Tonometer Market Size, Share, Trends and Forecast by Type, Technology, Portability, End User, and Region, 2025-2033

Tonometer Market Size and Share:

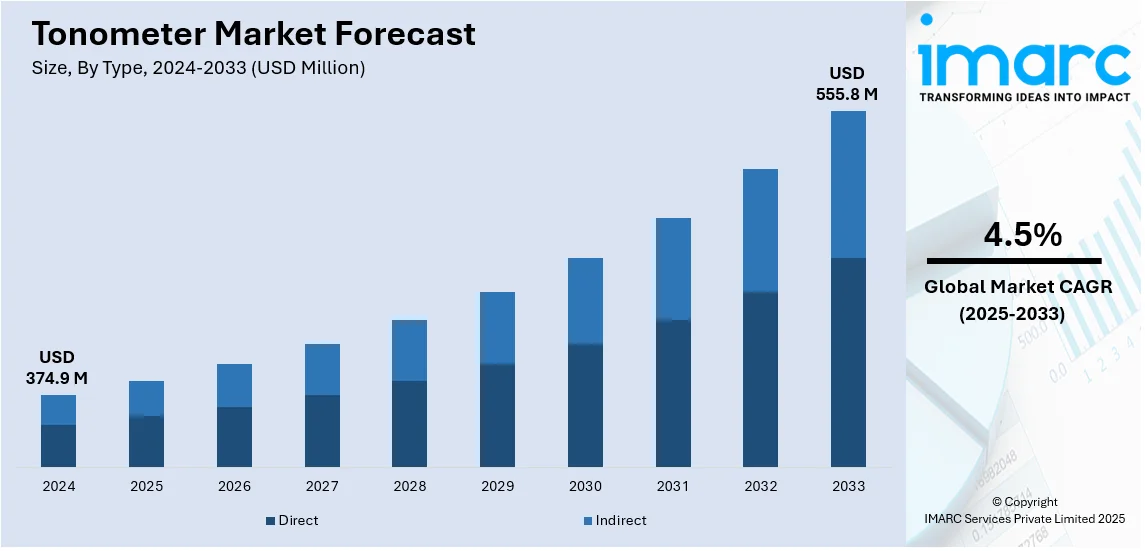

The global tonometer market size was valued at USD 374.9 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 555.8 Million by 2033, exhibiting a CAGR of 4.5% from 2025-2033. North America currently dominates the market, holding a market share of over 39.6% in 2024. This dominance can be attributed to high glaucoma prevalence, advanced healthcare infrastructure, strong reimbursement policies, and widespread adoption of digital tonometers. Increased R&D investments, aging population, and regular eye screenings further drive market growth, ensuring early disease detection and treatment.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 374.9 Million |

|

Market Forecast in 2033

|

USD 555.8 Million |

| Market Growth Rate (2025-2033) | 4.5% |

The global tonometer market is driven by technological advancements in tonometry, including non-contact and rebound tonometers, which enhance patient comfort and diagnostic accuracy. Increasing government initiatives for vision care programs, especially in developing nations, are expanding accessibility to tonometry. The rise in diabetes-related eye disorders, such as diabetic retinopathy and ocular hypertension, necessitates regular intraocular pressure monitoring. Growing investments in AI-integrated diagnostic tools are improving early disease detection. Expanding healthcare infrastructure in emerging economies and the increasing presence of specialized ophthalmic clinics contribute to market growth. Additionally, the surge in telemedicine and remote eye screening services is fostering market expansion by enabling early and widespread detection of ocular diseases.

The U.S. tonometer market is propelled by a strong regulatory framework ensuring product innovation and quality standards, leading to the adoption of FDA-approved advanced tonometry devices. The increasing prevalence of myopia and hyperopia among younger populations has heightened the demand for routine eye examinations. Strategic collaborations between ophthalmology device manufacturers and research institutions are driving technological enhancements. The rising popularity of portable and handheld tonometers supports use in home healthcare and ambulatory settings. Expanding insurance coverage for preventive eye care services encourages frequent screenings. Furthermore, the presence of leading ophthalmic equipment manufacturers and increasing investment in AI-driven tonometry solutions are accelerating market growth in the country. For instance, in May 2024, Reichert Technologies launched the Tono-Vera tonometer in the US, featuring the patented ActiView system for automated, reliable intraocular pressure (IOP) measurements. This handheld device uses rebound tonometry, eliminating the need for anesthetic. It provides quick, accurate readings, comparable to Goldmann tonometry, with user-friendly design and Bluetooth connectivity. Reichert, a leader in eye care diagnostics, continues its innovation with Tono-Vera, enhancing glaucoma patient care.

