Vertebroplasty and Kyphoplasty Needles Market Report by Procedure (Kyphoplasty Procedures, Vertebroplasty Procedures), End Use (Hospitals, Ambulatory Surgical Centers), and Region 2026-2034

Vertebroplasty And Kyphoplasty Needles Market Overview:

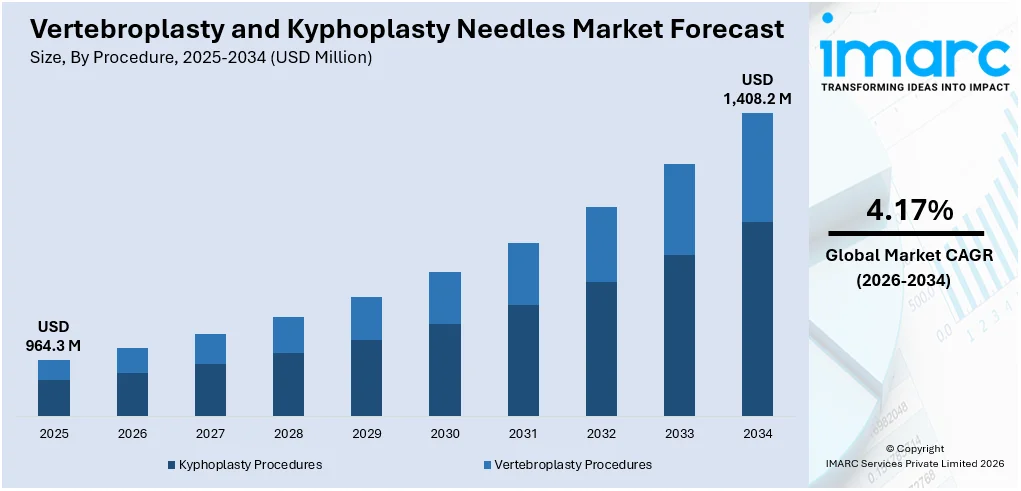

The global vertebroplasty and kyphoplasty needles market size reached USD 964.3 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 1,408.2 Million by 2034, exhibiting a growth rate (CAGR) of 4.17% during 2026-2034. The increasing prevalence of osteoporosis and vertebral compression fractures, rising awareness of minimally invasive spine surgeries, continuous advancements in needle design and technologies. growing healthcare expenditure, and escalating collaborations between manufacturers and research institutions are few of the factors fueling the vertebroplasty and kyphoplasty needles market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 964.3 Million |

| Market Forecast in 2034 | USD 1,408.2 Million |

| Market Growth Rate 2026-2034 | 4.17% |

Vertebroplasty and Kyphoplasty Needles Market Analysis:

- Market Growth and Size: The market is witnessing moderate growth on account of increasing incidences of spinal disorders, along with the rising geriatric population.

- Technological Advancements: Innovations in needle design and material assist in enhancing the efficacy and safety of vertebroplasty and kyphoplasty procedures.

- Industry Applications: Vertebroplasty and kyphoplasty needles are primarily used in orthopedic and radiology departments for treating vertebral compression fractures and providing symptomatic relief while restoring vertebral height.

- Geographical Trends: North America leads the market, driven by the presence of well-established healthcare infrastructure. However, Asia Pacific is emerging as a fast-growing market due to the increasing awareness among individuals about advanced treatment solutions.

- Competitive Landscape: Key players are constantly innovating and expanding their product portfolios to include technologically advanced needles.

- Challenges and Opportunities: While the market faces challenges, such as risk associated with the procedures, like infection, bleeding, or nerve damage, it also encounters opportunities on account of the improvements in technique and technology to mitigate these risks.

- Future Outlook: The future of the vertebroplasty and kyphoplasty needles market looks promising, with the rising development of more advanced, safer, and efficient needles. In addition, the increasing focus on patient-centric approaches is projected to bolster the market forward.

To get more information on this market Request Sample

Vertebroplasty and Kyphoplasty Needles Market Trends/Drivers:

Rising prevalence of osteoporosis and vertebral compression fractures

The global vertebroplasty and kyphoplasty needles market is being driven by the increasing prevalence of osteoporosis and vertebral compression fractures, particularly among the aging population. Osteoporosis, characterized by reduced bone density and increased fracture susceptibility, has become a significant public health concern. These minimally invasive techniques offer effective pain relief and vertebral stabilization, addressing the debilitating consequences of fractures. Given the rising awareness of the impact of osteoporosis on quality of life, both patients and healthcare providers are increasingly opting for these procedures.

