Surge Protection Devices Market Size, Share, Trends and Forecast by Product, Type, Power Rating, End User, and Region, 2026-2034

Surge Protection Devices Market Size and Share:

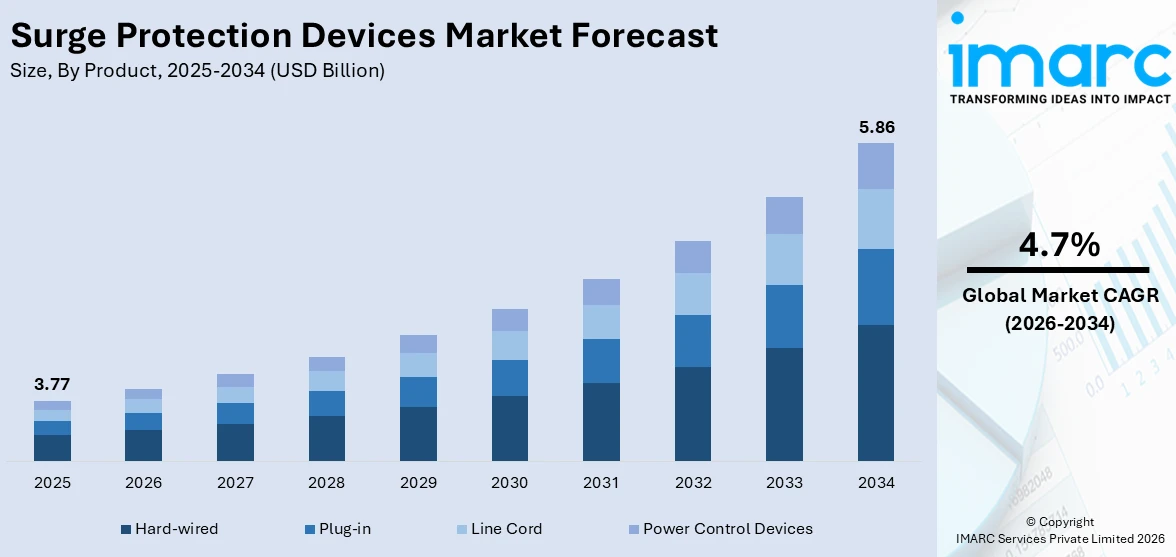

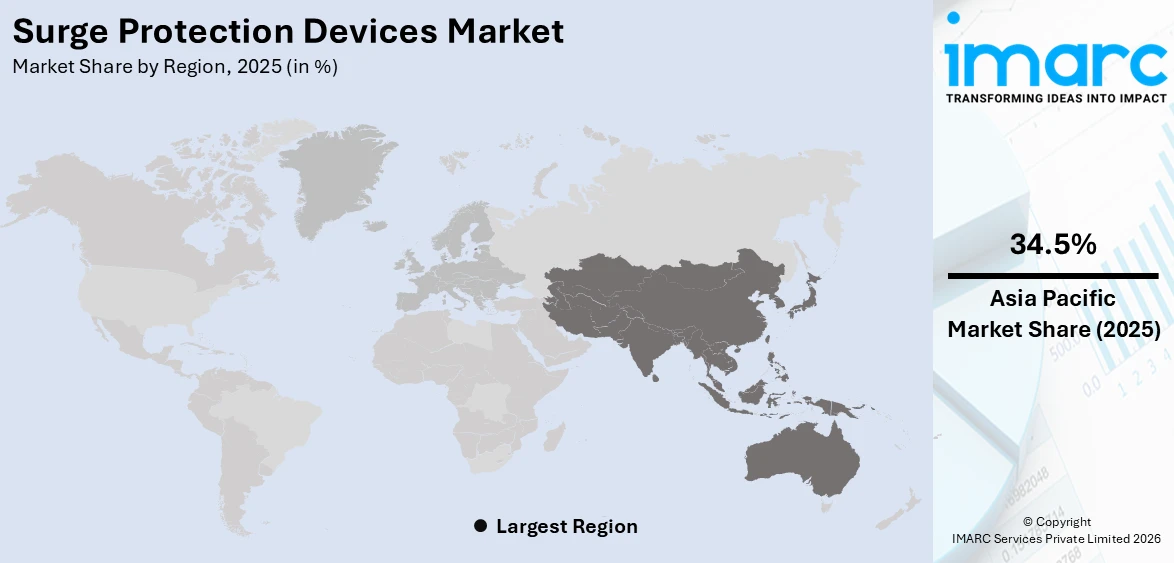

The global surge protection devices market size was valued at USD 3.77 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 5.86 Billion by 2034, exhibiting a CAGR of 4.7% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of 34.5% in 2025. The region benefits from advanced electrical infrastructure, stringent regulatory standards mandating surge protection in commercial and industrial facilities, significant investments in grid modernization and renewable energy integration, and rising demand for power quality solutions in data centers and telecommunications sectors, contributing to the surge protection devices market share.

The growing frequency of power surges caused by lightning strikes, switching transients, and utility grid fluctuations is a primary factor driving the market growth. Expanding electrification across residential, commercial, and industrial sectors is creating a substantial need for robust power protection systems. The proliferation of sensitive electronic equipment, including computing systems, telecommunications infrastructure, and automation controllers, necessitates effective surge suppression to prevent costly downtime and equipment damage. Additionally, tightening electrical safety codes and building regulations worldwide are mandating the installation of surge protective devices in new constructions and renovation projects. The rising adoption of renewable energy systems, such as solar photovoltaic installations and wind turbines, further amplifies demand as these systems require dedicated surge protection to safeguard inverters, charge controllers, and monitoring equipment from transient overvoltages during normal and abnormal operating conditions.

The United States has emerged as a major region in the surge protection devices market growth owing to many factors. The country maintains a vast and aging electrical grid infrastructure requiring continuous upgrades, including the installation of advanced surge protection systems to mitigate power quality issues. In 2025, utilities such as Pacific Gas & Electric unveiled a multibillion‑dollar transmission upgrade plan to accommodate surging electricity demand from data centers and other critical loads highlighting infrastructure stress and the need for better power‑quality safeguards. Rapid expansion of data center facilities across the nation is creating significant demand for high-performance surge protective devices to safeguard critical computing and networking equipment.

To get more information on this market Request Sample

Surge Protection Devices Market Trends:

Integration of IoT-Enabled Surge Protection Systems

