Steel Grating Market Size, Share, Trends and Forecast by Material Type, Fabrication, Surface Type, Application, End Use Industry, and Region, 2026-2034

Global Steel Grating Market Size, Share, Trends & Forecast (2026-2034)

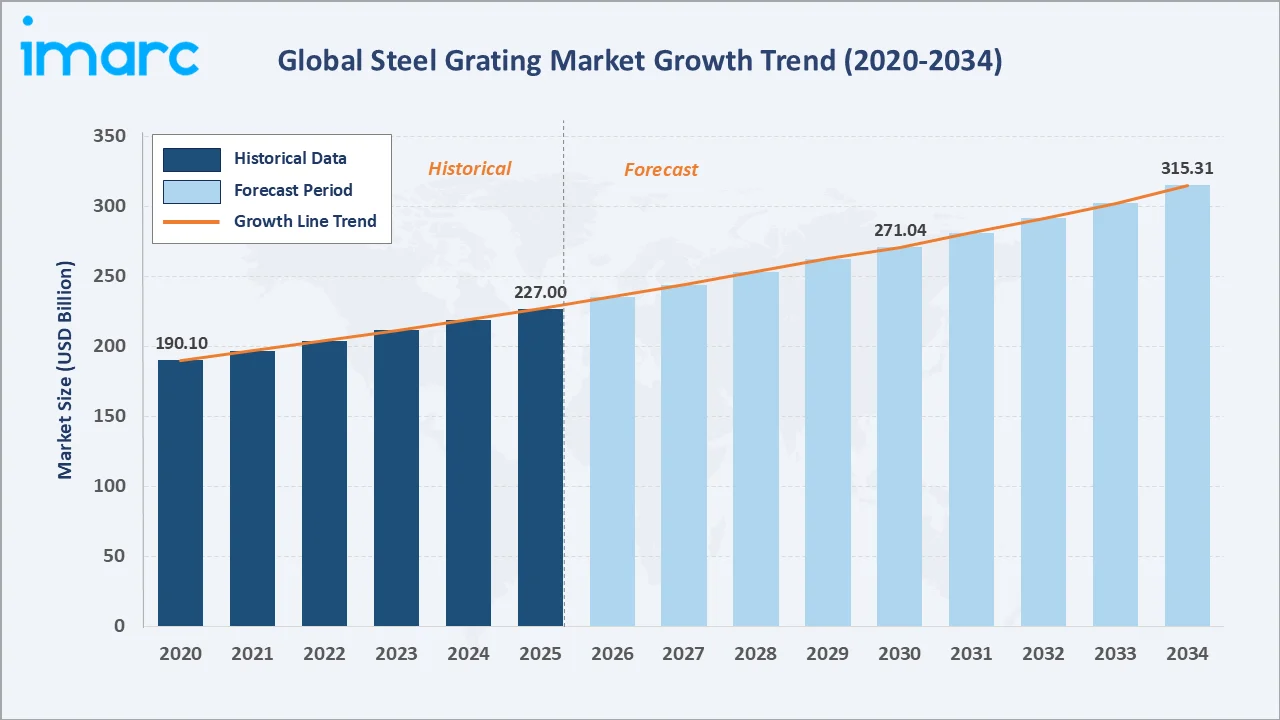

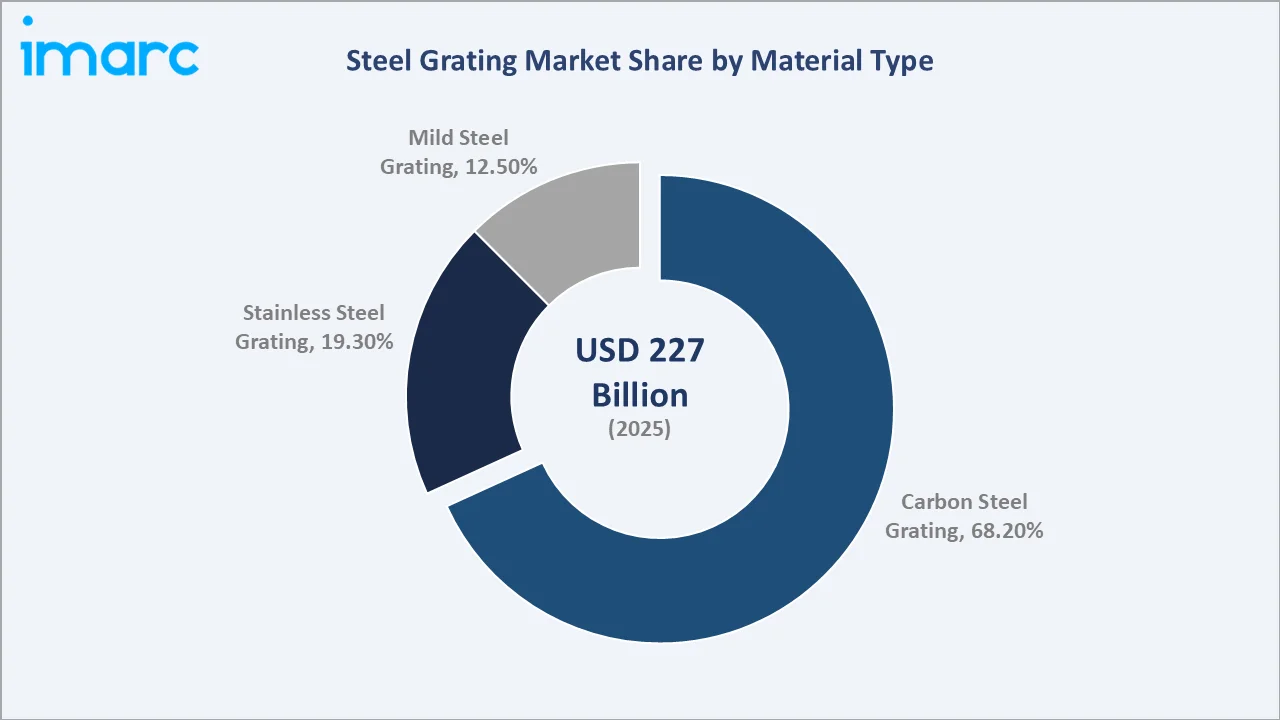

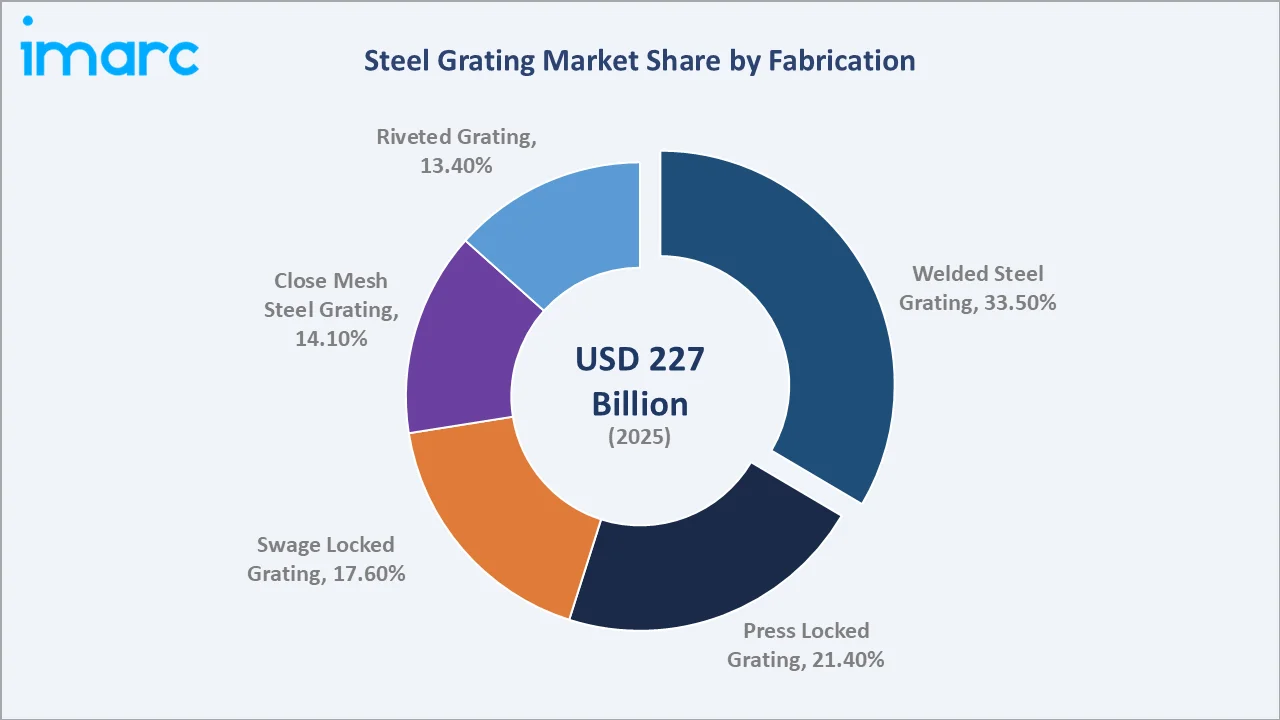

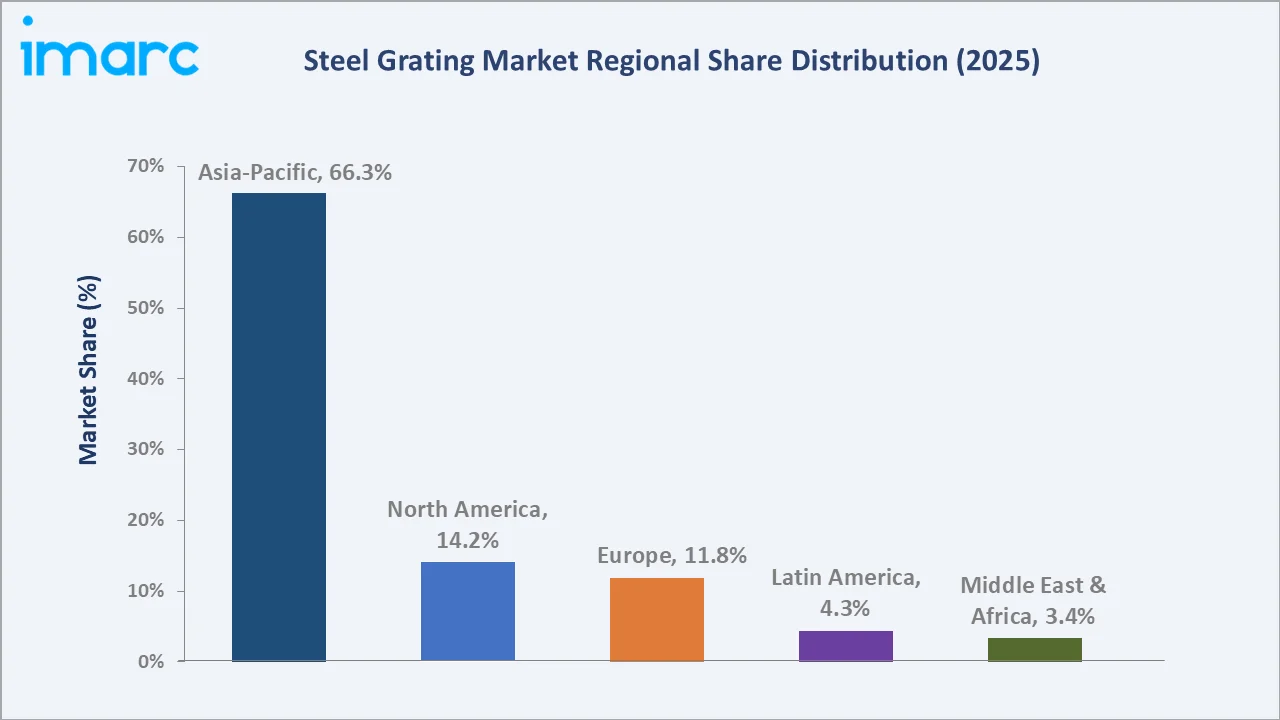

The global steel grating market size reached USD 227.0 Billion in 2025 and is projected to reach USD 315.3 Billion by 2034, exhibiting a CAGR of 3.61% during 2026-2034. Accelerating global infrastructure investment with Private Participation in Infrastructure (PPI) investment reached $100.7 billion in 2024, robust expansion of oil and gas processing facilities, and