Supercapacitor Market Size, Share, Trends and Forecast by Product Type, Module Type, Material Type, End Use Industry, and Region, 2026-2034

Global Supercapacitor Market Size, Share, Trends & Forecast (2026-2034)

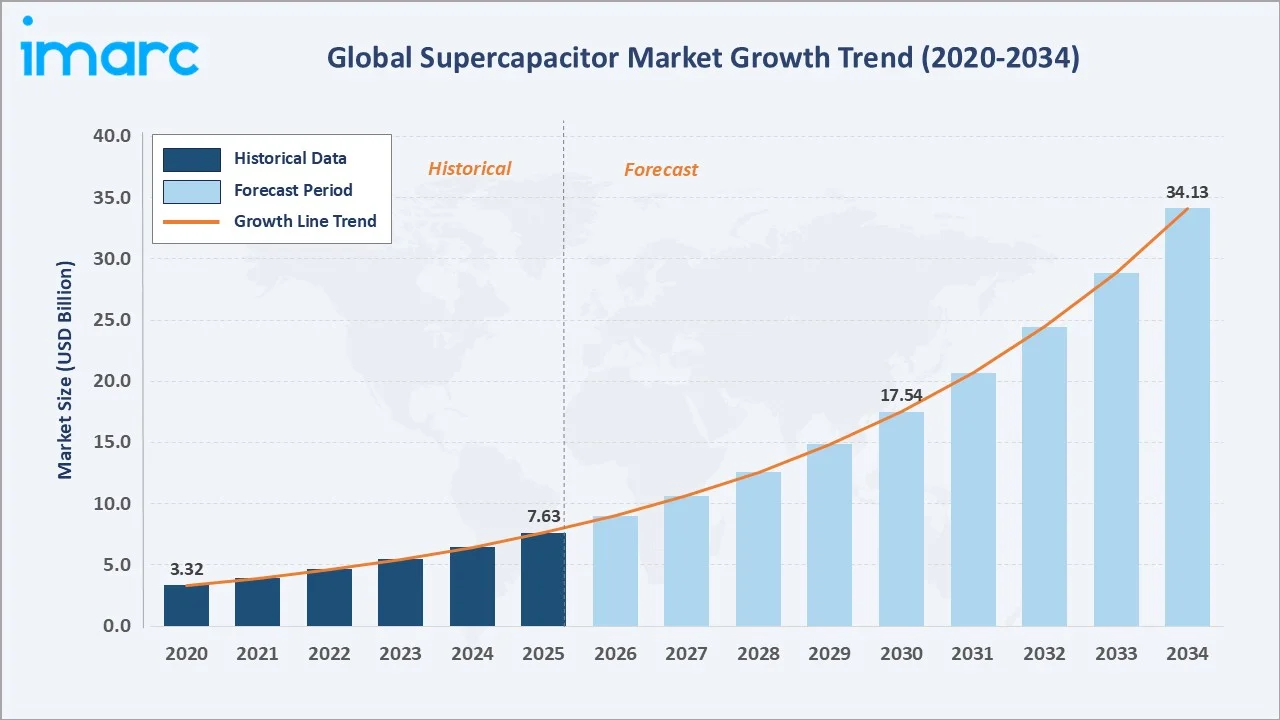

The global supercapacitor market size was valued at USD 7.63 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 34.13 Billion by 2034, exhibiting a CAGR of 18.11% during the forecast period (2026-2034). Rapid expansion of electric vehicle infrastructure, the scaling of renewable energy storage systems, and the proliferation of consumer electronics requiring high-power compact solutions are collectively propelling supercapacitor market growth globally.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.63 Billion |

