United States Meat Market Size, Share, Trends and Forecast by Type, Product, Distribution Channel, and Region, 2026-2034

United States Meat Market Size, Share, Trends & Forecast (2026-2034)

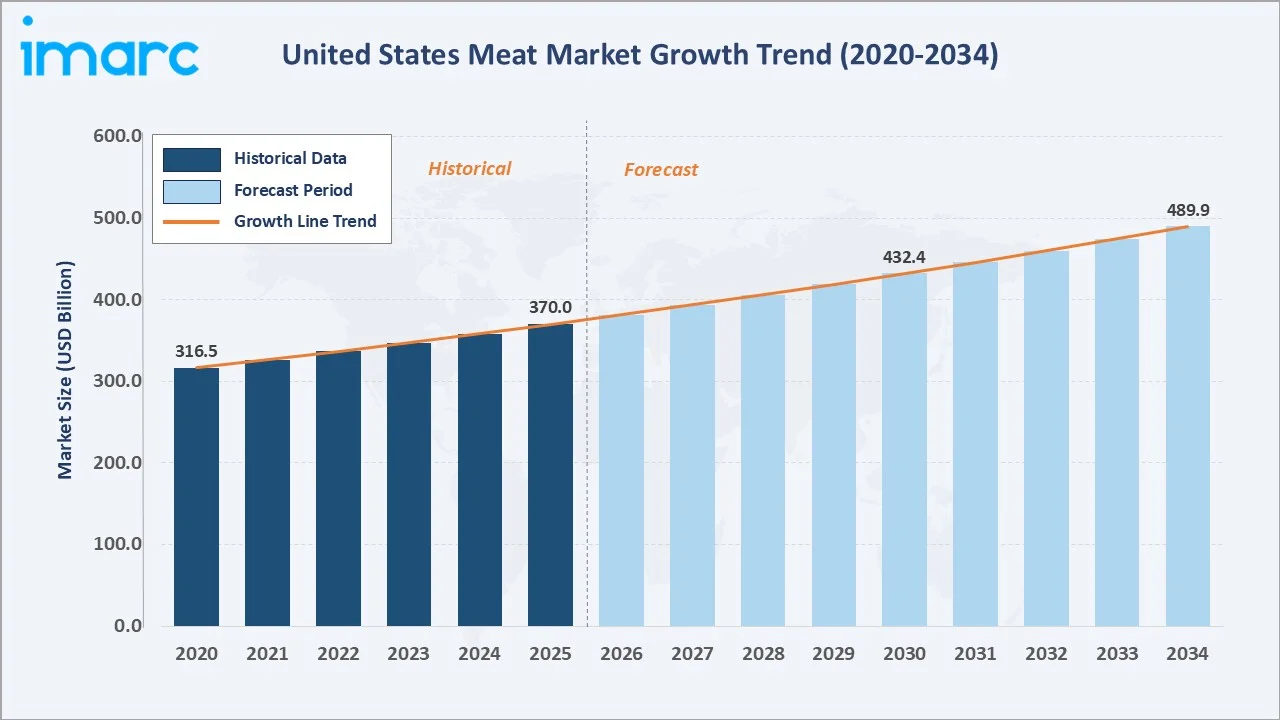

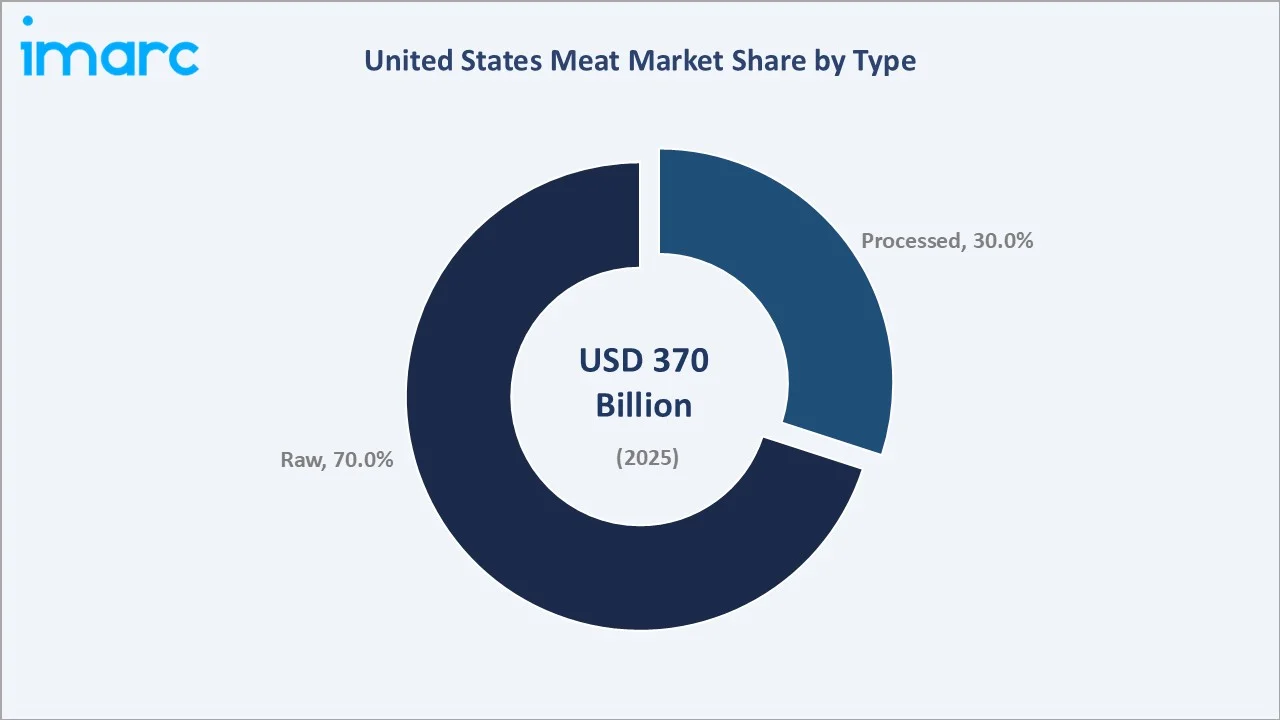

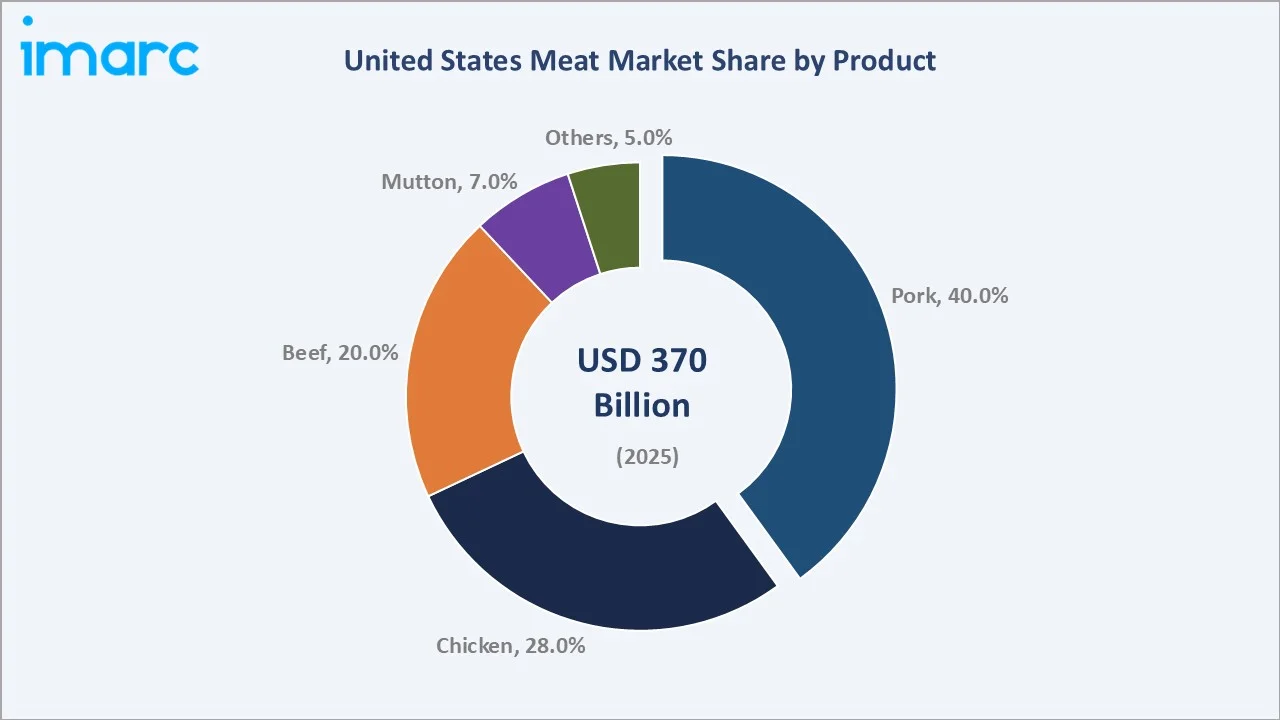

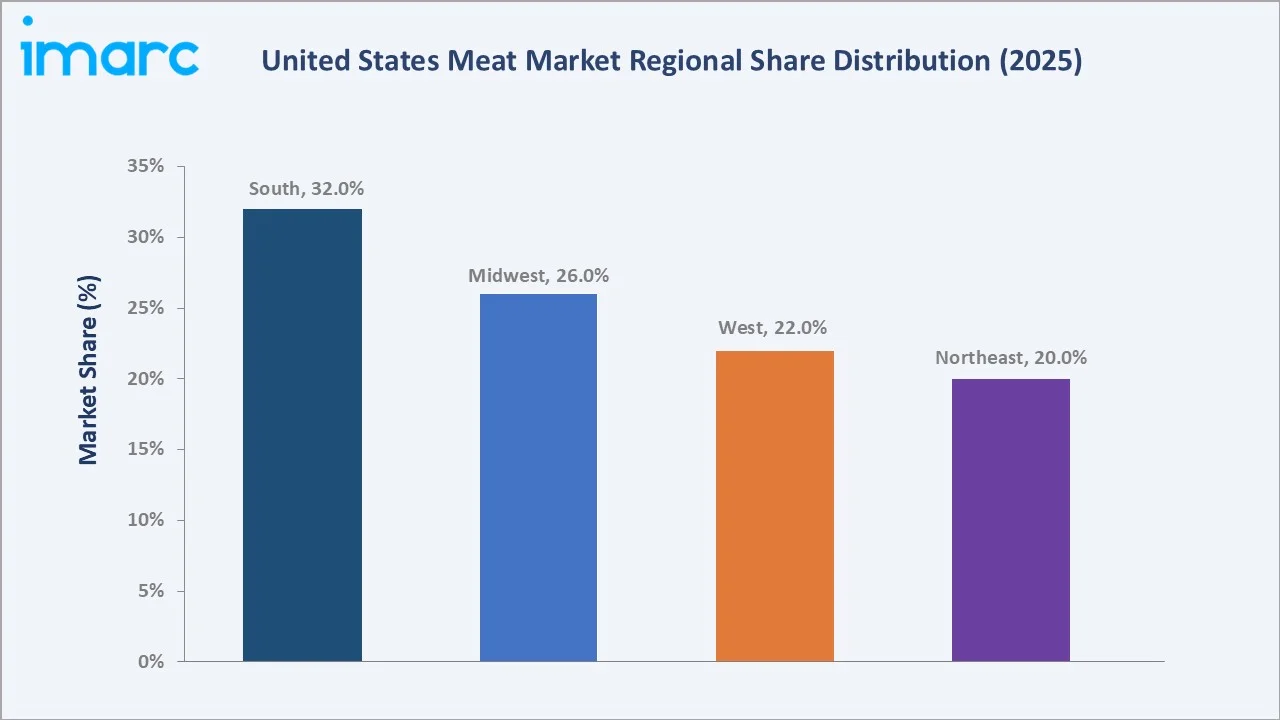

The United States meat market size was valued at USD 370.0 Billion in 2025 and is projected to reach USD 489.9 Billion by 2034, exhibiting a CAGR of 3.17% during the forecast period 2026-2034. Sustained consumer appetite for protein-rich diets, growing preference for premium and organic meat products, and expanded retail distribution infrastructure are driving the United States meat market growth. Raw meat leads the type segment at 70.0% in 2025, while Pork dominates the product segment at 40.0%. The South region accounts for 32.0% of the total United States meat market revenue in 2025, the largest regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 370.0 Billion |

