Trade Management Market Size, Share, Trends and Forecast by Component, Functionality, Deployment Type, Enterprise Size, End-Use Sector, and Region 2026-2034

Global Trade Management Market Size, Share, Trends & Forecast (2026-2034)

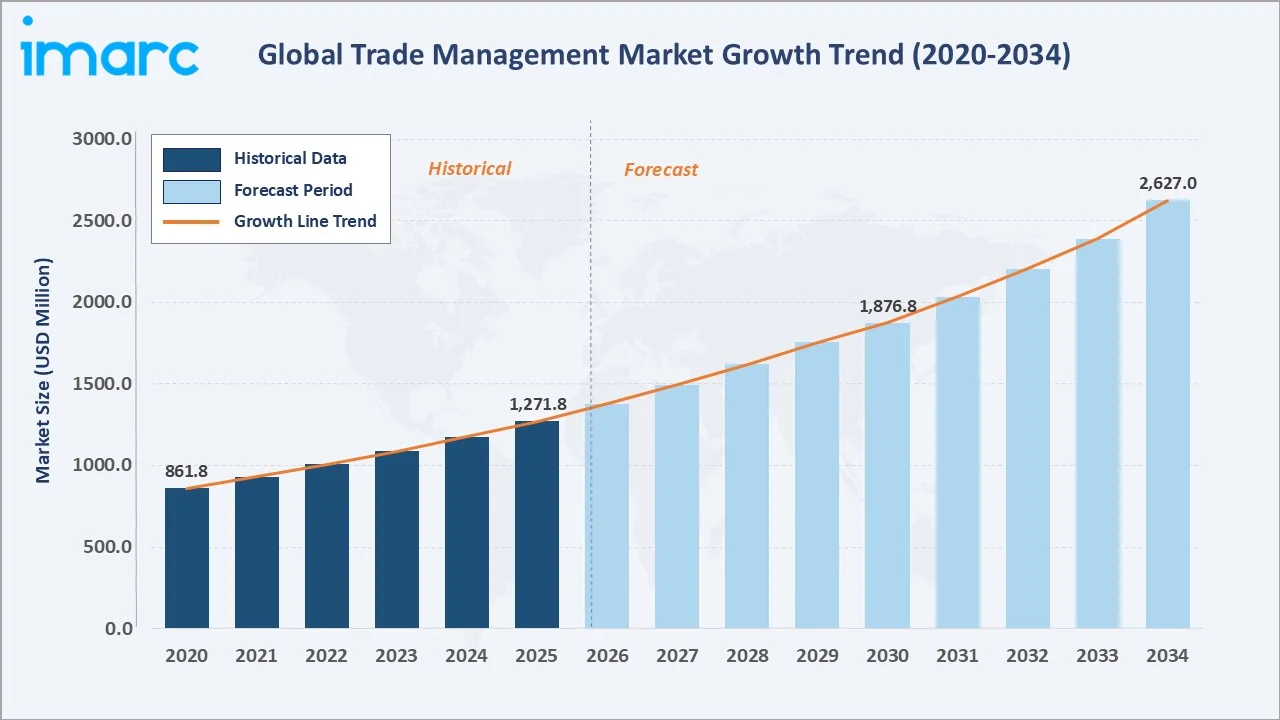

The global trade management market size reached USD 1,271.8 Million in 2025 and is projected to reach USD 2,627.0 Million by 2034, exhibiting a CAGR of 8.1% during 2026-2034. Rising complexity of cross-border trade operations, rapid globalization, and the integration of artificial intelligence (AI) and automation are primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,271.8 Million |

