Tungsten Carbide Market Size, Share, Trends and Forecast by Grade, Application, Industry Vertical, and Region 2025-2033

Tungsten Carbide Market Size and Share:

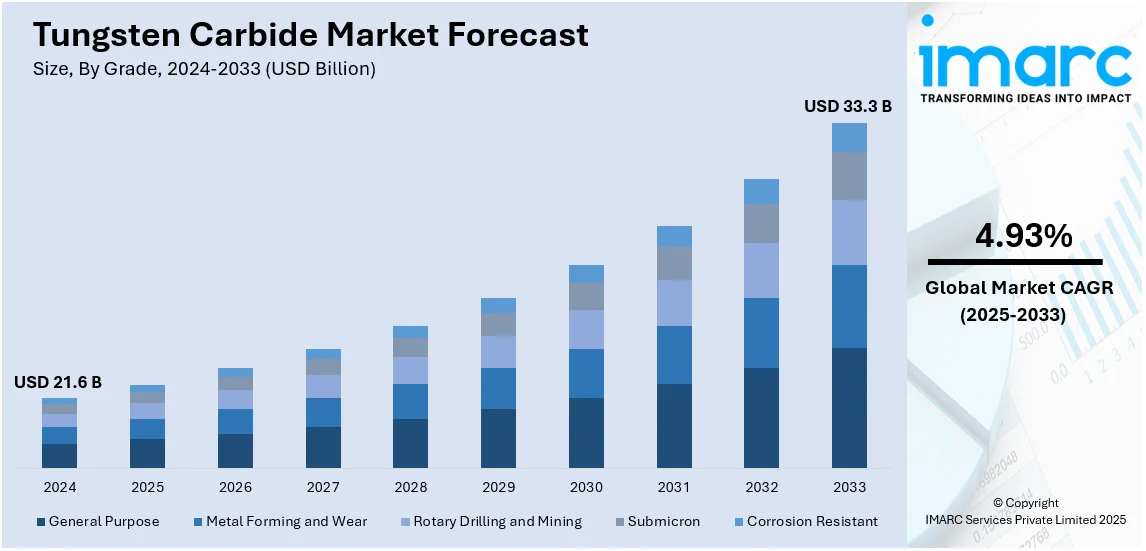

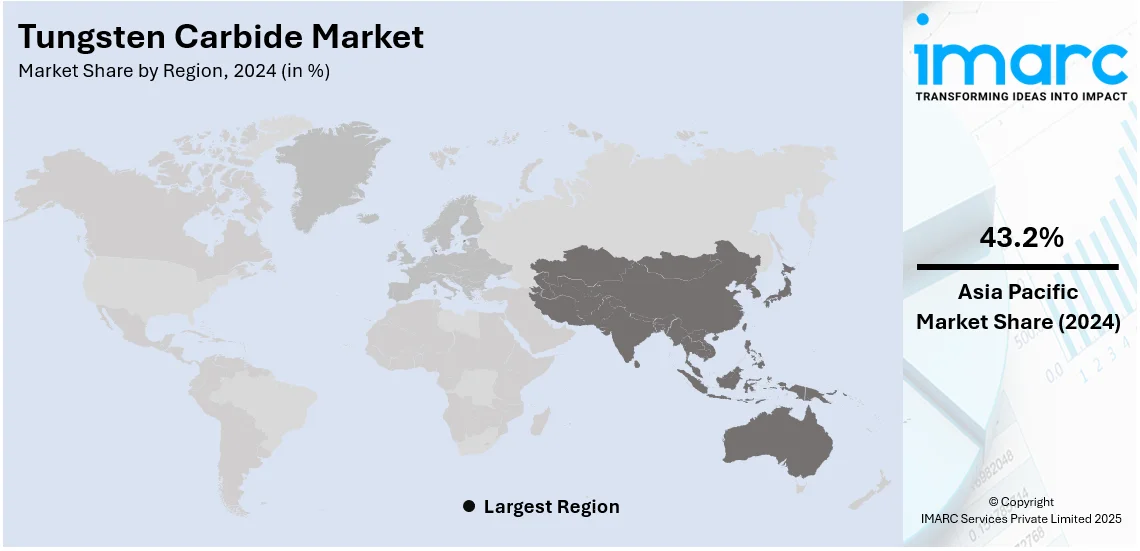

The global tungsten carbide market size was valued at USD 21.6 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 33.3 Billion by 2033, exhibiting a CAGR of 4.93% during 2025-2033. Asia-Pacific currently dominates the market, holding a significant market share of over 43.2% in 2024. This dominance is driven by industrial growth, manufacturing advancements, and the rising product demand across key sectors.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 21.6 Billion |