Tonometer Market Trends:

Integration of Artificial Intelligence in Tonometry

The incorporation of artificial intelligence (AI) in tonometry is transforming intraocular pressure (IOP) measurement by improving diagnostic accuracy and patient management. AI-powered tonometers utilize machine learning algorithms to analyze large datasets, enabling early detection of glaucoma and ocular hypertension. These devices can assess subtle variations in IOP that might be missed by conventional methods, allowing for more precise monitoring. AI integration also supports automated data interpretation, reducing dependence on specialist evaluations and enhancing accessibility in remote or underserved areas. Additionally, AI-enabled tonometers facilitate predictive analytics, identifying patients at risk for developing glaucoma before significant vision loss occurs. The growing focus on personalized medicine and digital health solutions is driving further advancements in AI-assisted tonometry, improving patient outcomes. For instance, in May 2024, Topcon Healthcare partnered with Microsoft to advance AI-driven "Healthcare from the Eye" solutions. They'll use cloud platforms for pre-screening systemic and neurological diseases via eye scans. Topcon's IDHea fosters AI research, ensuring data security. They're investing in AI innovators and using Microsoft Azure for secure data management. This aims to improve healthcare access, quality, and affordability through AI-powered eye diagnostics.

Rise of Non-Contact and Portable Tonometers

The increasing adoption of non-contact and portable tonometers is shaping the market by offering enhanced patient comfort and convenience. Non-contact tonometers (air-puff tonometers) eliminate the need for anesthesia, reducing discomfort and the risk of cross-contamination. These devices are particularly beneficial for pediatric and geriatric patients who may be sensitive to traditional tonometry techniques. For instance, in April 2023, Nidek released the NT-1/1e non-contact tonometers, omitting pachymetry to meet market needs. The NT-1 offers automated IOP measurements with patient safety features and voice guidance. The NT-1e provides manual measurement with 3D tracking. Both models feature a flexible, space-saving design for improved clinic efficiency and patient comfort. In parallel, handheld and portable tonometers are gaining popularity in home care settings, ambulatory centers, and teleophthalmology services, enabling remote monitoring and reducing the need for frequent clinical visits. The miniaturization of tonometry devices, combined with wireless connectivity and cloud-based data storage, allows real-time data sharing between healthcare providers and patients, facilitating continuous IOP monitoring and timely intervention in high-risk individuals.

Expansion of Teleophthalmology and Remote Eye Care Services

The rising demand for teleophthalmology and remote eye care solutions is significantly influencing the tonometer market. With increasing emphasis on accessible and cost-effective eye care, many healthcare providers are integrating tonometry into digital health platforms. Remote IOP measurement, enabled by connected tonometry devices and telemedicine applications, allows ophthalmologists to monitor patients without requiring frequent in-person consultations. This trend is particularly impactful in rural and underserved regions, where access to specialized ophthalmic care is limited. Additionally, the expansion of wearable tonometers capable of continuous IOP monitoring is enhancing early disease detection. For instance, in March 2024, the National Eye Institute granted USD 6.7 Million to Purdue University to develop innovative smart contact lens tonometers. These patent-pending devices, utilizing "StickTronics," will continuously monitor intraocular pressure (IOP) and deliver therapeutic drugs, aiding in the management of chronic eye conditions like glaucoma. Besides this, the shift toward virtual eye screenings and AI-powered diagnostics is expected to bridge the gap in glaucoma management, ensuring timely intervention and reducing the risk of vision impairment.

Tonometer Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global tonometer market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on type, technology, portability, and end user.

