Stem Cell Manufacturing Market Report by Product (Consumables, Instruments, Stem Cell Lines), Application (Research Applications, Clinical Application, Cell and Tissue Banking Applications), End User (Pharmaceutical & Biotechnology Companies, Academic Institutes, Research Laboratories and Contract Research Organizations, Hospitals and Surgical Centers, Cell and Tissue banks, and Others), and Region 2026-2034

Stem Cell Manufacturing Market Size:

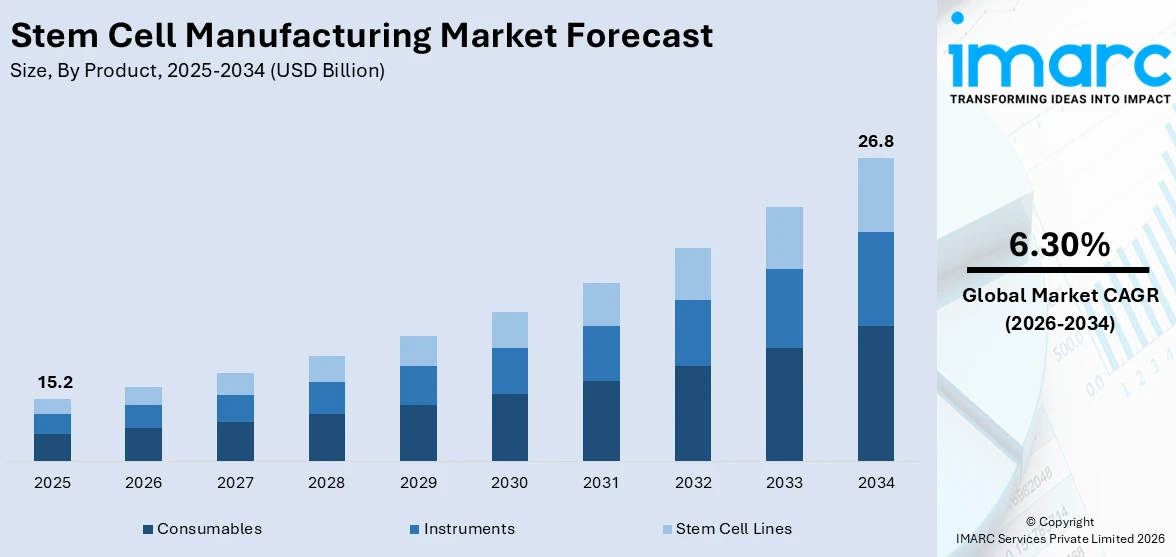

The global stem cell manufacturing market size reached USD 15.2 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 26.8 Billion by 2034, exhibiting a growth rate (CAGR) of 6.30% during 2026-2034. Increasing investments in stem cell research, rising chronic disease prevalence, advancements in biotechnology, collaborations between academia and industry, stringent regulations, and expanding awareness of stem cell therapies are stimulating the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2034 | USD 26.8 Billion |

| Market Growth Rate (2026-2034) | 6.30% |

Stem Cell Manufacturing Market Analysis:

- Major Market Drivers: Growing venture capital investment in stem cell research, supported by favorable government initiatives are majorly driving the stem cell manufacturing market. This, in turn, reflects the increasing recognition of stem cell’s potential in advancing healthcare and regenerative medicine.

- Key Market Trends: Some of the key trends in the stem cell manufacturing market include rising expenditure on stem cell research and regenerative medicine, automation of processes, increasing collaborations among industry players, and rapid advancements in bioreactor technology.

- Geographical Trends: North America is leading the stem cell manufacturing market due to several factors, including the presence of leading biotechnology and pharmaceutical companies, a supportive regulatory framework towards clinical trials and commercialization of stem cell manufacturing, robust research and development (R&D) infrastructure, and the rising demand for regenerative medicine therapies in the region.

- Competitive Landscape: Some of the major market players in the stem cell manufacturing industry include AcceGen, Bio-Rad Laboratories, Inc., Cellular Engineering Technologies, Inc, Corning Incorporated, Lonza Group AG, REPROCELL Inc, Sartorius AG, Takara Bio Inc., and Thermo Fisher Scientific Inc., among many others.

- Challenges and Opportunities: Government initiatives to boost the biotechnology and biopharmaceutical industries represent a significant opportunity for the market. Initiatives, such as grants, tax incentives, and subsidies, aim to promote R&D, attract investments, adopt advanced technologies, and accelerate scientific discoveries and innovations in therapies and treatments. However, the market also faces a significant challenge like technical limitations associated with manufacturing scale-up, which will require companies specialized equipment and infrastructure to overcome.