|

Forecast Market Size (2034) |

USD 34.13 Billion |

|

CAGR (2026-2034) |

18.11% |

|

Largest Region |

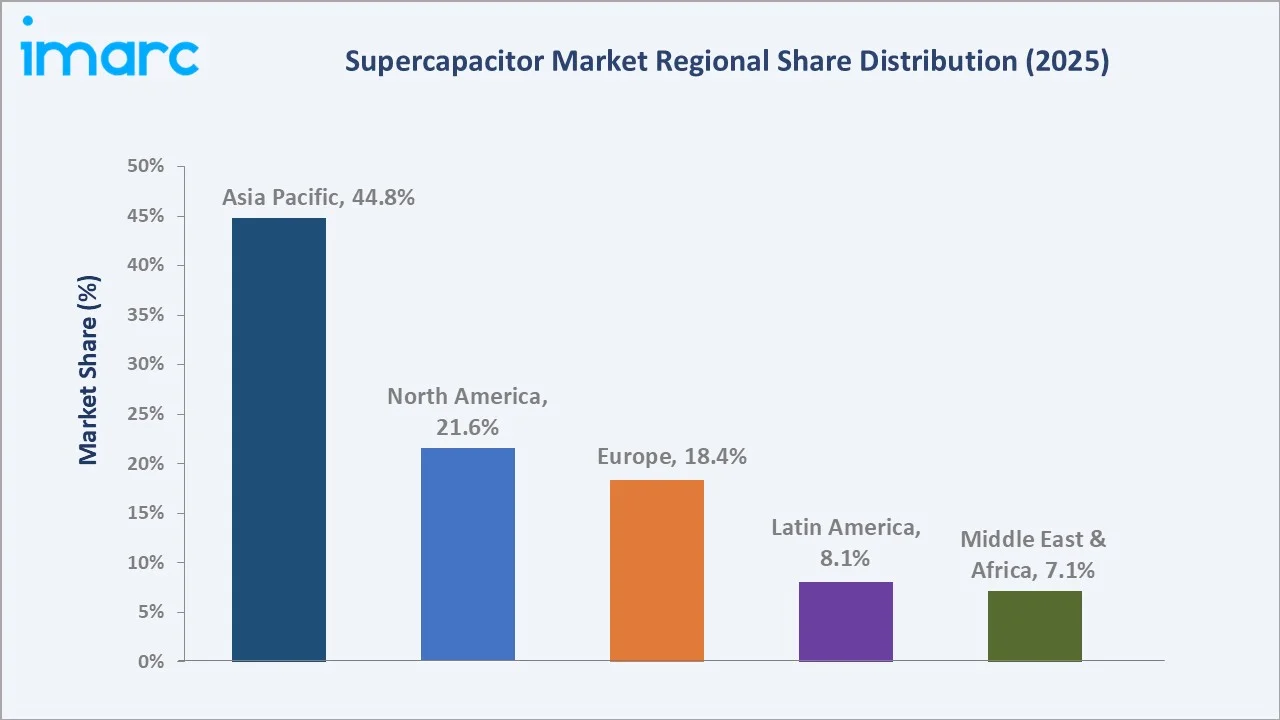

Asia Pacific (44.8%, 2025) |

|

Fastest Growing Region |

Latin America |

|

Leading Product Type |

Pseudocapacitors (38.5%, 2025) |

|

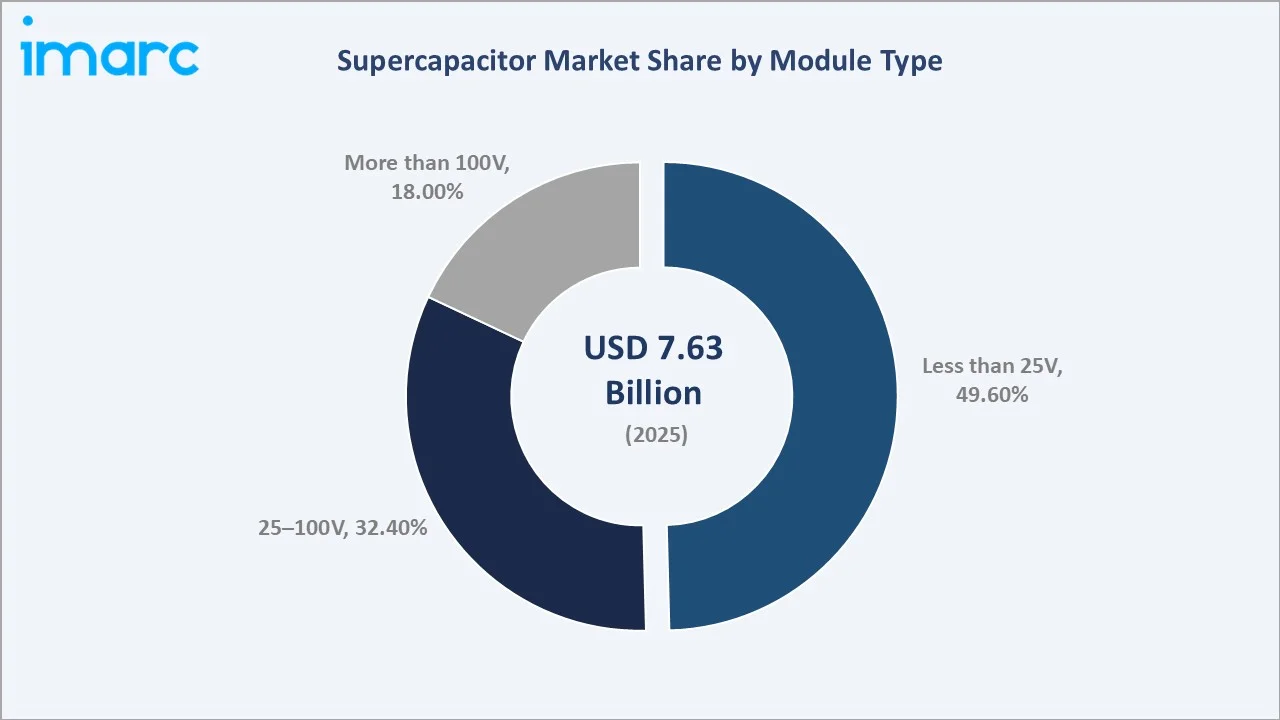

Leading Module Type |

Less than 25V (49.6%, 2025) |

The expanding ecosystem of renewable energy globally is creating sustained demand for fast-charge, high-cycle energy storage components, as solar and wind assets require responsive buffering systems in which supercapacitors excel. The surge in electric vehicle production, with global EV sales approaching 14 million units in 2023, according to the International Energy Agency (IEA), has generated significant demand for supercapacitors enabling regenerative braking and rapid power delivery.

To get more information on this market, Request Sample

The United States has emerged as a major region in the supercapacitor market owing to many factors. According to the International Energy Agency, new electric car registrations in the United States totaled 1.4 million in 2023, marking a more than 40% increase compared to the prior year, driving parallel demand for supercapacitor-based hybrid energy management systems.

Executive Summary

The global supercapacitor market was valued at USD 7.63 Billion in 2025, propelled by the accelerating adoption of electric vehicles, expanding deployment of renewable energy systems, and rapid proliferation of IoT devices and industrial automation applications worldwide. The market is projected to reach USD 34.13 Billion by 2034, exhibiting a CAGR of 18.11% over the forecast period 2026–2034.