The integration of Internet of Things (IoT) capabilities into surge protection devices represents a significant shift in power protection technology. Modern surge protectors are being equipped with embedded sensors, wireless connectivity modules, and cloud-based monitoring platforms that enable real-time tracking of device health, surge event logging, and predictive maintenance alerts. As per sources, Weidmüller launched its VARITECTOR PU AC IoT surge protection arrester series with real‑time status monitoring and cloud integration, showcasing industry momentum toward intelligent, connected surge protection hardware. These smart surge protection systems allow facility managers and building operators to remotely monitor the operational status of protection devices across multiple locations simultaneously, reducing the need for manual inspections.

Adoption of Type 2 Coordinated Protection Solutions

The growing emphasis on coordinated surge protection strategies is reshaping the surge protection devices market outlook as end users increasingly adopt multi-stage protection architectures. Type 2 surge protective devices serve as the cornerstone of coordinated protection schemes, providing secondary protection at distribution panels that complements primary Type 1 devices installed at service entrances. In October 2025, Schneider Electric launched an industry first plug and play surge protection device that integrates Type 2+3 protection directly into distribution boards, reflecting how manufacturers are simplifying and standardizing coordinated multi‑stage protection solutions. This layered approach ensures that residual surge energy passing through upstream protection is effectively clamped to safe levels before reaching sensitive downstream equipment.

Expansion of Surge Protection in Renewable Energy Systems

The rapid global deployment of renewable energy installations is creating substantial opportunities for surge protection device manufacturers as the surge protection devices market forecast indicates growing requirements for specialized protection solutions. Solar photovoltaic systems and wind energy installations are particularly vulnerable to transient overvoltages caused by lightning strikes and switching operations due to their exposed mounting locations and extensive wiring configurations. In February 2026, Phoenix Contact launched its VALVETRAB Safe Protection Plus surge protective devices that include enhanced features specifically supporting photovoltaic applications and industrial power systems, highlighting how manufacturers are addressing surge risks in renewable energy environments. Surge protective devices specifically designed for direct current applications and photovoltaic string protection are experiencing strong demand as solar installations proliferate across utility-scale, commercial, and residential segments.