|

Forecast Market Size (2034) |

USD 489.9 Billion |

|

CAGR (2026-2034) |

3.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South (32.0% share, 2025) |

|

Fastest Growing Region |

South |

|

Leading Type |

Raw (70.0%, 2025) |

|

Leading Product |

Pork (40.0%, 2025) |

To get more information on this market, Request Sample

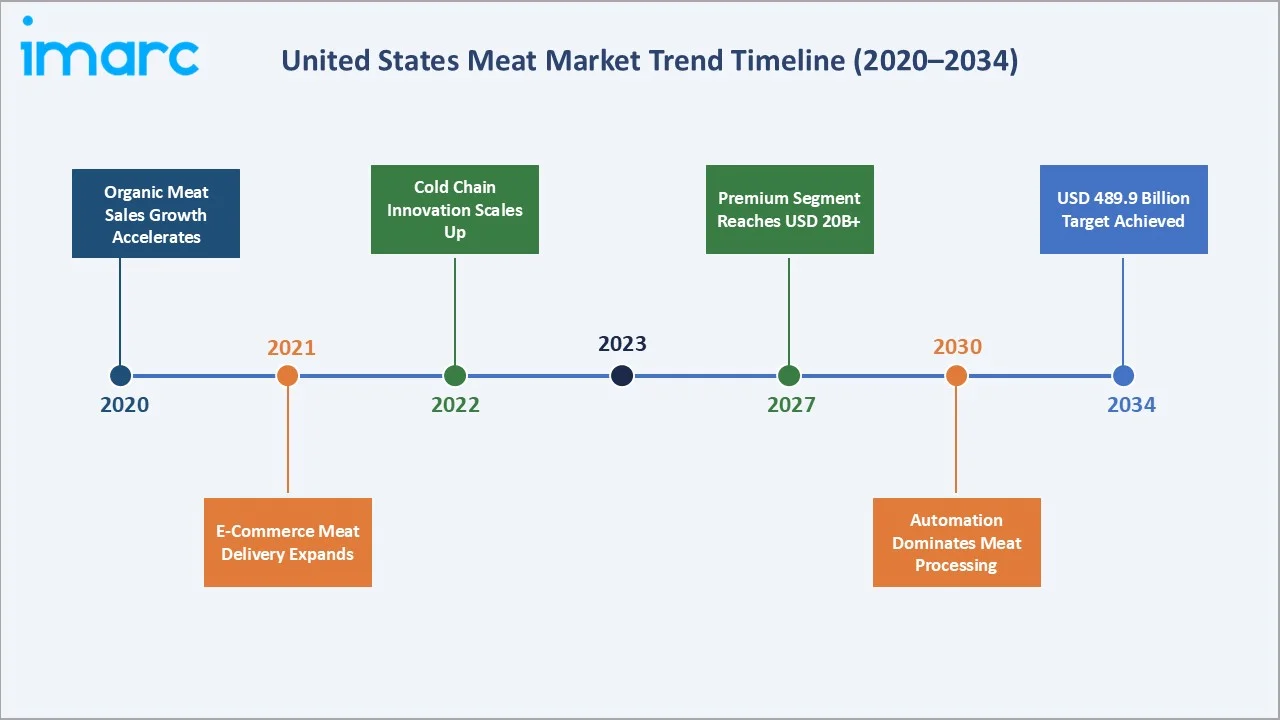

The United States meat market growth trajectory from 2020 through 2034 reflects steady historical expansion. According to the Power of Meat 2025 report, retail meat sales reached a record high of USD 104.6 Billion in 2024, a 2.3% increase year-on-year, confirming enduring consumer demand despite inflationary pressures.

