Structural Core Materials Market Size, Share, Trends and Forecast by Product Material, Skin Material, End Use, and Region, 2025-2033

Structural Core Materials Market Size and Trends:

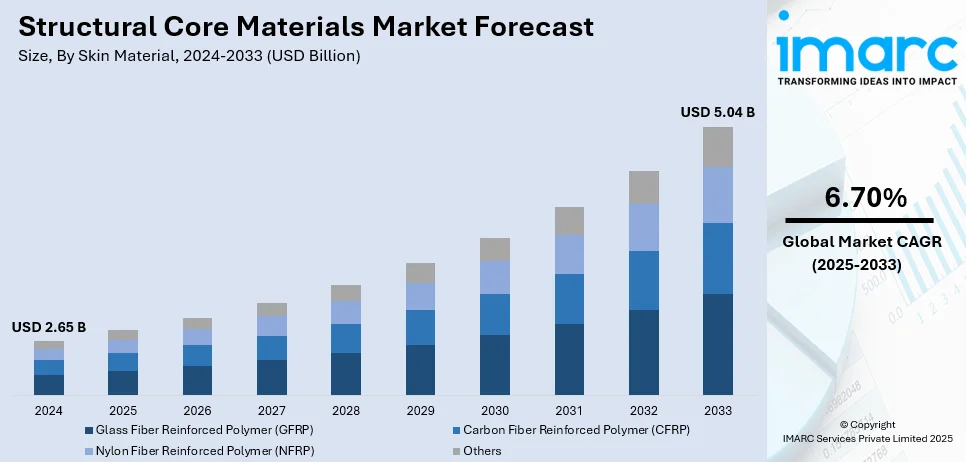

The global structural core materials market size was valued at USD 2.65 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 5.04 Billion by 2033, exhibiting a CAGR of 6.70% from 2025-2033. North America currently dominates the market, holding a market share of over 35.6% in 2024. These are driven by robust demand in aerospace, automotive, and wind energy sectors, alongside advancements in manufacturing technologies and sustainability-focused innovations.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 2.65 Billion |

| Market Forecast in 2033 | USD 5.04 Billion |

| Market Growth Rate (2025-2033) | 6.70% |

The global structural core materials market growth is propelled by escalating demand across industries like aerospace, wind energy, automotive, and construction. The need in aerospace is lightweight materials for improved fuel efficiency and emission reduction that drives the adoption of such material. In wind energy applications, strength-to-weight ratio enables making longer and more efficient blades. Automotive applications of these materials have grown to incorporate structural core materials for reduced weight and enhanced crash protection to promote the move to electric vehicles. Applications in construction have expanded due to the growing importance of durability and sustainability of composite technologies. Additionally, rising environmental awareness has spurred the development of eco-friendly core materials, aligning with global sustainability goals. Increasing investments in research and development for innovative materials further support market growth. For instance, In November 2024, 3A Composites Core Materials launched the Engicore business line, expanding Airex and Baltek brands with custom-shaped core solutions optimized for specific manufacturing processes and sustainability goals. Furthermore, these combined factors ensure robust demand and continued expansion of the structural core materials market globally.

The structural core materials market share in the United States is driven by strong demand across key industries such as wind energy, automotive, and aerospace. The aerospace sector plays a pivotal role, leveraging lightweight materials like honeycomb and foam cores to decrease emission and augment fuel efficiency in aircraft production. The automotive sector observes an amplified adoption of electric vehicles (EVs) that call for lighter materials to enhance the efficiency of the battery and mileage range. In the wind energy sector, structural core materials are also intensely used to make turbine blades more energy-efficient and durable. Besides these, there is acceleration in the manufacturing of the structural core materials market by advances in technologies such as automation and 3D printing. Growing investments in infrastructure and construction activities also help fuel the market growth as light, high-strength materials are an integral part of modern designs. Sustainability objectives and environmental regulations are further driving the innovation of eco-friendly core materials, which propels market growth.