|

Forecast Market Size (2034) |

USD 2,627.0 Million |

|

CAGR (2026-2034) |

8.1% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

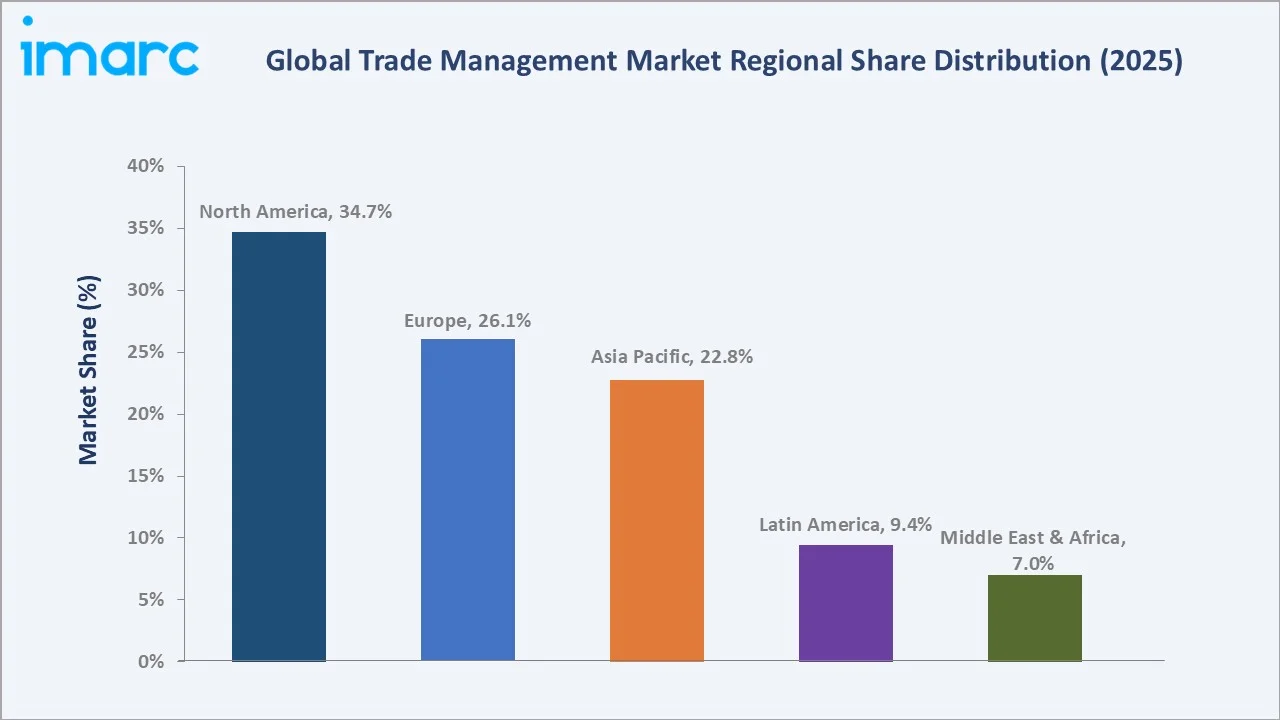

Largest Region |

North America (34.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (~9.8% CAGR) |

|

Leading Component |

Solutions (58.4%, 2025) |

|

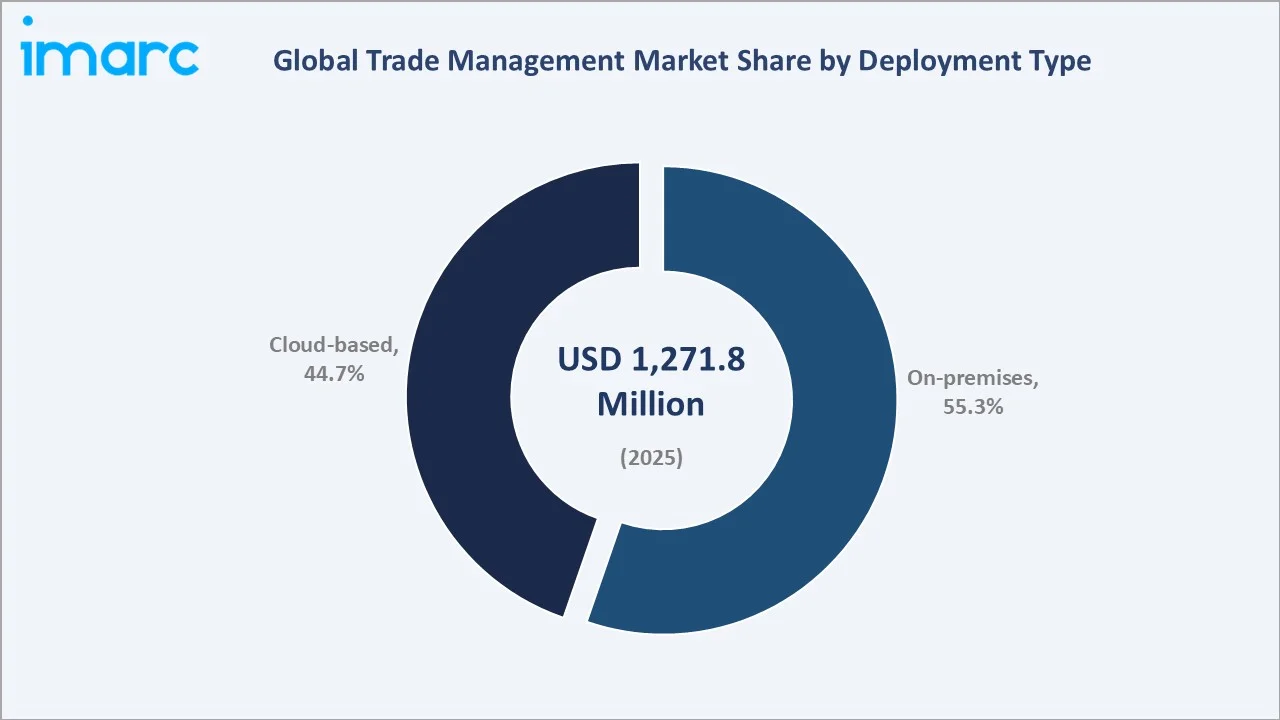

Leading Deployment Type |

On-premises (55.3%, 2025) |

The chart below illustrates the global trade management market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve driven by globalization, regulatory mandates, and AI-enabled trade automation.