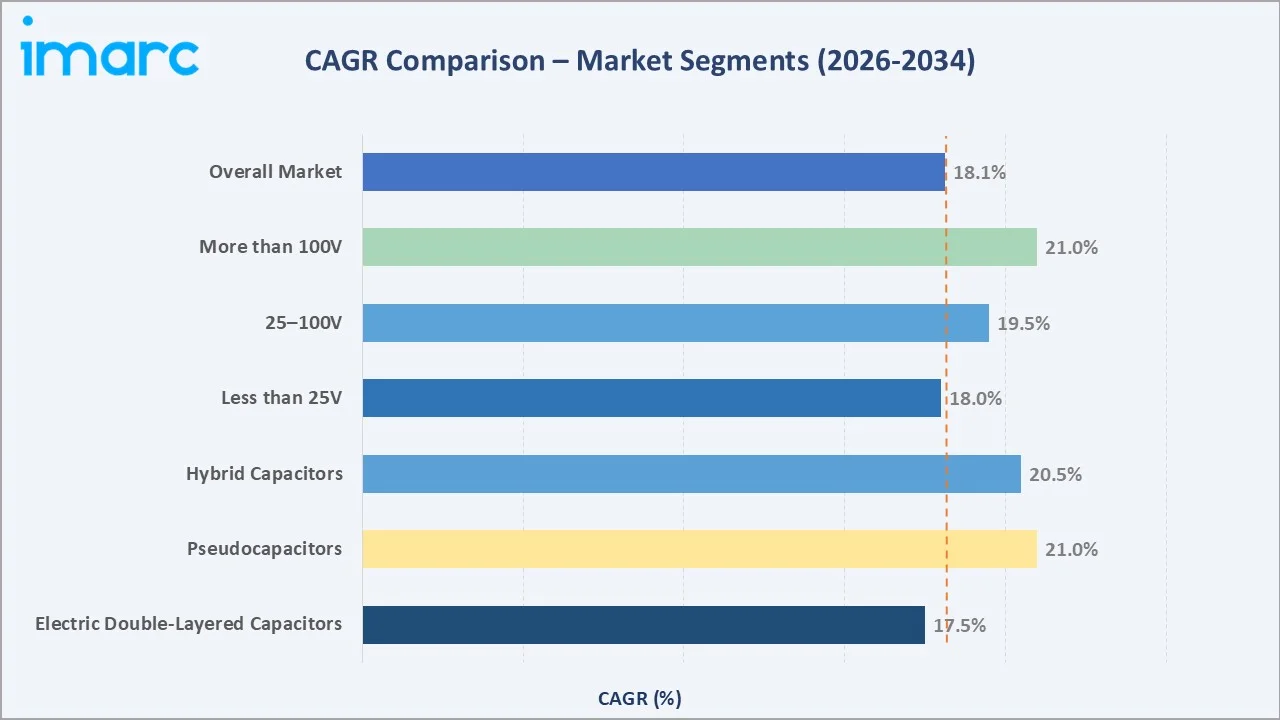

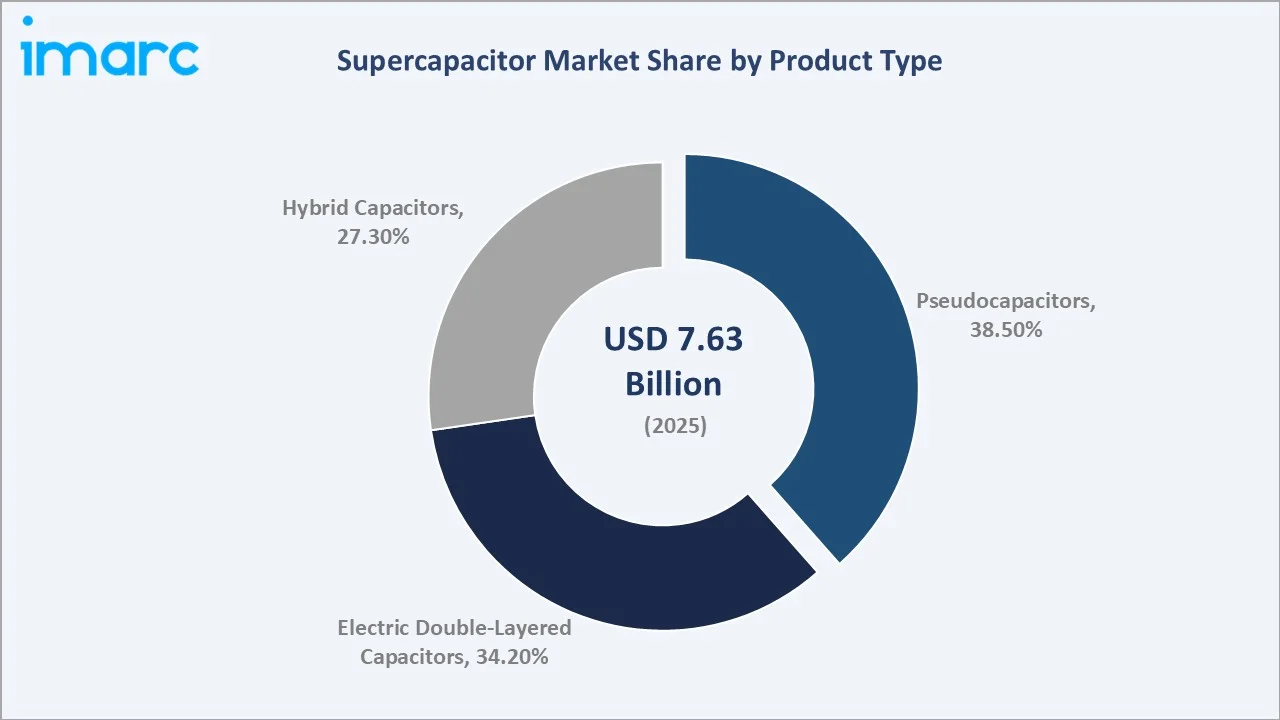

By product type, pseudocapacitors lead at 38.5% (2025), valued for their superior energy density and versatile applicability across portable electronics, medical devices, and IoT platforms through faradaic electrode reactions. Electric Double-Layered Capacitors (EDLCs) account for 34.2%, preferred for high-power, long-cycle applications in automotive and renewable energy, while Hybrid Capacitors hold the remaining 27.3%, emerging as the fastest-growing sub-segment.

By module type, the less than 25V segment dominates at 49.6% (2025), driven by expansive consumer electronics and low-power IoT device demand, followed by the 25–100V range at 32.4% for automotive and industrial control systems, and the more than 100V tier at 18.0% serving heavy industrial and grid-scale applications.