Analysis by Type:

- Direct

- Indirect

Indirect stand as the largest type in 2024. The dominance of the indirect segment within the tonometer market is largely attributed to the increasing prevalence of glaucoma and the growing need for efficient and patient-friendly intraocular pressure (IOP) measurement. Indirect tonometers, particularly rebound tonometers, offer advantages such as reduced patient discomfort and a lower risk of corneal damage, making them suitable for widespread screening, including in pediatric and geriatric populations. Additionally, advancements in technology have improved the accuracy and reliability of indirect tonometers, further driving their adoption in clinical settings.

Analysis by Technology:

- Applanation Tonometry

- Indentation Tonometry

- Rebound Tonometry

- Others

Applanation tonometry leads the market with around 51.4% of market share in 2024. Applanation tonometry's dominance in the tonometer market stems from its established reliability and accuracy in measuring intraocular pressure (IOP), a crucial factor in glaucoma diagnosis. The Goldmann applanation tonometer, in particular, is considered the "gold standard" for IOP measurement, contributing to its widespread use in clinical settings. This technique's ability to provide consistent and precise readings has solidified its position, even with the emergence of newer technologies. Additionally, established clinical practices and widespread familiarity among ophthalmologists reinforce the continued preference for applanation tonometers.

Analysis by Portability:

- Desktop

- Handheld

Handheld leads the market with around 72.2% of market share in 2024. The dominance of the handheld tonometer segment in the market stems from its enhanced portability and convenience. These devices enable healthcare professionals to conduct intraocular pressure (IOP) measurements in various settings, beyond traditional clinic environments. This flexibility is crucial for screening programs, home healthcare, and situations where patient mobility is limited. Furthermore, advancements in technology have led to increased accuracy and ease of use in handheld tonometers, making them a preferred choice for both practitioners and patients. The growing prevalence of glaucoma and the rising geriatric population, who require frequent IOP monitoring, further fuel the demand for these portable devices

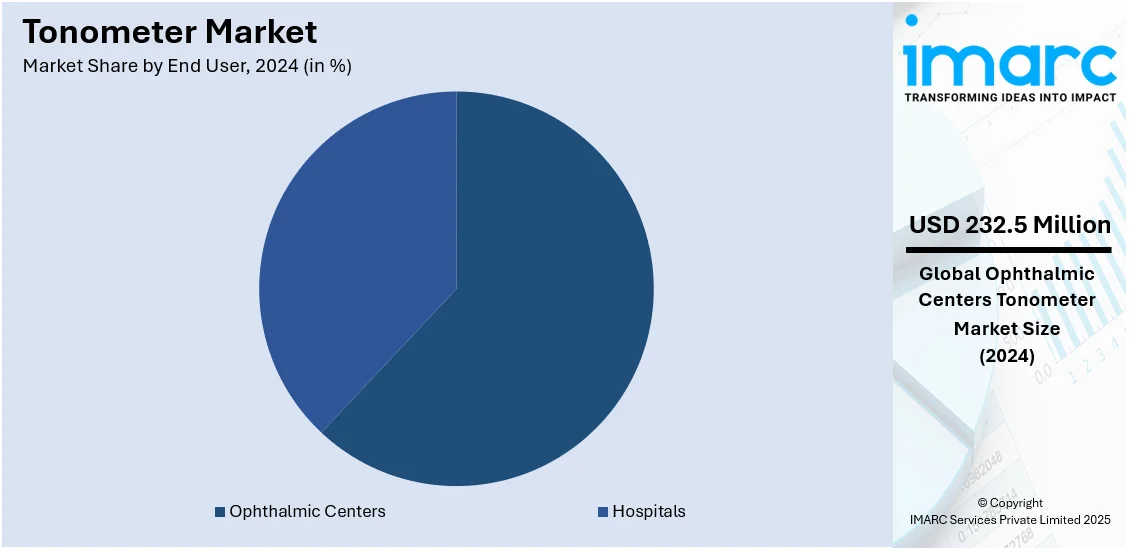

Analysis by End User:

- Hospitals

- Ophthalmic Centers

Ophthalmic centers lead the market with around 62.0% of market share in 2024. Ophthalmic centers dominate the tonometer market due to their specialized focus on eye care. These centers are primary locations for diagnosing and managing conditions like glaucoma, which necessitates frequent intraocular pressure (IOP) measurements. Therefore, they require a consistent and high volume of tonometer usage. Ophthalmic centers conduct routine screenings and detailed examinations, driving demand for both desktop and handheld tonometers. Additionally, these facilities often invest in advanced tonometer technology to ensure accurate and reliable IOP readings, contributing to their significant market share. The increase in eye related diseases, and an aging population, also increases the amount of patients visiting these centers.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