To get more information on this market, Request Sample

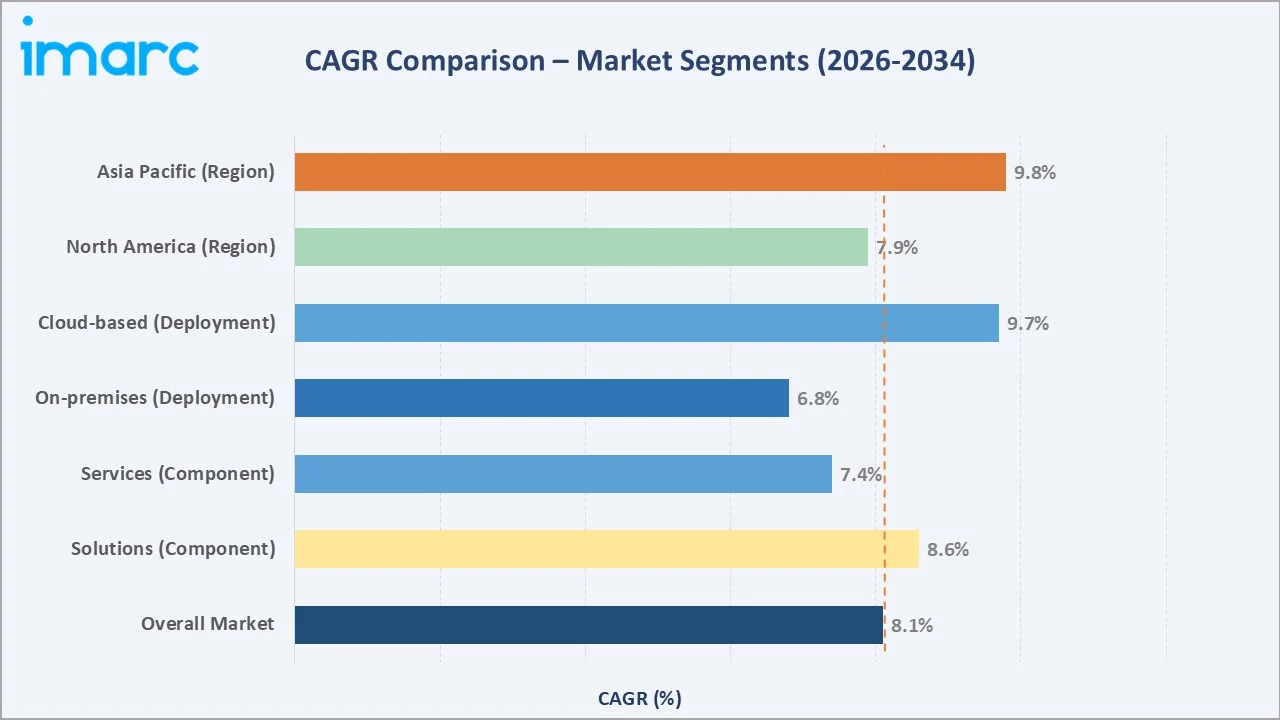

Segment-level CAGR comparisons highlighting cloud-based deployment adoption and Asia Pacific regional expansion as the fastest-growing sub-categories within the global trade management market forecast through 2034.

Figure 2: CAGR Comparison – Trade Management Market Segments (2026-2034)

Executive Summary

The global trade management market is experiencing robust structural growth, driven by accelerating globalization, escalating regulatory compliance demands, and rapid adoption of digital technologies across enterprises. Valued at USD 1,271.8 Million in 2025, the market is forecast to reach USD 2,627.0 Million by 2034, registering a CAGR of 8.1%. Growth from USD 861.8 Million in 2020 reflects a decade of structural demand expansion in enterprise trade operations.

Solutions accounted for 58.4% of market revenue in 2025, underpinned by broad deployment across customs compliance, trade finance, and import-export documentation workflows. North America leads with 34.7% of global revenue in 2025, anchored by the United States - the world largest market for enterprise trade compliance solutions.