Structural Core Materials Market Trends:

Growing Demand in Aerospace and Automotive Industries

The aerospace and automotive sectors are driving the demand for structural core materials due to their critical need for high strength and lightweight components. In aerospace, materials such as honeycomb cores are essential for reducing weight in aircraft interiors and fuselage while ensuring structural integrity and fuel efficiency. The accelerated production of commercial and military aircraft further boosts the demand for these materials. For instance, in October 2024, Hexcel outlined its strategy for high-rate aerospace composites, focusing on diverse material systems and processing methods to meet the growing demand for next-gen single-aisle and AAM aircraft production. Furthermore, the automotive industry, particularly the electric vehicle (EV) segment, relies on structural core materials to enhance vehicle range and battery performance. Lightweight materials are crucial for meeting stringent fuel efficiency and emission standards in both traditional and EV markets. Advanced manufacturing technologies, including automated production lines and 3D printing, enable the customization of core materials to meet specific aerospace and automotive requirements, driving their adoption and expanding their applications in these high-growth sectors.

Rapid Technological Advancements

Technological advancements in composite manufacturing are revolutionizing the market for structural core materials. Automated fiber placement, vacuum infusion, and 3D printing are improving the process of manufacturing by reducing the cost, waste, and enhancing material performance. Such advanced methods create lightweight, long-lasting, and high-strength materials that are crucial for many applications in wind energy and aerospace. Advances in resin systems and reinforcement technologies also bring superior core material performance for extreme operating conditions. Smart integration of such technologies, that include sensors embedded in resins, has opened vast possibilities in monitoring and predictive maintenance activities, mainly in high-performance applications. The boosting adoption of these technologies in industries is likely to lead to amplified demand for advanced structural core materials, creating opportunities across sectors, such as automotive, marine, and renewable energy.

Focus on Sustainability and Eco-Friendly Solutions

The structural core materials market is highly focused on sustainability as industries prioritize reducing their environmental footprint. Manufacturers are investing in the development of biodegradable and recyclable products to meet sustainability initiatives and comply with stringent regulations. For example, In April 2023, Diab launched sustainable core materials, including Divinycell PET, PL, and PR, made from recycled PET. These materials offer low resin uptake, high stability, and enhanced thermal insulation for eco-friendly applications. Moreover, lightweight materials also contribute to energy efficiency in aerospace, automotive, and construction industries, further driving their adoption. The encouragement for sustainable solutions has led to innovations in manufacturing processes, including the use of bio-based resins and renewable fibers. Bolstered R&D funding supports the creation of ecofriendly materials that reducing environmental affect and maintain performance standards. As sustainability becomes a core consideration for industries, the demand for eco-friendly structural core materials is expected to grow, shaping the market's future trajectory.

Structural Core Materials Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global structural core materials market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on product material, skin material, and end use.

Analysis by Product Material:

- Foam

- Balsa

- Honeycomb

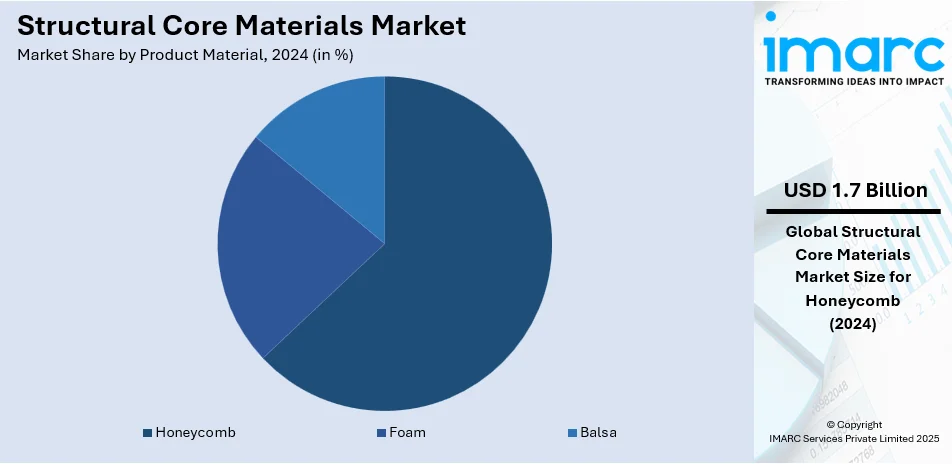

Honeycomb cores dominate the structural core materials market, holding a significant share of 63.5% in 2024. This material has an excellent strength-to-weight ratio and energy absorption. These properties make it very favorable in aerospace, automotive, and marine industries. It is lightweight in nature which reduces fuel consumption and enhances performance with high durability. Honeycomb structures are used in aircraft fuselage and interior parts, automotive panels, and boat hulls. This material, is in high demand and continues to grow with improvements in composite technology, further enhancing its strength and versatility, making it an essential material for high-performance applications.

