United States Agricultural Robots Market Size, Share, Trends and Forecast by Product Type, Application, Offering, and Region 2026-2034

United States Agricultural Robots Market Size, Share, Trends & Forecast (2026-2034)

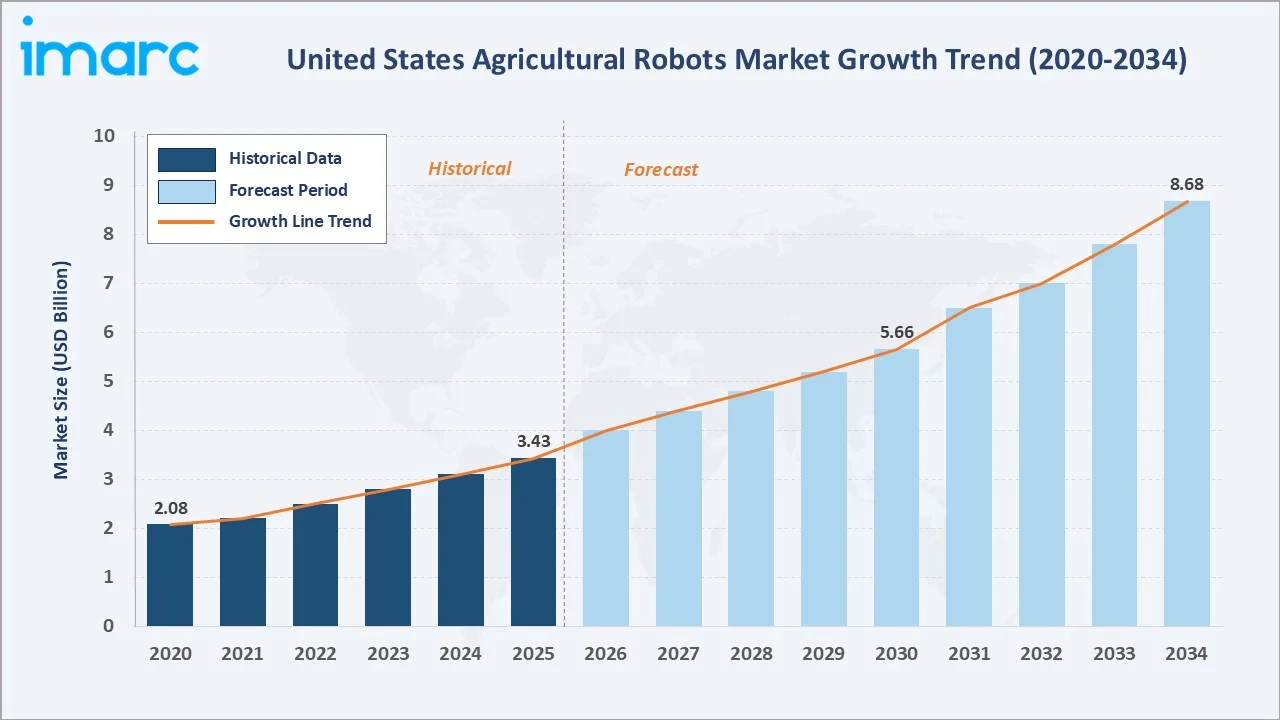

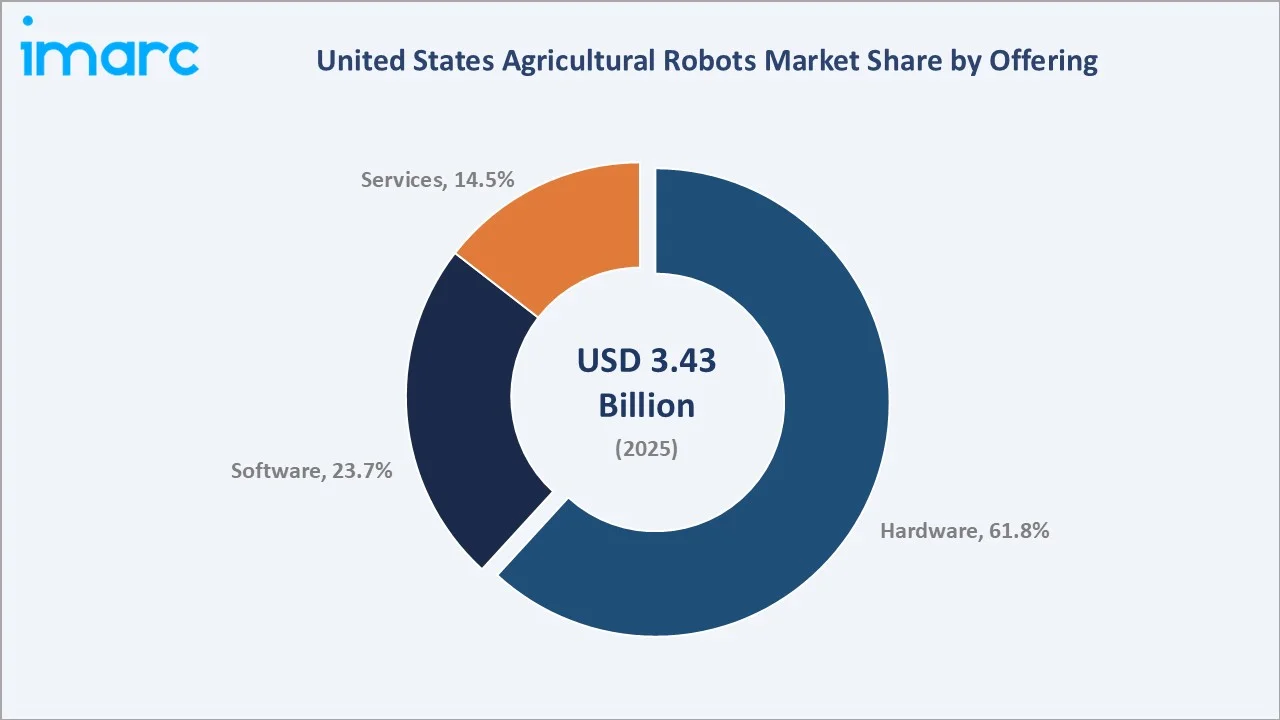

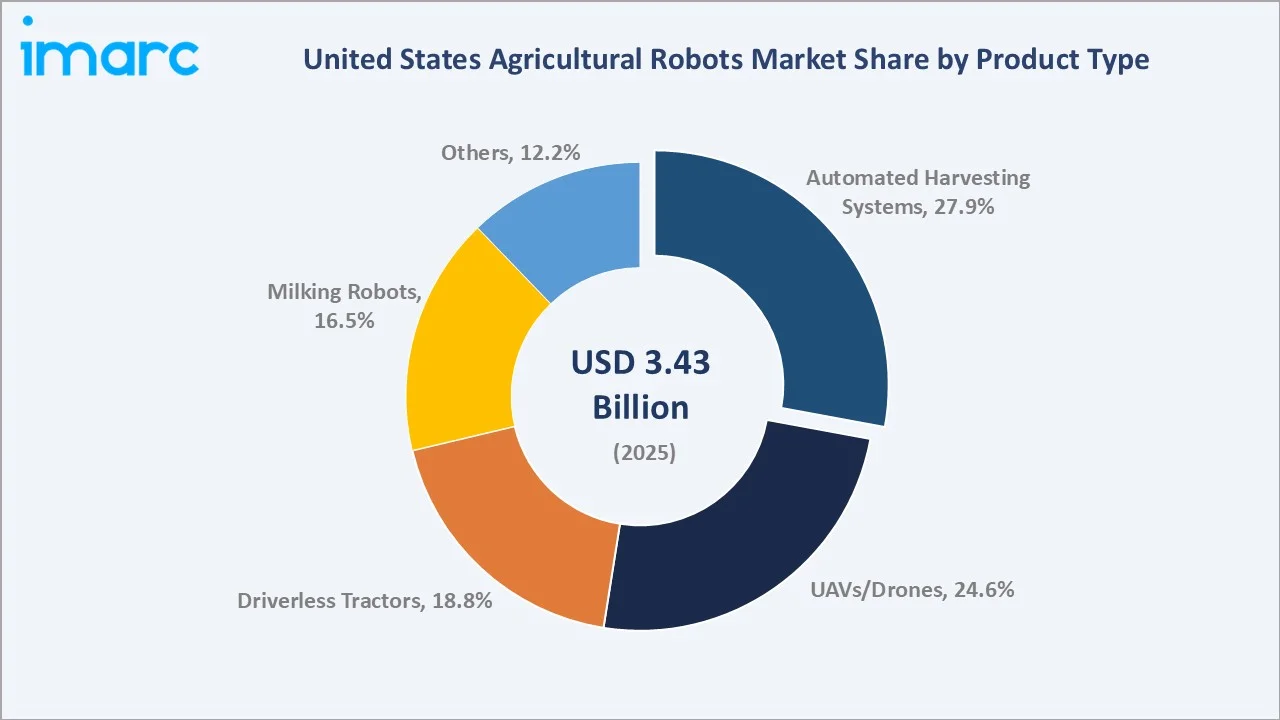

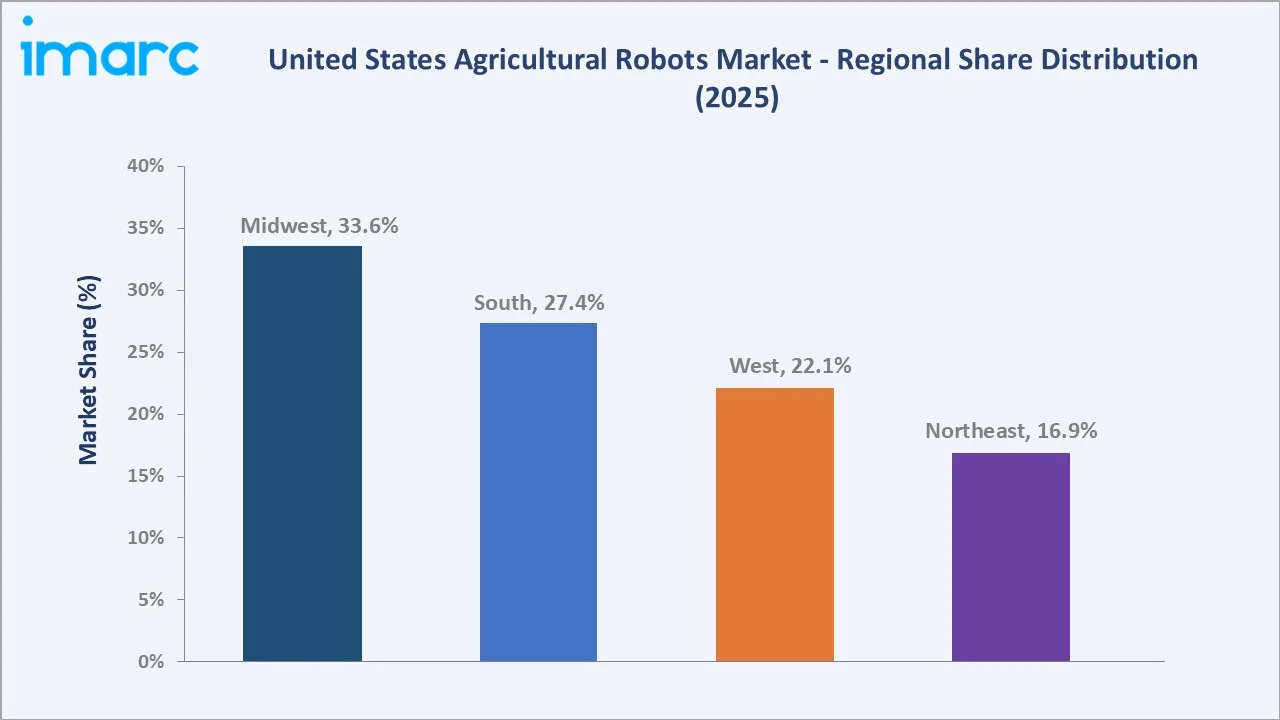

The United States agricultural robots market reached USD 3.43 Billion in 2025 and is projected to reach USD 8.68 Billion by 2034, growing at a CAGR of 10.53% during 2026-2034. The United States agricultural robots market is driven by rising labor shortages and increasing adoption of automation to improve farm productivity and efficiency. Researchers at Michigan State University indicated a 10% drop in domestic farm employment. Hardware leads at 61.8% offering share. Automated harvesting systems dominate product types at 27.9%. The Midwest commands 33.6% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.43 Billion |