The trade management market outlook remains strongly positive, with AI, blockchain, and real-time supply chain visibility emerging as transformational forces through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Solutions – 58.4% share (2025) |

|

Second Component |

Services – 41.6% share (2025) |

|

Leading Deployment Type |

On-premises – 55.3% share (2025) |

|

Fastest Growing Deployment Type |

Cloud-based – ~9.7% CAGR (2026-2034) |

|

Leading Region |

North America – 34.7% revenue share (2025) |

|

Top Companies |

SAP SE, Oracle, e2open, LLC., The Descartes Systems Group Inc, Kinaxis Inc., LSEG, MIC Datenverarbeitung GmbH |

|

Market Opportunity |

AI-driven compliance automation; Asia Pacific expansion |

Key analytical observations supporting the above data:

- Solutions' 58.4% dominance in 2025 reflects broad enterprise adoption for customs classification, trade compliance, and import-export documentation workflows, with SAP Global Trade Services and Oracle GTM Cloud leading procurement decisions in Fortune 500 companies.

- Services' 41.6% share is underpinned by demand for consulting, implementation, and managed trade compliance services - especially among multinational corporations navigating RCEP, USMCA, and EU Customs Code frameworks simultaneously.

- On-premises deployment's 55.3% majority is sustained by stringent data governance requirements in aerospace, defense, and healthcare sectors, where classified shipment data and export control mandates (EAR/ITAR) preclude cloud migration.

- Cloud-based platforms' ~9.7% CAGR reflects accelerating SME adoption and large enterprise cloud transformation, with SaaS-based trade management significantly lowering total cost of ownership compared to legacy on-premises systems.

- North America's 34.7% global leadership is anchored by U.S. Trade Compliance and CBP enforcement rigor, with American importers and exporters, driving compliance software investment.

- Asia Pacific's emergence as the fastest-growing region at ~9.8% CAGR This reflects RCEP-driven trade growth, rising cross-border e-commerce volumes in China, and India’s 2023 Foreign Trade Policy digitalization initiatives.

Global Trade Management Market Overview

Trade management encompasses software solutions and consulting services designed to automate, optimize, and ensure compliance across the full lifecycle of international trade - from order management and customs classification to trade finance, duty optimization, and export controls.

The ecosystem integrates enterprise resource planning (ERP) platforms, customs authorities, freight forwarders, financial institutions, and regulatory bodies. Macroeconomic forces driving adoption include heightened geopolitical trade volatility, post-pandemic supply chain restructuring, and escalating cross-border e-commerce.

Enterprises across manufacturing, retail, logistics, aerospace, and healthcare rely on trade management platforms to reduce compliance risk, optimize landed costs, and achieve real-time shipment visibility across multi-tier global supply networks.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Rising Complexity of International Trade Transactions: The globalization of supply chains has dramatically increased cross-border transaction complexity. Enterprises managing suppliers across numerous countries increasingly rely on advanced trade management systems to handle tariffs, customs regulations, and trade agreements like RCEP, USMCA, and EU-UK TCA, boosting global enterprise software demand.

- Stringent Regulatory Compliance Requirements: Customs enforcement agencies globally intensified scrutiny of import-export declarations. The U.S. CBP collected more than USD 88 billion in duties in 2024, while the EU's Union Customs Code reform mandates electronic customs filings across 27 member states.

- AI and Automation Integration: Artificial intelligence is reshaping trade management by automating HS code classification, denied party screening, and duty drawback processes. AI-powered platforms significantly reduce manual errors and accelerate customs clearance cycles.

- Cloud-Based Solution Adoption: The rapid shift to cloud-native trade management platforms is enabling real-time global visibility, rapid regulatory update deployment, and reduced IT overhead. Cloud adoption among trade management buyers accelerated post-2021, with SaaS-based platforms now accounting for the majority of new contract awards in mid-market enterprise segments.

Market Restraints

- Data Security and Sovereignty Concerns: Trade management platforms handle sensitive shipment data, classified export control information, and financial transaction records. Data residency requirements in the EU (GDPR), China (PIPL), and India (DPDP Act 2023) create compliance complexity for cross-border cloud deployments, slowing adoption in heavily regulated industries.

- High Implementation and Integration Costs: Enterprise trade management systems demand extensive integration with ERP platforms (such as SAP S/4HANA and Oracle ERP Cloud), customs portals, and freight management solutions. Lengthy implementation timelines and high costs remain key barriers for mid-market companies.

- Complexity of Legacy System Migration: Many large manufacturers and logistics operators rely on decades-old customs management systems. Migration to modern trade management platforms involves significant data quality remediation, business process reengineering, and staff retraining, creating organizational inertia that delays procurement decisions.

Market Opportunities

- AI-Driven Trade Compliance Automation: The integration of large language models (LLMs) with trade compliance databases is giving rise to autonomous compliance assistants. Early implementations at major importers show substantial reductions in tariff classification time and notable duty savings through optimized trade agreement use.