North America (21.6%), Europe (18.4%), Latin America (8.1%), and the Middle East and Africa (7.1%) complete the regional landscape. Key growth trends include the rapid development of hybrid energy storage architectures combining supercapacitors with lithium-ion batteries to optimize EV regenerative braking and grid frequency response, breakthroughs in graphene and carbon-metal oxide electrode materials substantially lifting energy density thresholds, and the growing integration of supercapacitors into AI datacenter infrastructure for peak power management.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type Segment |

Pseudocapacitors – 38.5% (2025) |

|

Largest Module Type Segment |

Less than 25V – 49.6% (2025) |

|

Leading Region |

Asia Pacific – 44.8% (2025) |

|

Fastest Growing Region |

Asia Pacific (dominant CAGR leadership) |

|

Top Companies |

Maxwell Technologies, Skeleton Technologies, Eaton, CAP-XX, Nippon Chemi-Con |

|

Key Opportunity |

EV + renewable energy hybrid storage systems — USD 15B+ addressable by 2034 |

Key analytical observations supporting the data points above:

- Pseudocapacitors' 38.5% share reflects their unique ability to deliver both high power and energy density via faradaic reactions at the electrode-electrolyte interface, making them the preferred technology for medical devices, portable electronics, and IoT applications.

- The less than 25V segment's 49.6% dominance is underpinned by enormous volume demand from consumer electronics, low-power IoT sensors, and industrial control systems.

- Asia Pacific's 44.8% share reflects China's dual position as both the world's largest EV manufacturer and the dominant hub for consumer electronics production, complemented by South Korea's advanced battery-supercapacitor hybrid R&D ecosystem and Japan's precision electronics supply chains driving consistent high-volume demand at scale.

Global Supercapacitor Market Overview

Market Trends

To evaluate market opportunities, Request Sample

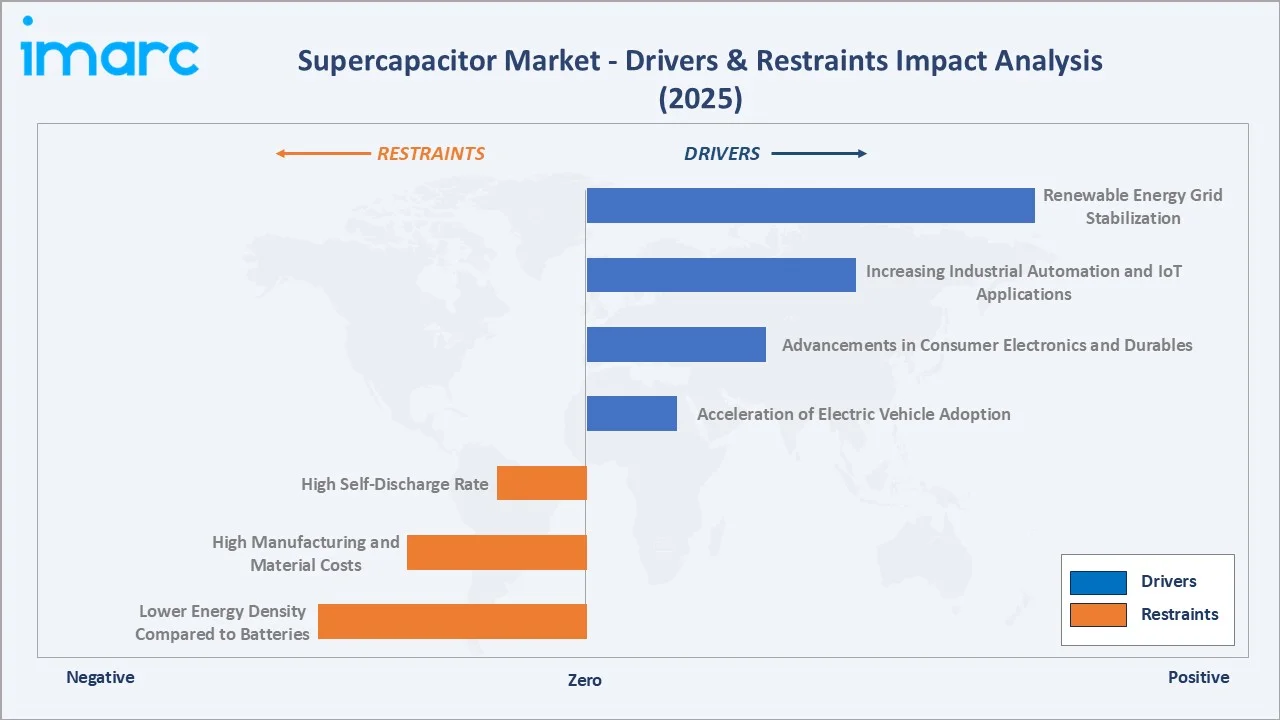

- Acceleration of Electric Vehicle Adoption: Electric vehicles are rapidly replacing internal combustion engine vehicles globally, driven by declining battery costs, expanding public charging infrastructure, and substantial government incentive programs across major economies. According to the International Energy Agency, Electric car sales topped 17 million worldwide in 2024, rising by more than 25%.1 Just the additional 3.5 million cars sold in 2024 compared to 2023 outnumber total electric car sales in the whole of 2020, reflecting the depth of policy-driven EV adoption in leading markets.

- Advancements in Consumer Electronics and Durables: The global consumer electronics and durables industry is advancing at an extraordinary pace, and wearable device adoption continuing its strong upward trajectory across health, fitness, and entertainment segments. As of October 2025, India is projected to become the fourth largest market for consumer durables by FY27, with the sector growing at an 11% CAGR. Escalating consumer expectations for faster device charging, longer operational durations, and progressively smaller form factors are intensifying engineering requirements for energy storage solutions that combine high power density with extended cycle life.

- Increasing Industrial Automation and IoT Applications: Industrial automation is fundamentally transforming manufacturing, logistics, and process management worldwide, driving parallel demand for dependable, high-cycle power solutions capable of supporting autonomous systems at scale. The Internet of Things (IoT) connectivity layer is expanding rapidly across smart factories, utility networks, and agricultural systems, with the number of connected IoT devices projected to grow by 13% by end of 2024 according to IoT Analytics.