Analysis by Skin Material:

- Glass Fiber Reinforced Polymer (GFRP)

- Carbon Fiber Reinforced Polymer (CFRP)

- Nylon Fiber Reinforced Polymer (NFRP)

- Others

Carbon fiber reinforced polymer (CFRP) is the leading skin material in the structural core materials market, valued for its exceptional strength, stiffness, and low weight. CFRP has greater benefits in aerospace, automobile, and renewable energy-related applications, where performance, strength, and weight reduction are necessary. It has excellent properties in terms of fatigue and corrosion resistance and high temperature, which makes it favorable for high-performance applications. Its use in commercial aircraft, military aircraft, and electric vehicles is one of the major growth drivers. CFRP’s high strength-to-weight ratio allows for better fuel efficiency and enhanced performance, pushing its use in high-performance components like turbine blades and structural panels.

Analysis by End Use:

- Aerospace

- Automotive

- Wind Energy

- Marine

- Construction

- Others

The aerospace sector represents the largest end-use segment for structural core materials, capturing 38.1% of the market share in 2024. There is a demand for lightweight and strong materials which save on fuel consumption during the aircraft's operation. These are causing an amplifying demand for honeycomb and foam in core material requirements. This factor contributes to why advanced structural core materials have found wide acceptance in aerospace firms in their wings, fuselages, and interiors. Growth in the commercial aviation and military aircraft productions further contributes to the superiority of the aerospace segment over the others in the structural core material market. It is a significant source of expansion for the market.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America holds a significant share of 35.6% in the global structural core materials market, driven by strong demand across aerospace, automotive, and wind energy sectors. As the North America is a prime aerospace manufacturing country, advanced structural materials are widely used to meet performance and fuel efficiency standards. Furthermore, the region is also expected to support the growing production of electric vehicles (EVs) and renewable energy projects. Moreover, technology advancements in manufacturing and acceleration in sustainability initiatives add up to the reason that North America holds such a strong market position as a key region in the structural core materials industry.

Key Regional Takeaways:

United States Structural Core Materials Market Analysis

The United States is a major market in the global structural core materials market, mainly because of strong demand from the aerospace, automotive, and renewable energy sectors. In the case of the aerospace sector, the demand for structural core materials is escalating with increased usage of lightweight materials for the production of aircraft for improving fuel efficiency and lowering emission levels. Moreover, structural core materials are witnessing rising demand in automotive applications as the production of EVs propels. Sustainability efforts in the U.S. also receive strong emphasis. In fact, investments into more eco-friendly and recyclable materials are boosting constantly. Technological advancements related to manufacturing, including automation and 3D printing, will further spur the expansion of the market and ensure a strong position for the United States in structural core material innovation.

Europe Structural Core Materials Market Analysis

The structural core materials market in Europe is highly impacted by the aerospace and automotive industries. The aircraft industry remains the largest consumer of high-performance lightweight materials. Some of the strongest production centers for these products are found in Germany, France, and the United Kingdom. The automotive industry also takes into consideration the advent of electric vehicles, where it needs lightweight core materials for improved battery performance and, the vehicle. In addition, Europe is focused on sustainability, asthere has been significant investment in R&D to produce eco-friendly materials that meet strict environmental legislations. Renewable energy rises, especially wind turbine, which contributes to the expansion in the market of Europe.

Asia Pacific Structural Core Materials Market Analysis

Asia Pacific leads the structural core materials market, driven by rapid industrialization and growing investments in key sectors, such as aerospace, automotive, and wind energy. China, Japan, and India are at the forefront of market growth, with aerospace and automotive industries increasingly adopting lightweight materials to enhance efficiency and performance. The rise in electric vehicles in the region has added fuel to the fire of durable, lightweight core materials in the automotive industry. The renewable energy sector, especially wind energy, is expanding. This refers to a great deal of high-strength materials is required for turbine blades. The manufacturing technologies and a strong emphasis on sustainability drive this market forward in the region and lead it to continuous growth.