|

Forecast Market Size (2034) |

USD 8.68 Billion |

|

CAGR (2026-2034) |

10.53% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Offering |

Hardware (61.8%, 2025) |

|

Largest Product Type |

Automated Harvesting Systems (27.9%, 2025) |

|

Dominant Region |

Midwest (33.6%, 2025) |

The market expanded from USD 2.08 Billion in 2020 to USD 3.43 Billion in 2025, anchored at USD 5.66 Billion in 2030, and forecast to reach USD 8.68 Billion by 2034. COVID-19's exacerbation of the structural farm labor shortage permanently accelerated farmer investment in automation, establishing robotics as an operational necessity rather than an optional technology upgrade across US row-crop and specialty-crop operations.

To get more information on this market, Request Sample

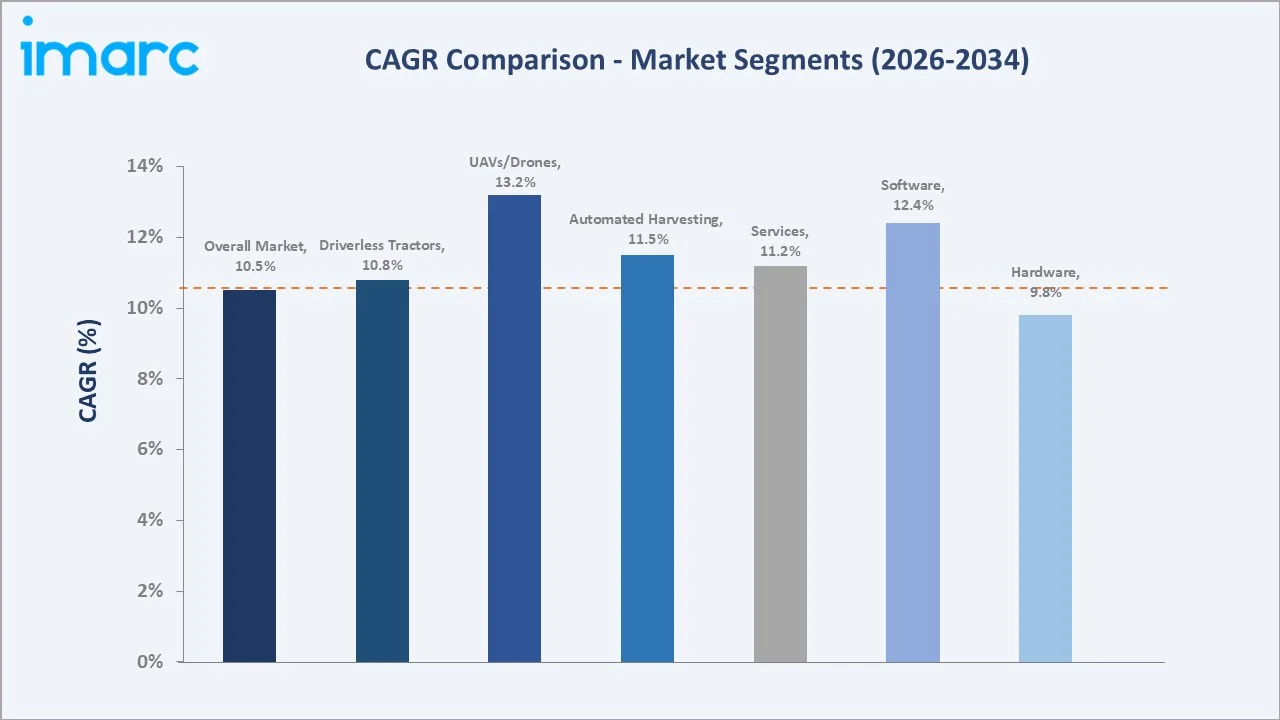

Software grows fastest at ~12.4% CAGR (2026-2034), driven by AI platform subscriptions becoming mission-critical farm management infrastructure. UAVs/drones grow at ~13.2% CAGR, the fastest product type.

Executive Summary

The United States agricultural robots market reached USD 3.43 Billion in 2025, driven by agriculture, food, and related industries, which generated approximately $1.537 trillion in US GDP in 2023, according to data from the Bureau of Economic Analysis. The confluence of a structural farm labor crisis and maturing AI, computer vision, and GPS precision technologies has made robotic automation a commercially viable necessity for US farms of all scales. The market is projected to reach USD 8.68 Billion by 2034 at a 10.53% CAGR.

Hardware dominates at 61.8% (2025), encompassing autonomous tractors, milking robots, and harvesting systems. Automated harvesting systems at 27.9% lead product types as specialty crop farmers in California, Florida, and Washington face the most acute labor shortages. The Midwest at 33.6% leads through its dominance of US row-crop agriculture.

Key Market Insights

|

Insight |

Data |

|

Largest Offering |

Hardware - 61.8% share (2025) |

|

Largest Product Type |

Automated Harvesting Systems - 27.9% share (2025) |

|

Dominant Region |

Midwest - 33.6% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Hardware at 61.8% (2025) reflects the capital-intensive nature of agricultural robot deployment: The hardware dominates the market due to high demand for autonomous tractors, harvesting robots, drones, and precision farming equipment. Significant upfront investment in physical robotic systems and continuous upgrades further drive its leading share.

- Automated harvesting systems at 27.9% addressing speciality crops' critical labor crisis: US specialty crop farmers face the most severe labor shortages among all agricultural sectors. Their efficiency in reducing crop losses and operational costs makes them a preferred solution for large-scale farming operations.

- Midwest at 33.6% share: The Midwest region dominates the market due to its extensive large-scale farms and strong adoption of precision agriculture technologies. High cultivation of row crops like corn and soybeans, along with greater mechanization, drives demand for advanced robotic solutions.