Surge Protection Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global surge protection devices market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, type, power rating, and end user.

Analysis by Product:

- Hard-wired

- Plug-in

- Line Cord

- Power Control Devices

Hard-wired holds 48.5% of the market share, these are permanently installed within the electrical panel or distribution board of a building, providing comprehensive whole-structure protection against transient overvoltages. These devices are favored in commercial, industrial, and residential applications due to their ability to protect all downstream circuits and connected equipment simultaneously. The permanent installation nature eliminates the risk of user error associated with portable alternatives and ensures continuous protection without requiring manual intervention. Electricians and building contractors increasingly specify hard-wired surge protectors as integral components of modern electrical systems to meet evolving safety codes and building regulations. The growing complexity of electrical installations in smart buildings and automated facilities further necessitates robust panel-mounted surge protection. Additionally, hard-wired devices offer superior surge handling capacity and longer operational lifespans compared to plug-in alternatives, making them a preferred choice for mission-critical applications where uninterrupted protection is essential.

Analysis by Type:

- Type 1

- Type 2

- Type 3

- Type 4

Type 2 leads the market with a share of 58.5%, these are installed at the main distribution board level, serving as the primary protection layer for downstream electrical circuits and connected equipment within buildings. These devices are designed to handle residual surge energy that passes through upstream protection and limit transient overvoltages to safe levels before they reach sensitive loads. The surge protection devices market trends reflect growing preference for type 2 devices due to their versatility in protecting a wide range of commercial and industrial electrical systems. As per sources, DEHN introduced the DEHNguard M DC ACI 1250 FM, a modular Type 2 arrester for high-power DC fast charging and battery storage, providing protection up to 1250 V. Type 2 devices offer an optimal balance between protection performance and cost efficiency, making them the preferred choice for standard installations in office buildings, manufacturing plants, retail establishments, and institutional facilities.

Analysis by Power Rating:

- 0-50 kA

- 50.1-100 kA

- 100.1-200 kA

- 200.1 kA and Above

0-50 kA dominates the market, with a share of 45.5%, deploying across residential, light commercial, and small-scale industrial applications due to their suitability for protecting standard electrical circuits and sensitive consumer electronics. These devices provide adequate protection against typical transient overvoltages encountered in everyday environments, including those caused by lightning-induced surges, utility grid switching, and internal load changes. Their compact form factor, cost-effectiveness, and ease of installation make them highly accessible to a broad customer base, from individual homeowners to small business operators. The growing proliferation of electronic devices, home automation systems, and connected appliances in residential settings continues to drive demand for protection solutions within this power rating category. Additionally, the increasing availability of compact modular designs facilitates integration into existing electrical panels and consumer power strips without significant modifications.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Commercial Complexes