Latin America Structural Core Materials Market Analysis

The Latin America structural core materials market is slowly growing and is mainly driven by the automotive and renewable energy industries. Countries, such as Brazil and Mexico are experiencing growth in the adoption of lightweight materials for automotive manufacturing, especially electric vehicles. The wind energy industry is also advancing in the region, which requires structural core materials for turbine blades. The various areas in the region will observe advancements as industrial growth in the region continues due to sustainable development programs. Attention and efforts on environmentally friendly practices would most likely support market increases to the coming years.

Middle East and Africa Structural Core Materials Market Analysis

The market for structural core materials in the Middle East and Africa is expected to have stable growth, especially from aerospace and construction sectors. Middle East's aerospace sector is expanding, which raises demand for lightweight and tough structural materials for aircraft. Other areas, such as big infrastructural projects and constructions happening in the UAE and Saudi Arabia, require low-cost yet very tough structural material for usage. Renewable energy sector, comprising solar and wind energy projects, is also a rising contributor since such industries demand high-grade materials to ensure greater efficiency and sustainability. Technology and innovation continue to be the ongoing investments of the region that make sure the market evolves further.

Competitive Landscape:

The structural core materials market is highly competitive, with a presence of many established players and innovators. Companies are interested in providing lightweight and high-strength solutions that satisfy the increasing needs of the aerospace, automotive, wind energy, and construction industries. New technologies, like automation and 3D printing enable the manufacturers to optimize the production process and enhance the portfolio of products. Incorporation of greater and constant consideration towards sustainability drives the market as research is profoundly developed towards developing sustainable or 'eco-friendly' recyclable materials. An intensifying concern towards R&D, aiming at improved strength-to-weight ratios, durability, or thermal resistance of the materials is in vogue. Strategic mergers, collaborations, acquisitions are frequently practiced in an aim to establish strong position of a company in a chosen market area. Industry-specific challenges are also addressed by tailored solutions, and strict regulatory standards add to the competition, accelerating market innovation and growth.

The report provides a comprehensive analysis of the competitive landscape in the structural core materials market with detailed profiles of all major companies, including:

- Armacell

- Diab Group

- Euro-Composites

- Evonik Industries AG

- Gurit Services AG

- Schweiter Technologies AG

- The Gill Corporation

Latest News and Developments:

- In September 2024, Armacell launched its innovative ArmaFlex® ECO550 adhesives, designed to improve efficiency, safety, and sustainability in insulation applications. This eco-friendly solution requires only one-third of the quantity of conventional adhesives while maintaining high-quality results. It eliminates solvents, reduces airing times, and complies with environmental certifications such as LEED® and BREEAM®.

- In November 2024, Evonik unveiled its new PA12-based INFINAM® 6013 P and 6014 P powders at Formnext 2024, featuring carbon black for enhanced UV resistance and durability. Additionally, Evonik introduced the HP 3D HR PA12 FR, a halogen-free, flame-retardant polymer with 50% reusability, aiming to enhance cost-effective, sustainable 3D printing in aerospace, automotive, and electronics industries.

Structural Core Materials Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | USD Billion |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Materials Covered | Foam, Balsa, Honeycomb |

| Skin Materials Covered | Glass Fiber Reinforced Polymer (GFRP), Carbon Fiber Reinforced Polymer (CFRP), Nylon Fiber Reinforced Polymer (NFRP), Others |

| End Uses Covered | Aerospace, Automotive, Wind Energy, Marine, Construction, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Armacell, Diab Group, Euro-Composites, Evonik Industries AG, Gurit Services AG, Schweiter Technologies AG, The Gill Corporation., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the structural core materials market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global structural core materials market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the structural core materials industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global structural core materials market was valued at USD 2.65 Billion in 2024.

The market is estimated to reach USD 5.04 Billion by 2033, exhibiting a CAGR of 6.70% from 2025-2033.

The global structural core materials market is driven by rising demand in defense and wind energy sectors, where such materials are vital. Increasing adoption in electric vehicles and advancements in composite technology further fuel growth. The growing focus on sustainability and energy efficiency promotes the use of eco-friendly materials. Additionally, expanding applications in marine and construction industries support market expansion, driven by performance and durability requirements.

North America currently dominates the global structural core materials market. The dominance is driven by a strong aerospace and defense industry, significant growth in the wind energy sector, and increasing demand for lightweight and durable materials in transportation applications.

Some of the major players in the global structural core materials market include Armacell, Diab Group, Euro-Composites, Evonik Industries AG, Gurit Services AG, Schweiter Technologies AG, The Gill Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)