the growth of energy generation infrastructure are the primary forces driving steel grating market growth. Carbon steel grating dominates the material type at 68.2% in 2025, while welded steel grating leads the fabrication segment at 33.5%. Asia-Pacific commands a dominant 66.3% regional share in 2025, reflecting China and India's unparalleled construction and industrial activity.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 227.0 Billion |

|

Forecast Market Size (2034) |

USD 315.3 Billion |

|

CAGR (2026-2034) |

3.61% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (66.3% share, 2025) |

|

Second Region |

North America (14.2% share, 2025) |

|

Leading Material Type |

Carbon Steel Grating (68.2%, 2025) |

|

Leading Fabrication |

Welded Steel Grating (33.5%, 2025) |

The global steel grating market growth trajectory from 2020 through 2034, with the historical expansion to USD 227.0 Billion in 2025, reflects consistent infrastructure-driven demand, while the forecast to USD 315.3 Billion captures accelerating energy transition investment, industrial construction, and Asia-Pacific urbanization-led demand.

To get more information on this market, Request Sample

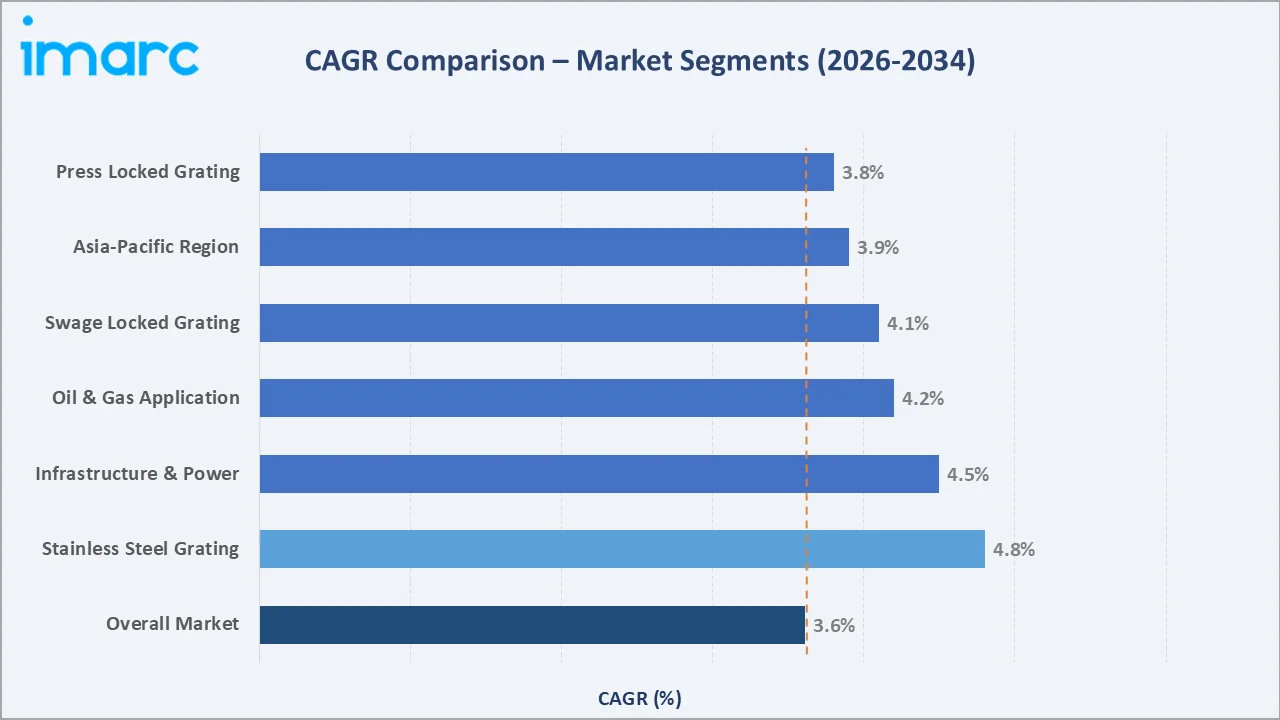

The CAGR trajectories across key material, fabrication, and regional sub-segments, with stainless steel grating at ~4.8% CAGR and infrastructure and power applications at ~4.5% CAGR, are the fastest-growing categories within the global steel grating industry analysis through 2034.