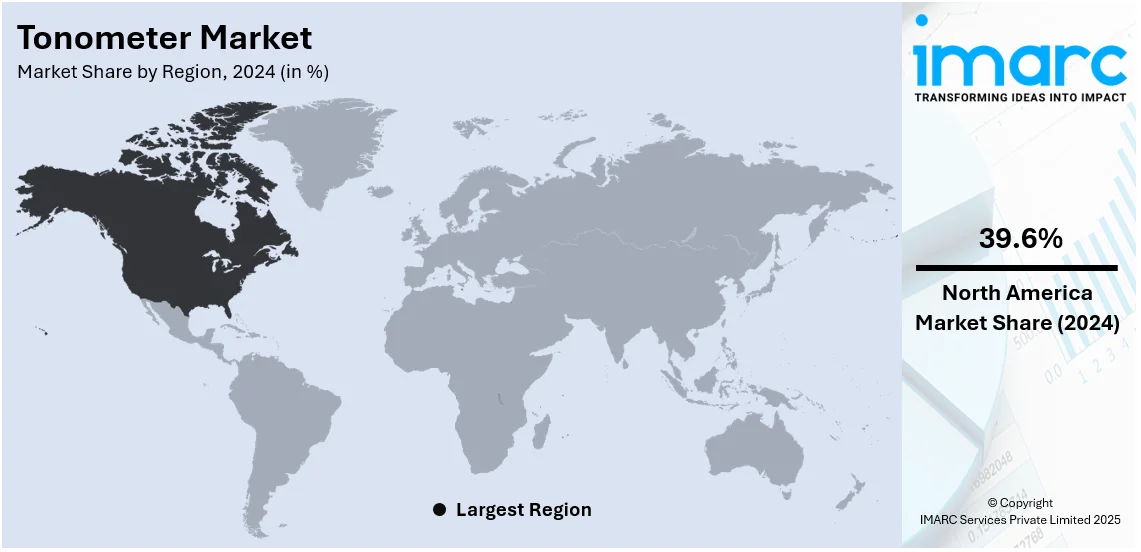

In 2024, North America accounted for the largest market share of over 39.6%. North America's dominance in the tonometer market stems from a confluence of factors. Robust healthcare infrastructure, coupled with a high prevalence of eye disorders like glaucoma, drives significant demand. For instance, the CDC reports glaucoma affects about 3 million Americans and is the second leading cause of global blindness. Open-angle glaucoma, the most common type, often has no early symptoms, leaving 50% of those affected unaware, heightening the need for diagnostic tools like tonometer. The region's advanced medical technology adoption, particularly in the United States, fosters innovation and the development of sophisticated tonometers. Furthermore, the presence of key industry players and established healthcare centers reinforces market leadership. A large geriatric population, which is more prone to glaucoma, also contributes to the high demand for tonometers. All of these points add up to North America being the leading market for tonometers.

Key Regional Takeaways:

United States Tonometer Market Analysis

In 2024, the United States held 91.4% of the market share in North America. The growing adoption of tonometer due to the rising prevalence of eye-related disorders is a significant market driver. According to reports, about 1.8 Million Americans aged 40 years and older are affected by AMD. With increasing cases of glaucoma and other ocular conditions, the demand for tonometer devices has risen across various healthcare settings. Regular eye screenings have become crucial as early detection of eye-related disorders help in effective treatment. The rising awareness about eye health, along with advancements in diagnostic technologies, are further fueling the adoption of tonometer. Additionally, improved healthcare infrastructure and accessibility to ophthalmic care have supported market expansion. The integration of digital tonometer devices in hospitals and clinics has also contributed to market growth. Increased healthcare expenditure and government initiatives promoting eye health screenings have encouraged the use of tonometer across different age groups. The focus on patient-centric care, coupled with ongoing innovations in non-contact tonometer devices, has led to wider acceptance in medical facilities. The expanding network of optometrists and ophthalmologists further supports the growing tonometer adoption due to growing eye-related disorders.