United States Agricultural Robots Market Overview

The United States agricultural robots market encompasses all autonomous and semi-autonomous robotic systems deployed in commercial farming operations, including autonomous tractors, agricultural drones, robotic harvesting systems, milking robots, weeding and cultivation robots, and precision soil management equipment. The market serves US farms across row-crop (corn, soybeans, wheat), specialty crop (fruits, vegetables, nuts), dairy, and livestock operations.

The ecosystem integrates component manufacturers, robot OEMs, AI software platform developers, agricultural dealer networks, and farm operators across the Midwest, South, West, and Northeast agricultural regions. The macroeconomic factors include rising labor costs, farm income fluctuations, and government support for agricultural modernization. Broader trends, including inflation, interest rates, and investments in agri-tech innovation, also impact adoption and capital spending.

Market Dynamics

To evaluate market opportunities, Request Sample

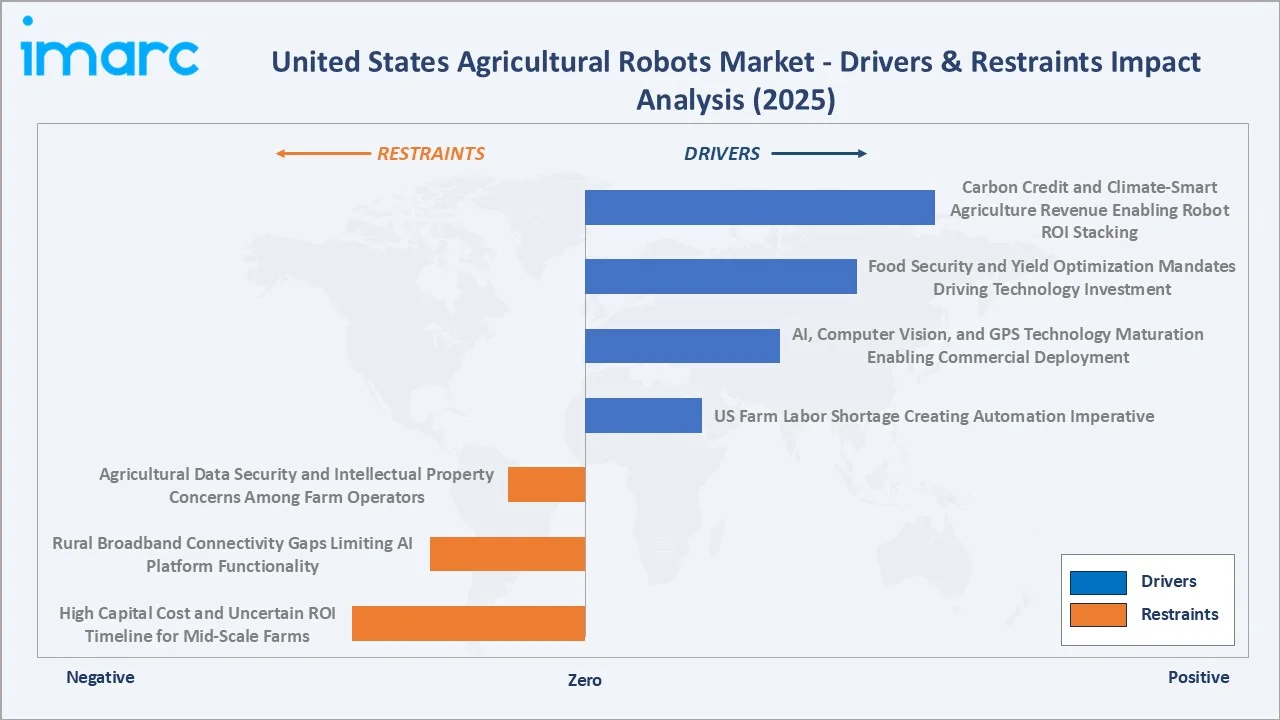

Market Drivers

- US Farm Labor Shortage Creating Automation Imperative: Paid farm labor accounts for 41% of all farm workers in the US. Specialty crop farmers are facing seasonal worker shortfalls in peak harvest periods. This structural labor deficit, not resolvable through visa expansion alone, creates a compelling automation business case across all farm scales.

- AI, Computer Vision, and GPS Technology Maturation Enabling Commercial Deployment: Agricultural robotics was constrained by insufficient sensor accuracy and AI processing capability. AI, computer vision, and GPS technology maturation are enabling precise navigation, real-time crop monitoring, and autonomous decision-making. These advancements improve operational efficiency, reduce labor dependency, and support large-scale commercial deployment of robotic farming solutions.

- Food Security and Yield Optimization Mandates Driving Technology Investment: USDA projects US agricultural output must increase 40% by 2050 to meet domestic and export food security demands with limited additional arable land. Precision agriculture robots provide the productivity multiplier, autonomous tractor operations run 24/7 during weather windows, variable-rate seeding robots optimize plant populations by soil zone, and precision spraying drones reduce input waste.

Market Restraints

- High Capital Cost and Uncertain ROI Timeline for Mid-Scale Farms: Full autonomous farming deployment requires USD 700,000-1,000,000+ in combined investment for a 1,000-acre Midwest row-crop operation, creating adoption hesitancy, particularly amid commodity price volatility that affects annual farm revenue.

- Rural Broadband Connectivity Gaps Limiting AI Platform Functionality: Agricultural robots' AI capabilities depend on cloud connectivity for model updates, data upload, and remote diagnostics. Rural broadband connectivity gaps are hindering the market by limiting real-time data transmission, cloud-based analytics, and remote monitoring capabilities. This reduces the effectiveness of AI-driven platforms, slowing adoption and constraining the full operational potential of autonomous farming solutions.

Market Opportunities

- Carbon Credit and Climate-Smart Agriculture Revenue Enabling Robot ROI Stacking: Carbon credit programs and climate-smart agriculture incentives are creating new revenue streams that improve the return on investment (ROI) for agricultural robots by “stacking” operational savings with environmental payments. For instance, robots enabling precision spraying or no-till farming can reduce emissions and qualify farms for carbon credits, allowing growers to offset equipment costs while enhancing sustainability outcomes.

- Swarm Robotics and Small Robot Economics Democratizing Farm Automation: While large autonomous tractors are accessible only to large-scale farms, the emerging category of small, low-cost swarm robots enables mid-scale and organic farm automation.

