Superalloys Market Size, Share, Trends and Forecast by Base Material, Application, and Region, 2026-2034

Superalloys Market Size and Share:

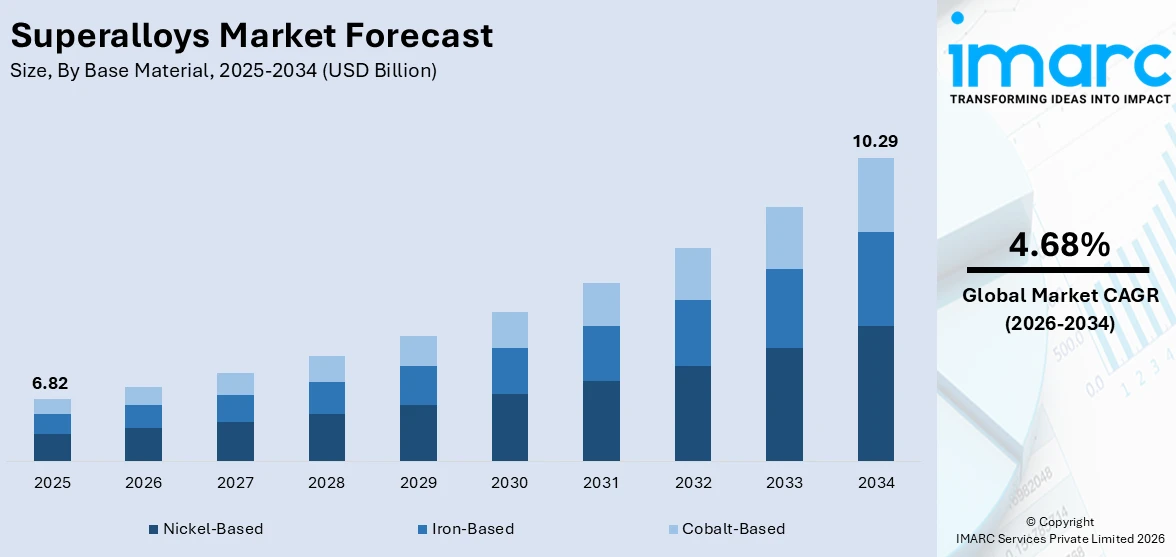

The global superalloys market size was valued at USD 6.82 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 10.29 Billion by 2034, exhibiting a CAGR of 4.68% from 2026-2034. North America currently dominates the market, holding a market share of 34% in 2025. The region benefits from a highly advanced aerospace and defense industrial base, substantial government investment in next-generation aircraft programs, and a deeply integrated specialty materials supply chain, all of which expand the superalloys market share.

The global superalloys market is propelled by a convergence of powerful structural demand forces spanning multiple high-performance industries. The growing utilization of superalloys in aerospace applications, particularly in the hot sections of commercial and military jet engines, stands as the foremost catalyst for superalloys market growth. These advanced engineered materials offer an unrivalled combination of high-temperature mechanical strength, thermal stability, oxidation resistance, and creep performance, making them absolutely indispensable for turbine blades, combustors, vanes, and discs operating under the most extreme thermal and mechanical loads. The rapid global expansion of civil aviation, driven by sustained passenger traffic growth and widespread airline fleet modernization, is generating consistent multi-year demand for advanced engine alloys across all major aircraft programs. Beyond aerospace, the deployment of high-efficiency gas turbines in power generation, growing oil and gas sector applications, and intensifying investment in military aviation programs further reinforce the favorable superalloys market outlook.

The United States has emerged as a major region in the market owing to many factors. The country hosts a world-class aerospace and defense manufacturing ecosystem comprising leading aircraft OEMs, engine manufacturers, and specialty materials producers operating across a highly integrated industrial supply chain. The sustained government commitment to defense modernization, including advanced military aircraft procurement programs spanning multirole fighters, strategic bombers, and next-generation platforms, generates consistent demand for high-performance superalloys capable of withstanding extreme operational conditions. The energy sector's ongoing investment in combined-cycle power generation infrastructure and advanced industrial gas turbine systems further reinforces domestic market demand. The U.S. Department of Energy funded a USD 12.5 million research initiative starting in 2024 to advance materials for extreme environments, demonstrating strong institutional support for superalloy innovation that underpins the nation's long-term superalloys market forecast trajectory.

