Storage Software Market Size, Share, Trends and Forecast by Software Type, Deployment Type, Organization Size, Vertical, and Region, 2025-2033

Storage Software Market Size and Share:

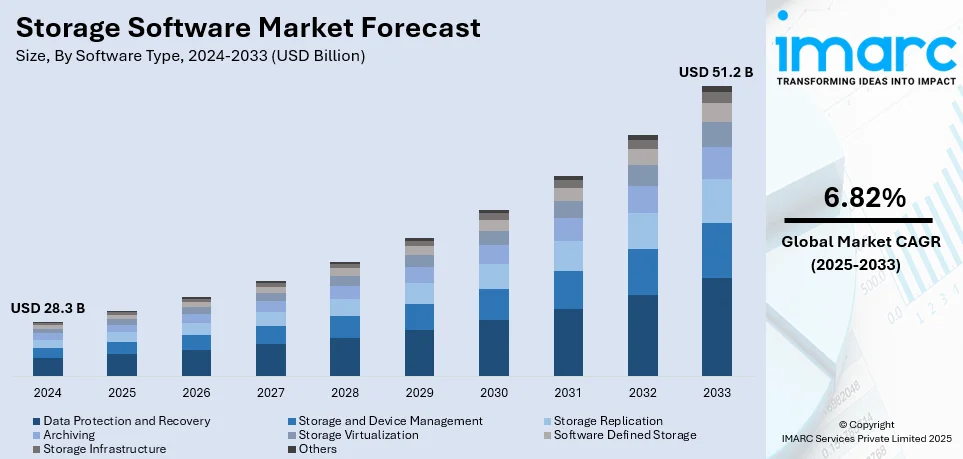

The global storage software market size was valued at USD 28.3 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 51.2 Billion by 2033, exhibiting a CAGR of 6.82% from 2025-2033. North America currently dominates the market, holding a market share of over 37.5% in 2024. The storage software market share is driven by rising data volumes, increasing cloud adoption, AI-driven storage demand, cybersecurity advancements, and strong investments in data center infrastructure, enhancing scalability, security, and enterprise data management solutions.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 28.3 Billion |

|

Market Forecast in 2033

|

USD 51.2 Billion |

| Market Growth Rate (2025-2033) | 6.82% |

A primary growth driver for storage software is data growth within industries, which is fueled by the changes brought about by digital transformation and boosted by cloud computing, Internet of Things (IoT), and big data analytics. With an ever-increasing pace of data production and consumption by organizations, effective data storage solutions have become highly imperative-and this represents a huge growth opportunity for the storage software market. With higher escalation in data volumes, businesses need more storage software that can look after large amounts of data with quicker access to data, integrity in data, and supports the requirement for regulation. The amplified trend towards digitalization has led to a greater dependency on cloud-native storage systems and Software Defined Storage (SDS), which help enhance adaptability, offer cost-effectiveness, and deliver high performance. For instance, in September 2024, IBM introduced the IBM Storage DS8000 (10th Generation) with 99.999999% availability, enhanced cybersecurity, AI-driven data management, and high-speed NVMe and FlashCore Module integration, optimizing performance for IBM Z mainframe workloads. Moreover, as organizations seek to improve operational efficiency and streamline data management, the storage software market will continue to expand globally, meeting the mounting demand for innovative solutions to handle evolving data storage needs.

Accelerating demand for the adoption of data-driven decision making in industries where storage software within the United States is one major driving factor. Through amplified demands, where industries can utilize data to analyze business with analytics, artificial intelligence (AI), and Machine Learning (ML). Heightened adoption of analytics, ML, and AI requires significant and scalable data storage. Many of the tech giants and startups in the U.S. drive the adoption of innovative storage software solutions for supporting growing data requirements from sectors, such as healthcare, finance, and retail. For example, in November 2024, NetApp launched new AFF A-Series and C-Series all-flash storage systems, enhancing performance, scalability, and AI readiness with 2.5X speed, 99% ransomware protection accuracy, and 97% power savings for businesses of all sizes. Additionally, remote work and digital collaboration also fuel demand for cloud storage and secure data management tools. With rising regulatory pressures by HIPAA, CCPA and others, more advanced data storage solutions enable compliance and safety which are being driven by U.S. companies as well. Moreover, the migration of enterprises into hybrid and multi-cloud environments becomes a driving force for the growing demand of high-performance and flexible storage software in the U.S. market.