Market Challenges

- Agricultural Data Security and Intellectual Property Concerns Among Farm Operators: Farm operators' precision agriculture data has significant commercial value. Data security concerns about multinational equipment companies retaining, analyzing, or selling farm operational data create adoption resistance, particularly among independent farm operators wary of data-driven price leverage by input suppliers and grain buyers.

- Skilled Technician Availability for Agricultural Robot Service and Maintenance: Agricultural robots' mechanical complexity and software sophistication require specialized technician skills not typically available in rural service areas.

Emerging Market Trends

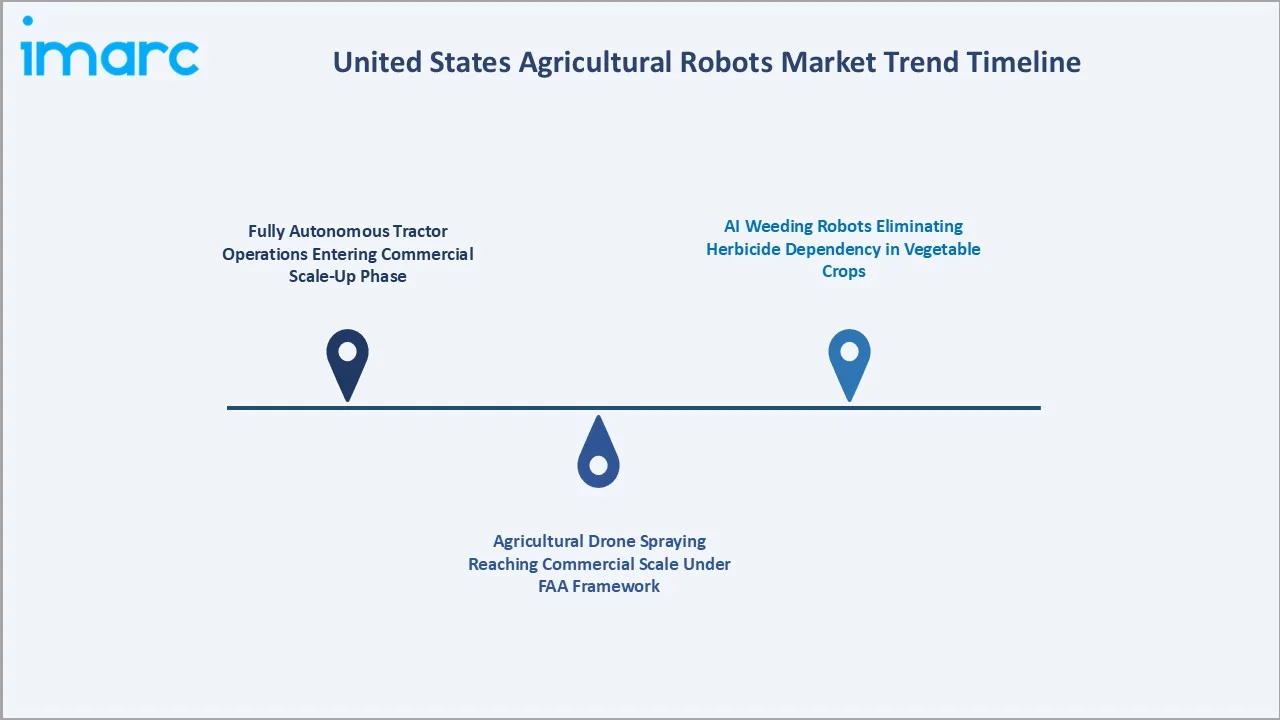

1. Fully Autonomous Tractor Operations Entering Commercial Scale-Up Phase

Fully autonomous tractor operations are entering a commercial scale-up phase as advancements in AI, GPS, and sensor technologies enable reliable, driverless field operations. Growing labor shortages and the need for higher efficiency are accelerating adoption, with large farms increasingly integrating autonomous tractors into routine agricultural workflows.

2. Agricultural Drone Spraying Reaching Commercial Scale Under FAA Framework

Agricultural drone spraying is reaching commercial scale as clearer FAA regulations and approvals enable broader deployment for crop protection and precision application. Improved efficiency, reduced chemical usage, and the ability to cover large or difficult terrain are driving adoption across commercial farming operations.

3. AI Weeding Robots Eliminating Herbicide Dependency in Vegetable Crops

In February 2026, Carbon Robotics introduced the world’s first Large Plant Model (LPM), an advanced AI system for plant detection and identification, trained on a dataset of 150 million labeled plants. The innovation enables farmers to quickly deploy laser weeding across different crops and fields, significantly improving precision and operational efficiency. These platforms are growing where herbicide restrictions and premium organic price premiums provide the strongest ROI.