| Market Forecast in 2033 | USD 33.3 Billion |

| Market Growth Rate 2025-2033 | 4.93% |

The widespread adoption of tungsten carbide in the automotive and aerospace industries is a key driver of the tungsten carbide market growth. Tungsten carbide is widely used in cutting tools, engine components, and wear-resistant parts due to its exceptional hardness, high melting point, and superior durability. For instance, in December 2024, The U.S. Department of Defense declared awarding $15.8 million to Fireweed Metals Corp. to accelerate tungsten mine development at Mactung, Yukon, supporting resource definition, metallurgical testing, feasibility studies, and construction planning. The automotive sector relies on tungsten carbide for precision machining, improving fuel efficiency and extending component lifespan. Similarly, the aerospace industry integrates tungsten carbide in critical applications, such as turbine blades and high-performance drills. With rising production in both sectors, the demand for tungsten carbide is expected to grow, reinforcing its role as a high-performance material.

The United States plays a pivotal role in the tungsten carbide market through advanced manufacturing, innovation, and strategic raw material sourcing. Leading U.S. companies produce high-performance tungsten carbide tools, components, and coatings for industries, such as aerospace, automotive, mining, and defense. This represents one of the key tungsten carbide market trends. For instance, Almonty Industries, a leading global producer of tungsten concentrate, announced partnership with American Defense International to strengthen its U.S. market presence, supporting government policies and the defense sector while advancing its redomiciling and strategic positioning in critical metals. The country leverages cutting-edge technology to enhance product durability, efficiency, and precision machining. Additionally, the U.S. imports and processes tungsten ore to ensure a stable supply chain, reducing dependency on foreign sources. Government initiatives and investments in domestic tungsten production further strengthen the market, positioning the U.S. as a key supplier of high-quality tungsten carbide solutions.

Tungsten Carbide Market Trends:

Rising Automotive Investments Driving Tungsten Carbide Demand

The rapid expansion of the automotive industry is fostering a positive tungsten carbide market outlook, particularly for tungsten carbide applications. For instance, since 2021, automakers have invested over USD 75 billion in the U.S., driving demand for high-performance materials. Tungsten carbide is extensively used in automotive components such as ball joints, brakes, crankshafts, and tire studs, offering superior durability, heat resistance, and wear protection. Additionally, the material is crucial for cutting tools used in manufacturing critical automotive parts, including engines, transmissions, axles, and steering assemblies. This widespread utilization, coupled with increasing vehicle production and technological advancements, is further stimulating tungsten carbide market demand in the automotive sector.

Increasing Demand in Mining Industry

The increase in the demand for tungsten carbide in the drilling and mining industries for the manufacture of drill bits, roller cutters, downhole hammers, and tunnel boring machines is providing a great boost indeed. According to the data from the Department of Statistics and Programme Implementation (MOSPI), for the third quarter of FY23, India's mining GDP stood at Rs. 76,877 crore (USD 9.25 Billion), whereas for the third quarter of FY24, it grew to Rs. 82,680 crore (USD 9.95 Billion). The increase in its use in 3-D printing to manufacture efficient and cost-effective high-performance parts helps drive the demand. Also, the large-scale utilization of the product for surgical instruments in the medical field, including scissors, forceps, blade handles, hemostats, graspers, needle holders, and others, gives another push to the market's expansion.

Growing Demand in Electric Vehicles (EVs) and Renewable Energy

The tungsten carbide market is witnessing increased demand from the electric vehicle (EV) and renewable energy sectors. For instance, a March 2025 report from EV research firm Rho Motion states that U.S. EV sales increased by 28% in the first two months of the year. EV manufacturing requires high-performance cutting tools, wear-resistant coatings, and precision components made from tungsten carbide for battery production, motor components, and powertrain systems. Additionally, the expansion of wind and solar energy projects is driving demand for tungsten carbide-based drilling and cutting tools used in infrastructure development. The shift toward sustainable energy solutions and the increasing focus on energy efficiency are expected to create long-term growth opportunities for tungsten carbide in advanced machining and high-performance material applications.