- Data Centre

- Industries and Manufacturing Units

- Medical

- Residential Buildings and Spaces

- Telecommunication

- Transportation

- Others

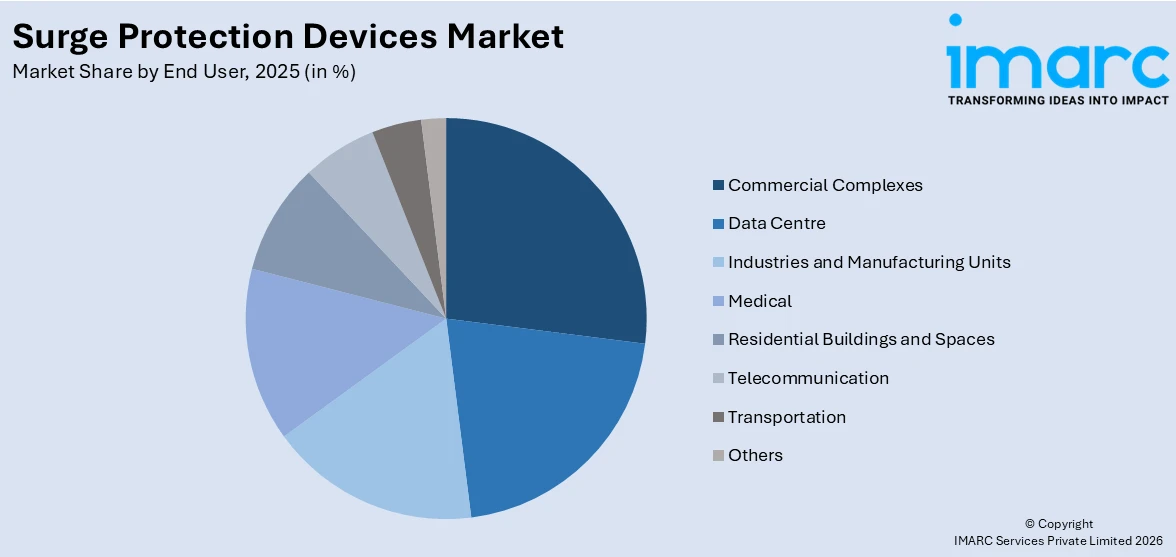

Commercial complexes represent the leading segment, with a market share of 26.8%, encompassing office buildings, retail centers, hospitality establishments, and mixed-use developments, constitute the largest end-user segment for surge protection devices owing to their extensive electrical infrastructure and reliance on sensitive electronic systems. These facilities house critical equipment including HVAC control systems, fire and safety networks, elevators, point-of-sale terminals, security cameras, and computer networks that require continuous and reliable protection against power surges. The increasing adoption of building management systems and smart building technologies further amplifies the need for comprehensive surge protection across multiple distribution points within commercial properties. Property managers and building owners recognize that the cost of surge-related equipment damage, data loss, and operational downtime far exceeds the investment in proper surge protection infrastructure. Insurance requirements and compliance with local electrical safety codes additionally mandate the installation of surge protective devices in commercial buildings.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Other

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Other

- Latin America

- Brazil

- Mexico

- Other

- Middle East and Africa

Asia Pacific, accounting for 34.5% of the share, maintaining the leading position in the market. The region's dominance is primarily attributed to its massive and rapidly expanding industrial base, extensive infrastructure development programs, and growing investments in power generation and distribution networks across major economies. Countries such as China, India, Japan, South Korea, and Australia are driving demand through large-scale construction activities, manufacturing expansion, and the modernization of aging electrical grids. The proliferation of data centers, telecommunications infrastructure, and renewable energy installations across the region further elevates the requirement for reliable surge protection solutions. Government-led initiatives promoting electrical safety standards and smart grid development are accelerating the adoption of surge protective devices. Additionally, the rising urbanization rate and increasing consumer awareness regarding the protection of sensitive electronic equipment in residential and commercial settings are contributing to sustained market expansion throughout the Asia Pacific region.

Key Regional Takeaways:

North America Surge Protection Devices Market Analysis

North America represents a significant and mature market for surge protection devices, driven by well-established electrical safety regulations, advanced infrastructure networks, and high awareness regarding power quality management among commercial and industrial end users. The region benefits from stringent building codes enforced at both national and state levels that mandate the installation of surge protective devices in new construction and renovation projects. The rapid growth of data center capacity across the United States and Canada, fueled by increasing demand for cloud computing, artificial intelligence, and digital services, is generating substantial requirements for comprehensive surge protection systems. The expansion of renewable energy installations, particularly solar photovoltaic systems and wind farms, is creating additional demand for specialized protection solutions tailored to distributed generation applications. Furthermore, the increasing frequency of severe weather events, including thunderstorms and lightning activity, heightens awareness and urgency among property owners and facility managers to invest in robust surge protection infrastructure. The modernization of aging electrical grids and the integration of smart grid technologies across the region are also propelling market advancement, as these upgraded systems require enhanced protection against transient overvoltages to maintain operational reliability.