- Expanding Cross-Border E-Commerce Requirements: Global cross-border e-commerce reached USD 1.1 trillion in 2023 . E-commerce platforms require automated de minimis threshold management, origin certification, and consumer-facing duty calculation - creating a large, underserved SME segment for cloud-native trade management vendors.

- Emerging Market Regulatory Digitalization: India's Foreign Trade Policy 2023, Vietnam's VNACCS customs modernization, and Saudi Arabia's FATOORA e-invoicing mandate are driving enterprise software adoption in high-growth emerging markets that have historically relied on manual trade documentation workflows.

Market Challenges

- Geopolitical Trade Policy Volatility: Frequent tariff adjustments, anti-dumping measures, export control expansions, and Section 301 duties necessitate constant updates within trade management platforms. Recent rounds of U.S. tariff changes have placed significant pressure on platform update cycles and vendor support.

- Fragmented Regulatory Landscape: Trade management platforms need to manage compliance content across hundreds of national customs jurisdictions, free trade agreements, and constantly changing denied party and sanctions lists. Maintaining this regulatory content accounts for a significant portion of vendor operating costs, limiting profitability for smaller providers.

Emerging Market Trends

1. Rapid Adoption of AI-Powered Trade Compliance

Artificial intelligence and machine learning are fundamentally reshaping trade compliance workflows. Automated HS code classification, real-time sanctions screening, and predictive duty optimization are transitioning from premium features to baseline platform expectations. Enterprise trade management vendors including SAP SE, Oracle, and e2open, LLC have embedded AI compliance modules in their 2024-2025 platform releases.

2. Cloud-Native Trade Management Platform Migration

The transition from on-premises to cloud-based trade management platforms is accelerating, fueled by the need for real-time regulatory updates and seamless collaboration with logistics partners. Cloud solutions are especially attractive to mid-market enterprises due to significant cost advantages over legacy systems.

3. Blockchain for Trade Finance and Documentation

Distributed ledger technology is increasingly used in trade finance and documentation workflows. Blockchain-enabled letter of credit platforms is processing substantial transaction volumes, with interoperability between trade management software and blockchain networks emerging as a key competitive advantage.

4. Real-Time Shipment Visibility and Risk Intelligence

Enterprises are demanding integrated risk intelligence layers within trade management platforms, combining real-time shipment tracking, port congestion data, and geopolitical risk scoring. The Red Sea shipping crisis of 2024 highlighted critical gaps in supply chain visibility, accelerating procurement of integrated trade risk management modules.

5. Sustainable Trade and Carbon Border Adjustment Compliance

The EU Carbon Border Adjustment Mechanism (CBAM), which entered transitional reporting phase in October 2023, is creating new compliance requirements for importers of steel, aluminum, cement, and fertilizers. Trade management platforms are expanding to incorporate carbon content reporting and CBAM certificate management as embedded compliance functions.

Industry Value Chain Analysis

The global trade management industry value chain spans six integrated stages from data intelligence provision through end-user compliance operations. Each stage presents distinct competitive dynamics and technology investment requirements relevant to the overall trade management market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Data & Intelligence Providers |

Bloomberg, LSEG, Dun & Bradstreet, Bureau van Dijk - providing trade statistics, tariff databases, and sanctioned party screening lists |

|

Software Developers & ISVs |

SAP SE, Oracle Corporation, Descartes Systems, E2open, Kinaxis - core trade management platform development, AI/ML integration, and regulatory content management |

|

Platform Integrators |

Accenture, Deloitte, Capgemini, Wipro - ERP integration, customs authority portal connectivity, and multi-country deployment services |

|

Consulting & Advisory |

KPMG Trade, PwC Global Trade, Grant Thornton - customs advisory, FTA utilization optimization, and export control compliance consulting |

|

End-Use Sectors |

Retail & consumer goods, manufacturing, transportation & logistics, aerospace & defense, healthcare - deploying trade management platforms for daily cross-border operations |

|

Regulatory Compliance |

U.S. CBP, EU Directorate-General for Taxation & Customs Union, WTO, WCO - setting the regulatory frameworks that mandate trade management software adoption |

Platform integrators hold the highest strategic value by bridging trade management software capabilities with enterprise ERP systems and government customs portals. Simultaneously, AI-driven regulatory content management is emerging as the most critical value chain activity - platforms offering real-time tariff schedule updates and automated sanctions screening are capturing premium pricing and long-term contract renewals.

Technology Landscape in the Trade Management Industry

Artificial Intelligence and Machine Learning

AI and machine learning are revolutionizing trade management. NLP automates HS code classification with high accuracy, while ML enhances denied party screening and reduces false positives, cutting analyst workloads by over half in major enterprise deployments.