Growing awareness of minimally invasive spine surgeries

The market for vertebroplasty and kyphoplasty needles is experiencing growth due to the growing awareness and appreciation of minimally invasive spine surgeries. Traditional open surgeries often entail extended hospital stays, longer recovery periods, and higher risks of complications. In contrast, vertebroplasty and kyphoplasty procedures offer minimally invasive alternatives that involve smaller incisions, reduced tissue trauma, and quicker patient recuperation. The dissemination of information about these benefits through medical professionals, patient education initiatives, and digital platforms is driving patient preference for these procedures. Moreover, healthcare providers are recognizing the advantages of offering minimally invasive options to their patients, which is further propelling the adoption of vertebroplasty and kyphoplasty techniques. This increased awareness is positioning these procedures as efficient solutions for addressing spinal issues while minimizing patient discomfort and healthcare costs.

Advancements in needle design and technologies

One of the pivotal drivers in the global vertebroplasty and kyphoplasty needles market is the continuous advancement in needle design and related technologies. Precision and accuracy are critical in these procedures to ensure optimal placement of cement or biocompatible material to stabilize vertebral fractures. Manufacturers are investing in research and development to create needles that enhance procedural efficiency, minimize tissue disruption, and provide real-time visualization. The incorporation of features like improved needle-tip designs, guided navigation systems, and compatibility with various imaging modalities is enhancing the overall effectiveness of these procedures. These advancements are not only making vertebroplasty and kyphoplasty procedures safer and more reliable but also inspiring greater confidence among healthcare providers to perform these techniques.

Vertebroplasty and Kyphoplasty Needles Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global vertebroplasty and kyphoplasty needles market report, along with vertebroplasty and kyphoplasty needles market forecast at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on procedure and end use.

Breakup by Procedure:

- Kyphoplasty Procedures

- Vertebroplasty Procedures

Kyphoplasty procedures dominates the market

The report has provided a detailed breakup and analysis of the market based on the procedure. This includes kyphoplasty and vertebroplasty procedures. According to the report, kyphoplasty procedures represented the largest segment.

The growth of the kyphoplasty procedures segment is fueled by the rising incidence of vertebral compression fractures due to osteoporosis. Moreover, the increasing awareness among patients and healthcare professionals about the benefits of minimally invasive procedures is propelling the adoption of kyphoplasty. This technique offers reduced pain, shorter hospital stays, and quicker recovery times compared to traditional open surgeries. In line with this, advancements in medical technology and needle design are enhancing the precision and safety of kyphoplasty procedures, instilling confidence in medical practitioners and patients alike. Furthermore, the integration of imaging technologies like fluoroscopy and CT scans allows for real-time visualization, contributing to the accurate placement of cement during the procedure. Additionally, the collaboration between medical device manufacturers and research institutions is fostering innovation, leading to improved outcomes and expanding the availability of kyphoplasty procedures. Besides this, the growing aging population and increasing healthcare expenditure further stimulate the growth of the kyphoplasty procedures segment, as more individuals seek effective solutions for spinal health issues.

Breakup by End Use:

Access the comprehensive market breakdown Request Sample

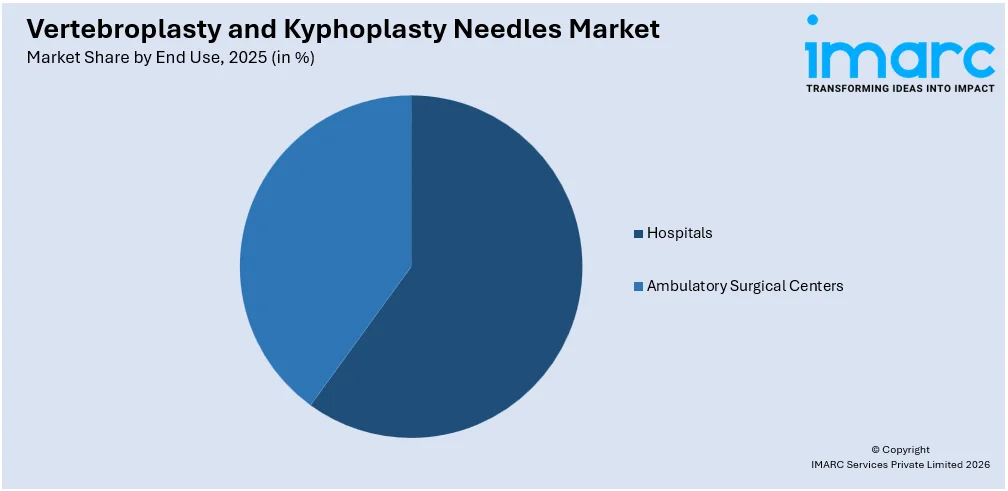

- Hospitals

- Ambulatory Surgical Centers

Hospitals dominate the market

The report has provided a detailed breakup and analysis of the market based on the end use. This includes hospitals and ambulatory surgical centers. According to the report, hospitals represented the largest segment.