Market Restraints

- Lower Energy Density Compared to Batteries: Supercapacitors exhibit a lower energy density compared to batteries. Li-ion batteries can achieve energy densities up to 650 watt-hours per liter (Wh/L), while even the most advanced supercapacitors offer only around 10 Wh/L or 1.5% of a battery's energy density. This significant disparity limits supercapacitor suitability for applications requiring sustained, long-duration power delivery, such as extended-range EVs or large-scale grid storage, where batteries continue to dominate.

- High Manufacturing and Material Costs: A major restraint in the supercapacitor market is the high production cost, particularly for models utilizing advanced materials such as graphene and carbon nanotubes. These materials, while offering improved performance, increase the overall manufacturing cost of supercapacitors, making them less economically viable for mass adoption in price-sensitive industries such as consumer electronics and renewable energy storage.

- High Self-Discharge Rate: Some supercapacitors can exhibit a higher self-discharge rate compared to batteries, which may be a concern for long-term energy storage applications. This characteristic limit supercapacitor deployment in standby or low-duty-cycle applications where energy retention over extended periods is a critical operational requirement, such as backup systems in remote infrastructure.

Market Opportunities

- Renewable Energy Grid Stabilization: As global renewable capacity additions grew from 180 GW to 360 GW, the demand for supercapacitors in grid applications increased sharply from 12 million to 45 million units. The accelerating integration of solar and wind power globally is creating sustained demand for fast-response energy buffering solutions, and supercapacitors, with their sub-second response capabilities, are uniquely positioned to address grid frequency regulation and intermittency management at scale.

- AI-Driven Data Center Power Demand: Datacenter demand for uninterruptible power during artificial intelligence surges is emerging as a high-value opportunity segment. In June 2025, Skeleton Technologies launched GrapheneGPU, a peak-shaving capacity shelf that ditches lithium for supercapacitor energy storage based on Skeleton Technologies' patented Curved Graphene technology.

- Micro-Supercapacitors for Wearables and IoT: The miniaturization of supercapacitor energy storage devices opens new opportunities in wearable technology and IoT devices, where quick charging and long cycle life are critical requirements. The exponential growth of connected sensor networks, health monitoring wearables, and edge computing devices is creating a high-volume addressable market for compact, maintenance-free supercapacitor solutions engineered for constrained form factors.

Market Challenges

- Energy Density Limitations vs. Batteries: While supercapacitors offer high power density and rapid charge/discharge capabilities, they have significantly lower energy density compared to lithium-ion batteries. This limits their ability to store energy for long durations, restricting their adoption in applications requiring sustained power supply such as electric vehicles and grid storage.

- High Initial Cost and Material Constraints: Supercapacitors rely on advanced materials such as activated carbon, graphene, and other nanomaterials, which increase production costs. Compared to conventional batteries, the higher upfront cost creates adoption barriers, particularly in price-sensitive markets and large-scale commercial applications.

- Integration and Standardization Challenges: The lack of standardized designs and integration frameworks across industries makes it difficult to seamlessly incorporate supercapacitors into existing systems. Compatibility issues with current battery-based architectures and the need for hybrid energy storage systems increase complexity, requiring additional engineering and system-level optimization.

Emerging Market Trends

The global supercapacitor market is being reshaped by five converging trends redefining product architecture, application expansion, and competitive dynamics across all geographies through 2034.

1. Hybridization of Energy Storage Architecture

The most defining structural shift of 2025 is the transition from pure Electric Double-Layered Capacitors to Lithium-Ion Capacitors and hybrid supercapacitor-battery systems. These architectures deliver battery-like energy density alongside capacitor-grade power delivery, addressing OEM demands across automotive, grid-stabilization, and industrial automation sectors simultaneously.

In January 2024, Skeleton Technologies, AVL Deutschland, and Fraunhofer IEE demonstrated up to 20% longer battery life and 6% improved electrical efficiency through their SuKoBa hybrid energy storage project, validating hybrid architecture's commercial viability at scale.

2. Advanced Materials Innovation — Graphene and Curved Carbon Electrodes

Breakthroughs in graphene and nanocarbon electrode materials are fundamentally elevating supercapacitor performance. Curved graphene now enables electrode surface areas exceeding 2,000 m²/g, pushing energy densities toward 65 Wh/kg, substantially narrowing the gap with lithium-ion batteries at commercially viable cost points.

In November 2024, NETL U.S. National Laboratory converted coal tar pitch into high-quality graphene for advanced supercapacitors, reducing production costs significantly. Ionic liquid electrolytes, scaling commercially in 2025, have pushed per-cell voltage from 2.7V to 3.0V, improving energy density by approximately 23%.

3. Electric Vehicle and Regenerative Braking Integration

Global EV adoption is the single largest demand driver for supercapacitors. Their millisecond-level charge-discharge capability makes them irreplaceable for regenerative braking and start-stop systems, recovering up to 85% more kinetic energy than battery-only configurations across hybrid and fully electric vehicle platforms.

Industry Value Chain Analysis

The supercapacitor industry value chain encompasses seven interconnected stages from raw material sourcing through end-application deployment. Specialized materials science expertise, precision manufacturing capabilities, and rigorous quality management are required at each stage to meet the power, cycle-life, and safety performance demanded by automotive, industrial, and electronics end-users globally.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Sourcing |

Activated carbon, graphene, ionic liquid electrolytes, conductive polymer procurement |

Coconut-shell carbon suppliers, First Graphene, Vorbeck Materials, electrolyte chemical manufacturers |

|

Electrode & Cell Manufacturing |

Carbon electrode fabrication, electrolyte filling, separator integration, cell assembly |

Maxwell Technologies, Skeleton Technologies, Nippon Chemi-Con, LS Materials Co., Ltd., VINATech |

|

Module & System Integration |

Multi-cell module assembly, voltage balancing, thermal management, BMS integration |

Eaton, Siemens, Cornell Dubilier, IOXUS, Musashi Energy Solutions |

|

OEM & Application Engineering |

Product customization for EV, grid, industrial, and consumer electronics requirements |

Maxwell, Murata Manufacturing, CAP-XX, TDK Corporation |

|

Distribution & Channel Management |

Global distribution networks, e-commerce platforms, OEM direct supply contracts |

Premier Farnell (Avnet), Arrow Electronics, regional distributors across Asia, Europe, and the Americas |

|

End-Application Deployment |

EV regenerative braking, grid frequency response, IoT devices, AI datacenters, medical |

Automotive OEMs, grid operators, consumer electronics brands, defense agencies, datacenter operators |

The electrode and cell manufacturing stage is the primary value creation point, where proprietary electrode materials and cell architectures determine energy density, power output, and cycle-life, the key performance differentiators.