Storage Software Market Trends:

Cloud Storage Growth

The cloud-based storage solution is a significant trend in the storage software market growth. As an organization starts relying more on digital data than physical data, the need for a readily available, cost-effective storage facility has grown to be severely important. Cloud-based solutions are highly adaptable for managing complex volumes of data without high one-time expenses for infrastructure with on-premises storage. According to the U.S. Department of Commerce, the global cloud computing market is estimated to reach USD 832.1 billion by 2025, with storage services being one of the core drivers of this growth. Such growth is propelled by factors like heightening adoption of cloud computing, the need for disaster recovery, and the growing remote workforce requiring accessible data storage. Key drivers of this rapid growth include the increasing adoption of cloud computing, need for disaster recovery, and the emergence of the remote workforce, which increases the demand for accessible data storage for employees. Additionally, businesses are drawn to cloud storage’s ability to handle big data analytics and backup, while offering a pay-per-use model that reduces long-term capital expenses. This trend is expected to accelerate as more organizations embrace hybrid and multi-cloud environments.

AI and Automation Integration

The integration of AI and ML technologies into the storage software has transformed data management and operational efficiency. With the use of AI, storage solutions can automate some of the core processes, which include data migration, predictive maintenance, and data tiering. AI-driven systems can analyze gigantic datasets in real time, so storage solutions are able to make dynamic resource allocations based on a workload or changed data patterns. This level of automation reduces the need for manual intervention, thus lowering labor costs and human error. With AI-enhanced storage solutions, it is possible to optimize storage space by finding redundant data, thus cost-effectiveness improves. ML models can predict the storage future requirements and, hence, reallocate resources in advance so that business will run at all times without disruptions. With volumes of data continuing to increase, an industrial report predicts that by 2025 AI and automation will be central to managing and storing the projected 175 zettabytes of global data.

Data Security and Compliance

Increasing concerns over data privacy and stringent regulatory frameworks around the world compel the companies who opt for storage software to be on high security and compliance standards. Areas of healthcare, finance, and government are most likely to be targeted with high views due to the nature of their work being highly sensitive. Storage solutions are, thus, expected to incorporate more sophisticated security features into their systems, such as end-to-end encryption, multi-factor authentication, and identity access management. According to data from the Identity Theft Resource Center, the United States witnessed a significant increase in data breaches in 2023, with data compromises reaching a total of 3,205 cases and over 353 million individuals affected. This rise in data breaches shows the importance of advanced data security measures. Storage solutions that offer robust compliance capabilities, like the ability to meet GDPR, HIPAA, and other regulatory standards, are in high demand. As organizations handle larger volumes of personal, financial, and proprietary data, the risk of data breaches also rises. To mitigate these risks, businesses are increasingly adopting software that can protect against unauthorized access, ensure data integrity, and maintain audit trails. This focus on data security and compliance will continue to drive demand for advanced storage software designed to safeguard critical information and reduce potential liabilities.

Storage Software Industry Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the global storage software market report, along with forecasts at the global, regional and country level from 2025-2033. Our report has categorized the market based on software type, deployment type, organization size, and vertical.

Analysis by Software Type:

- Data Protection and Recovery

- Storage and Device Management

- Storage Replication

- Archiving

- Storage Virtualization

- Software Defined Storage

- Storage Infrastructure

- Others

In 2024, Software Defined Storage (SDS) holds a dominant market share of 63.0%. SDS is gaining great mileage because it offers flexibility and cost-effectiveness for managing data in various storage infrastructures. SDS allows businesses to manage and control storage resources efficiently, which in turn offers scalability, agility, and ease of use. Growth in data volumes and the necessity for efficient data management solutions has led to SDS adoption in the healthcare, manufacturing, and retail sectors. The other key advantage of SDS solutions is the integration of advanced software technologies into cloud and hybrid environments, helping businesses transform into digital. Concurrently, more businesses are adopting SDS to cut costs on infrastructure, improve performance, and ensure greater data availability as storage infrastructure catches up with ever-changing business requirements and demands.

Analysis by Deployment Type:

- Cloud-based

- On-premises

Cloud-based storage software solutions have been widely adopted for their scalability, flexibility, and cost-effectiveness. More and more businesses opt for cloud deployment to save infrastructure costs and ease data management. Cloud storage enables on-demand resource scaling and allows for seamless remote access, which is suitable for organizations with varying data requirements.