To get more information on this market Request Sample

Stem Cell Manufacturing Market Trends:

Increasing Investments in Stem Cell Research and Regenerative Medicine

The global stem cell manufacturing market is experiencing a significant upsurge due to the substantial investments pouring into stem cell research and regenerative medicine. Governments and private organizations are channeling resources toward these fields, recognizing their potential to revolutionize healthcare. This driver is fueled by the promising prospects of stem cell therapies in addressing previously untreatable conditions, such as neurodegenerative diseases and spinal cord injuries. For instance, an article published in the New England Journal of Medicine in August 2023 revealed the anticipated potential of stem cell gene therapy in treating Sickle Cell Disease (SCD). These investments support cutting-edge research, the development of advanced manufacturing techniques, and the expansion of clinical trials. For example, in September 2021, LifeCell International Pvt. Ltd received an investment of INR 225 crore (USD 27.2 million) from OrbiMed Asia Partners IV to further leverage its technological expertise and wide network to foray into adjacent new categories like fertility health and cell-based therapeutics. Moreover, in November 2023, ACROBiosystems Inc., a US-based company specializing in recombinant proteins and essential reagents, launched GM-grade DLL4 protein, a soluble form of Delta-like Ligand 4 (DLL4), crucial in stem cell development and differentiation.

Rising Prevalence of Chronic Diseases and the Demand for Innovative Treatments

Another vital driver propelling the global stem cell manufacturing market is the escalating prevalence of chronic diseases. Conditions like diabetes, heart disease, and autoimmune disorders are on the rise, necessitating novel and effective treatments. Stem cell therapies hold immense promise in addressing these ailments by regenerating damaged tissues and organs. For instance, in March 2021, Vertex Pharmaceuticals received FDA grant as a fast track designation to VX-880, a human stem-cell derived therapy for patients with Type-1 diabetes. Moreover, as per the December 2022 data provided by the US Food and Drug Administration (FDA), there are over 7,000 rare diseases that affect more than 30 million people in the United States. The prevalence of chronic diseases rises with age, and stem cell manufacturing exhibits promise in combating these conditions. For example, a World Health Organization factsheet from October 2021 projects that globally there will be 1.4 billion people over the age of 65 by 2030 and this number is expected to double at 2.2 billion by 2050.

Advancements in Biotechnology and Cell Culture Techniques

Advancements in biotechnology and cell culture techniques are revolutionizing the field of stem cell manufacturing. This driver is pivotal in enhancing the efficiency and scalability of stem cell production. Breakthroughs in cell culture technology, such as 3D cell culture systems and bioreactors, enable the cultivation of high-quality stem cells in larger quantities. Additionally, innovations in genetic editing techniques, like CRISPR-Cas9, offer precise control over stem cell characteristics, further expanding their therapeutic potential. These advancements not only streamline the manufacturing process but also ensure the safety and quality of stem cell-based therapies, instilling confidence among healthcare professionals and patients alike. For instance, in September 2021, Cellino, a US-based biotech company with specialization in stem cell manufacturing, presented how its system integrates AI, machine learning, and lasers, along with other hardware and software, to enhance yields and reduce production costs.

Stem Cell Manufacturing Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product, application, and end user.

Breakup by Product:

- Consumables

- Culture Media

- Others

- Instruments

- Bioreactors and Incubators

- Cell Sorters

- Others

- Stem Cell Lines

- Hematopoietic Stem Cells (HSC)

- Mesenchymal Stem Cells (MSC)

- Induced Pluripotent Stem Cells (iPSC)

- Embryonic Stem Cells (ESC)

- Neural Stem Cells (NSC)

- Multipotent Adult Progenitor Stem Cells

Consumables dominate the market

The report has provided a detailed breakup and analysis of the market based on the product. This includes consumables (culture media and others), instruments (bioreactors and incubators, cell sorters, and others), and stem cell lines (hematopoietic stem cells (HSC), mesenchymal stem cells (MSC), induced pluripotent stem cells (iPSC), embryonic stem cells (ESC), neural stem cells (NSC), and multipotent adult progenitor stem cells). According to the report, consumables represented the largest segment.

The consumables segment within the stem cell manufacturing market is experiencing robust growth due to the increasing adoption of stem cell-based research and therapies, necessitating a constant supply of consumables, including cell culture media, reagents, and growth factors. As research in this field expands, so does the demand for these essential materials. Moreover, the growing number of stem cell clinical trials and applications in regenerative medicine fuels the consumption of consumables. Clinical research and therapy development require a consistent and reliable source of high-quality consumables to ensure the safety and efficacy of stem cell-based treatments. In line with this, technological advancements in the production of consumables are driving growth.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Research Applications