Technology Landscape in the Supercapacitor Industry

AI-Driven Manufacturing and Predictive Performance Optimization

AI and machine learning are transforming supercapacitor production and field deployment. AI-driven manufacturing processes have improved production efficiency by approximately 20%, reducing unit costs while enhancing graphene electrode quality control across high-volume production lines in Asia, Europe, and North America.

Smart Grid and Renewable Energy Integration Technology

Supercapacitors are increasingly deployed as grid-edge fast-response storage operating alongside batteries in hybrid energy systems. Their sub-second response capability provides frequency regulation and voltage stabilization for solar and wind installations where intermittent generation creates grid instability challenges across both developed and emerging market power networks.

Hybrid Supercapacitor-Battery Integration Technology

Hybrid energy storage systems combining supercapacitors with lithium-ion batteries are rapidly transitioning from laboratory prototypes to commercial deployments. This architecture leverages supercapacitors for instantaneous peak-power delivery while batteries handle sustained energy output — optimizing both performance and battery longevity across EV, industrial automation, and grid-stabilization applications simultaneously.

Market Segmentation Analysis

By Product Type

Pseudocapacitors account for 38.5% of the global supercapacitor market share in 2025, establishing them as the dominant product segment by revenue. Unlike conventional electric double-layer capacitors, pseudocapacitors utilize faradaic charge-transfer mechanisms at the electrode-electrolyte interface, enabling significantly higher energy density while retaining the rapid charge-discharge capability that defines

the supercapacitor category.

To access detailed market analysis, Request Sample

By Module Type

The less than 25V module type accounts for 49.6% of the global supercapacitor market in 2025, establishing it as the dominant segment by a substantial margin. Low-voltage supercapacitors are extensively deployed across consumer electronics, IoT edge devices, industrial control systems, and medical monitoring equipment, all markets experiencing strong secular demand growth.

Regional Market Insights

The region is segmented to Asia-Pacific, North America, Europe, Latin America, Middle east and Africa. Asia Pacific holds the largest regional market share at 44.8% in 2025, underpinned by China's dominant position in EV manufacturing and consumer electronics production, Japan's longstanding expertise in precision energy storage components, and South Korea's rapidly expanding semiconductor and electronics industries.

The U.S. supercapacitor market demonstrates robust growth momentum driven by the convergence of clean energy investment, accelerating EV adoption, and advanced materials innovation. According to the US Department of Energy, California had approximately 1,256,646 and Florida 254,878 light-duty electric vehicle registrations in 2023, reflecting sustained policy-driven and consumer-led momentum that is directly reinforcing supercapacitor adoption across transportation, grid storage, and industrial applications throughout the country.

Europe's supercapacitor market is advancing steadily, supported by the European Union's ambitious carbon neutrality targets and the region's significant concentration of automotive and industrial manufacturing capacity. The United Kingdom, the second-largest car market in Europe accounted for 30% of global electric car sales in 2023 according to the IEA, creating substantial demand for supercapacitor-enhanced EV power systems.

Latin America's supercapacitor market is experiencing emerging growth, supported by the region's transition toward renewable energy and early-stage electric vehicle ecosystem development. The Middle East and Africa supercapacitor market is in early-stage development but growing at an increasing pace, as Gulf Cooperation Council nations accelerate portfolio diversification toward solar and renewable energy sources.

Competitive Landscape

The global supercapacitor market is characterized by active competitive dynamics, with established players focusing heavily on research and development to advance energy density, power density, and production economics. The competitive landscape in the supercapacitor market reflects a balance between incremental performance enhancement by established players and disruptive material innovations emerging from research-intensive technology companies globally.

|

Company |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Cap-XX Limited |

CAP-XX |

Challenger – Compact/IoT Specialist |

Thin, prismatic supercapacitor design for consumer electronics and IoT; strategic IP partnerships (SCHURTER AG, 2025); innovation in space-constrained OEM applications |

|

Cornell-Dubilier |

Cornell Dubilier |

Emerging Leader – Industrial/Energy |

Application-specific capacitor solutions for transportation, power management, and grid energy storage; strong R&D pipeline targeting industrial and heavy-duty deployments |

|

Eaton Corporation |

Eaton Supercapacitors |

Global Leader – Power Management |

Integration of supercapacitors into smart grids, UPS systems, and hybrid EVs; broad product distribution (125,000+ products); decarbonization and digitalization focus |

|

Fastcap Ultracapacitors, LLC. (a Nanoramic, Inc.’s subsidiary) |

FastCAP |

Specialist – High-Temperature/Industrial |

High-reliability, compact supercapacitors for extreme environments; focus on oil & gas, aerospace, and defense; vertical integration for rugged application performance |

|

Ioxus |

iMOD / iCAP / THiNCAP |

Established – Industrial/Transportation |

Modular, high-power ultracapacitor systems for rugged transportation and industrial use; vertical integration approach; cell balancing innovation for reliable energy delivery |

|

KYOCERA AVX Components Corporation |

AVX SCC Series |

Established – Automotive/Electronics |

First automotive-grade supercapacitors (AEC-Q200 compliant); diversified components portfolio; focus on miniaturized, surface-mount designs for automotive and industrial OEMs |