Organizations that strictly need control over their data and infrastructure prefer to use on-premises storage solutions. Enhanced security and compliance capabilities make this a good solution for sectors like BFSI and healthcare, wherein data privacy and control are imperative. However, on-premises deployment will be more costly and less agile than cloud deployment.

Analysis by Organization Size:

- Small and Medium Enterprises

- Large Enterprises

Storage software solutions are adopted by SMEs in accelerating numbers as they look for cost-effective, scalable options. These businesses typically prefer cloud-based solutions as they provide flexibility without heavy upfront investments. Storage software helps SMEs manage data efficiently, improve operations, and comply with regulatory requirements, which contribute to their digital transformation efforts.

Large enterprises usually prefer a hybrid model of cloud-based and on-premises storage solutions to manage large volumes of data securely and effectively. Such organizations usually require high performance, scalability, and disaster recovery capabilities. They invest in advanced storage systems to maintain business continuity, ensure data integrity, and comply with industry standards.

Analysis by Vertical:

- BFSI

- Healthcare

- Manufacturing

- Retail

- IT and Telecom

- Government

- Others

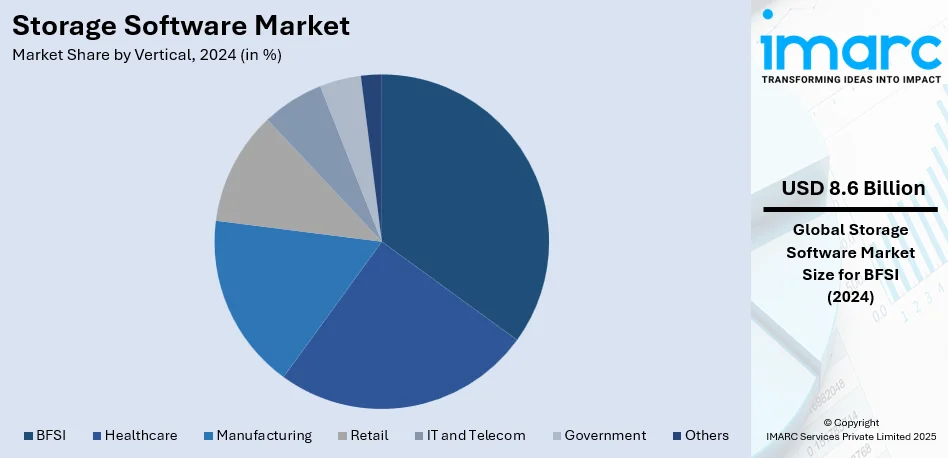

The Banking, Financial Services, and Insurance (BFSI) sector accounts for 30.2% of the storage software market in 2024. This substantial market share is driven primarily by the accelerating need for secure and compliant data storage solutions. Financial institutions manage vast volumes of sensitive data, comprising customer information and transaction records, which require robust storage systems to ensure security, accessibility, and integrity of data. Further, increasing adoption of digital banking services, cloud-based applications, and AI-driven financial tools has indeed caused a surge in data storage requirements across BFSI. As financial services move forward with the era of digital transformation, there is a greater need to move toward scalable, flexible, and secure storage solutions. Additionally, stringent regulations in the BFSI sector in terms of data privacy and storage compliance further boost the demand for advanced storage software solutions tailored to meet industry-specific needs.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America captures 37.5% of the global storage software market share, owing to its strong presence of major technology providers and widespread adoption of advanced storage solutions. The region houses the top tech companies that are always innovating and upgrading the most advanced storage technologies. Industries everywhere - health care, retail, finance, and manufacturing - are digitizing their operations and therefore require highly performing, secure, and scalable storage solutions. Cloud computing popularity in North America along with growing data centers has also helped to grow the market. The regulatory framework of the region, especially in data privacy and security, is another key driver of the need for compliant storage solutions. As enterprises in North America optimize their data storage strategies, demand for software-driven storage management systems continues to increase, which would ensure the region remains a market leader in the global market.

