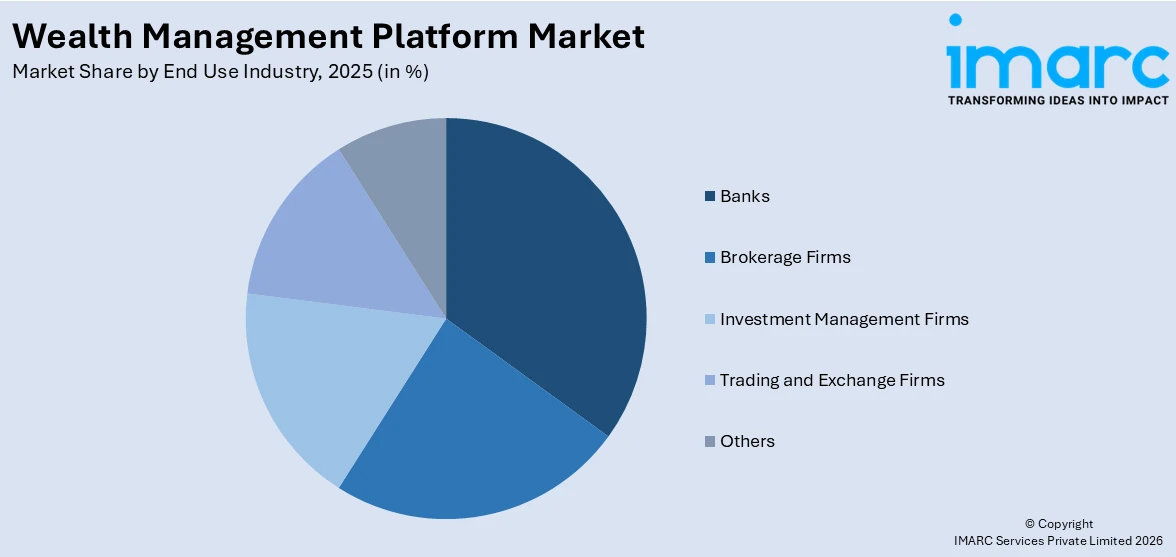

Banks account for the largest share of 30% in the end use industry segment. Banks represent a critical end user category for wealth management platforms, as they leverage these solutions to offer comprehensive financial advisory services alongside their traditional banking products. The growing emphasis on holistic client relationship management is prompting banks to integrate wealth management capabilities into their core banking infrastructure, enabling seamless cross-selling of investment, insurance, and retirement planning products. Retail and private banking divisions within large banking institutions are increasingly deploying advanced platforms that support personalized financial planning, goal-based investing, and digital onboarding processes. The rising demand from bank clients for unified financial dashboards that consolidate banking and investment information is further accelerating platform adoption. Additionally, banks are leveraging wealth management platforms to enhance client retention, increase fee-based revenue streams, and differentiate their service offerings in an increasingly competitive financial services landscape that demands sophisticated digital engagement capabilities.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 30% of the share, enjoys the leading position in the market. The region's dominance is primarily attributed to its advanced financial services ecosystem, which includes a high concentration of wealth management firms, registered investment advisors, and technology-driven financial institutions that are early adopters of innovative platform solutions. The presence of major technology companies and fintech startups focused on developing cutting-edge wealth management tools further strengthens the region's market position. North American wealth management firms benefit from a sophisticated regulatory environment that encourages transparency and digital innovation, driving the adoption of platforms equipped with compliance automation and client reporting capabilities. The high penetration of digital financial services among consumers in the United States and Canada creates a favorable environment for platform growth. Additionally, the significant volume of assets under management in the region necessitates robust, scalable platform solutions capable of handling complex multi-asset portfolios and diverse client requirements efficiently.

Key Regional Takeaways:

United States Wealth Management Platform Market Analysis

The United States represents the most significant contributor to the wealth management platform market growth, supported by its expansive and mature financial services industry. The country's large population of high-net-worth individuals and the growing affluence of mass-market investors are driving substantial demand for advanced wealth management solutions that deliver personalized advisory experiences. In October 2025, Picture Wealth announced that its estate‑planning software platform integrated directly with Advyzon’s wealth management system—streamlining data flows and enabling advisors to offer more comprehensive planning services without manual entry. The increasing adoption of hybrid advisory models, which combine automated investment management with dedicated human advisor support, is a key growth factor in the United States market. Regulatory frameworks, including fiduciary standards enforced by financial oversight bodies, are compelling wealth management firms to adopt platforms that ensure compliance while enhancing operational efficiency. The rapid growth of independent registered investment advisor firms seeking technology solutions to compete with larger institutions is creating new market opportunities.

Europe Wealth Management Platform Market Analysis

Europe represents a significant market for wealth management platforms, driven by the region's diverse financial services landscape and increasingly stringent regulatory requirements. The implementation of comprehensive financial regulations, including investor protection directives and data privacy frameworks, is compelling European wealth management firms to invest in platforms that automate compliance processes and ensure transparent client reporting. The growing demand for cross-border wealth management services within Europe, facilitated by harmonized financial regulations in several countries, is encouraging the adoption of platforms capable of managing multi-currency, multi-jurisdictional portfolios. The increasing penetration of digital banking services and the rising preference among European investors for technology-enabled advisory solutions are further supporting market expansion. Major financial centers across the region are witnessing growing adoption of cloud-based wealth management platforms that offer flexibility and scalability. Additionally, the expanding robo-advisory segment in Europe, driven by cost-conscious retail investors seeking accessible investment management services, is creating new opportunities for platform providers to serve previously underserved market segments.