Tungsten Carbide Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global tungsten carbide market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on grade, application, and industry vertical.

Analysis by Grade:

- General Purpose

- Metal Forming and Wear

- Rotary Drilling and Mining

- Submicron

- Corrosion Resistant

Rotary drilling and mining stand as the largest grade with 34.7% of the tungsten carbide market share in 2024, driven by increasing mining activities, oil & gas exploration, and infrastructure development. Tungsten carbide is extensively used in drill bits, cutting tools, and wear-resistant components due to its high hardness, toughness, and thermal stability. The growing demand for minerals, metals, and fossil fuels has led to increased adoption of tungsten carbide-based drilling equipment for deep-sea mining, tunneling, and rock excavation. The Asia-Pacific region, particularly China, Australia, and India, leads in mining operations, further boosting demand. Market players focus on enhancing material durability, recycling tungsten from used tools, and developing advanced carbide composites to improve efficiency in rotary drilling and mining applications.

Analysis by Application:

- Machine Tools and Components

- Cutting Tools

- Dies and Punches

- Abrasive Products

- Others

Tungsten carbide is widely used in machine tools and components for its exceptional hardness and wear resistance. It is employed in manufacturing cutting tools, gears, and bearings, ensuring high performance and durability in machining operations. Tungsten carbide’s resistance to abrasion and high-temperature stability allows machine tools to maintain precision and efficiency, driving growth in industries like automotive and aerospace.

Tungsten carbide is integral to the cutting tools market due to its superior hardness and toughness. It is used in drill bits, milling cutters, and turning tools, offering extended tool life and high cutting speeds. Tungsten carbide cutting tools enhance machining efficiency by reducing tool wear, improving surface finish, and enabling precise, high-speed operations in industries like metalworking and manufacturing.

Tungsten carbide is essential in producing dies and punches, which are critical for stamping, molding, and shaping metals and plastics. Its hardness, wear resistance, and ability to withstand high pressures make it ideal for forming tools. Tungsten carbide dies and punches ensure long-lasting performance, reduce production costs, and improve the accuracy and quality of mass-produced parts, driving growth in manufacturing.

Tungsten carbide is a key material in abrasive products, such as grinding wheels, sandpaper, and polishing tools. Its high hardness and wear resistance allow abrasives to maintain sharpness and efficiency over extended periods. By enabling superior surface finishing and material removal, tungsten carbide-based abrasives support industries like automotive, aerospace, and construction, where precision and durability are critical in material processing.

Analysis by Industry Vertical:

- Aerospace and Defense

- Automotive

- Mining and Construction

- Electronics

- Others

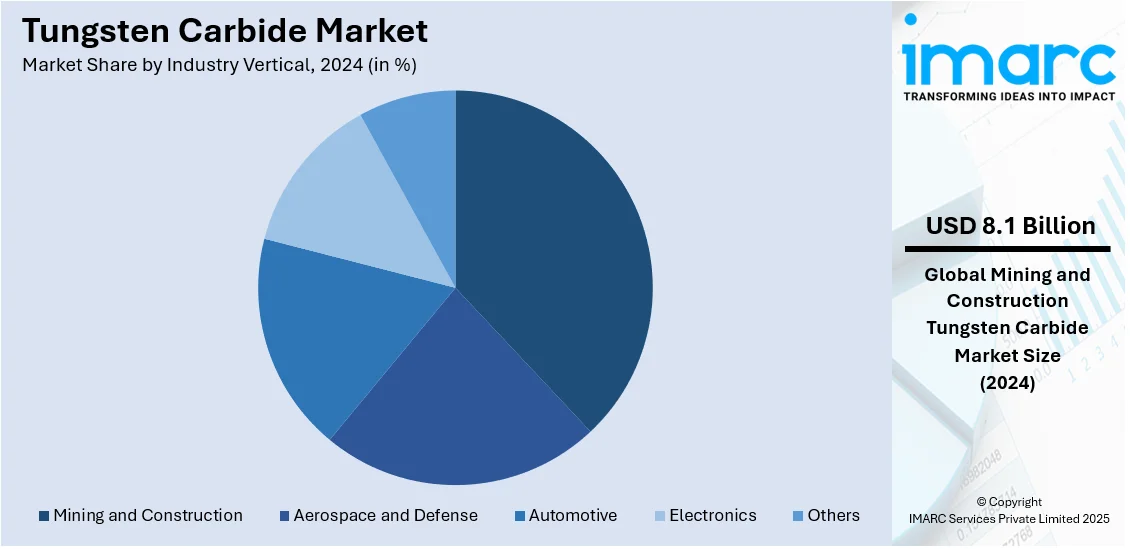

Mining and construction lead the market with a 37.6% share in 2024, driven by increasing infrastructure projects, urbanization, and resource extraction activities. Tungsten carbide-based tools and equipment, including drill bits, cutting tools, wear plates, and tunneling machinery, are essential for high-performance mining and construction applications due to their superior hardness, wear resistance, and durability. The Asia-Pacific region, particularly China, India, and Australia, drives market growth with large-scale mining operations and construction projects. North America and Europe also contribute significantly, focusing on road development, renewable energy infrastructure, and commercial construction. Advancements in powder metallurgy, carbide recycling, and additive manufacturing are further enhancing the performance of tungsten carbide components, solidifying the dominance of mining and construction in the market.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, Asia-Pacific accounted for the largest market with a 43.2% share, driven by strong industrial growth, manufacturing advancements, and increasing demand from key sectors such as automotive, construction, aerospace, and mining. The region’s rapid industrialization, particularly in countries like China, India, and Japan, has spurred the demand for high-performance materials like tungsten carbide, which are critical for cutting tools, abrasives, and manufacturing equipment. The presence of major tungsten carbide manufacturers and suppliers in Asia-Pacific, coupled with the region’s expanding production capabilities and infrastructure, further strengthens its market dominance. Additionally, the growing adoption of precision machining and advanced manufacturing processes in the region fuels the demand for tungsten carbide-based products, supporting its sustained growth in Asia-Pacific.

Key Regional Takeaways:

United States Tungsten Carbide Market Analysis

US accounts for 83.80% share of the market in North America. United States is experiencing an increasing demand for tungsten carbide as the aerospace and defense sector expands, driven by the rising production of military and commercial aircraft. For instance, the United States aerospace and defense industry is currently experiencing significant expansion, with a substantial increase in sales revenue reaching over USD 955 Billion in 2023. The requirement for high-performance materials in aircraft components, turbine blades, and cutting tools is fuelling the use of tungsten carbide due to its durability and heat resistance. The aerospace and defense sector relies on advanced machining tools for precision manufacturing, where tungsten carbide plays a critical role in enhancing efficiency. The development of next-generation fighter jets, space exploration programs, and military advancements further amplify the need for high-strength materials. As aircraft manufacturers adopt lightweight and wear-resistant materials, tungsten carbide becomes essential for structural integrity and extended operational lifespan. The aerospace and defense sector's focus on enhancing performance and reducing maintenance costs strengthens tungsten carbide applications in engine components, nozzles, and armor-piercing ammunition. The integration of cutting-edge technologies and increased defense budgets contribute to a sustained rise in tungsten carbide consumption, reinforcing its significance in the industry.

North America Tungsten Carbide Market Analysis

The North America tungsten carbide market is growing due to increasing demand in automotive, aerospace, mining, oil & gas, and industrial manufacturing. Tungsten carbide is widely used in cutting tools, wear-resistant coatings, drilling equipment, and precision components due to its high hardness, strength, and durability. For instance, in March 2025, American Tungsten Corp. intends to initiate a normal course issuer bid (NCIB) to buy back as many as 500,000 common shares, about 2% of its 25,932,806 shares that are issued and outstanding. This move reflects confidence in the company's financial position and market outlook, particularly within the tungsten carbide industry. The U.S. and Canada drive market expansion with advanced machining and metalworking industries, along with rising infrastructure projects. Growth in electric vehicles (EVs) and energy-efficient technologies further boosts demand for tungsten carbide-based components. Market players focus on recycling tungsten materials and developing nano-structured carbide composites to enhance performance. Stringent environmental regulations and supply chain constraints in raw materials remain challenges, while technological advancements in powder metallurgy and additive manufacturing support market expansion.