To get more information on this market Request Sample

Superalloys Market Trends:

Surging Demand from High-Temperature Industrial Applications

The accelerating necessity for materials capable of enduring extreme thermal and mechanical environments is one of the most consequential forces shaping the global superalloys landscape. Across the aerospace and power generation industries, jet engines and industrial gas turbines routinely operate at temperatures that far exceed the melting points of conventional metallic alloys, rendering superalloys virtually irreplaceable for critical rotating and stationary components. These advanced materials deliver unmatched combinations of mechanical strength at elevated temperatures, oxidation and corrosion resistance, and dimensional stability under thermal cycling, qualities that no alternative class of engineering materials can fully replicate. The relentless industry-wide drive toward greater thermodynamic efficiency has incentivized the adoption of higher turbine inlet temperatures, which in turn place increasingly stringent demands on structural alloys. Global defense spending surpassed USD 2.7 trillion in 2024, driving heightened procurement of next-generation military aircraft and naval propulsion systems that rely extensively on advanced superalloys for their propulsion and structural components. This combination of commercial and defense-driven demand ensures that high-temperature industrial application requirements will continue to powerfully reinforce Superalloys market growth over the coming decade.

Advances in Material Science Expanding Market Scope

Groundbreaking developments in material science and metallurgy have profoundly broadened both the performance envelope and the application scope of superalloys, transforming them from primarily aerospace-centric materials into indispensable components across a widening spectrum of industries. Decades of meticulous research into alloy composition, microstructural design, and thermomechanical processing have yielded materials exhibiting extraordinary levels of creep resistance, fatigue tolerance, and resistance to oxidation and hot corrosion in environments that would rapidly degrade conventional engineering metals. The emergence of computational materials design tools has significantly accelerated the discovery of new alloy compositions with predictively optimized property profiles, compressing development timelines and enabling more targeted innovation. Each breakthrough in alloy development not only refines existing applications but also opens entirely new market verticals, creating a positive feedback loop that continually expands the superalloys market trends and application universe. in 2025, Wheels India announced signed a technical assistance agreement with Topy Industries for design, development and production of aluminium alloy wheels.

Integration of Additive Manufacturing in Superalloy Production

The increasing adoption of additive manufacturing technologies within the superalloy production landscape represents one of the most transformative developments reshaping the competitive dynamics of the global market. Traditional superalloy fabrication through investment casting, directional solidification, and single-crystal growth involves complex multi-step processes that generate significant material waste and impose geometric constraints on component design. Additive manufacturing enables the production of intricate internal cooling geometries, lattice structures, and topology-optimized shapes that are physically impossible to achieve through conventional subtractive or formative manufacturing routes, directly translating into superior component performance and longer service life. EOS introduced two new nickel-based superalloys, EOS NickelAlloy IN738 and EOS NickelAlloy K500, commercially available for industrial additive manufacturing systems from December 2024, signaling the rapid maturation of 3D-printing-compatible superalloy material portfolios. The convergence of advanced powder metallurgy feedstock development, laser powder bed fusion, and directed energy deposition techniques is progressively democratizing access to complex superalloy components, enabling faster iteration cycles for engine developers and reducing lead times across the aerospace supply chain, thereby supporting the favorable Superalloys market forecast for the coming years.

Superalloys Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global superalloys market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on base material and application.

Analysis by Base Material:

- Nickel-Based

- Iron-Based

- Cobalt-Based

Nickel-based holds 68% of the market share. Nickel-based superalloys have established themselves as the cornerstone material of the global high-temperature alloys industry, owing to their exceptional and well-documented capacity to maintain structural integrity and mechanical performance at temperatures approaching their incipient melting points. The unique gamma-prime precipitate strengthening mechanism inherent to nickel-based compositions delivers a rare combination of tensile strength, creep resistance, and fatigue tolerance that no alternative alloy system can fully replicate at comparable temperature ranges. These properties are absolutely critical for turbine blades, discs, vanes, and combustor liners in both aero and industrial gas turbine engines, which must operate continuously at extreme temperatures while withstanding complex stress states and corrosive combustion environments. The alloy's natural affinity for refractory element additions further enables the engineering of highly optimized compositions tailored to specific component requirements.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Aerospace