Cloud and SaaS Architecture

Modern trade management platforms leverage multi-tenant cloud architectures, allowing simultaneous regulatory updates across all customer instances. SaaS-based solutions ensure high uptime and accelerate update deployment, while API-first designs from vendors like Oracle GTM Cloud and SAP GTS Cloud enable real-time integration with ERP, freight forwarding, and customs systems.

Blockchain and Distributed Ledger Technology

Blockchain is increasingly used in trade finance, including letter of credit management and origin certification. Integration with trade management platforms helps reduce documentary fraud and speeds up payments, offering significant potential cost savings for global trade.

Robotic Process Automation and Integration

Robotic process automation (RPA) is streamlining repetitive trade compliance tasks such as customs filings, duty drawback claims, and FTA certificate generation. Enterprises report major reductions in manual processing time and errors, while iPaaS solutions enable seamless connectivity with hundreds of carriers, customs, and ERP system APIs.

Market Segmentation Analysis

By Component

Solutions lead the global trade management market with a 58.4% share in 2025. Demand is driven by enterprise adoption of comprehensive trade management suites covering import compliance, export controls, tariff classification, trade analytics, and free trade agreement management.

To access detailed market analysis, Request Sample

By Deployment Type

On-premises deployment retains market leadership at 55.3% share in 2025. Regulated industries including aerospace and defense, healthcare, and government contractors maintain on-premises trade management platforms to ensure compliance with ITAR, EAR, and national data sovereignty requirements. On-premises deployments are supported by deep ERP integration maturity and long-established vendor relationships.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.7% |

U.S. CBP enforcement, USMCA compliance, Fortune 500 enterprise adoption, export control rigor |

|

Europe |

26.1% |

EU Union Customs Code, post-Brexit trade restructuring, CBAM implementation, EU-UK TCA compliance |

|

Asia Pacific |

22.8% |

RCEP implementation, China cross-border e-commerce, India FTP 2023, ASEAN trade digitalization |

|

Latin America |

9.4% |

Brazil customs modernization (SISCOMEX+), Mexico nearshoring boom, CAFTA-DR compliance |

|

Middle East & Africa |

7.0% |

GCC digitalization mandates, Saudi Vision 2030 trade facilitation, Africa Continental Free Trade Area |

North America commands 34.7% global revenue share in 2025. The United States remains the most critical national market for trade management, due to stringent customs enforcement and complex import-export regulations. High transaction volumes and ACE compliance requirements are driving continuous investment in certified trade management platforms.

Europe holds 26.1% of global revenue, anchored by the EU's complex multi-country customs union framework and post-Brexit trade compliance restructuring. The EU Union Customs Code reform mandating full electronic customs declaration systems by 2025 is driving platform upgrades across European importers and exporters. The EU Carbon Border Adjustment Mechanism (CBAM) creates new trade management compliance requirements for 2024-2034.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

SAP SE |

SAP GTS |

Leader |

ERP integration, global customs coverage |

|

Oracle |

Oracle GTM |

Leader |

Cloud-native, AI compliance, ERP synergy |

|

e2open, LLC. |

E2open Trade Management |

Leader |

Supply chain visibility, trade content |

|

The Descartes Systems Group Inc |

Descartes GTM |

Leader |

Customs filing, logistics integration |

|

Kinaxis Inc. |

Kinaxis RapidResponse |

Challenger |

Supply chain AI, risk management |

|

LSEG |

TORA,, LSEG AlphaDesk |

Challenger |

Trade content, sanctions screening |

|

MIC Datenverarbeitung GmbH |

MIC Customs |

Emerging |

European customs specialization |

The global trade management market's competitive landscape is moderately concentrated, with global enterprise software powerhouses competing alongside specialized customs compliance vendors. Leading players compete on regulatory content breadth, AI-powered automation, ERP integration depth, and geographic customs coverage. Strategic acquisitions are a key growth mechanism: E2open acquired Amber Road in 2020 for USD 425 million to expand its trade content and analytics capabilities.

Key Company Profiles

SAP SE

SAP SE, headquartered in Walldorf, Germany, is the global market leader in enterprise resource planning and the dominant provider of enterprise trade management solutions. Founded in 1972, SAP serves over 400,000 customers across 100 countries.

- Product & Platform Portfolio: SAP's trade management offerings center on SAP Global Trade Services (SAP GTS), covering customs management, compliance management, risk management, and trade preference management. SAP GTS integrates natively with SAP S/4HANA.

- Recent Developments: In 2025, SAP introduced its S/4HANA 2025 Cloud Private Edition with enhanced trade management capabilities. The update allows organizations to choose NAST, SAP S/4HANA Output Control, or both at the trading contract level, streamlining output management and improving automation and transparency in global trade operations.