The growth of the hospitals segment in the vertebroplasty and kyphoplasty needles market is propelled by the escalating prevalence of osteoporosis-related fractures and spinal conditions, which has increased the demand for minimally invasive procedures offered by hospitals. Moreover, the expanding awareness among patients and healthcare professionals about the benefits of vertebroplasty and kyphoplasty procedures has led to higher adoption rates within hospital settings. Additionally, advancements in medical imaging technologies have enhanced the precision and safety of these procedures, aligning with the capabilities and resources available in hospital environments. Furthermore, strategic collaborations between hospitals and medical device manufacturers have facilitated the availability of cutting-edge needle technologies, boosting patient confidence and clinician expertise. In line with this, the comprehensive range of post-procedure care and rehabilitation services offered by hospitals contributes to patient satisfaction and successful outcomes, further driving the segment's growth.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest vertebroplasty and kyphoplasty needles market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

North America is experiencing substantial growth in the vertebroplasty and kyphoplasty needles market, propelled by the region's aging population that is more susceptible to osteoporosis and related vertebral fractures. Furthermore, the well-established healthcare infrastructure and high healthcare expenditure contribute to greater accessibility to advanced medical procedures, including vertebroplasty and kyphoplasty. In line with his, the region's strong focus on medical research and innovation fosters the development of cutting-edge needle technologies, enhancing procedural precision and patient outcomes. Additionally, the rising awareness among both healthcare providers and patients about the benefits of minimally invasive spine surgeries supports the adoption of these techniques. Moreover, the North American market benefits from active collaborations between medical device manufacturers and research institutions, fostering rapid advancements. Apart from this, patient preference for treatments with shorter recovery times and reduced postoperative pain aligns with the minimally invasive nature of vertebroplasty and kyphoplasty, further driving the market's growth in the region.

Competitive Landscape:

The competitive landscape of the vertebroplasty and kyphoplasty needles market is characterized by a dynamic interplay of key players who are driving advancements and innovations in the field. These players demonstrate a strong commitment to research and development, consistently striving to enhance needle design, procedural efficacy, and patient outcomes. With a focus on technological innovation, these companies continuously introduce new and improved needle solutions that cater to the evolving needs of healthcare providers and patients. Collaborations with research institutions further bolster their capabilities to develop cutting-edge products, positioning them as leaders in the market. The competitive environment encourages healthy competition, fostering a culture of innovation that benefits the medical community and ultimately, patients. As market leaders vie to offer superior solutions, the entire landscape is driven towards excellence, with a mutual goal of advancing the field of vertebroplasty and kyphoplasty needles while contributing to the improvement of patient care.

The report has provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- Adroit Manufacturing Company

- Biopsybell S.R.L. Società Unipersonale

- IZI Medical Products (Halma plc)

- Jayon Implants Pvt.Ltd.

- Medtronic Plc

- Merit Medical Systems, Inc.

- MOLLER Medical GmbH

- Stryker Corporation

- Suretech Medical INC

- Swastik Enterprise

- Tecres S.p.A.

- Teknimed

Vertebroplasty and Kyphoplasty Needles Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Procedures Covered | Kyphoplasty Procedures, Vertebroplasty Procedures |

| End Uses Covered | Hospitals, Ambulatory Surgical Centers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Adroit Manufacturing Company, Biopsybell S.R.L. Società Unipersonale, IZI Medical Products (Halma plc), Jayon Implants Pvt.Ltd., Medtronic Plc, Merit Medical Systems, Inc., MOLLER Medical GmbH, Stryker Corporation, Suretech Medical INC, Swastik Enterprise, Tecres S.p.A., Teknimed, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global vertebroplasty and kyphoplasty needles market performed so far, and how will it perform in the coming years ?

- What are the drivers, restraints, and opportunities in the global vertebroplasty and kyphoplasty needles market ?

- What is the impact of each driver, restraint, and opportunity on the global vertebroplasty and kyphoplasty needles market ?

- What are the key regional markets ?

- Which countries represent the most attractive vertebroplasty and kyphoplasty needles market ?

- What is the breakup of the market based on procedure ?

- Which is the most attractive procedure in the vertebroplasty and kyphoplasty needles market ?

- What is the breakup of the market based on the end use ?

- Which is the most attractive end use in the vertebroplasty and kyphoplasty needles market ?

- What is the competitive structure of the global vertebroplasty and kyphoplasty needles market ?

- Who are the key players/companies in the global vertebroplasty and kyphoplasty needles market ?

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the vertebroplasty and kyphoplasty needles market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global vertebroplasty and kyphoplasty needles market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the vertebroplasty and kyphoplasty needles industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)