- Commercial and Cargo

- Business

- Military

- Rotary

- Industrial Gas Turbine

- Electrical

- Mechanical

- Automotive

- Oil and Gas

- Industrial

- Others

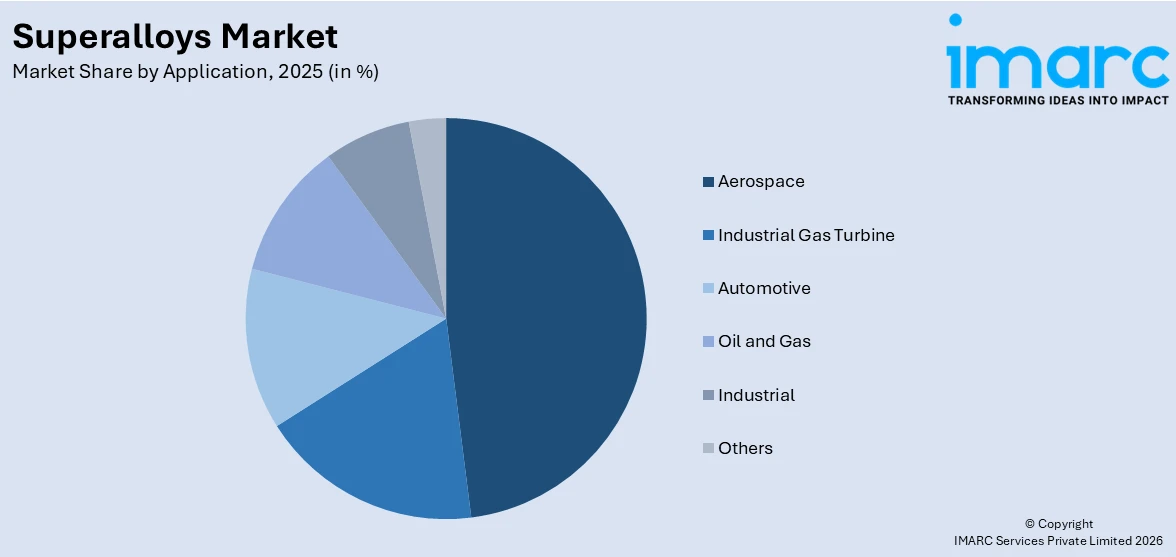

Aerospace leads the market with a share of 48%. The aerospace application segment anchors the global superalloys market, driven by the irreplaceable role of high-performance alloys in virtually every critical propulsion and structural component of modern commercial and military aircraft. Superalloys are indispensable in the hot section of gas turbine engines, encompassing turbine blades, nozzle guide vanes, discs, combustion chambers, and afterburner components, where they must simultaneously withstand peak mechanical loads and temperatures exceeding 1,000°C while resisting oxidation, creep, and thermal fatigue over extended service intervals measured in tens of thousands of flight hours. The relentless competitive pressure among aircraft manufacturers and engine OEMs to achieve higher thrust-to-weight ratios, lower specific fuel consumption, and reduced lifecycle emissions has consistently driven investment in advanced alloy development and manufacturing technology. The substantial allocations for military aircraft procurement and aerospace capability enhancement programs is reflecting the powerful defense-driven demand component that further underpins the aerospace segment's dominant position in the global superalloys market.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 34% of the share, enjoys the leading position in the market. North America's supremacy in the global superalloys market is underpinned by an unparalleled concentration of aerospace and defense manufacturing capabilities, anchored by the world's most powerful aerospace industrial ecosystem encompassing aircraft developers, engine manufacturers, and precision component producers. The region's commanding position reflects decades of sustained investment in advanced materials research, manufacturing technology, and workforce development across the entire specialty alloys value chain. The United States drives the vast majority of North American demand, supported by extensive commercial aircraft production programs, a large and technologically advanced military aviation fleet, and a robust network of maintenance, repair, and overhaul facilities requiring premium alloy replacement components. Canada contributes meaningfully through its established aerospace manufacturing sector and world-class research institutions advancing novel alloy processing techniques. The U.S. Air Force requested USD 24.8 billion for aircraft procurement in the fiscal year 2026 budget proposal, illustrating the sustained government-driven demand for advanced aerospace platforms that reinforces North America's structural leadership in superalloy consumption.