|

Maxwell Technologies |

Maxwell Ultracapacitors |

Global Leader – Automotive/Grid |

Largest portfolio of high-performance ultracapacitor modules; deep system integration expertise across automotive, grid stabilization, and renewable energy |

|

Nippon Chemi-Con Corporation |

NCC Supercapacitors |

Leader – Japan/Asia Pacific |

Premium passive components heritage; strong presence in Japanese automotive and industrial electronics; reliability-led positioning with mature manufacturing and quality standards |

|

Skeleton Technologies |

SuperBattery / GrapheneGPU |

Innovator – Graphene/High Power Density |

Proprietary curved graphene electrode technology; EUR 600M SuperBattery hub in France; GrapheneGPU launched for AI data center peak-shaving (June 2025); European leadership |

|

TDK Corporation |

TDK Supercapacitors |

Leader – Advanced Materials/Grid |

Advanced materials and integrated system solutions; grid modernization and EV mobility focus; leverages global electronics manufacturing scale for consistent innovation |

The companies covered in the report includes Cap-XX, Cornell-Dubilier, Eaton Corporation, Fastcap Ultracapacitors, LLC, Ioxus, KYOCERA AVX Components Corporation, Maxwell Technologies, Nippon Chemi-Con Corporation, Skeleton Technologies, TDK Corporation, etc.

Key Company Profiles

Maxwell Technologies

Maxwell Technologies, now operating under Clarios following its November 2025 acquisition, is a global pioneer in ultracapacitor technology. Founded in 1965 in San Diego, California, Maxwell holds one of the industry’s largest patent portfolios in dry electrode manufacturing.

- Product Portfolio: Ultracapacitor Cells & Modules: High-capacitance cylindrical cells (up to 3,400 F) and pre-assembled 16V–125V modular systems for EV, bus, and grid applications.

- Recent Developments: In November 2025, Clarios completed the acquisition of Maxwell Technologies, integrating Maxwell’s ultracapacitor technology into Clarios’s global automotive and energy storage portfolio, expected to accelerate hybrid energy storage system development across automotive and industrial markets.

Eaton Corporation

Eaton Corporation is a diversified global power management company headquartered in Dublin, Ireland. Its supercapacitor lines, part of the electrical components and eMobility divisions, offer hybrid energy storage solutions delivering up to 10 times higher energy density than standard supercapacitors.

- Product Portfolio: HS/HSL Hybrid Supercapacitor Cells: Cylindrical cells at 3.8 V (30–220 F) with up to 10x higher energy density than standard supercapacitors; HSL variant optimized for −25°C, HS for +85°C environments.

- Recent Developments: In October 2025, Eaton introduced an 800 VDC architecture for AI data centers that uses supercapacitors as fast-cycle backup buffers to manage power fluctuations from GPU clusters, reinforcing its role in next-generation data center energy infrastructure.

Skeleton Technologies

Skeleton Technologies is a European leader in high-power, fast-charging energy storage, headquartered in Estonia with manufacturing in Germany and Finland. Its products are built on patented Curved Graphene electrode material, delivering the highest commercially available power density without reliance on critical raw materials.

- Product Portfolio: Curved Graphene Supercapacitor Cells; Flagship high-power-density cells with 1M+ cycle life, sub-90-second charging, and extreme temperature resilience; produced at up to 12 million units per year at the Leipzig SuperFactory.

- Recent Developments: In November 2025, Skeleton officially opened its €220 million SuperFactory in Markranstädt, Leipzig, with 12 million cells per year capacity. The facility immediately began delivering to Siemens, GE, and Hitachi Energy for European grids and to US hyperscalers for AI infrastructure.

TDK Corporation

TDK Corporation is a global Japanese electronics and components manufacturer founded in 1935, headquartered in Tokyo, Japan, with operations across 250+ locations in 30+ countries. Its pouch-type EDLC supercapacitors leverage proprietary thin-film manufacturing to achieve thicknesses as low as 0.45 mm, making TDK a preferred supplier for miniaturized IoT, wearables, smart meters, and automotive electronics applications.

- Product Portfolio: IoT & Smart Meter EDLCs; Compact battery-assist EDLC components for wireless smart meters, energy harvesting sensors, and industrial IoT nodes; extend battery life and support wireless transmission bursts.

- Recent Developments: In March 2025, TDK launched its edgeRX predictive maintenance sensor platform integrating TDK sensors with AI and edge computing, relying on EDLC energy management for high-current wireless transmission bursts in manufacturing and logistics monitoring.

Nippon Chemi-Con Corporation

Nippon Chemi-Con Corporation is a Japanese electronic components manufacturer founded in 1931, headquartered in Tokyo, Japan, and recognized as the world leader in aluminum electrolytic capacitors. Its proprietary DLCAP™ supercapacitor product family uses a safe propylene carbonate-based electrolyte (eliminating toxic acetonitrile), and the DKA Series was the world’s first supercapacitor adopted in an automotive regenerative braking energy recovery system, initially by Mazda Motor Corporation.

Product Portfolio:

- DLCAP™ DKA Series: Automotive-grade radial lead-type EDLC with industry-leading low internal resistance, −40°C to +70°C operating range, and safe PC-based electrolyte; used in vehicle regenerative braking and start-stop systems.

- DLCAP™ DKG Series: Enhanced radial lead-type EDLC with upgraded 2.7 V rated voltage and up to 20% size reduction vs. prior generation (launched April 2024); optimized for automotive backup power and compact industrial equipment.

Market Concentration Analysis

The global supercapacitor market is structurally concentrated at the technology and manufacturing tier, with a limited number of vertically integrated players from the United States, Japan, South Korea, and Europe commanding the majority of global cell and module production. Competition is driven primarily by electrode material innovation, manufacturing scale, product performance, and application-specific customization.

In mature segments such as automotive regenerative braking, grid frequency regulation, and industrial UPS systems, market concentration is higher. Established manufacturers with proven OEM qualifications and long-cycle validation data hold durable competitive advantages, reinforced by multi-year supply agreements that create meaningful barriers to entry for new participants.