Executive Summary

The global steel grating market is on a sustained growth trajectory from USD 227.0 Billion in 2025 to USD 315.3 Billion by 2034. Steel grating, an essential structural and safety component deployed across platforms, walkways, flooring, drainage covers, and stair treads in industrial, infrastructure, and commercial construction, benefits from the non-discretionary nature of its demand.

Carbon steel grating dominates material type at 68.2% in 2025, owing to its favorable cost-to-strength ratio and broad availability across global steel supply chains. Stainless steel grating (19.3%) commands premium pricing in corrosive environments, food processing facilities, offshore platforms, chemical plants, and pharmaceutical cleanrooms, growing at the fastest material CAGR of ~4.8% through 2034. Welded steel grating leads fabrication at 33.5% in 2025, reflecting its widespread specification in industrial flooring, drainage, and general walkway applications.

Asia-Pacific dominates at 66.3% in 2025, reflecting China's position as both the world's largest steel producer and its largest construction market. India, Southeast Asia, Japan, and South Korea contribute meaningfully to the region's demand. North America (14.2%) and Europe (11.8%) follow, driven by infrastructure maintenance and industrial reinvestment cycles.

Key Market Insights

|

Insight |

Data |

|

Largest Material Type |

Carbon Steel Grating - 68.2% share (2025) |

|

Leading Fabrication |

Welded Steel Grating - 33.5% share (2025) |

|

Leading Region |

Asia-Pacific - 66.3% revenue share (2025) |

|

Second Region |

North America - 14.2% revenue share (2025) |

|

Top Companies |

Nucor, Webforge (Valmont), IKG, Ohio Gratings, MEISER GmbH, Lionweld Kennedy, AMICO |

Key Analytical Observations Supporting the Above Data:

- Carbon steel grating, with 68.2% in 2025, dominates because of its superior cost-to-strength profile. For the vast majority of industrial applications, manufacturing plant walkways, drainage covers, vehicle access panels, and hot-dip galvanized structural steel provide 72-73 years of life at a minimum total cost of ownership.

- Welded steel grating, with 33.5% in 2025, leads fabrication because it represents the most cost-effective and specification-flexible production method. Welded grating satisfies the broadest range of ASTM A1011, EN 1433, and AS/NZS 3996, load-bearing code requirements and is the standard specification for the majority of industrial flooring, walkway, and drainage applications globally.

- Asia-Pacific's 66.3% dominance in 2025 reflects multiple structural forces acting simultaneously. China produces approximately 54% of global crude steel and maintains vertically integrated steel grating manufacturing at cost structures 30-50% below Western equivalents.

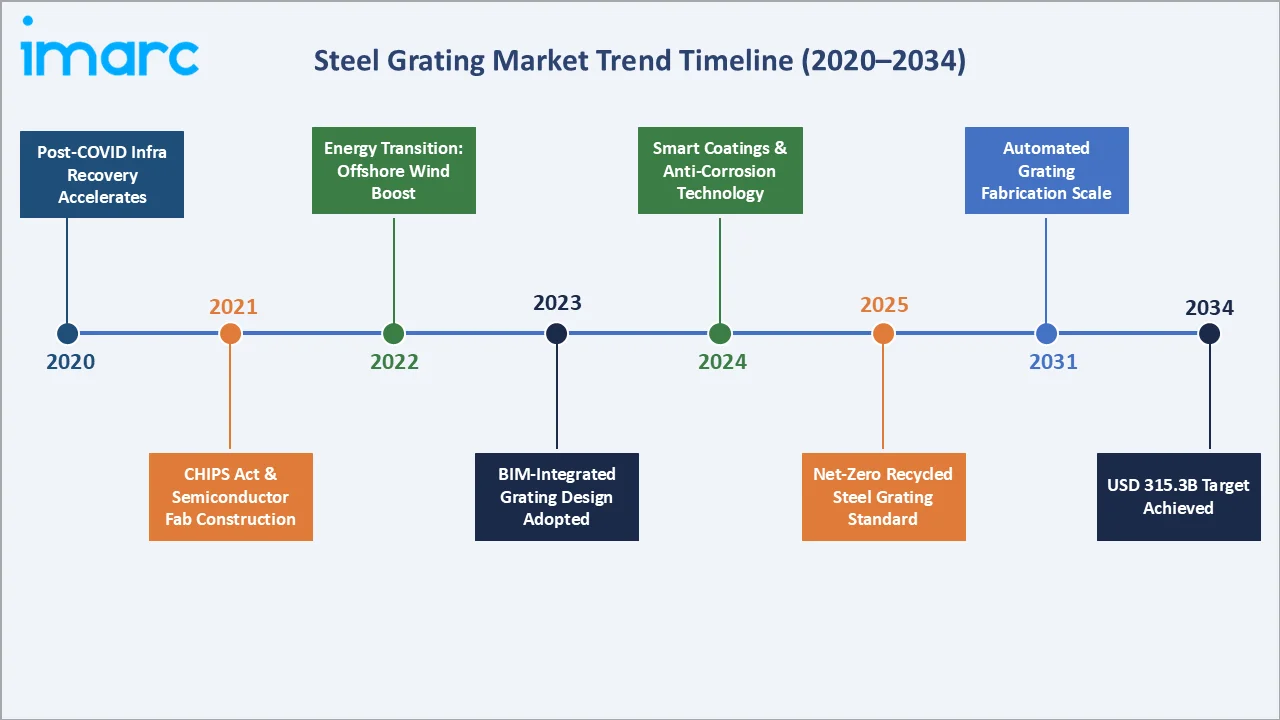

- North America, with 14.2% in 2025 benefits from the US CHIPS and Science Act's USD 52 Billion semiconductor manufacturing investment wave and the continued expansion of US petrochemical and LNG export facilities, all generating industrial grating procurement demand from domestic manufacturers.