- Life Science Research

- Drug Discovery and Development

- Clinical Application

- Allogenic Stem Cell Therapy

- Autologous Stem Cell Therapy

- Cell and Tissue Banking Applications

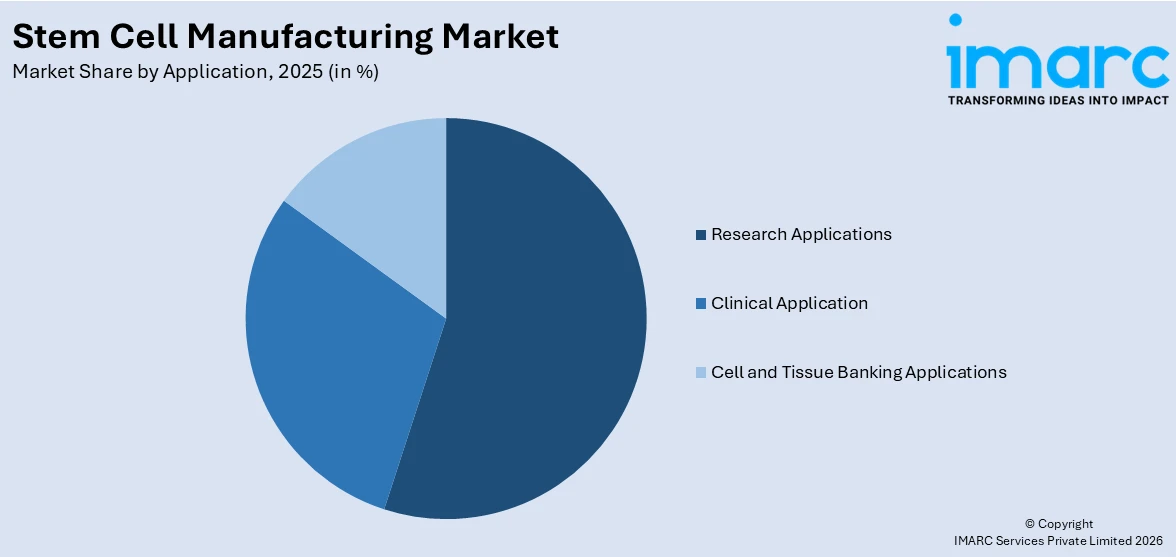

Research applications dominate the market

The report has provided a detailed breakup and analysis of the market based on the application. This includes research applications (life science research and drug discovery and development), clinical application (allogenic stem cell therapy and autologous stem cell therapy), and cell and tissue banking applications. According to the report, research applications represented the largest segment.

The growth of the research applications segment within the stem cell manufacturing market is underpinned by the relentless pursuit of scientific knowledge and breakthrough discoveries in stem cell biology. Stem cells serve as essential tools for investigating various biological processes, disease mechanisms, and potential therapeutic avenues. Researchers across diverse fields, including regenerative medicine, developmental biology, and drug development, rely on stem cells to advance their studies. Moreover, the increasing funding and grants allocated to stem cell research bolster this segment's growth. Governments, private institutions, and non-profit organizations recognize the transformative potential of stem cell research and provide financial support to drive innovation. Additionally, technological advancements in stem cell culture techniques, genetic editing, and cell characterization tools enhance the efficiency and accuracy of research applications. These advancements enable researchers to work with a broader range of stem cell types and manipulate them with precision, further expanding the scope of research possibilities. For instance, in May 2023, Sernova announced research collaboration with AstraZeneca to evaluate novel potential therapeutic cell applications.

Breakup by End User:

- Pharmaceutical & Biotechnology Companies

- Academic Institutes, Research Laboratories and Contract Research Organizations

- Hospitals and Surgical Centers

- Cell and Tissue banks

- Others

Pharmaceutical & biotechnology companies dominate the market

The report has provided a detailed breakup and analysis of the market based on the end user. This includes pharmaceutical & biotechnology companies, academic institutes, research laboratories and contract research organizations, hospitals and surgical centers, cell and tissue banks, and others. According to the report, pharmaceutical & biotechnology companies represented the largest segment.

The growth of pharmaceutical and biotechnology companies is propelled by the continuous expansion of the global population and the aging demographic trends. With an aging population, the demand for healthcare services, medications, and innovative therapies rises, providing a substantial market for pharmaceutical and biotechnology companies to cater to. Moreover, the increasing prevalence of chronic diseases, including cardiovascular disorders, cancer, and diabetes, necessitates ongoing research and the development of new pharmaceutical solutions. These companies play a pivotal role in creating advanced drugs and therapies to combat these health challenges. Furthermore, advancements in biotechnology, including gene therapy, precision medicine, and biopharmaceuticals, are shaping the industry.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest stem cell manufacturing market share

The market research report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America accounted for the largest market share.