Asia Pacific Tonometer Market Analysis

The escalating prevalence of glaucoma, projected to impact 27.8 million additional people in Asia by 2040, primarily in India and China, is fueling substantial tonometer demand. Rapid urbanization and lifestyle shifts increase glaucoma incidence, driving routine eye screenings. Enhanced healthcare infrastructure expands tonometer accessibility in facilities, while governmental initiatives promote early ocular disease detection. The growing number of eye care professionals further broadens access to advanced tonometer technologies. The need for convenient monitoring encourages the adoption of portable, user-friendly home tonometers. Continuous R&D efforts are yielding innovative tonometers with improved accuracy and efficiency, crucial for effective glaucoma management.

Europe Tonometer Market Analysis

The expanding elderly population is a primary catalyst for tonometer market growth, as age significantly elevates the risk of ocular diseases. WHO data highlights the European Region's aging trend, with projections of 300 million individuals aged 60+ by 2050. This demographic shift intensifies demand for tonometers, crucial for diagnosing conditions like glaucoma. Geriatric care facilities are increasingly equipped with these devices, enhancing early detection. Continued research fuels innovation in tonometer technology, resulting in more accurate and user-friendly devices, such as automated and digital models. This technological advancement allows for more efficient screening. Moreover, government investments in elderly healthcare, combined with heightened public awareness about proactive eye health, further propel tonometer adoption. Integrating tonometers into comprehensive ophthalmic care ensures timely intervention, preserving vision in the aging population.

Latin America Tonometer Market Analysis

The surging diabetic population in Latin America is significantly fueling tonometer device demand. With 31.6 million diabetics in 2019, projections indicate a rise to 40.2 million by 2030, and 49.1 million by 2045. This growth directly correlates with increased diabetic retinopathy and glaucoma cases, necessitating routine intraocular pressure monitoring. Healthcare providers are integrating tonometers into standard diabetes care, enhancing early detection. Expanding healthcare initiatives are improving tonometer accessibility in hospitals and diagnostic centers. The diabetic surge is also driving research into advanced tonometer technologies for improved diagnostic precision. Public health campaigns are crucial, educating individuals about the critical link between diabetes and eye health, thereby promoting proactive eye care.

Middle East and Africa Tonometer Market Analysis

The tonometer market is expanding due to the rapid growth of healthcare facilities, as evidenced by Dubai's sector, which saw a surge to 4,482 private medical facilities and 55,208 licensed professionals by 2022, with further growth projected. Increased healthcare infrastructure investments are enhancing access to advanced tonometers. Additionally, rising health awareness campaigns emphasizing preventive eye care, coupled with expanding ophthalmic diagnostic services, are driving routine tonometer screenings. This heightened focus on early detection is significantly contributing to market growth.

Competitive Landscape:

The tonometer market's competitive landscape is characterized by a mix of established medical device manufacturers and specialized ophthalmic technology companies. Innovation is a key driver, with firms focusing on developing more portable, user-friendly, and accurate tonometers. Competition centers on technological advancements, such as non-contact and rebound tonometry, and integrated devices with digital capabilities. Market players strive to offer comprehensive solutions, including data management and connectivity, to enhance clinical workflows. Price competition exists, particularly for basic models, while premium devices with advanced features command higher prices. Strategic partnerships and acquisitions are also common tactics to expand product portfolios and market reach. Regulatory approvals and adherence to stringent quality standards are critical for market entry and sustained growth.

The report provides a comprehensive analysis of the competitive landscape in the tonometer market with detailed profiles of all major companies, including:

- 66 Vision Tech Co. Ltd. (Yuwell-Jiangsu Yuyue Medical Equipment & Supply Co. Ltd.)

- AMETEK Inc.

- Canon Inc.

- Haag-Streit Group (Metall Zug AG)

- Keeler Ltd. (Halma plc)

- Kowa American Corporation (Kowa Company Limited)

- Nidek Co. Ltd.

- Revenio Group Oyj

- Rexxam Co. Ltd.