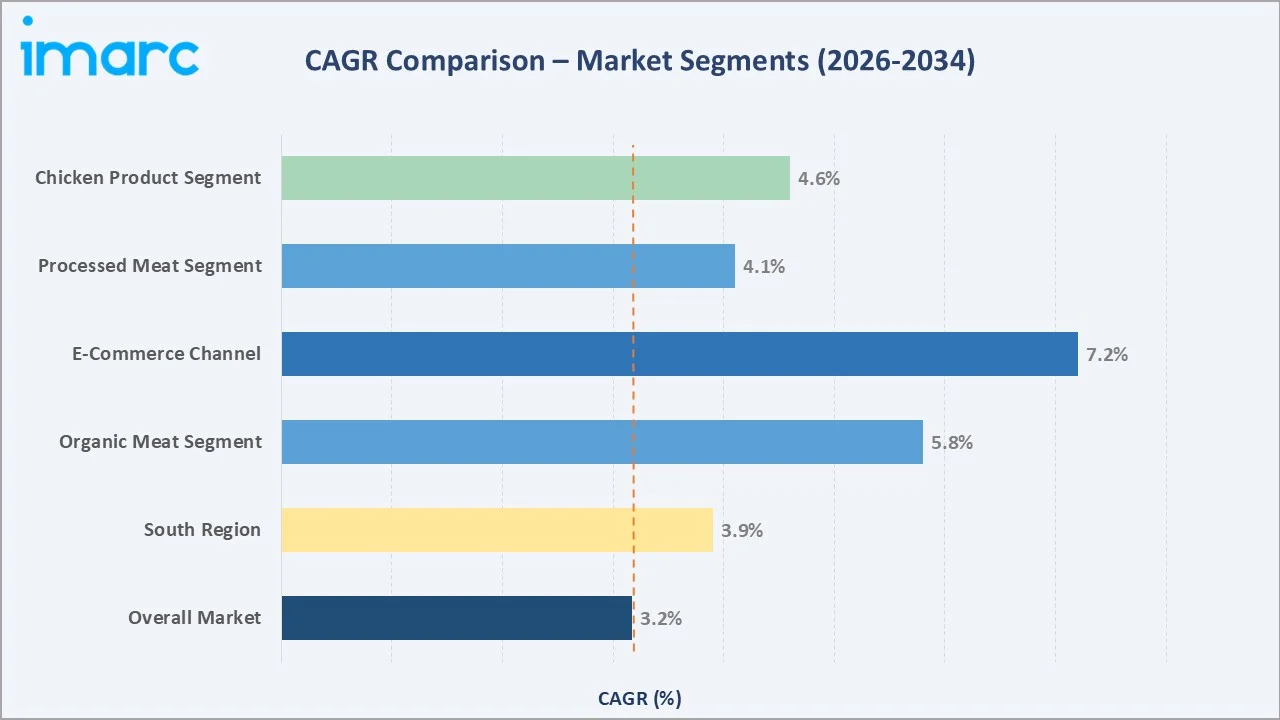

Segment-level CAGR comparisons highlighting e-commerce meat delivery and organic meat as the two fastest-growing sub-categories within the United States meat market through 2034.

Executive Summary

The United States meat market is one of the largest food markets globally, valued at USD 370.0 Billion in 2025 and forecast to reach USD 489.9 Billion by 2034 at a CAGR of 3.17%. Consumer demand for animal protein remains structurally resilient. Health-consciousness is elevating interest in antibiotic-free, grass-fed, and organic varieties. According to the Power of Meat 2025 report, organic meat sales surpassed USD 3 Billion for the first time in 2024, representing a 14.3% year-on-year increase, signaling a strong premiumization wave across the industry.

Raw meat commands a dominant 70.0% share in 2025, underpinned by American household preference for fresh cuts at retail butchery counters. Pork leads the product segment at 40.0%, driven by culinary versatility across fresh, cured, and processed formats. Chicken follows at 28.0%, supported by its health positioning as a lean protein source and widespread use in foodservice applications across quick-service and casual dining channels.

The South region leads at 32.0% in 2025, reflecting its large population base, deeply ingrained barbecue and grilling culture, and a dense foodservice network across Texas and Florida. Supermarkets and hypermarkets remain the dominant distribution channel with 55.0% share. E-commerce meat delivery represents the fastest-growing channel, accelerated by cold chain innovation and direct-to-consumer subscription models.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Raw Meat – 70.0% share (2025) |

|

Largest Product Segment |

Pork – 40.0% share (2025) |

|

Second Product Segment |

Chicken – 28.0% share (2025) |

|

Leading Region |

South – 32.0% revenue share (2025) |

|

Top Distribution Channel |

Supermarkets & Hypermarkets – 55.0% (2025) |

|

Top Companies |

Tyson Foods, Inc., JBS Foods, Cargill, Incorporated, WH Group Limited |

Key Analytical Observations Supporting the Above Data:

- Raw Meat’s 70.0% dominance in 2025 reflects deeply embedded consumer preference for fresh, unprocessed cuts, supported by USDA grading standards, retail butchery infrastructure, and the growth of direct farm-to-table sourcing models.

- Pork’s 40.0% product segment leadership in 2025 is driven by its multi-format utility across fresh cuts, cured products (bacon, ham), and processed variants (sausage, hot dogs), combined with a cost advantage versus beef.

- Chicken at 28.0% is the fastest-growing mainstream protein, underpinned by health positioning, affordability, and rapid innovation in ready-to-cook and pre-seasoned product formats targeting convenience-oriented households.

- The South’s 32.0% regional dominance reflects its position as the most populous and fastest-growing U.S. region, combined with strong barbecue and grilling culture and rapid foodservice expansion in Florida and Texas.

- Supermarkets and hypermarkets retain a 55.0% distribution share in 2025 through broad consumer reach, refrigeration infrastructure, and competitive pricing across all protein categories.

- E-commerce meat retail is the fastest-growing distribution channel, with direct-to-consumer subscription services gaining traction among millennial and Gen Z households seeking convenience and specialty product access.

United States Meat Market Overview

The United States meat market encompasses the production, processing, distribution, and retail sale of fresh, chilled, and frozen meat products, including beef, pork, chicken, mutton, and other proteins across residential and foodservice channels. The market operates through an integrated supply chain spanning livestock rearing, slaughtering and processing facilities, cold chain logistics, and a multi-tier retail and foodservice distribution network.

Applications span household cooking, restaurant and foodservice supply, institutional procurement, and export markets. The United States produces approximately 96 billion pounds of red meat and poultry annually.

Macroeconomic drivers include a stable population, rising household incomes driving premiumization, and evolving dietary trends favouring high-quality animal proteins across all demographic segments.