Global Steel Grating Market Overview

Steel grating is a structural grid product manufactured by joining longitudinal bearing bars with transverse cross bars through welding, pressing, swaging, or riveting to create open-grid floor panels, walkways, platforms, drainage covers, and stair treads. Product configurations are defined by bearing bar size and spacing, cross bar pitch, panel dimensions, and surface treatment (plain, serrated, or galvanized).

The global ecosystem integrates primary steel producers, steel bar and flat product rolling mills, grating fabrication and finishing companies, surface treatment providers, steel service centre distributors, engineering procurement and construction (EPC) contractors, and diverse end-use industries spanning oil and gas, petrochemicals, power generation, transportation infrastructure, mining, food processing, and commercial architecture.

Market Dynamics

To evaluate market opportunities, Request Sample

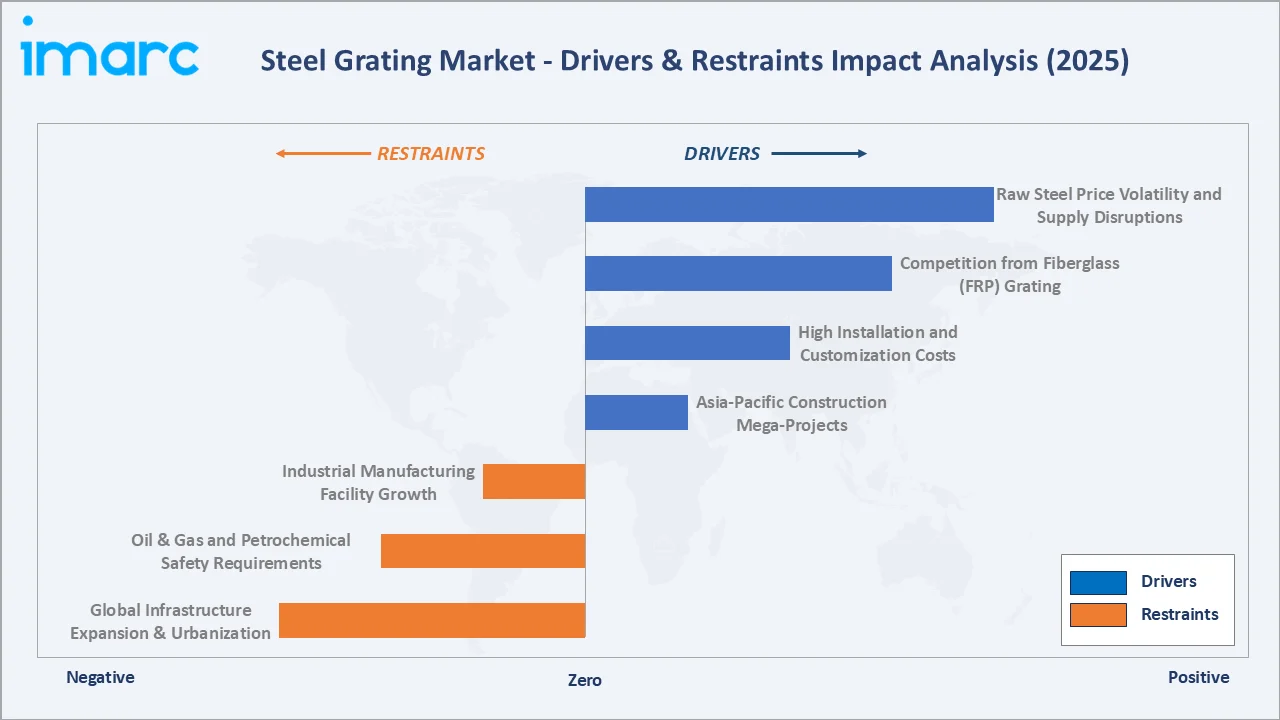

Market Drivers

- Global Infrastructure Expansion and Urbanization: The World Bank estimates USD 94 Trillion in global infrastructure investment is needed through 2040 to meet developing economy urbanization demands.

- Oil & Gas and Petrochemical Industry Expansion: The liquefied natural gas (LNG) capacity expansion, with an additional 200 million tonnes of LNG expected to be added, representing about 50% of the current annual LNG trade by 2030, is generating large-scale offshore platform and onshore processing facility construction.

- Semiconductor Manufacturing and Industrial Reinvestment: The global semiconductor manufacturing renaissance, driven by the US CHIPS Act (USD 52 Billion), EU Chips Act (EUR 43 Billion), Japan's semiconductor subsidy programme (USD 13 Billion), and South Korea's K-Chips Act, is constructing the largest wave of semiconductor fabrication facilities in history.

Market Restraints

- Raw Steel Price Volatility and Supply Chain Disruptions: International steel prices stayed between USD 605 and USD 654 per tonne from March 2019 to December 2020. Prices rose in December 2020 due to supply disruptions caused by the COVID-19 pandemic and increased raw material costs. The escalation continued with the onset of the Russia-Ukraine war in February 2022.

- Customization Complexity and Lead Time Challenges: Steel grating projects requiring non-standard panel dimensions, specialized load ratings, unique bar configurations, or proprietary surface treatments generate engineering and production lead times of 4-12 weeks versus 1-2 weeks for standard stocked panel sizes.