Asia Pacific Wealth Management Platform Market Analysis

Asia Pacific is emerging as a rapidly growing market for wealth management platforms, fueled by the region's expanding high-net-worth individual population and increasing digital financial services adoption. The rapid economic growth in countries across the region is creating a significant pool of investable wealth that requires sophisticated management solutions. The growing penetration of mobile banking and digital payment platforms is establishing a technology-ready environment for wealth management platform adoption. Governments across the region are implementing financial inclusion initiatives and regulatory modernization efforts that encourage digital transformation in financial services. The rising demand for personalized investment advisory services among the growing middle class and affluent populations is driving platform providers to develop solutions tailored to regional preferences and regulatory frameworks. Additionally, the increasing presence of global wealth management firms expanding their operations into the region is contributing to the growing demand for advanced platform solutions.

Latin America Wealth Management Platform Market Analysis

Latin America is witnessing gradual growth in the wealth management platform market, driven by the expanding financial services sector and increasing digitization of investment management processes across the region. The growing affluent population in major economies is creating demand for professional wealth management services supported by technology-enabled platforms. Financial institutions in the region are modernizing their operations by adopting cloud-based wealth management solutions that offer improved client engagement and portfolio management capabilities. The increasing regulatory focus on financial transparency and investor protection is encouraging firms to implement platforms with built-in compliance features. Additionally, the rising penetration of digital financial services and mobile connectivity is creating a supportive environment for platform adoption.

Middle East and Africa Wealth Management Platform Market Analysis

The Middle East and Africa is experiencing emerging growth in the wealth management platform market, supported by the increasing development of financial services infrastructure and rising wealth accumulation in key economies. The growing emphasis on economic diversification in several countries is encouraging investments in sophisticated financial technology solutions, including wealth management platforms. The expanding high-net-worth individual population, particularly in major financial hubs across the region, is driving demand for personalized advisory services and digital portfolio management tools. Financial institutions are increasingly adopting modern platform solutions to attract and retain affluent clients seeking comprehensive wealth management services. The ongoing regulatory modernization efforts are further supporting platform adoption across the region.

Competitive Landscape:

The competitive landscape of the wealth management platform market is characterized by intense rivalry among established technology providers, financial software companies, and emerging fintech startups vying for market share. Key players are focusing on strategic acquisitions, partnerships, and product innovation to strengthen their market positions and expand their client bases globally. Companies are investing heavily in research and development to incorporate advanced technologies such as AI, ML, and blockchain into their platform offerings, aiming to deliver differentiated solutions that address evolving client needs. The trend toward open banking and application programming interface-based architectures is enabling platform providers to create integrated ecosystems that enhance the value proposition for wealth management firms. Additionally, providers are increasingly offering modular platform solutions that allow firms to customize their technology stacks based on specific business requirements.

The report provides a comprehensive analysis of the competitive landscape in the wealth management platform market with detailed profiles of all major companies, including:

- Avaloq (NEC Corporation)

- Backbase

- Broadridge Financial Solutions, Inc.

- Comarch SA

- Crealogix AG

- Edgeverve Systems Limited (Infosys Limited)

- FIS

- Profile Software

- Prometeia s.p.a.

- SEI

- SS&C Technologies, Inc.

- TATA Consultancy Services Limited

- Temenos

Latest News and Developments:

- In November 2025, WealthLine launched WealthReach, an AI-driven prospecting platform for RIAs and wealth management firms. The platform identifies warm, high-intent prospects, enriches leads with detailed financial and behavioral data, and automates personalized outreach, enhancing advisor productivity and accelerating client acquisition.

- In September 2025, Altruist launched Hazel, an AI-powered platform for wealth advisors. Hazel automates tasks like note-taking, CRM updates, meeting preparation, and email management, providing personalized insights from client data. The platform enhances advisor productivity, streamlines workflows, and integrates seamlessly with leading CRM systems.

Wealth Management Platform Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Advisory Models Covered | Hybrid, Robo Advisory, Human Advisory |

| Deployment Modes Covered | On-premises, Cloud-based |

| Business Functions Covered | Reporting, Performance Management, Financial Advice Management, Risk and Compliance Management, Portfolio, Accounting and Trading Management, Others |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| End Use Industries Covered | Banks, Brokerage Firms, Investment Management Firms, Trading and Exchange Firms, Others |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Avaloq (NEC Corporation), Backbase, Broadridge Financial Solutions, Inc., Comarch SA, Crealogix AG, Edgeverve Systems Limited (Infosys Limited), FIS, Profile Software, Prometeia s.p.a., SEI, SS&C Technologies, Inc., TATA Consultancy Services Limited, Temenos, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the wealth management platform market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global wealth management platform market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the wealth management platform industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Wealth Management Platform Market Report

The wealth management platform market was valued at USD 6.10 Billion in 2025.

The wealth management platform market is projected to exhibit a CAGR of 10.44% during 2026-2034, reaching a value of USD 14.91 Billion by 2034.

The wealth management platform market is driven by the increasing digitization of financial services, growing demand for personalized advisory solutions, rising adoption of hybrid advisory models, expanding high-net-worth individual population globally, increasing regulatory compliance requirements, and the ongoing shift toward cloud-based deployment models that offer scalability and cost efficiency to wealth management firms.

North America currently dominates the wealth management platform market, accounting for a share of 30%. The region benefits from its advanced financial services infrastructure, high concentration of wealth management firms, early technology adoption, and a large population of high-net-worth individuals.

Some of the major players in the wealth management platform market include Avaloq (NEC Corporation), Backbase, Broadridge Financial Solutions, Inc., Comarch SA, Crealogix AG, Edgeverve Systems Limited (Infosys Limited), FIS, Profile Software, Prometeia s.p.a., SEI, SS&C Technologies, Inc., TATA Consultancy Services Limited, Temenos, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)