Synchrophasors Market Size, Share, Trends and Forecast by Component, Application, and Region, 2025-2033

Synchrophasors Market Size and Share:

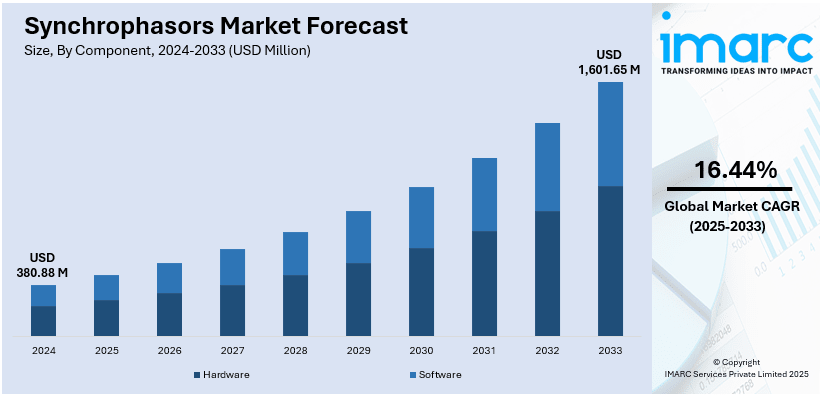

The global synchrophasors market size was valued at USD 380.88 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 1,601.65 Million by 2033, exhibiting a CAGR of 16.44% from 2025-2033. North America currently dominates the market, holding a market share of over 38.6% in 2024. The market is driven by significant grid modernization investments, FERC and NERC reliability regulations with a stick, growing integration of renewable energy, mounting cybersecurity threats, and the increasing demand for real-time monitoring to minimize threats from weather events and old infrastructure, with the aim of improved grid stability and resilience.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 380.88 Million |

|

Market Forecast in 2033

|

USD 1,601.65 Million |

| Market Growth Rate 2025-2033 | 16.44% |

The growing incidence of power outages, grid collapse, and severe weather is fueling demand for synchrophasors as utilities want sophisticated solutions to monitor in real-time and stabilize the grid. As power systems become highly advanced with growing electricity demand and addition of distributed energy resources (DERs), synchrophasors offer increased situational awareness, fault identification, and preventive maintenance. Governments and regulatory agencies across the globe are imposing tighter grid reliability standards, encouraging utilities to invest in phasor measurement units (PMUs) and advanced monitoring systems. Furthermore, growing concerns regarding cybersecurity threats and the necessity of real-time protection against grid disturbance are driving synchrophasor adoption. As more countries upgrade their aging power infrastructure and emphasize disaster preparedness measures, the synchrophasor market is likely to expand substantially, with utilities giving top priority to automation, real-time analytics, and self-healing grid technologies to achieve long-term grid resilience. For instance, in November 2024, the joining of synchrophasors with digital twin technology revolutionized grid management, allowing utilities to model conditions, forecast failures, and improve performance with real-time data for greater reliability and efficiency.

The U.S. market currently holds a total share of 87.60% owing to the implementation of various government initiative towards grid modernization and energy resilience is a major impetus for c deployment. According to the sources, in January 2023, NASPI highlighted cutting-edge networking, deep learning, and high-definition sensors for the resilience of the power grid with an emphasis on synchrophasor deployment in distribution, wildfire prevention, equipment monitoring, and system anomaly detection to advance reliability and operations planning. Moreover, with deteriorating power grid and increasing electricity demand, federal and state governments are making huge investments in grid upgrades, real-time monitoring infrastructure, and big data analytics to improve energy reliability. Legislations like the Grid Resilience and Innovation Partnerships (GRIP) Program and the Infrastructure Investment and Jobs Act (IIJA) invest billions of dollars in upgrading transmission networks, incorporating real-time monitoring of data, and enhancing the grid's resilience. Moreover, the mounting frequency of wildfires, hurricanes, and catastrophic weather patterns in the U.S. has fueled the requirement for phasor measurement units (PMUs) to identify faults, minimize blackout possibilities, and optimize power delivery. The Federal Energy Regulatory Commission (FERC) and the North American Electric Reliability Corporation (NERC) are also requiring higher grid monitoring standards, further propelling synchrophasor deployment nationwide.