Asia Pacific Tungsten Carbide Market Analysis

Asia-Pacific is witnessing a surge in tungsten carbide utilization as the electronics sector continues to expand, driven by advancements in semiconductor manufacturing, consumer electronics, and precision machining. As per the India Brand Equity Foundation, India, recognized as a key manufacturing center, has increased its local electronics output from USD 29 Billion in 2014-15 to USD 101 Billion in 2022-23. The rising demand for microelectronics, circuit boards, and wear-resistant components fuels the adoption of tungsten carbide due to its superior hardness and thermal conductivity. The electronics sector relies on ultra-precision machining tools to manufacture intricate components for smartphones, laptops, and semiconductor wafers, where tungsten carbide plays a crucial role in maintaining dimensional accuracy and longevity. The miniaturization of electronic devices increases the need for high-performance cutting tools and dies, further accelerating tungsten carbide applications. As production capacities expand, manufacturers seek durable materials to enhance efficiency and reduce operational downtime. The electronics sector’s emphasis on high-speed machining and component durability solidifies tungsten carbide’s role in enabling advanced fabrication techniques.

Europe Tungsten Carbide Market Analysis

Europe is witnessing rising tungsten carbide adoption as the automotive sector expands with increasing vehicle ownership, boosting the demand for high-performance machining tools, wear-resistant components, and precision cutting applications. As reported by the International Council on Clean Transportation, approximately 10.6 million new vehicles were registered in the 27 Member States in 2023, reflecting a 14% increase compared to 2022. The automotive sector requires durable materials for engine components, transmission systems, and fuel injection parts, where tungsten carbide offers exceptional hardness and resistance to wear. The rising production of electric vehicles further amplifies the need for high-precision tooling in battery manufacturing and drivetrain components. The automotive sector’s shift towards lightweight materials and fuel-efficient designs increases reliance on tungsten carbide in machining aluminum and composite materials. The expansion of automotive production facilities and growing consumer preferences for advanced vehicle technologies support the increased application of tungsten carbide in high-speed machining, stamping dies, and injection molds. As vehicle ownership rates continue to grow, automakers focus on improving manufacturing efficiency and durability, strengthening the demand for tungsten carbide across the automotive sector’s diverse production processes.

Latin America Tungsten Carbide Market Analysis

Latin America is experiencing increased tungsten carbide demand as the mining sector expands, driven by rising mineral extraction activities and investments in advanced drilling technologies. For instance, Latin America accounts for about 48% of global copper reserves, 20% of global gold reserves, over 60% of global lithium reserves, 50% of global silver reserves, and an unspecified percentage of global potash reserves. The mining sector requires high-strength materials for rock drilling, excavation, and ore processing, where tungsten carbide enhances tool lifespan and operational efficiency. The use of tungsten carbide in drill bits, cutting tools, and wear-resistant components improves productivity in open-pit and underground mining operations. As mineral demand rises, mining companies seek durable solutions to optimize extraction rates and reduce downtime.

Middle East and Africa Tungsten Carbide Market Analysis

Middle East and Africa is witnessing rising tungsten carbide adoption as the Construction sector grows, fuelled by infrastructure development and urban expansion. According to reports, Saudi Arabia's construction sector is booming, with over 5,200 projects currently underway, valued at USD 819 Billion. The construction sector relies on durable materials for heavy machinery, cutting tools, and wear-resistant components, where tungsten carbide enhances equipment performance and longevity. Increased roadways, commercial buildings, and industrial projects drive the need for efficient drilling and cutting applications. The Construction sector’s demand for high-strength materials in tunnelling, concrete processing, and structural fabrication strengthens tungsten carbide usage in key operations.

Competitive Landscape:

The tungsten carbide industry is fiercely competitive, with major companies emphasizing technological progress, product development, and strategic collaborations. Major companies dominate the industry through extensive R&D and high-performance product offerings. For instance, in January 2024, Mitsubishi Materials Europe B.V. acquired HC Starck Holding GmbH expanding tungsten production across Germany, Canada, and China, strengthening its supply chain and tungsten-based tool manufacturing capabilities. Emerging manufacturers are strengthening their positions by investing in advanced manufacturing techniques and expanding production capacity. The market is also witnessing increased mergers and acquisitions to enhance global reach and supply chain efficiency. With rising demand across industries, competition remains intense, prompting companies to differentiate through superior material quality, precision engineering, and cost-effective solutions.

The report provides a comprehensive analysis of the competitive landscape in the tungsten carbide market with detailed profiles of all major companies, including:

- American Elements

- Ceratizit S.A (Plansee SE)

- Extramet AG

- Federal Carbide Company

- H.C. Starck Tungsten GmbH

- Japan New Metal Co. Ltd.