United States Surge Protection Devices Market Analysis

The United States represents the largest national market within North America, driven by extensive electrical infrastructure development and stringent safety regulations governing commercial and industrial installations. The country maintains a vast network of commercial buildings, industrial facilities, and data centers that require comprehensive surge protection to safeguard sensitive electronic equipment and maintain operational continuity. According to reports, in January 2026, ABR Electric reported that updated NEC surge protection requirements now mandate Type 1 or Type 2 SPDs in residential panelboards, affecting over 1.2 million U.S. homes annually. The national electrical code has progressively expanded requirements for surge protective device installation, including mandatory whole-house surge protection for residential dwelling units, significantly expanding the addressable market. Rapid growth in data center construction, particularly hyperscale facilities supporting cloud computing and artificial intelligence workloads, creates substantial demand for high-performance surge protection solutions. The increasing deployment of renewable energy systems, including rooftop solar installations and community solar projects, generates requirements for specialized direct current surge protective devices. Federal infrastructure investment programs supporting grid modernization and electrification initiatives provide additional growth opportunities for manufacturers and suppliers. The mature electrical contractor and distributor network facilitates efficient market penetration across diverse geographic regions and end-use applications, supporting widespread adoption of advanced surge protection technologies throughout the country.

Europe Surge Protection Devices Market Analysis

Europe represents a significant market for surge protection devices, supported by comprehensive regulatory frameworks and the region's focus on electrical safety and equipment protection. The European Union's low voltage directive and harmonized standards, including IEC 61643 series requirements, establish clear guidelines for surge protective device performance and installation that drive consistent market demand. The region's extensive industrial manufacturing base, particularly in automotive, pharmaceutical, and precision engineering sectors, requires reliable surge protection to maintain production quality and minimize equipment downtime. Growing investment in renewable energy infrastructure, especially solar photovoltaic and offshore wind installations, creates expanding demand for specialized surge protection solutions designed for renewable energy applications. The ongoing transition toward smart building technologies and building automation systems in commercial properties increases the need for effective transient overvoltage protection. European manufacturers continue to develop advanced surge protective devices incorporating innovative technologies and enhanced safety features that meet the region's stringent performance and environmental standards, contributing to product development and technological leadership within the global surge protection industry.

Asia-Pacific Surge Protection Devices Market Analysis

Asia-Pacific is leading as a rapidly growing market for surge protection devices, driven by accelerating industrialization, expanding urban infrastructure development, and increasing electrification across developing economies. The region's massive construction activity, encompassing residential complexes, commercial buildings, and industrial parks, creates substantial requirements for electrical protection equipment including surge protective devices. Growing adoption of manufacturing automation and process control systems in countries throughout the region necessitates reliable surge protection to safeguard sensitive electronic equipment. The rapid expansion of telecommunications infrastructure, data centers, and renewable energy installations further amplifies demand for specialized surge protection solutions. Increasing awareness of power quality challenges and the economic impact of equipment damage caused by transient overvoltages encourages both public and private sector investment in comprehensive electrical protection measures throughout the region.

Latin America Surge Protection Devices Market Analysis

Latin America presents growing opportunities for the surge protection devices market, supported by increasing infrastructure investment, expanding industrial activity, and rising awareness of electrical safety requirements across the region. The development of commercial real estate, manufacturing facilities, and telecommunications infrastructure drives demand for reliable surge protective devices. Growing deployment of renewable energy systems, particularly solar installations, creates additional requirements for specialized protection solutions. Improving regulatory frameworks in key markets are gradually introducing mandatory surge protection requirements for commercial and industrial buildings. The region's susceptibility to frequent lightning activity in tropical areas heightens the need for robust surge protection. Additionally, ongoing modernization of electrical distribution networks and increasing adoption of digital technologies in industrial operations further contribute to growing demand.