- Tomey Corporation

- Topcon Corporation

- Ziemer Ophthalmic Systems AG

Latest News and Developments:

- January 2025: Keeler has launched servicing for Goldmann Applanation Tonometers (GATs) at its European Distribution site in Terrasa, Spain, enhancing support for EU-based professionals. This expansion ensures faster turnaround and cost-effective maintenance for Keeler’s KAT Tonometers, previously serviced in the UK. The initiative builds on the site's existing ophthalmic equipment servicing and training capabilities.

- September 2024: Topcon Healthcare has introduced the TRK-3 OMNIA, a 4-in-1 auto kerato-refracto tonometer, to the European market at the 42nd ESCRS Congress in Barcelona. The device enhances clinical efficiency by combining refractometry, keratometry, tonometry, and pachymetry in one compact unit. Featuring improved connectivity and a user-friendly interface, the TRK-3 OMNIA aims to streamline eye care diagnostics.

- September 2024: iCare has launched the ST500, a slit-lamp-mounted tonometer using rebound tonometry technology. The device features a universal adapter for compatibility with most slit lamps and a Quick Measure function for rapid IOP readings. iCare also introduced the SmartCradle, a charging and storage port enabling future digital connectivity.

- June 2024: NIDEK has introduced the RS-1 Glauvas Optical Coherence Tomography, featuring a 250kHz scan speed for high-quality imaging and deep learning-based analytics. Designed for efficient glaucoma and retinal diagnostics, the system enhances workflow alongside NIDEK’s tonometer solutions.

- February 2024: Topcon Healthcare has introduced the TRK-3 OMNIA, a 4-in-1 auto kerato-refracto tonometer, to the Asian market. This advanced device enhances clinical workflow by combining a refractometer, keratometer, non-contact tonometer, and pachymeter in a single unit. Featuring one-touch operation and DICOM connectivity, it streamlines patient care and improves efficiency for eye care professionals.

- January 2024: New York-based DevelopAll Inc. has launched the Diaton digital tonometer, a groundbreaking device that measures intraocular pressure (IOP) through the eyelid, bypassing corneal limitations. FDA-approved and endorsed by top specialists, Diaton offers a non-invasive, anesthesia-free solution for glaucoma screenings, enhancing accuracy and patient comfort.

Tonometer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Direct, Indirect |

| Technologies Covered | Applanation Tonometry, Indentation Tonometry, Rebound Tonometer, Others |

| Portabilities Covered | Desktop, Handheld |

| End Users Covered | Hospitals, Ophthalmic Centers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 66 Vision Tech Co. Ltd. (Yuwell-Jiangsu Yuyue Medical Equipment & Supply Co. Ltd.), AMETEK Inc., Canon Inc., Haag-Streit Group (Metall Zug AG), Keeler Ltd. (Halma plc), Kowa American Corporation (Kowa Company Limited), Nidek Co. Ltd., Revenio Group Oyj, Rexxam Co. Ltd., Tomey Corporation, Topcon Corporation, Ziemer Ophthalmic Systems AG., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the tonometer market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global tonometer market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the tonometer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The tonometer market was valued at USD 374.9 Million in 2024.

The tonometer market is projected to exhibit a CAGR of 4.5% during 2025-2033, reaching a value of USD 555.8 Million by 2033.

Key factors driving the tonometer market include the rising prevalence of glaucoma and other ocular diseases, an aging global population, and increasing awareness of preventive eye care. Technological advancements, such as portable and non-contact tonometers, and growing healthcare infrastructure investments also contribute significantly.

North America currently dominates the tonometer market, accounting for a share of 39.6%. North America's dominance stems from its advanced healthcare infrastructure, high prevalence of eye disorders, significant geriatric population, and robust adoption of advanced medical technologies, driving substantial tonometer demand.

Some of the major players in the tonometer market include 66 Vision Tech Co. Ltd. (Yuwell-Jiangsu Yuyue Medical Equipment & Supply Co. Ltd.), AMETEK Inc., Canon Inc., Haag-Streit Group (Metall Zug AG), Keeler Ltd. (Halma plc), Kowa American Corporation (Kowa Company Limited), Nidek Co. Ltd., Revenio Group Oyj, Rexxam Co. Ltd., Tomey Corporation, Topcon Corporation, Ziemer Ophthalmic Systems AG., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)