Synchrophasors Market Trends:

Rising Adoption of Synchrophasors for Grid Reliability and Resilience

The increasing deployment of synchrophasors in power grids is significantly enhancing grid reliability and resilience. These devices provide real-time monitoring and measurement of critical grid components, enabling operators to detect faults, prevent blackouts, and improve overall system stability. As power outages become more frequent due to extreme weather events, equipment failures, and cyber threats, utilities are prioritizing advanced grid-monitoring solutions. A January 22, 2025, study in PLOS Climate analyzed data from 2018 to 2020 across 1,600+ U.S. counties, revealing that 75% experienced major power outages caused by severe weather, and 50% faced multiple simultaneous events. With grid reliability becoming a national priority, synchrophasors are highly integrated into disaster response strategies, predictive maintenance programs, and real-time fault detection systems. Their ability to provide enhanced situational awareness, reduce downtime, and prevent cascading failures makes them a crucial technology in modern energy infrastructure.

Integration of Smart Grid Technologies and Renewable Energy

The global shift toward smart grid modernization and renewable energy integration is accelerating the demand for synchrophasors. These devices play a crucial role in gathering, distributing, and analyzing grid data to improve automation, optimize energy flow, and enhance real-time decision-making. With the increasing adoption of solar, wind, and other renewable energy sources, power grids require advanced monitoring systems to manage variable energy loads and maintain stability. Synchrophasors help balance renewable energy fluctuations, detect grid disturbances, and optimize load distribution, reducing dependence on fossil fuels. Additionally, the integration of machine learning (ML) and cloud computing enables utilities to process vast amounts of synchrophasor data for predictive maintenance, early fault detection, and automated response mechanisms. As smart cities expand and governments push for low-carbon energy solutions, synchrophasors are emerging as a critical technology for achieving efficient, flexible, and resilient power distribution networks.

Government Policies and Investments Driving Market Expansion

Governments worldwide are prioritizing investments in power grid modernization to enhance stability, security, and efficiency. Regulatory policies promoting energy efficiency, decarbonization, and smart grid deployment are driving the adoption of advanced monitoring technologies such as synchrophasors. Several nations are implementing grid reliability standards and financial incentives for utilities to integrate real-time monitoring, automation, and predictive analytics into their systems. Additionally, public and private sector investments in grid digitalization, renewable energy projects, and cyber-resilient infrastructure are accelerating market growth. Programs supporting carbon neutrality, demand response management, and grid decentralization further emphasize the role of synchrophasors in achieving long-term energy sustainability. With growing concerns over aging power infrastructure, rising electricity demand, and environmental regulations, governments are expected to increase funding for smart grid technologies, making synchrophasors a key component of future-ready energy networks.

Synchrophasors Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global synchrophasors market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on component, and application.

Analysis by Component:

- Hardware

- Software

The hardware segment is the largest in the synchrophasors market share with 85.0% in 2024, propelled by the large-scale installation of Phasor Measurement Units (PMUs), communication networks, and data concentrators. The need for real-time monitoring of the grid, fault detection, and stability measurement has resulted in high investments in sophisticated hardware solutions. Utilities and grid operators emphasize high-accuracy measurement equipment to enhance energy reliability, minimize transmission losses, and incorporate renewable sources of energy harmoniously. Further, developments in sensor technology, GPS synchronization, and edge computing are boosting the capabilities of future-generation PMUs. With governments globally investing in grid modernization initiatives, the hardware segment will continue to hold its ground with ongoing innovation in cybersecurity, AI-based analytics, and cloud integration.