Key Regional Takeaways:

United States Superalloys Market Analysis

The United States stands as the pre-eminent national market for superalloys globally, supported by the world's most expansive aerospace and defense industrial complex comprising multiple Tier 1 engine manufacturers, a large fleet of advanced military aircraft, and a prolific commercial aviation delivery pipeline. The country's unrivalled aerospace manufacturing infrastructure, spanning large-scale investment casting facilities, precision forging operations, and vacuum arc remelting plants, positions it as both the largest consumer and a leading producer of high-performance alloy materials. Government policies promoting domestic defense manufacturing and supply chain resilience have further incentivized substantial capital investment in specialty alloy production capacity. The energy sector's accelerating shift toward cleaner power generation technologies, including high-efficiency combined-cycle gas turbine systems, is opening additional demand channels for advanced superalloys beyond the traditional aerospace end market. In 2025, Working alongside Stoke Space in Kent, Washington, USA, QuesTek Innovations LLC in Evanston, Illinois, has effectively created a new nickel-based superalloy intended for Additive Manufacturing and extreme-pressure, high-temperature oxygen settings. The aim was to create high-efficiency, completely reusable launch systems that are more affordable and capable of more frequent launches.

Europe Superalloys Market Analysis

Europe represents one of the most technologically sophisticated and strategically important regional markets in the global superalloys landscape, anchored by a world-class aerospace manufacturing sector encompassing leading commercial aircraft developers, aero-engine manufacturers, and an extensive network of precision component suppliers concentrated across Germany, France, the United Kingdom, and Italy. The region's aerospace OEMs maintain some of the industry's most demanding superalloy specifications, continuously driving alloy developers and material producers toward higher performance standards. Military aviation modernization programs, including next-generation combat aircraft platforms and allied defense cooperation initiatives, are generating significant incremental demand for specialized high-performance alloys. The industrial gas turbine market for power generation also drives sustained demand for high-quality superalloy components across Europe's energy sector. The Superalloys market trends in Europe continue to reflect a strong innovation orientation.

Asia-Pacific Superalloys Market Analysis

Asia-Pacific represents the fastest-growing regional market for superalloys, driven by rapidly expanding aerospace manufacturing capabilities, surging civil aviation demand, and ambitious government-backed defense modernization programs across multiple major economies. China's substantial and sustained investment in indigenous commercial and military aviation development, including advanced fighter aircraft and narrow-body commercial jet programs, has generated powerful demand for high-performance alloys and catalyzed the development of a domestic superalloy production industry. India's government-sponsored aerospace programs, including indigenous jet engine development and military procurement, are contributing meaningfully to regional demand growth. In 2025, The Shanghai Futures Exchange (SHFE) plans to join China's recycled metal futures market by launching futures and options for cast aluminium alloy. The action is seen as a long-term strategic effort intended to enhance the global market by facilitating access to China’s cast aluminum alloy futures and options. China is the leading producer and consumer of cast aluminium alloy globally, boasting an annual production capacity of approximately 13 million tonnes. The superalloys market forecast for Asia-Pacific remains exceptionally favorable across the medium and long term.

Latin America Superalloys Market Analysis

Latin America represents an emerging growth frontier for the superalloys market, underpinned by expanding civil aviation fleets, growing energy infrastructure investment, and developing industrial manufacturing capabilities across the region's largest economies. Brazil anchors the regional market, with its internationally competitive aerospace manufacturing industry and a robust commercial aviation sector driving sustained demand for advanced engine materials. Mexico's expanding automotive and energy manufacturing base is generating incremental demand for iron-based and nickel-based alloys in specialized high-temperature industrial applications across the country.

Middle East and Africa Superalloys Market Analysis

The Middle East and Africa superalloys market is gaining momentum, supported by rapid expansion of aviation infrastructure, major oil and gas sector investment, and intensifying defense modernization efforts across several key economies. The Gulf Cooperation Council countries, particularly Saudi Arabia and the UAE, are dramatically expanding their aviation sectors as part of broader economic diversification initiatives, fueling demand for advanced alloy components in aircraft engines and gas turbines. Saudi Arabia's General Authority of Civil Aviation is overseeing the development of King Salman International Airport in Riyadh, designed to serve 120 million passengers annually upon completion, reflecting the region's significant long-term aviation growth ambitions. The oil and gas sector's ongoing demand for high-performance materials in drilling and processing equipment provides an additional structural demand foundation for superalloys across the region.