Key Regional Takeaways:

United States Storage Software Market Analysis

The US storage software market is witnessing growth at a rate that is amazing. The growing rate of digital transformation and an increased demand for data across the industries are primarily driving the market. As per our report, the market size of the US digital transformation currently stood at USD 210.4 billion in the year 2024 and is poised to reach USD 1,375.5 billion during 2033, by thereby registering a healthy CAGR of 21.6%. This expansion is largely driven by the widespread adoption of cloud computing, artificial intelligence (AI), machine learning, and data analytics. The healthcare, financial services, and retail industries are particularly active in digitizing operations, fueling the demand for scalable storage solutions to manage vast amounts of data. Furthermore, rising concerns over cybersecurity and stricter data governance regulations are accelerating the need for secure and efficient storage systems. As the U.S. continues to be a global technology hub, both local and international companies are heavily investing in innovative storage solutions to support the nation’s growing digital infrastructure.

Europe Storage Software Market Analysis

The storage software market in Europe is growing because of increased data generation and the ever-increasing need for regulating compliance. Enterprise storage software revenue in the European geographical area reached USD 9.4 billion in 2023, according to the European Commission's 2023 DESI, mainly from Germany, the UK, and France. European companies are more concerned about data security as the data protection laws are more stringent, such as GDPR. Therefore, European companies are implementing newer storage solutions to maintain compliance. Almost 50 percent of European companies are using these hybrid and multi-cloud environments for data management purposes. Tech behemoths SAP and Oracle along with innovative start-ups are helping the cause through cutting-edge backup, archiving, and disaster recovery solutions. The regional market is further being shaped by an emerging focus on data sovereignty and the available options to host locally.

Asia Pacific Storage Software Market Analysis

The storage software market in Asia Pacific is growing at a rapid pace, driven by the rapid digital transformation of various industries. According to industrial reports, Japan has experienced remarkable growth, its related solutions service market for digital transformation has grown from approximately USD 7.69 billion or 1,163.4 billion JPY in 2019 to USD 12.96 billion or 1,961.9 billion JPY in 2022, growing at an astonishing annual rate of 19%. The growth is due to the adoption of cloud computing, 5G technologies, and smart devices, which have increased the demand for data storage solutions. Even countries like China, India, South Korea, and Singapore have adopted digitalization, and respective governments are investing in smart cities, IoT, and data-driven infrastructure. Also, the boom in e-commerce, financial services, and AI-driven solutions boosts the demand for efficient storage software. This also increases strategic partnerships among local and international companies in developing technology, further solidifying Asia Pacific's place as a prime contributor to the global storage software market.

Latin America Storage Software Market Analysis

In Latin America, storage software is on the increase because of the rapid digitalization of industries and increased requirements for data compliance. The overall revenue generated from the enterprise software industry in Latin America is approximately USD 8.47 billion in 2023, industrial reports suggest. Brazil has a budget for IT amounting to USD 12.4 billion in 2023, which is mainly directed towards the provision of cloud and data storage solutions for businesses. As business-houses are being moved to the cloud, the hybrid cloud model is gaining more end-users. More than 45% of organizations in Latin America are using hybrid solutions in their data management. Other factors include increased e-commerce and digital banking popularity, creating demand for safe storage systems. Local players like Totvs and Linx are, therefore, also teaming up with international suppliers such as Microsoft and Amazon Web Services to fortify their local offerings and take advantage of demand in Latin America, a budding market for storage software solutions.

Middle East and Africa Storage Software Market Analysis

In the Middle East and Africa, increasing digitalization and regional investment in data infrastructure propel the market of storage software. According to the official portal of the UAE government, the economy of the UAE for 2023 stands at USD 509 billion with a population of 11 million and is currently investing heavily in digital transformation across all economic sectors. Developments here include the setting up of 5G wireless, Smart City technologies, and cloud computing ecosystems towards rising the digital economy from 12 percent of non-oil GDP in the UAE to 20 percent by 2030. All these measures help in developing it as a tech innovator in the region with data as a crucial value driver. UAE is also investing in large-scale data center infrastructure and AI-driven solutions to further improve digital job matching and support smart city initiatives. Public-private partnerships further strengthen the development of digital solutions, making the UAE a prominent player in the regional storage software market.