Middle East and Africa Surge Protection Devices Market Analysis

The Middle East and Africa region is witnessing growing adoption of surge protection devices, driven by large-scale infrastructure development projects, expanding industrial diversification initiatives, and increasing investment in energy infrastructure. Rapid urbanization and construction of commercial buildings, hospitality facilities, and industrial zones create demand for electrical protection solutions including surge protective devices. The development of renewable energy projects, particularly solar installations in sun-rich areas, requires dedicated surge protection for photovoltaic systems and associated equipment. Growing telecommunications infrastructure deployment across the region further supports market expansion. Improving electrical safety awareness and the gradual adoption of international electrical standards encourage broader implementation of surge protective measures across commercial and industrial installations throughout the region.

Competitive Landscape:

The global surge protection devices market is characterized by the presence of several established manufacturers competing through product innovation, technological advancement, and strategic expansion initiatives. Leading companies focus on developing surge protective devices with enhanced performance characteristics, including higher surge current ratings, faster response times, improved coordination capabilities, and integrated monitoring features. Strategic acquisitions and partnerships enable major players to expand their product portfolios and strengthen their geographic presence across key markets. Manufacturers are investing in research and development to introduce next-generation surge protection solutions incorporating IoT connectivity, predictive analytics, and smart monitoring capabilities that address evolving customer requirements. The competitive landscape also features regional manufacturers offering cost-competitive solutions tailored to local market requirements and regulatory standards.

The report provides a comprehensive analysis of the competitive landscape in the surge protection devices market with detailed profiles of all major companies, including:

- ABB Ltd.

- Eaton Corporation PLC

- Emerson Electric Co.

- Havells India Ltd.

- Hubbell Incorporated

- Legrand S.A.

- Littelfuse, Inc.

- Mersen

- Schneider Electric

- Siemens AG

- Signify Holding

Latest News and Developments:

- In November 2024, Noark Electric NA introduced the U4 Surge Protective Device series, featuring Type 4 modular plug-in SPDs with 20 kA nominal discharge, 175–660 V operating voltage, multiple pole configurations, and UL 1449 recognition, suitable for commercial, residential, and industrial applications to protect against transient voltage surges.

- In August 2024, Bourns introduced the Model 1270 Series IEC Class I AC Surge Protective Devices, providing up to 80 kA surge protection. These DIN-rail pluggable SPDs are designed for main switchboards, branch panels, EV charging stations, and heavy industrial installations, ensuring compliance with IEC/EN 61643-11 standards.

Surge Protection Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Hard-wired, Plug-in, Line Cord, Power Control Devices |

| Types Covered | Type 1, Type 2, Type 3, Type 4 |

| Power Ratings Covered | 0-50 kA, 50.1-100 kA, 100.1-200 kA, 200.1 kA and Above |

| End Users Covered | Commercial Complexes, Data Center, Industries and Manufacturing Units, Medical, Residential Buildings and Spaces, Telecommunication, Transportation, Others |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | ABB Ltd., Eaton Corporation PLC, Emerson Electric Co., Havells India Ltd., Hubbell Incorporated, Legrand S.A., Littelfuse, Inc., Mersen, Schneider Electric, Siemens AG, Signify Holding, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the surge protection devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global surge protection devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the surge protection devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The surge protection devices market was valued at USD 3.77 Billion in 2025.

The surge protection devices market is projected to exhibit a CAGR of 4.7% during 2026-2034, reaching a value of USD 5.86 Billion by 2034.

The surge protection devices market is primarily driven by expanding electrical infrastructure development, increasing adoption of sensitive electronic equipment across industrial and commercial sectors, stringent regulatory requirements mandating surge protection in buildings, growing deployment of renewable energy systems requiring specialized protection, and rising awareness of the economic consequences associated with equipment damage caused by transient overvoltage events.

Asia Pacific currently dominates the surge protection devices market, accounting for a share of 34.5%. The region benefits from mature electrical infrastructure requiring ongoing upgrades, stringent safety codes mandating surge protection, extensive data center deployments, and substantial investments in grid modernization, renewable energy integration, and smart building technologies.

Some of the major players in the surge protection devices market include ABB Ltd., Eaton Corporation PLC, Emerson Electric Co., Havells India Ltd., Hubbell Incorporated, Legrand S.A., Littelfuse, Inc., Mersen, Schneider Electric, Siemens AG, Signify Holding, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)