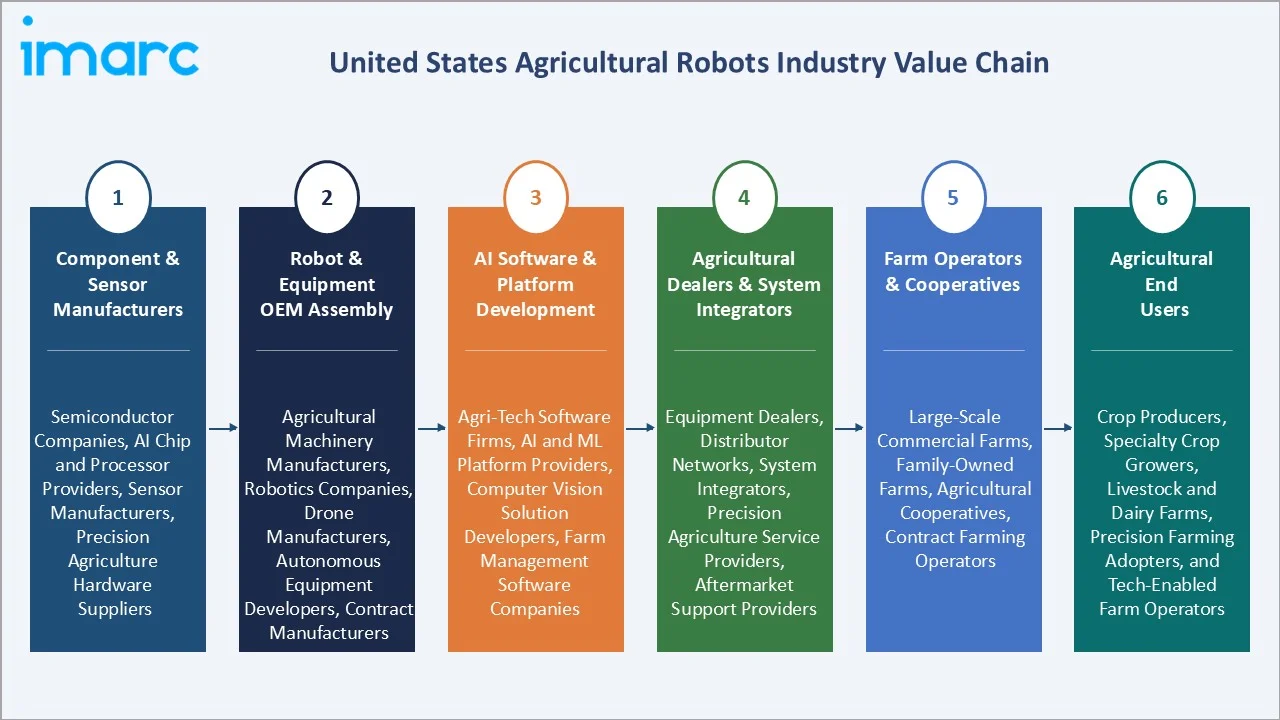

Industry Value Chain Analysis

The United States agricultural robots value chain spans semiconductor and sensor component manufacturing through robot OEM assembly, AI software development, agricultural dealer distribution, and farm operator deployment across US farms. Hardware OEMs capture 40-55% gross margins on premium autonomous equipment; software platform providers earn 60-75% margins on SaaS subscriptions; dealers earn 15-25% on equipment sales plus service contract revenues.

|

Stage |

Key Participants |

|

Component & Sensor Manufacturers |

Semiconductor companies, AI chip and processor providers, sensor manufacturers, and precision agriculture hardware suppliers |

|

Robot & Equipment OEM Assembly |

Agricultural machinery manufacturers, robotics companies, drone manufacturers, autonomous equipment developers, and contract manufacturers |

|

AI Software & Platform Development |

Agri-tech software firms, AI and machine learning platform providers, computer vision solution developers, and farm management software companies |

|

Agricultural Dealers & System Integrators |

Equipment dealers, distributor networks, system integrators, precision agriculture service providers, and aftermarket support providers |

|

Farm Operators & Cooperatives |

Large-scale commercial farms, family-owned farms, agricultural cooperatives, and contract farming operators |

|

Agricultural End Users |

Crop producers, specialty crop growers, livestock and dairy farms, precision farming adopters, and tech-enabled farm operators |

The value chain's most strategically contested layer is the software/data platform tier. Platform lock-in through proprietary equipment telemetry creates compounding competitive advantages as connected equipment data volumes grow.

Technology Landscape in the United States Agricultural Robots Industry

Autonomous Navigation and GPS Guidance Systems

Autonomous navigation and GPS guidance systems form a core part of the agricultural robots technology landscape by enabling precise positioning, path planning, and real-time field navigation for autonomous equipment. These systems integrate RTK-GPS, sensor fusion, and AI-based guidance to improve accuracy, reduce input waste, and support large-scale automation in farming operations.

Computer Vision and AI for Crop and Weed Detection

Computer vision and AI for crop and weed detection, enabling machines to accurately differentiate crops from weeds and perform targeted actions such as precision spraying or laser weeding. These systems use image processing and deep learning to identify plant types in real time, reducing chemical use and improving crop health. AI-powered systems like smart sprayers and robotic weeders can detect multiple weed types with high accuracy and selectively apply herbicides.

Drone Payload and Spraying Technology

Drone payload and spraying technology enable precise, automated aerial application of fertilizers, pesticides, and biological agents with optimized droplet control and variable-rate spraying. These systems integrate sensors, AI, and high-capacity payload tanks to improve coverage efficiency while reducing chemical usage and environmental impact.

Market Segmentation Analysis

By Offering

Hardware leads at 61.8% market share (2025). This encompasses all physical equipment, such as autonomous tractors, agricultural drones, harvesting robots, and precision guidance systems. Hardware grows at ~9.8% CAGR (2026-2034) as new product launches and farm equipment replacement cycles drive sustained capital investment, tempered by price compression from manufacturing scale economies, reducing unit hardware costs 8-12% annually.

To access detailed market analysis, Request Sample

Software at 23.7% grows fastest at ~12.4% CAGR, driven by AI farm management platform SaaS subscriptions serving US agricultural acres. Services at 14.5% encompassing implementation, maintenance, and data analytics services, grow at ~11.2% CAGR as robot deployment scale and operational complexity require specialized ongoing technical support.

By Product Type

Automated harvesting systems lead at 27.9% market share (2025), driven by specialty crop farms' acute labor shortage, creating immediate commercial demand regardless of technology cost. UAVs/drones at 24.6% grow fastest at ~13.2% CAGR as drone spraying and mapping cost-per-acre economics become compelling for Midwest row-crop operators. Driverless tractors at 18.8% are the highest-value per-unit segment.

Milking robots at 16.5% serve the US dairy farms; current penetration below 5% of US dairy herds represents a substantial expansion opportunity as labor economics and milk yield improvements drive adoption. Others at 12.2% encompasses weeding robots, soil management robots, and livestock monitoring systems growing at 10-15% CAGR.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Midwest |

33.6% |

Largest agricultural production hub with extensive corn and soybean farming, strong adoption of precision agriculture and autonomous machinery, and large-scale farms enable higher investment in robotics |

|

South |

27.4% |

Diverse crop production and large-scale farming operations are driving demand for automation, increasing the use of GPS-guided tractors, drones, and irrigation automation |

|

West |

22.1% |

High concentration of specialty crops such as fruits, vegetables, and vineyards, strong demand for harvesting and weeding robots, and a focus on water efficiency and precision farming technologies |

|

Northeast |

16.9% |

Smaller but technologically advanced farms, higher adoption of dairy automation and milking robots, and increasing use of smart farming solutions and data-driven agriculture in high-value crop segments |

The Midwest's 33.6% dominance reflects the geographic concentration of US row-crop agriculture. John Deere's Moline, Illinois headquarters and its densest US dealer network concentration in the Midwest provide both geographic and commercial advantages in autonomous tractor deployment.