Analysis by Application:

- Fault Analysis

- State Estimation

- Stability Monitoring

- Power System Control

- Operational Monitoring

- Improve Grid Visualization

- Others

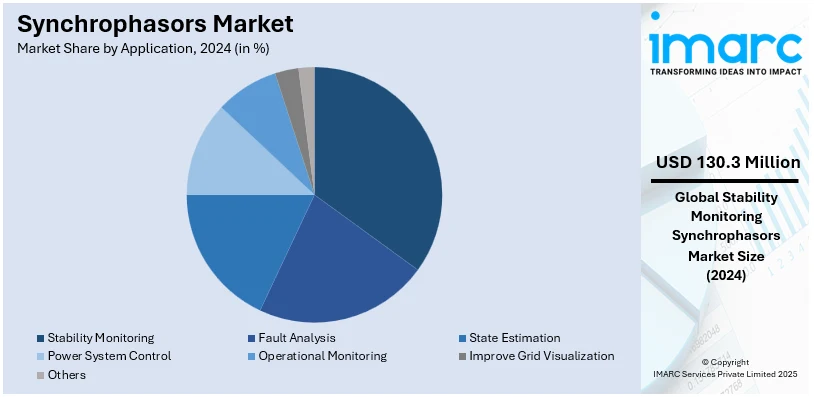

Stability monitoring is the most prominent application in the synchrophasors market, accounting for 34.2% share in 2024. Due to the growing grid complexity arising from renewable energy integration, distributed energy resources (DERs), and increasing power demand, utilities are emphasizing real-time stability evaluations to avoid disruptions and optimize operational efficiency. Synchrophasors provide high-speed data acquisition and dynamic system monitoring, enabling operators to anticipate and manage grid disturbances before they become unmanageable. Implementation of machine learning (ML) and predictive analytics based on AI is further enhancing grid stability and automation. Government regulations for grid reliability and cybersecurity are also fueling investments in stability monitoring solutions. In the process of transition of power systems toward digitization and automation, synchrophasors are of pivotal importance in providing smooth power distribution as well as better grid resilience.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America dominates the worldwide synchrophasors market and held a 38.6% market share in 2024 due to massive investments made in grid modernization, security strengthening, and smart grid implementation. The U.S. government's efforts, including the Infrastructure Investment and Jobs Act (IIJA) and the Grid Resilience and Innovation Partnerships (GRIP) Program, have played a crucial role in increasing the use of phasor measurement technology. Regulatory organizations such as FERC and NERC are enforcing stringent grid reliability measures, prompting utilities to invest in real-time monitoring and predictive analytics. The region also confronts growing threats from extreme weather conditions, cyberattacks, and mature power infrastructure, which requires advanced fault detection and grid stability solutions. Since North America remains a leader in renewable energy integration, AI-driven grid analytics, and decentralization of energy, it will continue to lead the synchrophasors market.

Key Regional Takeaways:

United States Synchrophasors Market Analysis

The synchrophasors market in the United States is significantly growing as utilities invest in smart grid infrastructure and grid modernization programs. The U.S. Department of Energy (DOE) has committed USD 2.2 Billion to 8 projects across 18 states under the Grid Resilience and Innovation Partnerships (GRIP) Program, leveraging USD 10 Billion in public-private funds. These projects will expand grid capacity by 13 GW, upgrade 1,000+ miles of transmission lines, and create 5,000 jobs, strengthening resilience against extreme weather. Key initiatives include 625 miles of new HVDC transmission lines and 5,500 hours of outage prevention for 700,000 customers. The North American Synchrophasor Initiative (NASPI) is driving phasor measurement unit (PMU) deployment to improve grid reliability and prevent blackouts. The Federal Energy Regulatory Commission (FERC) supports PMU integration for real-time grid monitoring and fault detection. Utilities are enhancing power flow analysis and renewable energy integration using synchrophasor technology. Major players are investing in wide-area monitoring systems and advanced data analytics to improve grid visibility. Growing cybersecurity concerns in critical energy infrastructure are driving demand for secure data transmission and predictive maintenance technologies, ensuring continued market expansion in the U.S.