Competitive Landscape:

The global superalloys market is characterized by a concentrated competitive structure dominated by a select group of highly specialized international materials producers with deep expertise in advanced alloy metallurgy, precision manufacturing, and aerospace-grade quality systems. Leading market participants are intensifying investment in research and development to develop next-generation alloy compositions delivering superior high-temperature performance, enhanced oxidation resistance, and improved manufacturability for additive manufacturing platforms. Companies are actively pursuing strategic partnerships and long-term supply agreements with major aerospace OEMs and engine manufacturers to secure multi-year revenue visibility and deepen their integration into critical supply chains. Sustainability initiatives, including the development of superalloy recycling programs and circular economy supply chain models, are emerging as important competitive differentiators as aerospace OEMs and industrial customers apply increasing scrutiny to the environmental credentials of their materials suppliers.

The report provides a comprehensive analysis of the competitive landscape in the superalloys market with detailed profiles of all major companies, including:

- Allegheny Technologies Inc

- AMG Superalloys

- Aperam S.A.

- Cannon-Muskegon Corporation

- Carpenter Technology Corporation

- Doncasters Group

- Haynes International Inc

- IHI Corporation

- IMET Alloys

- Mishra Dhatu Nigam Limited

- Special Metals Corporation

- Western Australian Specialty Alloys (Precision Castparts Corp.)

Latest News and Developments:

- October 2025: Defence Minister Rajnath Singh inaugurated a Titanium and Superalloy Materials Plant at PTC Industries' Strategic Materials Technology Complex in Lucknow, emphasizing that India needs to manufacture rare and essential materials for defence and aerospace to protect its technological independence and establish itself as a technology innovator.

- October 2025: PTC Industries Limited, via its subsidiary Aerolloy Technologies Limited, opened an advanced Titanium & Superalloys Materials Plant in the U.P. Defence Industrial Corridor, Lucknow. Defence Minister Rajnath Singh and UP Chief Minister Yogi Adityanath were present at the Lokarpan Ceremony. The facility intends to produce titanium and superalloy materials essential for defence, aerospace, and industrial sectors, matching India's self-reliance initiative. This advancement aims to decrease reliance on imports and enhance local production abilities in key materials.

Superalloys Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Base Materials Covered | Nickel-Based, Iron-Based, Cobalt-Based |

| Applications Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Allegheny Technologies Inc, AMG Superalloys, Aperam S.A., Cannon-Muskegon Corporation, Carpenter Technology Corporation, Doncasters Group, Haynes International Inc, IHI Corporation, IMET Alloys, Mishra Dhatu Nigam Limited, Special Metals Corporation, Western Australian Specialty Alloys (Precision Castparts Corp.), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the superalloys market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global superalloys market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the superalloys industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The superalloys market was valued at USD 6.82 Billion in 2025.

The superalloys market is projected to exhibit a CAGR of 4.68% during 2026-2034, reaching a value of USD 10.29 Billion by 2034.

Key drivers of the Superalloys market include rising demand from aerospace applications particularly for jet engine components, increasing global military expenditure requiring advanced high-performance materials, the growing deployment of industrial gas turbines in power generation, expanding research and development activity in advanced material science, and the broadening adoption of additive manufacturing for complex superalloy component production.

North America currently dominates the superalloys market, accounting for a share of 34% in 2025. The region benefits from a highly concentrated aerospace and defense manufacturing base, sustained government investment in military aircraft programs, and robust commercial aviation production activity that collectively drive the highest regional superalloy consumption globally.

Some of the major players in the superalloys market include Allegheny Technologies Inc, AMG Superalloys, Aperam S.A., Cannon-Muskegon Corporation, Carpenter Technology Corporation, Doncasters Group, Haynes International Inc, IHI Corporation, IMET Alloys, Mishra Dhatu Nigam Limited, Special Metals Corporation, Western Australian Specialty Alloys (Precision Castparts Corp.), etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)