Market Dynamics

To evaluate market opportunities, Request Sample

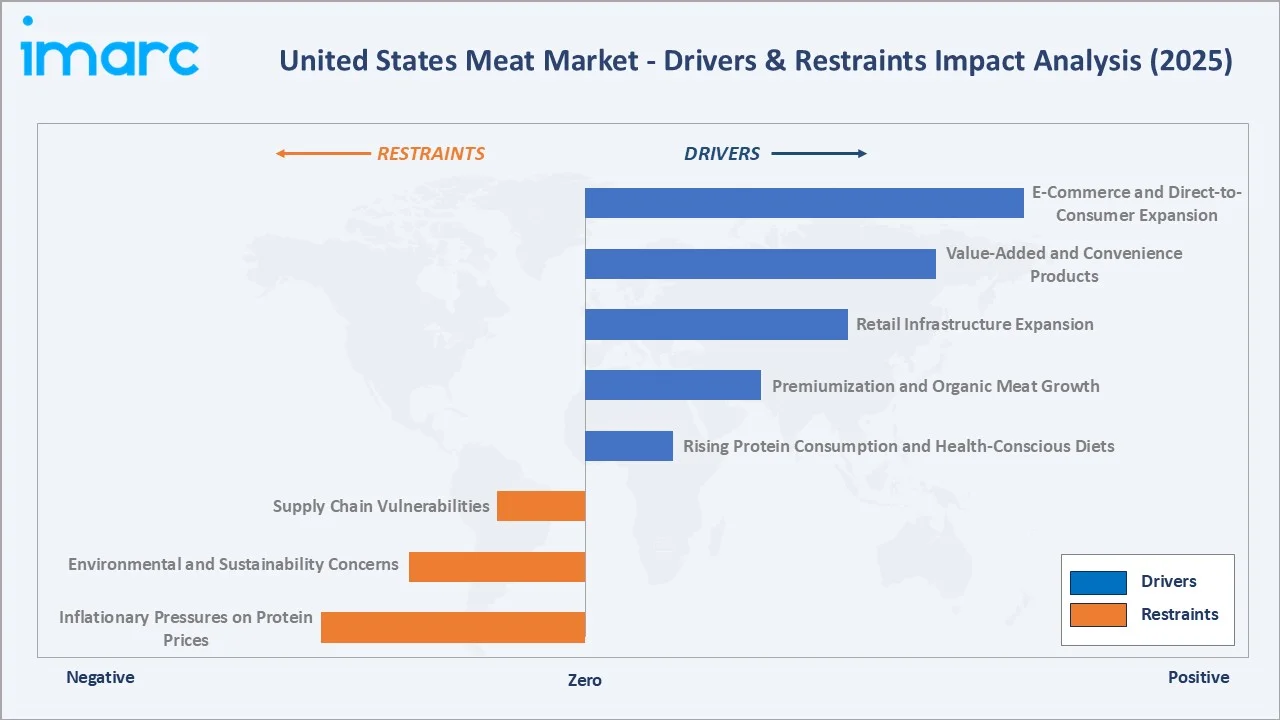

Market Drivers

- Rising Protein Consumption and Health-Conscious Diets: Per capita meat consumption in the United States remains among the world’s highest at approximately 274 pounds per person annually. Growing awareness of dietary protein’s role in muscle health, weight management, and satiety continues to support a steady baseline demand across all age groups.

- Premiumization and Organic Meat Growth: Consumers demonstrate strong willingness to pay premium prices for antibiotic-free, grass-fed, and humanely raised certifications, creating margin-accretive growth opportunities.

- Retail Infrastructure Expansion: Ongoing expansion of supermarkets, warehouse clubs, and specialty grocery stores is improving meat product accessibility across urban and rural markets. In-store butchery counters are being upgraded with display technologies and on-demand custom cutting services.

- Value-Added and Convenience Products: Busy consumer lifestyles are driving demand for pre-marinated cuts, meal kit components, and semi-prepared protein portions.

Market Restraints

- Inflationary Pressures on Protein Prices: Sustained cost inflation in feed grains, energy, and processing labor has increased production costs for meat processors, placing upward pressure on retail prices. Prolonged affordability pressure may trigger protein substitution toward lower-cost alternatives.

- Environmental and Sustainability Concerns: Animal agriculture accounts for approximately 14.5% of global greenhouse gas emissions. Increasing regulatory scrutiny around livestock methane emissions, water use, and manure management is raising operational compliance costs for large-scale producers.

- Supply Chain Vulnerabilities: The COVID-19 pandemic exposed critical vulnerabilities in the highly consolidated meat processing sector. Recurring risks from labor disruptions, disease outbreaks such as avian influenza, and extreme weather events continue to pose intermittent disruption risks.

Market Opportunities

- E-Commerce and Direct-to-Consumer Expansion: Digital meat retail channels are expanding rapidly, with subscription-based services attracting health-conscious and convenience-seeking consumers. The direct-to-consumer model enables premium pricing, subscription revenue streams, and customer data collection unavailable through traditional retail formats.

- Alternative and Hybrid Protein Innovation: Blended products combining conventional protein with plant-based ingredients represent an emerging innovation frontier, meeting demand for reduced-impact protein while maintaining the sensory attributes traditional meat consumers require.

- Export Market Penetration: The United States is a top global meat exporter with strong demand from Japan, South Korea, Mexico, and Canada for premium beef and pork cuts. Continued trade agreement expansion supports incremental volume growth in international markets.

Market Challenges

- Changing Consumer Preferences Toward Plant-Based Proteins: The U.S. plant-based meat alternatives sector has established a meaningful consumer base. Conventional meat companies must invest continuously in product quality, sustainability messaging, and marketing to retain share against evolving dietary alternatives.

- Labor Shortages in Processing Plants: Meat processing operations are labor-intensive with challenging working conditions, contributing to persistent workforce recruitment and retention challenges that increase per-unit operating costs and constrain peak production capacity.

Emerging Market Trends

1. Rising Demand for Clean-Label and Traceable Meat Products

Consumers increasingly demand full transparency in meat production, from farm origin and animal welfare standards to antibiotic use and processing methods. QR-code-enabled supply chain traceability is being adopted by leading retailers and processors, allowing consumers to verify product provenance through mobile applications. Investment in blockchain-based livestock tracking systems and third-party certification programs is accelerating across the industry.

2. Expansion of E-Commerce Meat Delivery and Subscription Services

Online meat retail is growing at a significantly higher rate than conventional channels. Subscription-based direct-to-consumer services are capturing health-conscious and premium-oriented consumer segments. Cold chain logistics innovation, including insulated packaging and next-day delivery capabilities, is extending the geographic reach of online meat retail beyond major urban centers across the United States.

3. Value-Added Product Portfolio Expansion

Meat processors are expanding into higher-margin value-added categories, including pre-seasoned proteins, stuffed cuts, fully cooked entrees, and refrigerated meal kit components. These products reduce consumer preparation time and command 20-40% price premiums over equivalent unprocessed cuts. Tyson Foods, Hormel, and Smithfield have significantly expanded their convenience protein portfolios through 2024-2025.