- Strategic Focus: SAP's trade management strategy centers on deep S/4HANA integration, AI-powered classification automation, and expansion of its Business Network ecosystem to create end-to-end digital trade infrastructure for global manufacturing and retail enterprises.

Oracle

Oracle headquartered in Austin, Texas, USA, is a global technology leader offering the Oracle Global Trade Management (GTM) Cloud as part of its Supply Chain Management Cloud suite. Oracle serves over 430,000 customers worldwide across 175 countries.

- Product & Platform Portfolio: Oracle GTM Cloud provides import-export compliance, trade classification, trade agreement management, denied party screening, and trade analytics. The platform's multi-tenant cloud architecture enables real-time regulatory content updates across all customer instances.

- Recent Developments: In 2025, Oracle announced new trade management features in its Fusion Cloud Supply Chain & Manufacturing solution. The updates enhance automation, shipment visibility, and decision-making across global supply chains, helping businesses navigate evolving international tariffs and trade regulations.

- Strategic Focus: Oracle's strategy focuses on cloud-native trade management leadership, AI-powered compliance automation, and deep integration with Oracle ERP Cloud to create seamless procure-to-pay trade compliance workflows for enterprise customers.

E2open LLC.

E2open LLC is a leading provider of cloud-based supply chain and global trade management software, headquartered in Austin, Texas, USA, with a presence across North America, Europe, and Asia Pacific. The company delivers integrated solutions that span trade compliance, transportation, inventory planning, and multi-enterprise supply chain visibility.

- Product & Platform Portfolio: E2open's Trade Management solution covers global trade compliance, import-export management, trade agreement optimization, and denied party screening. The platform's trade content database covers 200+ country customs regimes, 350+ trade agreements, and 28+ million product classifications.

- Recent Developments: In 2025, E2open LLC enhanced its Global Trade software with AI-driven compliance capabilities and secured strategic partnerships with a global health brand, a Europe-based freight forwarder, and a U.S. food and beverage manufacturer.

- Strategic Focus: E2open focuses on integrating supply chain visibility with trade compliance, delivering a unified platform for end-to-end supply chain risk management that includes trade policy impact modeling, origin optimization, and global logistics orchestration.

Market Concentration Analysis

The global trade management market exhibits a moderately concentrated competitive structure. The top five vendors - SAP SE, Oracle, e2open, LLC., The Descartes Systems Group Inc, Kinaxis Inc - collectively account for approximately 55-60% of global market revenue in 2025. This concentration is driven by the high switching costs associated with deep ERP system integrations, long-term enterprise license agreements averaging 3-5 years.

Market fragmentation persists across SME and regional segments. Specialized customs compliance vendors including MIC Customs Solutions, Customs City, and Integration Point serve niche geographic or industry verticals with targeted solutions. Fragmentation is particularly pronounced in Asia Pacific, where domestic vendors in China, Japan, and India maintain strong positions in local customs filing and domestic trade compliance workflows.

Consolidation is accelerating. Private equity-backed platform aggregation strategies - exemplified by E2open's multi-acquisition model - are reshaping the competitive landscape.

Investment & Growth Opportunities

Fastest-Growing Segments

- Cloud-based deployment: Projected to grow at ~9.7% CAGR through 2034, with SaaS-based trade management adoption accelerating across SME and enterprise segments seeking lower total cost of ownership and real-time regulatory updates.

- AI-driven compliance automation: Automated HS classification, sanctions screening, and FTA utilization are creating significant growth opportunities in trade management software, driving substantial incremental license and SaaS subscription revenue by 2027.

- Trade finance integration: The convergence of trade management and trade finance platforms is creating a large combined market opportunity, driven by blockchain-enabled letter of credit and supply chain finance integration, with strong growth potential through 2030.

Emerging Market Opportunities

- Asia Pacific SME segment: Millions of SMEs in Asia Pacific engage in cross-border trade without enterprise-grade trade management systems. Cloud-native, subscription-based platforms targeting this segment present a significant greenfield revenue opportunity.

- Africa Continental Free Trade Area (AfCFTA): The implementation of AfCFTA across African Union member states is driving demand for trade agreement management, rules of origin certification, and customs automation, presenting a largely untapped market for global trade management providers.

Venture and Strategic Investment Trends

Venture capital investment in trade technology has surged in recent years, with major funding directed toward AI-powered customs classification, blockchain trade finance, and supply chain risk intelligence platforms. Strategic acquirers, including large enterprise software vendors and private equity-backed consolidators, continue to pursue acquisitions that expand regulatory content coverage, enhance AI capabilities, or open new geographic markets in Asia Pacific and Latin America.

Future Market Outlook (2026-2034)

The global trade management market is projected to grow from USD 1,271.8 Million in 2025 to USD 2,627.0 Million by 2034, representing a CAGR of 8.1% and a cumulative value creation of USD 1,355.2 Million over the forecast period.