The West's 22.1% reflects California's unique agricultural economics in annual crop output concentrated in specialty crops requiring hand labor that faces the nation's most acute farmworker shortage. The Northeast's 16.9% is disproportionately driven by dairy farm robotics.

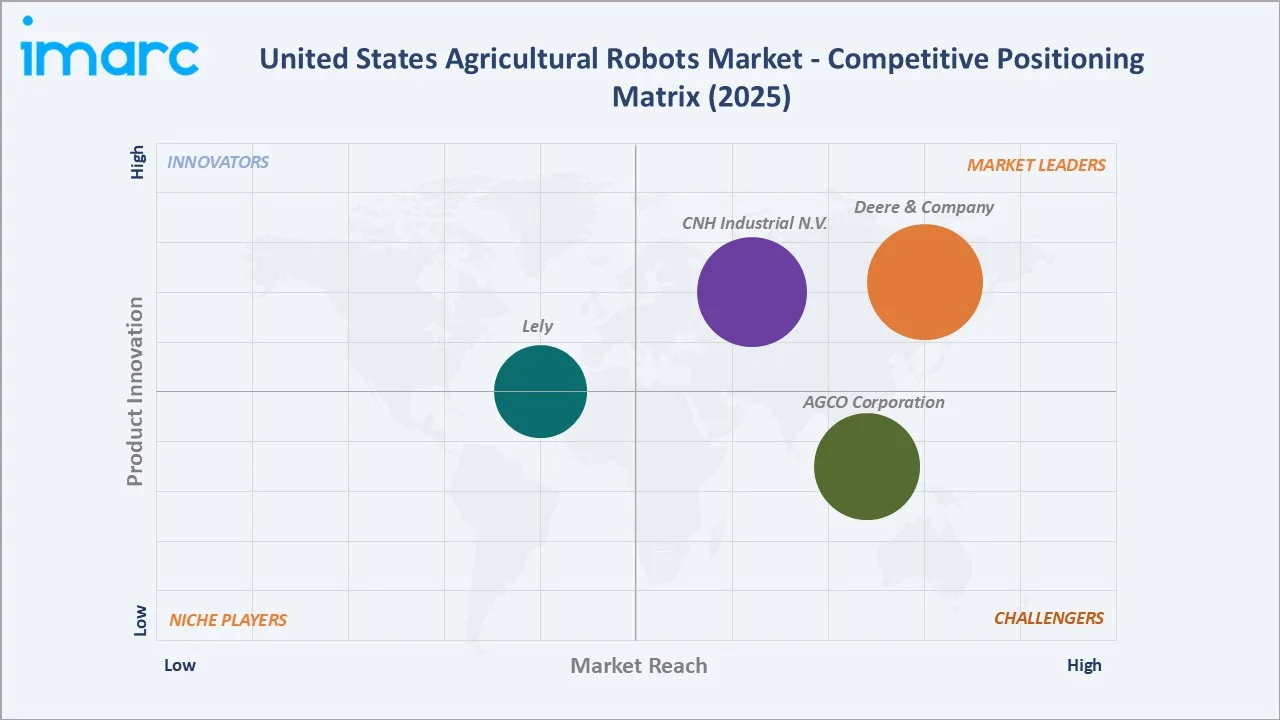

Competitive Landscape

The United States agricultural robots market is moderately concentrated at the large-scale equipment level. The market fragments significantly in specialty robot categories.

|

Company Name |

Brand |

Market Position |

Core Strength |

|

Deere & Company |

John Deere (Autonomous Tractors) |

Market Leader |

One of the world's largest agricultural equipment companies |

|

CNH Industrial N.V. |

Case IH, New Holland Agriculture |

Market Leader |

Raven Industries acquisition (2021) added autonomous guidance and precision spraying |

|

AGCO Corporation |

Fendt, PTx, Valtra, Massey Ferguson |

Strong Challenger |

Fendt is a renowned high-tech brand for customers with the highest demands and sets standards in agricultural technology. Valtra delivers easy-to-use, reliable solutions and highly customized tractors that are tough on the outside and smart on the inside. |

|

Lely |

Astronaut, Vector |

Established Player |

One of the global milking robot pioneers with Astronaut installations |

The competitive landscape is distinguished by a clear bifurcation between legacy agricultural equipment OEMs leveraging existing dealer networks, brand trust, and equipment financing relationships to dominate large autonomous equipment, versus AgTech startup challengers deploying subscription service models to penetrate specialty crop and smaller farm operations that cannot justify large capital equipment purchases.

Key Company Profiles

Deere & Company

Deere & Company is one of the world's largest agricultural equipment companies and the US agricultural robots market's undisputed technology leader.

- Brands: John Deere (Autonomous Tractors).

- Recent Developments: In January 2026, John Deere introduced updates to its Model Year 2027 application portfolio, focusing on improved maneuverability, enhanced visibility, and advanced precision agriculture capabilities. The upgrades include four-wheel steering for better handling, along with new tools and data-driven insights designed to optimize field logistics and streamline farm operations.

- Strategic Focus: Full farm autonomy through connected equipment-software-services platform.

CNH Industrial N.V.

CNH Industrial is also one of the world's largest agricultural equipment companies, operating through Case IH and New Holland brands with a combined agricultural segment.

- Brands: Case IH, New Holland Agriculture.

- Recent Developments: In November 2025, CNH Industrial hosted its 2025 Tech Day at Agritechnica, showcasing a comprehensive portfolio of existing and upcoming technologies under the theme “Every Field Feeds the Future.” The presentation highlighted innovations aimed at supporting farmers and advancing agricultural productivity worldwide.

- Strategic Focus: CNH Industrial N.V. focuses its US agricultural robot strategy on integrating AI, autonomy, and precision technology, aiming to nearly double its precision tech sales.

Market Concentration Analysis

The United States agricultural robots market exhibits moderate concentration in large-scale autonomous tractor systems; John Deere and CNH Industrial together hold approximately 50-55% of autonomous tractor revenues (2025), while drone, harvesting robot, and milking robot markets are substantially more fragmented.