Market Opportunities

- Data Center Infrastructure Expansion: Nearly 100 GW of new data centers are being added between 2026 and 2030, doubling global capacity, driven by AI computing infrastructure requirements from Hyperscalers and enterprise co-location demand. Each data center incorporates steel grating extensively in raised floor systems, cable management walkways, equipment mezzanines, and outdoor utility areas.

- Architectural and Commercial Premium Grating: The growing specification of industrial aesthetics in commercial architecture, exposed structural elements, perforated and mesh screens, open-grid flooring in upscale retail and hospitality, is creating demand for premium-finish steel grating products with tighter tolerances, powder coat or decorative surface treatments, and custom geometric configurations.

Market Challenges

- Decarbonization Pressure and Carbon Border Adjustment: The EU's Carbon Border Adjustment Mechanism (CBAM), taking effect from 2026, will impose carbon costs on steel and steel product imports into the EU from high-emission origins.

- Skilled Welding and Fabrication Workforce Shortage: The global welding skills shortage, the American Welding Society projects a deficit of 360,000 welders in the US alone by 2027, creates production capacity constraints for resistance welding-intensive welded grating production.

Emerging Market Trends

1. BIM Integration and Digital Fabrication Transforming Grating Procurement

Building Information Modeling (BIM) adoption across global EPC contractor practices is transforming how steel grating is specified, procured, and fabricated. BIM integration reduces design errors by 50-60%, enables automated quantity takeoffs that improve procurement accuracy, and supports just-in-time delivery scheduling that reduces site storage requirements.

2. Hot-Dip Galvanizing and Advanced Coating Technology Extending Service Life

Environmental regulations and total lifecycle cost optimization are driving adoption of higher-performance surface treatments that extend grating service life and reduce maintenance frequency. Duplex coating systems combining hot-dip galvanizing with powder coat top coating are gaining specification in coastal and chemical exposure environments.

3. Offshore Wind Platform and Energy Transition Grating Demand

GWEC's forecast of 380 GW of new offshore wind by 2032 implies the construction of offshore wind structures, each requiring customized marine-grade grating packages for transition pieces, ladder safety systems, J-tube cable guides, and boat landing platforms.

4. Automation in Grating Fabrication Reducing Production Costs

Advanced resistance welding robots, CNC plasma cutting, and automated galvanizing line technology are progressively reducing the labor intensity of grating fabrication. Robotic welding systems capable of producing standard welded grating panels are reducing per-unit production costs, enabling price competitiveness in volume commodity markets while freeing the workforce for higher-value custom fabrication work.

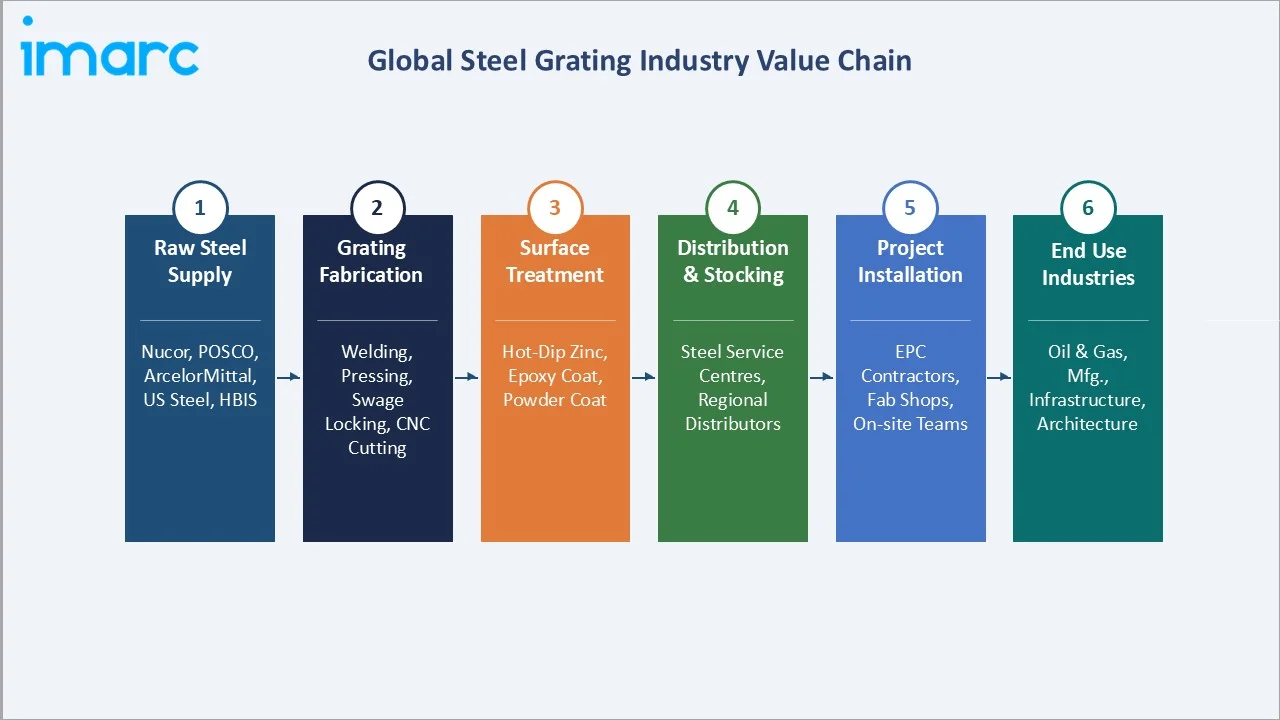

Industry Value Chain Analysis

The steel grating value chain spans six stages from raw steel input through end-use installation. Fabrication and surface treatment capture the highest value-add margins, while distribution logistics and project-specific customization generate significant working capital requirements that favor well-capitalized mid-to-large manufacturers.