Europe Synchrophasors Market Analysis

The market in Europe is expanding as utilities invest in smart grids and renewable energy integration. The European Environment Agency (EEA) Trends and Projections 2024 report indicates that EU greenhouse gas emissions fell by 8% in 2023, reaching 37% below 1990 levels. Renewables now account for 24% of total energy consumption, and primary energy use has declined by 19% since 2005. The energy sector’s emissions have halved since 2005, while buildings have cut emissions by over 30%. The EU targets a 55% reduction by 2030 and 90% by 2040 to reach climate neutrality by 2050. Countries like Germany, France, and the UK are leading synchrophasor deployments to improve grid resilience and efficiency as reliance on solar and wind power grows. The EU Clean Energy Package promotes energy security and decarbonization, encouraging investments in phasor measurement units (PMUs) and wide-area monitoring systems (WAMS). Transmission system operators (TSOs) are using synchrophasor data to optimize cross-border power flows and stabilize frequency fluctuations in interconnected grids. Horizon Europe research initiatives are advancing real-time grid analytics and monitoring. Collaborations between utilities and technology providers are fostering AI-driven analytics for predictive maintenance and operational efficiency.

Asia Pacific Synchrophasors Market Analysis

The Asia Pacific synchrophasor market is rapidly escalating, driven by grid modernization projects in China, India, and Japan. Government initiatives promoting smart grids and renewable energy integration are key to this expansion. China’s State Grid Corporation is deploying Phasor Measurement Units (PMUs) to improve transmission stability and reduce energy losses. In India, the National Smart Grid Mission is advancing real-time grid monitoring to address power transmission inefficiencies. Japan’s utilities are investing in synchrophasor-based systems to enhance disaster resilience and prevent cascading failures. Southeast Asian nations are also deploying PMUs with support from international energy organizations. The rising demand for industrial automation and digital substations further fuels this market. Companies are focusing on advanced synchrophasor analytics and AI-driven grid monitoring solutions to optimize power distribution. In related developments, Neara raised USD 31 Million in a Series C funding round in October 2024, expanding its AI-powered predictive modeling platform that aids utilities like CenterPoint Energy and Southern California Edison in improving network resilience.

Latin America Synchrophasors Market Analysis

The Latin America market is growing with investments in grid modernization and renewable energy projects. Brazil and Mexico are leading PMU adoption to enhance power system reliability amid growing solar and wind energy use. According to the Brazilian Association of Photovoltaic Solar Energy (ABSOLAR), Brazil’s installed solar capacity reached 38.4 GW in February 2024, accounting for 17.0% of its electricity matrix. The country ranked 8th globally in 2022 with 24 GW, and between January and September 2023, solar capacity increased by 3 GW, as per the International Renewable Energy Agency (IRENA). Utilities are deploying synchrophasor-based monitoring systems to manage voltage fluctuations and transmission losses. Despite high implementation costs and a lack of skilled personnel, international collaborations and smart grid initiatives are driving synchrophasors market growth, focusing on hybrid energy systems and DER integration.

Middle East and Africa Synchrophasors Market Analysis

The synchrophasors market in the Middle East and Africa is experiencing growth driven by increasing funding for grid modernization and transmission efficiency. GCC countries, including Saudi Arabia and the UAE, are integrating smart grid technologies to meet rising electricity demand and renewable energy goals. For example, on December 26, 2024, DEWA announced a USD 1.9 Billion smart grid project, set for completion by 2035, using AI and IoT to improve efficiency. Dubai’s power losses fell to 2% in 2023, with 1.06 CML minutes per customer, surpassing European and U.S. reliability benchmarks. South Africa is expanding PMU deployments to stabilize its grid amid increasing solar and wind integration. Despite high costs and limited infrastructure, international funding and technology partnerships are driving adoption in large-scale projects and industrial power networks.

Competitive Landscape:

The market for synchrophasors is extremely competitive, with vendors emphasizing technology innovation, strategic alliances, and regulatory support to enhance their market base. Existing vendors are investing in artificial intelligence-based analytics, cloud computing, and enhanced cybersecurity to enhance grid dependability and real-time monitoring features. The market is also seeing the rise of new companies and startups, which are coming up with affordable, lightweight, and AI-enabled synchrophasors to address the increasing need for smart grid solutions. Government policies supporting grid modernization, renewable energy integration, and power system resiliency are fueling increasing competition. Firms are engaging actively in partnership with utilities, research organizations, and energy companies to increase reach and deepen product offerings. As demand for real-time monitoring of the grid, predictive analysis, and automation grows, competition will pick up, with technology advancements in machine learning solutions, interoperability standards, and new-generation grid management solutions to promote long-term market growth.