Technological disruptions will reshape the competitive landscape over the forecast period. Generative AI trade compliance assistants are forecast to become mainstream by 2026-2027, automating complex ruling letter research, duty drawback optimization, and FTA origin qualification analysis.

Industry transformation will be driven by the convergence of trade management, supply chain visibility, and logistics execution within unified digital trade platforms. The regulatory landscape will intensify with CBAM expansion to additional product categories by 2026, evolving U.S.-China trade restrictions, and potential WTO digital trade framework adoption. Vendors investing in AI content management, cloud-native architecture, and emerging market expansion will capture disproportionate market share through 2034.

Research Methodology

Primary Research

Primary research for this report involved structured interviews with 120+ trade management practitioners, enterprise buyers, customs brokers, and freight forwarders across North America, Europe, and Asia Pacific. In-depth discussions with C-suite executives at 15 leading trade management platform vendors provided proprietary insights on product roadmaps, pricing strategies, and competitive positioning. Buyer surveys covering 280 enterprise trade management software users informed demand-side market sizing and segmentation analysis.

Secondary Research

Secondary research incorporated trade data from the World Customs Organization (WCO), World Trade Organization (WTO), and national customs authorities including U.S. CBP, EU DG TAXUD, and China GACC. Financial filings, earnings transcripts, and investor presentations from publicly listed trade management vendors provided revenue benchmarks. Trade association publications from the International Chamber of Commerce (ICC), FIATA, and NCBFAA supplemented industry trend analysis.

Forecasting Models

Market size estimates and forecasts are derived from a combination of bottom-up and top-down modeling approaches. The bottom-up model aggregates revenue estimates at the product segment, deployment type, enterprise size, end-use sector, and regional levels. The top-down model validates estimates against total technology spending data from IDC, Gartner, and company-reported revenues.

Trade Management Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solutions, Services |

| Functionalities Covered | Trade Function, Trade Compliance, Trade Finance, Trade Consulting, Others |

| Deployment Types Covered | Cloud-based, On-premises |

| Enterprise Sizes Covered | Small and Medium Sized Enterprises (SMEs), Large Enterprises |

| End-Use Sectors Covered | Retail and Consumer Goods, Transportation and Logistics, Aerospace and Defense, Healthcare, Manufacturing, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | SAP SE, Oracle, e2open LLC., The Descartes Systems Group Inc, Kinaxis Inc., LSEG, MIC Datenverarbeitung GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the trade management market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global trade management market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the trade management industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Trade Management Market Report

The global trade management market reached USD 1,271.8 Million in 2025. It is forecast to grow at an 8.1% CAGR, reaching USD 2,627.0 Million by 2034.

Primary drivers include rising cross-border trade complexity, stringent regulatory compliance mandates, AI and automation integration, and accelerating cloud-based platform adoption across enterprise segments globally.

North America leads with 34.7% of global revenue in 2025, driven by U.S. CBP enforcement rigor, USMCA compliance requirements, and large-scale Fortune 500 enterprise technology adoption.

Asia Pacific is the fastest-growing region, projected at approximately 9.8% CAGR through 2034, driven by RCEP implementation, China cross-border e-commerce growth, and India Foreign Trade Policy 2023 digitalization.

Solutions dominate with 58.4% of market revenue in 2025, covering customs compliance, trade finance, import-export management, and trade analytics software platforms across enterprise buyers globally.

On-premises deployment leads at 55.3% in 2025, sustained by data sovereignty requirements in regulated industries. Cloud-based platforms are the fastest-growing deployment mode at approximately 9.7% CAGR.

Leading players include SAP SE, Oracle, e2open, LLC., The Descartes Systems Group Inc, Kinaxis Inc., LSEG, and MIC Datenverarbeitung GmbH.

AI is automating HS code classification, denied party screening, duty optimization, and compliance document generation. Leading platforms report substantial reductions in manual compliance workloads through AI-driven automation.

Blockchain is streamlining trade finance, letter of credit management, and origin certification by providing secure, transparent transaction records. Integration with trade finance networks reduces documentary fraud and accelerates payment cycles.

The global trade management market is projected to reach USD 1,876.8 Million by 2030, representing consistent growth driven by cloud migration, AI compliance automation, and Asia Pacific regional expansion.

CBAM creates new compliance requirements for importers of steel, aluminum, cement, and fertilizers. Trade management platforms are adding CBAM reporting and certificate management modules as embedded compliance features for European enterprise buyers.

Key opportunities include cloud-native SME platforms in Asia Pacific, AI-driven compliance automation, Africa Continental Free Trade Area enablement, and convergence of trade management with supply chain visibility and trade finance platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)