No single platform commands a dominant US market share, and farm management platform switching costs are moderate, creating a competitive market for farmer data and analytics relationships that will determine long-term software revenue concentration. The robotics-as-a-service (RaaS) model represents a potential disruptive force - subscription access to specialized robots without capital purchase could fragment the addressable market away from hardware OEM purchase models toward service contracts.

Investment & Growth Opportunities

Fastest Growing Segments

Software/AI platforms (~12.4% CAGR), UAVs/drones (~13.2% CAGR), services (~11.2% CAGR), AI weeding robots (~30%+ CAGR from a small base), and milking robot expansion from 5% to 15-20% dairy farm penetration represent the highest-growth investment vectors through 2034. The total addressable market for milking robot penetration of US dairy farms represents the largest single-segment expansion opportunity with proven commercial economics.

Emerging Market Opportunities

Some of the US farms currently underserved by large autonomous equipment represent the largest underserved segment addressable through robotics-as-a-service models.

Investment Themes

- Agricultural Software-as-a-Service platforms: Precision agriculture AI platforms generate 60-75% gross margins on recurring SaaS subscriptions versus 40-55% for hardware. Investment in AI crop monitoring, yield prediction, and autonomous equipment management platforms provides superior margin profiles versus hardware-focused competitors.

- Specialty crop harvesting robots: California, Florida, and Washington specialty crop farmers face labor cost exposure that automated harvesting can address at 50-70% of hand labor cost. Companies demonstrating reliable commercial harvesting of strawberries, apples, or lettuce in 2-4 years of operations represent high-conviction investment opportunities in a clearly defined commercial need.

Future Market Outlook (2026-2034)

The United States agricultural robots market is projected to grow from USD 3.43 Billion in 2025 to USD 8.68 Billion by 2034, delivering a 10.53% CAGR over the forecast period. The market's anchor value of USD 5.66 Billion in 2030 reflects the commercial maturation of autonomous tractor scale-up, drone spraying normalization, and accelerating dairy milking robot adoption, three simultaneous deployment waves that each independently exceed high annual revenues by 2030.

Three structural forces define the United States agricultural robots market's growth trajectory with high certainty through 2034: the structural farm labor shortage that is demographic and irreversible creating a non-discretionary automation investment imperative for farms to maintain operational viability; precision agriculture subsidies providing cost-share support that directly reduces farmer capital payback periods, transforming adoption economics for mid-scale operations; and AI technology cost curves that are compressing component costs 8-12% annually while improving capability, systematically expanding the commercial robot feasibility frontier to smaller farms and more delicate crop types.

Research Methodology

Primary Research

Primary research comprised structured interviews with 75+ industry stakeholders (2025), including farm operators across Midwest row-crop, California specialty crop, and Vermont dairy segments; John Deere, CNH Industrial, and AGCO precision agriculture product managers; USDA National Agricultural Statistics Service (NASS) and Economic Research Service (ERS) researchers; FAA agricultural UAS regulatory specialists; and AgTech startup founders from Harvest CROO Robotics, FarmWise Labs, and Carbon Robotics.

Secondary Research

Secondary research encompassed USDA 2024 Agriculture Census preliminary data, USDA NASS Farm Computer Usage and Ownership Survey 2024, FAA UAS Registration and Operations data 2024, USDA ERS agricultural labor availability reports, company investor presentations and earnings disclosures, USDA IRA Inflation Reduction Act conservation program spending reports, and AgFunder AgriFood Tech Investment Report 2024. Over 130 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using bottom-up farm-count x adoption-rate x average-system-revenue models for each product type (autonomous tractors, agricultural drones, milking robots, harvesting systems), validated against company revenue disclosures and USDA equipment expenditure surveys. Key inputs include USDA Census farm count and size distribution data, H-2A visa issuance trend projections, IRA EQIP cost-share program funding allocations through 2030, FAA BVLOS rulemaking timeline scenarios, component cost learning curves, and US dairy farm demographic aging projections.

United States Agricultural Robots Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Unmanned Aerial Vehicles (UAVs)/Drones, Milking Robots, Automated Harvesting Systems, Driverless Tractors, Others |

| Applications Covered | Field Farming, Dairy Farm Management, Animal Management, Soil Management, Crop Management, Others |

| Offerings Covered | Hardware, Software, Services |

| Regions Covered | Northeast, Midwest, South, West |

| Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Lely, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the United States agricultural robots market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the United States agricultural robots market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the United States agricultural robots industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the United States Agricultural Robots Market Report

The US agricultural robots market reached USD 3.43 Billion in 2025, driven by a farm labor shortfall, AgTech subsidies, and drone spraying normalization across Midwest row-crop operations.

The market grows at 10.53% CAGR during 2026-2034, reaching USD 8.68 Billion by 2034, driven by autonomous tractor scaling, drone spraying expansion, milking robot adoption reaching 15-20% of US dairy herds, and software platform SaaS revenue growth.

Hardware leads at 61.8% (2025), encompassing autonomous tractors, agricultural drones, milking robots, and harvesting systems requiring substantial physical capital investment per deployment.

Software grows fastest at ~12.4% CAGR (2026-2034), driven by AI farm management SaaS platforms collectively serving US acres.

Automated harvesting systems lead at 27.9% (2025), driven by specialty crop farms' acute labor shortfall, creating immediate commercial demand for strawberry, apple, and vegetable harvesting robots.

UAVs/drones grow fastest at ~13.2% CAGR, driven by drone spray economics.

The Midwest leads at 33.6% (2025), anchored by 55%+ of US corn and soybean production across 100+ million acres in Illinois, Iowa, Indiana, and Minnesota.

Leading companies include Deere & Company, CNH Industrial N.V., AGCO Corporation, and Lely, among others.

The market reaches approximately USD 5.66 Billion by 2030, with autonomous tractors scaling, drones treating a high number of acres annually, milking robots reaching 10% US dairy penetration, and software platform SaaS high revenues.

Agricultural drones (UAVs) at 24.6% market share cover crop spraying and precision mapping, creating 40-60% operational cost savings versus traditional equipment while enabling variable-rate application and real-time crop health monitoring.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)