In emerging segments including AI data center power buffering, IoT energy harvesting, and flexible electronics, the landscape is more dynamic, with startups and mid-tier players challenging incumbents through graphene composite and conducting polymer electrode platforms. Regional manufacturers in India, Southeast Asia, and Latin America are also gaining ground by offering cost-competitive solutions tailored to local infrastructure requirements.

Investment & Growth Opportunities

Fastest Growing Segments

Hybrid supercapacitor-battery systems, graphene-based advanced electrode products, and miniaturized micro-supercapacitors for IoT and wearable devices represent the highest-growth investment vectors through 2034.

Emerging Market Expansion

Asia Pacific's sustained CAGR leadership represents the most compelling regional investment opportunity. China's EV ecosystem, India's renewable energy microgrid expansion, and South Korea's advanced battery-supercapacitor hybrid R&D programs are collectively generating large-scale procurement demand.

Technology and Innovation Investment Trends

- Graphene electrode material manufacturers and curved carbon nanostructure producers are experiencing strong B2B demand growth, as premium supercapacitor OEMs transition away from commodity activated-carbon electrodes toward high-performance graphene platforms commanding significantly higher price points and margins across automotive and grid-scale applications.

- Hybrid supercapacitor-battery system integrators and AI datacenter power infrastructure suppliers are attracting significant venture and strategic capital. Flex-Musashi's datacenter partnership and Skeleton Technologies' EUR 600 million SuperBattery hub exemplify the scale of investment flowing into integrated energy storage platforms combining supercapacitor and battery chemistries.

- Micro-supercapacitor developers targeting IoT, wearable electronics, and medical device segments are capturing consumer and healthcare technology investment. Start-ups focused on biodegradable polymer-based supercapacitors attracted over USD 75 million in early-stage funding, reflecting strong investor confidence in sustainable, application-specific supercapacitor product innovation through 2034.

Future Market Outlook (2026-2034)

The global supercapacitor market is poised for sustained, application-driven growth through 2034, anchored by the structural electrification of transportation, accelerating deployment of renewable energy infrastructure, and the rapid emergence of AI data center power management as a high-growth demand vertical. Rising regulatory pressure on carbon emissions across major economies, combined with the increasing commercial viability of hybrid energy storage architectures, is progressively expanding the addressable market for supercapacitors beyond traditional niche applications into mainstream industrial and consumer-facing segments.

Energy density improvement will be the primary technology battleground. Manufacturers that successfully close the gap between supercapacitor power performance and battery energy density, through advances in graphene composite electrodes, pseudocapacitive materials, and hybrid lithium-ion capacitor architectures, will unlock the highest-value application opportunities of the next decade, including primary energy storage in light electric vehicles and long-duration grid buffering. The emergence of supercapacitors as essential components in AI infrastructure, enabling GPU clusters to operate at full efficiency while reducing grid connection requirements by up to half, represents a structurally new and rapidly scaling demand category that was largely absent from market forecasts as recently as 2023.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 150 industry participants in 2024–2025, comprising bubble tea franchise operators, ingredient and equipment suppliers, retail buyers, food service distributors, and end consumers across Asia Pacific, North America, Europe, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company press releases, franchise disclosure documents, trade publications (QSR Magazine, Food Business News, Nation's Restaurant News), industry databases (Euromonitor, Mintel), and publicly available market data including government trade statistics and tea industry association reports. Over 250 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up outlet count and average revenue per outlet modeling, combined with top-down consumer expenditure analysis incorporating tea consumption data, café culture penetration rates, and social media trend analytics.

Supercapacitor Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Electric Double-Layered Capacitors, Pseudocapacitors, Hybrid Capacitors |

| Module Types Covered | Less than 25V, 25-100V, More than 100V |

| Material Types Covered | Carbon and Metal Oxide, Conducting Polymer, Composite Materials |

| End Use Industries Covered | Automotive and Transportation, Consumer Electronics, Power and Energy, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Cap-XX Limited, Cornell-Dubilier, Eaton Corporation, Fastcap Ultracapacitors LLC. (a Nanoramic Inc.’s subsidiary), Ioxus, KYOCERA AVX Components Corporation, Maxwell Technologies, Nippon Chemi-Con Corporation, Skeleton Technologies, TDK Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the supercapacitor market from 2020-2034.

- The supercapacitor market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the supercapacitor industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The supercapacitor market was valued at USD 7.63 Billion in 2025.

The supercapacitor market is projected to exhibit a CAGR of 18.11% during 2026-2034, reaching a value of USD 34.13 Billion by 2034.

The global supercapacitor market is driven by rising electric vehicle adoption, expanding renewable energy infrastructure, and surging consumer electronics demand. The proliferation of IoT devices, industrial automation advancement, and continuous innovation in electrode materials, including graphene and transition metal oxide composites, are collectively accelerating market growth and broadening commercial applications across diverse industries globally.

Asia Pacific currently dominates the supercapacitor market, accounting for a share of 44.8%. The region's leadership reflects its strong positions in electric vehicle manufacturing, consumer electronics production, and renewable energy deployment, particularly across China, Japan, South Korea, and India, supported by favorable government policy environments.

Some of the major players in the supercapacitor market include Cap-XX Limited, Cornell-Dubilier, Eaton Corporation, Fastcap Ultracapacitors LLC (a Nanoramic, Inc.’s subsidiary), Ioxus, KYOCERA AVX Components Corporation, Maxwell Technologies, Nippon Chemi-Con Corporation, Skeleton Technologies, TDK Corporation, etc.

The supercapacitor market faces challenges including lower energy density compared to lithium-ion batteries, high production costs associated with advanced materials such as graphene, and integration complexities in hybrid energy storage systems, which limit widespread adoption across certain applications.

Emerging opportunities include increasing adoption in electric vehicles for regenerative braking systems, growing use in renewable energy storage and grid stabilization, expansion in consumer electronics and IoT devices, and advancements in material science enabling higher energy density and improved performance characteristics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)