|

Stage |

Key Players / Examples |

|

Raw Steel Supply |

Nucor Corporation (US), ArcelorMittal (Global), HBIS Group (China), Tata Steel (India) |

|

Grating Fabrication |

Webforge (Valmont), Ohio Gratings, MEISER GmbH, AMICO, Lionweld Kennedy, Enzar Metal |

|

Surface Treatment |

AZZ Inc. (galvanizing), Thomas Galvanizing, industrial coating providers; in-house galvanizing at major manufacturers |

|

Distribution & Stocking |

Steel service centers, regional industrial distributors, and manufacturer direct to project |

|

Project Installation |

EPC contractors, mechanical/structural subcontractors, and maintenance turnaround firms |

|

End Use Industries |

Oil & Gas, Chemical, Power Generation, Manufacturing, Mining, Water Treatment, Transportation, Architecture |

Integrated grating manufacturers with captive steel sourcing arrangements and in-house galvanizing capabilities, such as Nucor's vertically integrated model incorporating its own EAF steel production, achieve lower material cost bases than processors relying entirely on spot market steel procurement. This vertical integration is a meaningful competitive advantage in commodity market segments where price competition is intense.

Technology Landscape in the Steel Grating Industry

Welding and Joining Technology: Resistance Welding to CNC Automation

The dominant welding technology in steel grating production is electrical resistance welding (ERW), where cross rods are resistance-welded to bearing bars at precisely controlled current, force, and time parameters. CNC-controlled shearing and sawing systems enable precision panel cutting to custom dimensions with ±1mm tolerances, meeting the tight dimensional specifications required for elevated platform and process equipment applications.

Material Innovation: High-Strength Low-Alloy and Duplex Stainless Steel

High-strength low-alloy (HSLA) steels, specifically ASTM A572 Grade 50 and Grade 60, are progressively replacing conventional A36 mild steel in bearing bar production for heavy-duty applications. HSLA steels, such as A572 steel, achieve yield strengths of 50,000 PSI, a tensile strength of 65,000 PSI, and elongation percentage of 18%.

Surface Treatment Technology: Hot-Dip Galvanizing and Thermal Spray

Hot-dip galvanizing to ASTM A123 remains the dominant surface protection system for carbon steel grating, applying metallurgically bonded zinc coatings through immersion in 450°C zinc baths. Electroless nickel plating and specialized polymer coatings are specified for pharmaceutical and food processing gratings where aluminum zinc residue is unacceptable.

Digital Design and BIM Object Libraries

Steel grating manufacturers are investing in digital product libraries compatible with Autodesk Revit, Bentley OpenBuildings, and Trimble Tekla Structures BIM environments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material Type |

Carbon Steel Grating |

68.2% |

2025 |

|

Fabrication |

Welded Steel Grating |

33.5% |

2025 |

|

Surface Type |

Serrated Steel Grating |

62.6% |

2025 |

|

Application |

Platform |

18.5% |

2025 |

| End Use Industry | Oil & Gas | 12.8% | 2025 |

|

Region |

Asia-Pacific |

66.3% |

2025 |

By Material Type

Carbon steel grating commands a 68.2% majority share in 2025 owing to its fundamental cost-competitiveness and broad structural performance across the majority of industrial and construction applications. The low-cost profile makes carbon steel grating the default specification across general manufacturing, petrochemical facility maintenance platforms, transportation infrastructure drainage, and commercial construction.

To access detailed market analysis, Request Sample

Stainless steel grating at 19.3% in 2025, growing fastest, is irreplaceable in environments where corrosion would compromise structural integrity and safety within standard design service life. The substantial per-tonne price premium generates revenue significance disproportionate to volume share. Mild steel grating (12.5%) serves light-duty and indoor applications where corrosion risk is minimal and budget sensitivity is high.

By Fabrication

Welded steel grating dominates the fabrication segment at 33.5% in 2025, representing the highest-volume, most cost-efficient production method for standard industrial applications. Large-format welded grating panels, up to 24" x 240", minimize installation joints and reduce field labor on elevated platform applications.

Press locked grating, with 21.4% in 2025, provides a flush surface with cross bars mechanically pressed through pre-punched slots in bearing bars to a friction fit, eliminating welding heat distortion and producing a dimensionally precise, aesthetically cleaner panel preferred in architectural and public area applications.

Swage locked grating, with 17.6% in 2025, uses a hydraulic swaging tool to mechanically deform bearing bars around cross rods, creating a permanent lock without welding, the preferred method for stainless steel grating fabrication, where avoiding heat-affected zone corrosion at welds is critical. Close mesh steel grating (14.1%) provides heel-proof and equipment-protection surfaces specified in areas where small objects falling through standard grid spacings would create safety hazards. Riveted grating (13.4%) offers high lateral rigidity for applications subject to horizontal loading and vibration.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

66.3% |

China's infrastructure dominance; ASEAN industrialization; offshore energy |

|

North America |

14.2% |

CHIPS Act semiconductor fabs; IIJ Act infrastructure; US LNG expansion; data center boom |

|

Europe |

11.8% |

Industrial maintenance cycles; EU Green Deal green hydrogen; offshore wind North Sea |

|

Latin America |

4.3% |

Brazil Petrobras offshore oil; Chile/Peru mining expansion; Mexico manufacturing nearshoring |

|

Middle East & Africa |

3.4% |

GCC Vision 2030 industrial diversification; NEOM mega-projects; African mining infrastructure |

Asia-Pacific's 66.3% market dominance in 2025 is driven by the most structurally exceptional combination of steel production scale, construction investment, and industrial expansion in any global market. China's crude steel production reached 952.14 million tons in the first 11 months of 2023, reflecting a 1.5% increase compared to the previous year, providing an unparalleled domestic supply base for Chinese steel grating manufacturers.