4. Foodservice and Restaurant Sector Recovery Driving Demand

The post-pandemic recovery of the U.S. foodservice sector continues to generate incremental meat demand. Quick-service restaurants, casual dining chains, and food delivery platforms are expanding premium protein offerings. Beef, chicken, and specialty pork cuts are gaining prominence on menu innovation platforms as consumers seek restaurant-quality protein experiences.

5. Sustainability and Regenerative Agriculture Integration

Leading meat companies are committing to sustainability targets, including reduced emissions, water use reduction, and responsible land management. Regenerative agriculture practices that sequester carbon, restore soil health, and improve watershed management are gaining traction among both producers and retailers as a differentiating environmental narrative aligned with ESG investment criteria.

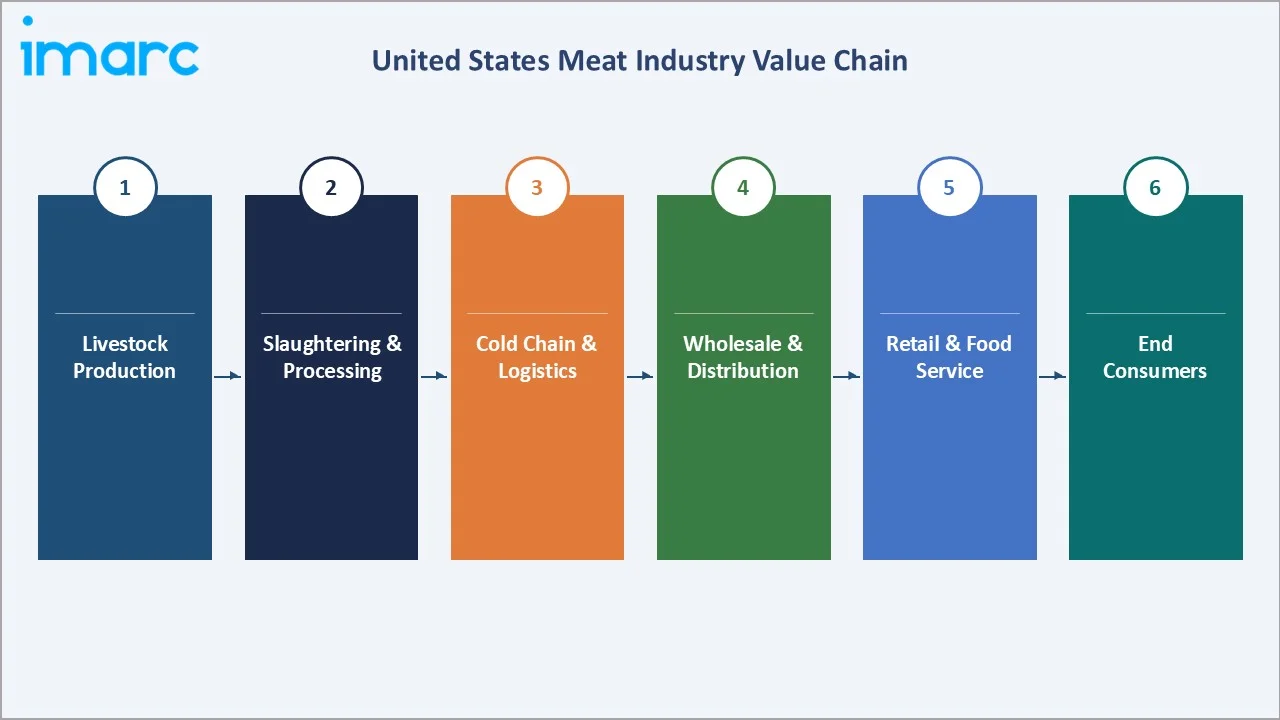

Industry Value Chain Analysis

The United States meat industry value chain spans six integrated stages from primary production through end-consumer delivery. Each stage is characterized by distinct competitive dynamics, capital intensity, and margin profiles.

|

Stage |

Key Players / Activities |

|

Livestock Production |

Fragmented, farmer-owned operations spanning cattle ranches, hog feedlots, and vertically integrated poultry farms; concentrated in the Midwest, South, and Southeast |

|

Slaughtering & Processing |

Highly consolidated; top four processors control approximately 80% of beef slaughter capacity and ~65% of pork processing volume nationally. |

|

Cold Chain & Logistics |

Capital-intensive network of USDA-regulated cold storage facilities, temperature-controlled reefer transport, and IoT-monitored distribution hubs |

|

Wholesale & Distribution |

Multi-tier distribution infrastructure connecting processors to retail chains, foodservice operators, and institutional buyers through national broadline networks. |

|

Retail & Foodservice |

Supermarkets and warehouse clubs dominate at 55% channel share; fastest growth in e-commerce delivery, specialty butcher retail, and QSR premium protein menus. |

|

End Consumer |

Diverse demand base spanning households, foodservice operators, and institutional buyers; supported by premium export demand across Asia-Pacific and North America |

Tier-1 processors occupy the highest strategic value position in the meat value chain. The top four beef processors – Tyson Foods, Inc., JBS Foods, Cargill, Incorporated, and WH Group Limited– collectively control approximately 80% of U.S. beef slaughter capacity, enabling economies of scale while creating systemic concentration risk, as demonstrated during COVID-19 processing disruptions in 2020.

Technology Landscape in the United States Meat Industry

Processing Automation and Robotics

Automation and AI-enabled robotics are increasingly used in meat processing to improve yield, consistency, and efficiency while reducing labor dependency. Leading processors like Tyson Foods and JBS are investing in vision-guided cutting and deboning systems to enhance productivity and optimize high-value meat recovery.

Food Safety and Quality Inspection Technologies

Advanced inspection systems such as X-ray imaging, AI-based vision, and spectroscopy enable real-time detection of contaminants and defects. These technologies improve product consistency, reduce manual inspection, and enhance regulatory compliance.