The report provides a comprehensive analysis of the competitive landscape in the synchrophasors market with detailed profiles of all major companies, including:

- ABB Ltd.

- Arbiter Systems Inc.

- Electric Power Group LLC

- General Electric Company

- NR Electric Co. Ltd.

- Qualitrol Company LLC (Fortive Corporation)

- Schweitzer Engineering Laboratories Inc.

- Siemens AG

- Toshiba Corporation

- Vizimax Inc.

Latest News and Developments:

- January 2025: Hitachi Energy urged immediate action to build out power grids and relieve grid bottlenecks, highlighting the importance of grid upgrades to facilitate the clean energy transition. The company introduced Grid-enSure to stabilize power systems with the latest power electronics, such as synchrophasor technology, to increase grid flexibility, inertia, frequency, and voltage control to relieve capacity constraints and enhance grid reliability.

- January 2025: State Grid Zhenjiang Power Supply Company effectively employed its "Autonomous Fault Diagnosis System for Distribution Network Disconnection and Phase Loss" to clear a fault within 40 minutes. The system, installed in 29 substations, identifies faults in five minutes, cutting the fault location time from more than 30 minutes. The system improves safety, reliability, and efficiency of fault handling.

- December 2024: GE Vernova won a contract from 50Hertz Transmission GmbH to supply high-tech 300 Mvar FACTSFLEX GFM STATCOM equipment with Grid Forming Control (GFM). The system stabilizes Germany's grid by controlling voltage variation as renewable energy sources, such as wind and solar, become part of the grid. It is very important in helping Germany meet its energy transition objectives.

- October 2024: Zurich's electric utility ewz introduced the KISTERS ControlStar system to control, monitor, and plan its power grid. The system improves grid security, load flow computation, and fault detection with real-time Swissgrid data. It also facilitates automated control energy processes and big data analysis for stability in the grid, enhancing efficiency and response time in power management, including synchrophasor capabilities.

- February 2024: Gridspertise demonstrated its Virtualization and Edge Processing Platform for Medium and Low Voltage Grid Automation at Distributech International. The platform increases visibility, control, and robustness of the grid, with the Quantum Edge device providing edge synchrophasor readings for microgrids. The solution enhances transformer and LV feeder monitoring to provide faster response and more trusted power delivery.

Synchrophasors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software |

| Applications Covered | Fault Analysis, State Estimation, Stability Monitoring, Power System Control, Operational Monitoring, Improve Grid Visualization, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB Ltd., Arbiter Systems Inc., Electric Power Group LLC, General Electric Company, NR Electric Co. Ltd., Qualitrol Company LLC (Fortive Corporation), Schweitzer Engineering Laboratories Inc., Siemens AG, Toshiba Corporation, Vizimax Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the synchrophasors market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global synchrophasors market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the synchrophasors industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The synchrophasors market was valued at USD 380.88 Million in 2024.

The synchrophasors market is projected to exhibit a CAGR of 16.44% during 2025-2033, reaching a value of USD 1,601.65 Million by 2033.

The synchrophasors market is fueled by growing grid modernization initiatives, mounting integration of renewable energy, rising demand for real-time monitoring of the grid, regulatory requirements for grid reliability, innovation in smart grid technologies, and increased emphasis on cybersecurity to avoid interruptions from severe weather conditions, equipment outages, and cyber-attacks.

North America currently dominates the synchrophasors market, accounting for a share of 38.6%. The market is spurred by large-scale grid modernization initiatives, stringent regulatory requirements, growing adoption of renewable energy, mounting cybersecurity issues, and the increasing requirement for real-time monitoring of the grid to increase power system reliability and stability.

Some of the major players in the synchrophasors market include ABB Ltd., Arbiter Systems Inc., Electric Power Group LLC, General Electric Company, NR Electric Co. Ltd., Qualitrol Company LLC (Fortive Corporation), Schweitzer Engineering Laboratories Inc., Siemens AG, Toshiba Corporation, Vizimax Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)