Competitive Landscape:

The storage software market is highly competitive, with key players offering a range of solutions across various sectors, including data management, backup, and cloud storage. Market leaders focus on providing scalable, secure, and high-performance solutions to meet the increasing demand for data storage due to the rise in digitalization and big data. Innovations in the cloud-native and artificial intelligence (AI) fields, and greater automation, raise competitive stakes with high efficiency storage technology. Integration and hybrid multi-cloud solutions allow corporations to better balance their infrastructure strategies. Storage data protection, recovery from disasters and compliance with privacy regulations increasingly form critical part of software components. With the rise of IoT, AI, and ML, competition continues to evolve as companies push the boundaries of storage capabilities to accommodate ever-expanding data needs.

The report provides a comprehensive analysis of the competitive landscape in the storage software market with detailed profiles of all major companies, including:

- Broadcom Inc.

- Citrix Systems, Inc.

- Dell Technologies, Inc.

- Fujitsu Limited

- Hewlett Packard Enterprise Development LP

- Hitachi Vantara LLC

- Huawei Technologies Co. Ltd

- International Business Machines Corporation (IBM)

- NetApp, Inc.

- Oracle Corporation

- Western Digital Corporation

Latest News and Developments:

- November 2024: Hitachi Vantara added a Virtual Storage Platform One to its Hybrid Cloud Storage Platform. The platform integrates object storage with block and file, incorporates QLC flash, and advances the integration of cloud. It provides reduced costs, better management of unstructured data, and enhanced energy efficiency for AI and analytics workloads.

- November 2024: Hewlett Packard Enterprise introduced its hybrid cloud advances with HPE GreenLake, making the management of heterogeneous environments easier. HPE VM Essentials integrates virtual workloads and enhances flexibility; HPE Alletra Storage MP X10000 is scalable object storage with very high performance, while HPE's disconnected private cloud solutions offer answers for the regulated sectors and new AI partnerships continue to increase innovation.

- May 2024: Dell launched PowerStore Prime at Dell Technologies World 2024. The firm's storage arrays received improved hardware, multi-cloud options, and AI capabilities with the new model. This one will feature a new QLC storage model at up to 5.9 petabytes and includes Apex integration for public cloud, as well as AIOps for improved infrastructure observability.

- February 2024: Huawei launched three key data storage technologies: an AI data lake solution, an all-scenario data protection solution, and a DCS full-stack data center solution, which enables carriers to upgrade their data infrastructure for the intelligent world.

- February 2024: Broadcom through VMware has released new innovations within its Software-Defined Edge portfolio. Key news items include the introduction of a single-vendor solution, VMware VeloCloud SASE and increased collaboration with Singtel. These innovations seek to modernize networks for CSPs and make it easier for enterprises to scale edge computing using increased automation and observability.

Storage Software Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Software Types Covered | Data Protection and Recovery, Storage and Device Management, Storage Replication, Archiving, Storage Virtualization, Software Defined Storage, Storage Infrastructure, Others |

| Deployment Types Covered | Cloud-based, On-premises |

| Organization Sizes Covered | Small and Medium Enterprises, Large Enterprises |

| Verticals Covered | BFSI, Healthcare, Manufacturing, Retail, IT and Telecom, Government, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Broadcom Inc., Citrix Systems, Inc., Dell Technologies, Inc., Fujitsu Limited, Hewlett Packard Enterprise Development LP, Hitachi Vantara LLC, Huawei Technologies Co. Ltd, International Business Machines Corporation, NetApp, Inc., Oracle Corporation, Western Digital Technologies, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the storage software market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global storage software market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the storage software industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The storage software market was valued at USD 28.3 Billion in 2024.

The storage software market is projected to exhibit a CAGR of 6.82% during 2025-2033, reaching a value of USD 51.2 Billion by 2033.

Key factors driving the storage software market include the growing volume of data, increasing demand for cloud storage solutions, the need for data security and backup, and the adoption of hybrid cloud environments. Additionally, advancements in AI and machine learning technologies are driving innovation in storage management and optimization.

North America currently dominates the storage software market, accounting for a share of 37.5%. This leadership is driven by factors such as the rapid adoption of advanced technologies, cloud migration, the growing volume of data, and increasing demand for enhanced data security and disaster recovery solutions across various industries.

Some of the major players in the storage software market include Broadcom Inc., Citrix Systems, Inc., Dell Technologies, Inc., Fujitsu Limited, Hewlett Packard Enterprise Development LP, Hitachi Vantara LLC, Huawei Technologies Co. Ltd, International Business Machines Corporation, NetApp, Inc., Oracle Corporation and Western Digital Technologies, Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)