Cold Chain Innovation and Smart Packaging

IoT-enabled monitoring and smart packaging solutions help maintain temperature control, extend shelf life, and reduce spoilage across the supply chain. Technologies like MAP and freshness indicators improve product quality and minimize waste.

Blockchain-Based Supply Chain Traceability

Blockchain-based traceability systems are being piloted to enable end-to-end product tracking, improving transparency, recall efficiency, and consumer trust in meat sourcing.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Raw |

70% |

2025 |

|

Product |

Pork |

40% |

2025 |

|

Distribution Channel |

Supermarkets and Hypermarkets |

55% |

2025 |

|

Region |

South |

32% |

2025 |

By Type

To access detailed market analysis, Request Sample

The United States meat market is segmented into Raw and Processed categories. Raw meat commands a dominant 70.0% share in 2025, reflecting deeply embedded consumer preference for fresh, unprocessed cuts purchased at retail butchery counters, supermarket fresh departments, and direct-from-producer channels.

Processed meat accounts for 30.0% of the market in 2025, encompassing cooked and cured products such as hot dogs, bacon, deli meats, sausages, and ham. Value-added processed meat innovation – including protein-enriched, clean-label, and reduced-sodium variants – is the primary growth driver within this segment through 2034.

By Product

Pork leads the product segment at 40.0% in 2025. Its dominance reflects multi-format versatility across fresh cuts (chops, tenderloin, ribs), cured products (bacon, ham, prosciutto), and value-processed formats (sausage, hot dogs). Chicken follows at 28.0% share in 2025, driven by health positioning and sustained foodservice demand.

Beef at 20.0% in 2025 retains strong premium positioning, particularly for high-grade steaks, ground beef, and specialty cuts. Mutton and other products collectively represent 12.0% of the market, supported by ethnic cuisine demand growth and specialty retail expansion in urban metropolitan areas with diverse demographic compositions.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South |

32.0% |

Largest population growth rate; BBQ and grilling culture; foodservice expansion across Texas, Florida, Georgia; major processing hubs in Arkansas, North Carolina |

|

Midwest |

26.0% |

Primary beef and pork production zone; Iowa, Kansas, Nebraska feedlot corridor; strong retail penetration in Chicago and Detroit metro areas |

|

West |

22.0% |

Premium and organic meat demand; California leads sustainable protein adoption; affluent consumer segments driving premiumization trends |

|

Northeast |

20.0% |

Urban density supports specialty retail; New York City and Boston are major hubs; growing halal and ethnic protein demand in diverse metro areas. |

The South’s 32.0% share is underpinned by its position as the largest U.S. region by population growth rate, combined with a deeply embedded meat-centric food culture and rapid foodservice expansion across Florida and Texas. The Midwest’s 26.0% share reflects its dual role as both a major production and consumption market, with proximity to feedlots and processing facilities ensuring competitive retail pricing.

The West region at 22.0% is characterized by premium and organic product demand, particularly in California, where sustainability credentials and antibiotic-free products drive above-average per-unit prices. The Northeast at 20.0% benefits from dense urban populations in New York City, Boston, and Philadelphia that support both premium retail and specialty ethnic protein formats.

Competitive Landscape

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Tyson Foods, Inc. |

Jimmy Dean, Ball Park |

Leader |

Largest U.S. meat company; diversified across beef, pork, chicken; strong retail and foodservice presence |

|

JBS Foods |

Pilgrim's, SAMPCO, Swift, Just Bare |

Leader |

World’s largest meat processor; dominant in beef and chicken; top U.S. export position |

|

Cargill, Incorporated |

Excel Fresh Meats, |

Leader |

Major beef and turkey operations; advanced sustainability and traceability programs; privately held |

|

WH Group Limited |

Smithfield |

Leader |

World’s largest pork processor; 6 billion lbs annual output; WH Group subsidiary |

|

MBRF |

Sadia Bassi |

Challenger |

Premium beef specialist; strong, high-grade cut and branded beef programs |

|

Perdue |

Niman Ranch |

Challenger |

Vertically integrated poultry; strong organic and antibiotic-free positioning |

|

Hormel Foods |

Applegate |

Challenger |

Diversified processed meat portfolio; health-focused brand innovation |

The United States meat processing competitive landscape is characterized by a small number of vertically integrated multinational processors. Tyson Foods and JBS USA collectively generate revenues exceeding USD 100 billion annually, establishing dominant market positions across multiple protein categories.

Key Company Profiles

Tyson Foods, Inc.

Tyson Foods is a U.S. meat company and one of the world’s largest food processors. The company operates across beef, pork, chicken, and prepared foods segments.

- Product & Platform Portfolio: Brand portfolio encompasses Jimmy Dean, Ball Park, Hillshire Farm, and State Fair, commanding significant share across retail and foodservice channels covering fresh proteins, value-added convenience formats, and fully prepared meal solutions.

- Recent Developments: In July 2025, Tyson Foods launched innovative protein-packed chicken nuggets with 23 grams of protein per serving made from 100% all-natural white meat chicken, exemplifying the industry's focus on convenient, nutrition-forward products aligned with modern dietary preferences.

- Strategic Focus: Tyson’s strategy centers on automation investment, value-added product portfolio expansion, and sustainability commitments. The company is investing heavily in robotics to reduce processing labor dependency and improve yield efficiency.

JBS Foods

JBS Foods operates across beef, pork, and poultry (through Pilgrim’s Pride) in the United States, with over 60 processing facilities.

- Product & Platform Portfolio: Brands include Swift, Pilgrim’s Pride (chicken), and Certified Angus Beef programs.

- Recent Developments: In March 2026, JBS USA and the National 4‑H Council announced a $750,000 partnership to expand hands-on agricultural education, science-based learning, and leadership development opportunities for young people across rural America.

- Strategic Focus: JBS’s U.S. strategy focuses on premium beef program development, export market capture in Japan, South Korea, and Mexico, and operational efficiency through automation. The company targets above-market growth in premium and organic beef segments.