The North American region is experiencing robust growth in the stem cell manufacturing market, propelled by the substantial government funding and private investments in stem cell research and regenerative medicine. These financial commitments support cutting-edge research, clinical trials, and the development of advanced manufacturing techniques. Moreover, the prevalence of chronic diseases, such as diabetes, heart disease, and neurodegenerative disorders, is on the rise in North America. Stem cell therapies offer innovative solutions to address these conditions, fueling demand for their production. In line with this, the region boasts a highly developed biotechnology sector, leading to significant advancements in cell culture techniques and bioprocessing technologies. This ensures efficient and scalable stem cell production, strengthening the industry's foothold in North America. Furthermore, regulatory frameworks in North America provide a conducive environment for stem cell research and clinical trials, fostering growth and innovation. Collaborative efforts between academic institutions and industry players, along with growing public awareness of the potential of stem cell-based treatments, are additional drivers.

Competitive Landscape:

The competitive landscape within the global stem cell manufacturing market is characterized by a dynamic interplay of numerous players, each vying to establish their prominence and contribute to the industry's growth. These entities span a spectrum of organizations, including research institutions, biotechnology companies, pharmaceutical giants, and contract manufacturing organizations. Their diverse backgrounds and resources contribute to a multifaceted ecosystem that fosters innovation and advancements in stem cell manufacturing. Key competitive strategies encompass research and development efforts to enhance manufacturing processes, scale up production, and improve the quality and safety of stem cell-based therapies. Additionally, partnerships and collaborations between these players are common, facilitating knowledge sharing and the development of cutting-edge technologies. For instance, in June 2021, Catalent, in a strategic move, acquired RheinCell Therapeutics Gmbh for an undisclosed amount to expand the creation of advanced cell treatments, thereby enhancing Catalent’s capacity for large-scale production. Regulatory compliance and adherence to ethical standards are pivotal in maintaining credibility within the market. Moreover, market participants often engage in marketing and educational initiatives to increase awareness of stem cell therapies among healthcare professionals and the public, further expanding their reach.

The report provides a comprehensive analysis of the competitive landscape in the global stem cell manufacturing market with detailed profiles of all major companies, including:

- AcceGen

- Bio-Rad Laboratories, Inc.

- Cellular Engineering Technologies, Inc

- Corning Incorporated

- Lonza Group AG

- REPROCELL Inc

- Sartorius AG

- Takara Bio Inc.

- Thermo Fisher Scientific Inc.

Stem Cell Manufacturing Market News:

- In July 2023, Bio-Techne Corporation announced the complete acquisition of Lunaphore Technologies SA, a leading developer of fully automated spatial biology solutions. Bio-Techne and Lunaphore are combining forces to accelerate their spatial biology leadership position in translational and clinical research markets.

- In June 2023, Becton Dickinson and Company announced to invest US$ 80 million in the construction of its third plant in Ciudad Juarez.

- In September 2023, FDA approved Motixafortide plus filgrastim used for the stem cell mobilization in multiple myeloma.

Stem Cell Manufacturing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Applications Covered |

|

| End Users Covered | Pharmaceutical & Biotechnology Companies, Academic Institutes, Research Laboratories and Contract Research Organizations, Hospitals and Surgical Centers, Cell and Tissue banks, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AcceGen, Bio-Rad Laboratories, Inc., Cellular Engineering Technologies, Inc, Corning Incorporated, Lonza Group AG, REPROCELL Inc, Sartorius AG, Takara Bio Inc., Thermo Fisher Scientific Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the stem cell manufacturing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global stem cell manufacturing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the stem cell manufacturing industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Stem Cell Manufacturing Market Report

The global stem cell manufacturing market was valued at USD 15.2 Billion in 2025.

We expect the global stem cell manufacturing market to exhibit a CAGR of 6.30% during 2026-2034.

The increasing adoption of stem cell across the pharmaceuticals industry for manufacturing Hematopoietic Stem Cells (HSC)- and Mesenchymal Stem Cells (MSC)-based drugs to treat tumors, leukemia, lymphoma, etc., is primarily driving the global stem cell manufacturing market.

The sudden outbreak of the COVID-19 pandemic has led to the growing demand for stem cell manufacturing to produce drugs that are utilized to treat patients with lung failures.

Based on the product, the global stem cell manufacturing market can be categorized into consumables, instruments, and stem cell lines, where consumables currently exhibit a clear dominance in the market.

Based on the application, the global stem cell manufacturing market has been segregated into research applications, clinical application, and cell and tissue banking applications. Currently, research applications account for the majority of the global market share.

Based on the end user, the global stem cell manufacturing market can be bifurcated into pharmaceutical & biotechnology companies, academic institutes, research laboratories and contract research organizations, hospitals and surgical centers, cell and tissue banks, and others. Among these, pharmaceutical & biotechnology companies hold the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global stem cell manufacturing market include AcceGen, Bio-Rad Laboratories, Inc., Cellular Engineering Technologies, Inc, Corning Incorporated, Lonza Group AG, REPROCELL Inc, Sartorius AG, Takara Bio Inc., and Thermo Fisher Scientific Inc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)