- Jiangxi Yaosheng Tunsten Company Ltd.

- Kennametal Inc.

- Merck KGaA

- OC Oerlikon Management AG

- Reade International Corp.

- Sumitomo Electric Industries Ltd.

- Umicore N.V.

Latest News and Developments:

- December 2024: For HVOF thermal spraying applications, as well as for high wear and corrosion resistance, Wall Colmonoy has launched for WallCarb tungsten carbide powders. These innovative powders enable dense, hard coatings formed with the lowest amount of porosity that improve efficiency in industries such as Oil & Gas as well as Mining. Deposit efficiency and consistency are enhanced with spherical, spray-dried, and sintered shapes.

- December 2024: Hyperion Materials and Technologies have acquired TEMSA Metallurgical Group for deepening its presence in Europe concerning custom tungsten carbide wear parts and tooling. TEMSA’s competence in precision tooling and hard materials will surely add to Hyperion’s strength concerning wear applications. After this acquisition, TEMSA now becomes the first of Europe for Hyperion’s Precision Solutions business.

- November 2024: The advent of Kazakhstan's first tungsten processing plant in Almaty, the first for its jurisdiction, is expected to stir the mining sector into significant action. The plant will process 300 million dollars of ore per year for 3.3 million tons and get 65 concentrations of tungsten. Future plans include an investment of 150 million dollars to refine tungsten up to 88.5 percent purity and develop high-purity tungsten carbide.

- September 2024: Kennametal Inc. broadens its tooling and wear protection offerings for mining with highly advanced tungsten carbide alternatives. The Defender™ Round Drill Steel System offers improved safety and efficiency of operation in combat with these innovations while PrimePoint™ PCD-tipped cutting tools have wear resistance at its best. Various mining needs are efficiently addressed by these improvements in uptime and operational time.

- March 2024: Hardide Coatings announces the commissioning of its tungsten carbide CVD-coated JP-5000 4" copper nozzle for HVOF thermal spray systems. This extends the nozzle life as much as 40 times, making it stronger and at lower cost. First production orders have already been shipped, as interest from both manufactures and thermal spray organizations is very strong.

Tungsten Carbide Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Grades Covered | General Purpose, Metal Forming and Wear, Rotary Drilling and Mining, Submicron, Corrosion Resistant |

| Applications Covered | Machine Tools and Components, Cutting Tools, Dies and Punches, Abrasive Products, Others |

| Industry Verticals Covered | Aerospace and Defense, Automotive, Mining and Construction, Electronics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | American Elements, Ceratizit S.A (Plansee SE), Extramet AG, Federal Carbide Company, H.C. Starck Tungsten GmbH, Japan New Metal Co. Ltd., Jiangxi Yaosheng Tunsten Company Ltd., Kennametal Inc., Merck KGaA, OC Oerlikon Management AG, Reade International Corp., Sumitomo Electric Industries Ltd. and Umicore N.V. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the tungsten carbide market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global tungsten carbide market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the tungsten carbide industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The tungsten carbide market was valued at USD 21.6 Billion in 2024.

IMARC estimates the tungsten carbide market to reach USD 33.3 Billion by 2033, exhibiting a CAGR of 4.93% during 2025-2033.

Key factors driving the tungsten carbide market include the growing demand for high-performance materials in industries like automotive, aerospace, and mining, technological advancements in manufacturing, increased use in cutting tools and abrasives, and the need for durable, wear-resistant components. Additionally, industrial growth in emerging economies contributes significantly to market expansion.

Asia Pacific currently dominates the market with a 43.2% share, driven by strong demand from industries such as mining, construction, automotive, and aerospace. Countries like China, India, and Japan contribute significantly to market growth due to their large-scale manufacturing, infrastructure development, and increasing industrial activities across the region.

Some of the major players in the tungsten carbide market include American Elements, Ceratizit S.A (Plansee SE), Extramet AG, Federal Carbide Company, H.C. Starck Tungsten GmbH, Japan New Metal Co. Ltd., Jiangxi Yaosheng Tunsten Company Ltd., Kennametal Inc., Merck KGaA, OC Oerlikon Management AG, Reade International Corp., Sumitomo Electric Industries Ltd. and Umicore N.V., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)