Hormel Foods

Hormel Foods operates across pork, turkey, and value-added meat products in the United States, with a strong presence in branded retail, foodservice, and refrigerated foods.

- Product & Platform Portfolio: SPAM, Jennie-O (turkey), Applegate (natural/organic meats), Columbus Craft Meats, and Hormel Black Label bacon.

- Recent Developments: In March 2026, Hormel Foods announced leadership changes in global food safety, with a new head appointed to strengthen quality and compliance functions. The company has also continued product innovation through collaborations and new flavor launches across retail and foodservice segments.

- Strategic Focus: Hormel’s U.S. strategy centers on expanding value-added and branded protein offerings, particularly in premium, natural, and organic segments (e.g., Applegate).

Market Concentration Analysis

The United States meat processing market is highly concentrated, particularly in the beef and pork segments. The top four beef processors—Tyson Foods, Inc., JBS Foods, Cargill, Incorporated, and WH Group Limited—collectively account for approximately 80–85% of U.S. fed cattle slaughter capacity, forming a long-standing oligopolistic structure.

The poultry segment is comparatively less concentrated. Tyson Foods, JBS-Pilgrim’s Pride, Wayne-Sanderson Farms, and Perdue Farms collectively control approximately 55% of broiler processing. Regional and specialty processors maintain meaningful niches in organic, antibiotic-free, and direct-to-farm product segments. The acquisition of Sanderson Farms for USD 4.5 Billion in 2022 exemplifies the ongoing consolidation trend expected to continue through the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Premium and organic meat is the highest-growth sub-segment, with organic sales growing at 14.3% year-on-year in 2024 and surpassing USD 3 billion for the first time. E-commerce meat delivery is growing at double-digit rates, enabled by subscription models, cold chain innovation, and digital customer acquisition platforms targeting millennial and Gen Z households.

Emerging Market Expansion

Value-added processing capacity expansion enables processors to capture 20-40% price premiums over commodity fresh meat categories through pre-marinated cuts, sous vide formats, and ready-to-cook portions. Export market development to Japan, South Korea, and Southeast Asia represents a meaningful volume growth lever for premium U.S. beef and pork producers.

Venture & Private Investment Trends

Capital investment in processing automation – robotics-enabled deboning, AI quality inspection, and IoT-monitored cold chain systems – delivers measurable unit cost reductions.

Future Market Outlook (2026-2034)

The United States meat market is projected to reach USD 489.9 Billion by 2034, growing at a CAGR of 3.17% from 2026. Structural growth drivers – including sustained protein demand, premiumization of product portfolios, e-commerce channel expansion, and foodservice recovery – are expected to sustain above-inflation revenue growth throughout the forecast period.

Technological disruption will reshape processing economics through 2034. Robotics, AI-powered quality inspection, and blockchain traceability will become industry standard capabilities. Sustainability imperatives – including scope 3 emissions reduction commitments and regenerative agriculture supply chain programs – will increasingly influence purchasing decisions by institutional buyers and premium consumers.

The competitive landscape will continue to consolidate through further M&A activity among mid-sized regional processors. Innovative direct-to-consumer meat brands and organic-focused regional processors will carve out defensible premium niches competing on quality, transparency, and sustainability credentials. By 2034, the U.S. meat industry is forecast to complete a meaningful transition toward a higher-value, premium-oriented market structure.

Research Methodology

Primary Research

Primary research encompassed structured interviews with meat industry stakeholders, including product directors at major processing companies, retail meat category managers, foodservice procurement executives, cold chain logistics operators, and institutional investors. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments across all protein categories and U.S. regions.

Secondary Research

Secondary sources include USDA Economic Research Service and Foreign Agricultural Service data, North American Meat Institute (NAMI) annual reports, Power of Meat report series (2024-2025), company annual reports and SEC filings, Federal Trade Commission concentration studies, and trade publications including Meat+Poultry, Food Business News, and Progressive Grocer. Regulatory data from USDA FSIS was also incorporated throughout the analysis.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, per-capita protein consumption trends, retail channel evolution data, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty and potential supply chain disruption risks through 2034.

United States Meat Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Raw, Processed |

| Products Covered | Chicken, Beef, Pork, Mutton, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Departmental Stores, Specialty Stores, Online Stores |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Tyson Foods, Inc., JBS Foods, Cargill, Incorporated, WH Group Limited, MBRF, Perdue, Hormel Foods, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the United States Meat Market Report

The United States meat market was valued at USD 370.0 Billion in 2025, driven by strong consumer protein demand and expanding retail distribution across urban and rural areas.

The market is projected to reach USD 489.9 Billion by 2034, growing at a CAGR of 3.17% during 2026-2034, driven by premiumization, e-commerce expansion, and sustained protein consumption.

The United States meat market is expected to exhibit a CAGR of 3.17% from 2026-2034, supported by organic meat growth, convenience product innovation, and distribution infrastructure investment.

Raw leads with a 70.0% share in 2025, reflecting strong consumer preference for fresh, unprocessed cuts purchased through retail butchery counters and supermarket fresh departments.

The South leads with a 32.0% share in 2025, driven by population density, barbecue and grilling culture, and rapid foodservice expansion in Texas and Florida.

Leading companies include Tyson Foods, Inc., JBS Foods, Cargill, Incorporated, WH Group Limited, MBRF, Perdue, and Hormel Foods.

Key trends include rising organic and premium demand, e-commerce channel expansion, value-added convenience products, foodservice recovery, and sustainability integration across the supply chain.

E-commerce growth is driven by subscription-based delivery services, cold chain innovation enabling next-day delivery, and shifting consumer purchasing behavior toward digital grocery channels.

The top four beef processors control approximately 80% of U.S. beef slaughter capacity, reflecting a highly consolidated processing sector with significant scale and cost advantages.

Supermarkets and hypermarkets lead with a 55.0% share in 2025, while e-commerce is the fastest-growing channel supported by specialty direct-to-consumer meat delivery and subscription services.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)