North America, with 14.2% in 2025, is experiencing a pronounced industrial renaissance. The Bipartisan Infrastructure Law's USD 1.2 Trillion investment includes USD 110 Billion for roads and bridges and USD 65 Billion for broadband, each category generating steel grating procurement through replacement and new construction.

Competitive Landscape

The global steel grating market is moderately fragmented, with regional leaders holding strong positions in their home markets while several large global suppliers compete across multiple geographies. Asia-Pacific's market is dominated by Chinese domestic manufacturers, while North American and European markets are served by well-established specialized grating companies.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

AMICO |

AMICO Bar Grating, Amico Safety Grating |

Leader |

US market leader; Bar grating + expanded metal; construction |

|

Anping Enzar Metal Products Co. Ltd. |

Welded Steel Bar Grating, Press-locked steel grating, Aluminum Bar Grating, Stainless Steel Bar Grating, Stair Tread Gratings, Interlocking Safety Grating |

Leader |

China & APAC export; welded & press locked; price leadership |

|

Gebrüder MEISER GmbH |

Press locked Grating, Press Welded Grating, Shelf Grating, Special Grating |

Leader |

Europe leader; architectural & industrial; offshore capability |

|

IKG (Harsco) |

Welded Grating, Pressure Locked Grating |

Leader |

North America & global; full fabrication range; oil & gas |

|

Lichtgitter GmbH |

Forge-welded gratings, Press-locked gratings, Shelf gratings, GRP Gratings, Grating steps |

Challenger |

European specialty; architectural; custom profiles |

|

Lionweld Kennedy |

Safegrid, Safedeck, Safegrid Treads |

Challenger |

UK & Middle East; offshore and industrial; stainless range |

|

Nucor Corporation |

Welded Bar Grating |

Leader |

Vertically integrated US leader; EAF steel + grating |

|

Ohio Gratings Inc. |

Carbon Steel Grating and Stainless Steel Grating |

Challenger |

US Midwest; welded bar grating; industrial distribution |

|

P&R Metals Inc. |

Carbon Steel and Stainless Steel Grating |

Emerging |

US East regional; bar grating; commercial & industrial |

|

Webforge Locker (Valmont Industries Inc.) |

Stock Panels or Fabricated Systems, Slip Resistance |

Leader |

Asia-Pacific & global; widest product range; offshore |

The competitive positioning of key global steel grating market participants across global market presence and strategic investment dimensions in 2025.

Key Company Profiles

Nucor Corporation

Nucor Corporation is the largest steel producer in the United States. Nucor's unique vertical integration from scrap steel procurement through EAF melting, rolling, and grating fabrication enables cost structures below competitors' dependent on external steel procurement.

- Product Portfolio: Offers welded bar grating for steel

- Recent Developments: In June 2023, ExxonMobil Low Carbon Solutions secured a new carbon capture and storage agreement with Nucor Corporation, one of North America’s largest steel producers.

- Strategic Focus: Nucor's grating strategy leverages its vertically integrated model to compete on total delivered cost in the US industrial and infrastructure market, while expanding its product range toward higher-value custom and specialty grating applications where fabrication expertise and rapid delivery capabilities command premium pricing over commodity steel panel imports.

Webforge Locker (Valmont Industries Inc.)

Webforge is the Asia-Pacific's largest steel grating manufacturer, operating as a division of Valmont Industries, a global infrastructure products company.

- Product Portfolio: Company offers Stock Panels or Fabricated Systems, Slip Resistance products for steel grating

- Recent Developments: The company secured major supply agreements, demonstrating its marine environment certification capabilities and positioning for the growing offshore energy transition grating market.

- Strategic Focus: Webforge's strategy focuses on maintaining Asia-Pacific market leadership through the broadest product range in the region, premium technical certification capabilities for offshore and energy transition applications, and digital specification tools that create preference advantage in EPC contractor procurement decision processes.

Gebrüder MEISER GmbH

Gebrüder MEISER GmbH is a leading European steel grating manufacturer headquartered in Germany, with manufacturing operations across Germany, Poland, Dubai, Hungary, France, Belgium, Egypt, Brazil, etc. The company serves both standard industrial markets and premium architectural applications, with particular strength in custom grating solutions requiring complex geometries, tight tolerances, and specialized surface treatments.

- Product Portfolio: The company offers Press locked Grating, Press Welded Grating, Shelf Grating, Special Grating for steel grating.

- Recent Developments: The company secured supply contracts, expanding its offshore energy market presence significantly.

- Strategic Focus: MEISER's strategy differentiates on technical quality and custom fabrication capability in European and export markets, targeting the premium architectural grating and offshore energy segments where its engineering depth, certification capabilities, and production precision command price premiums over commodity Asian imports.

Ohio Gratings Inc.

Ohio Gratings Inc. is a leading independent US steel grating manufacturer headquartered in Canton, Ohio. Founded in 1970, the company specializes in welded and pressure locked steel grating for the industrial, commercial, and construction markets, serving customers across the United States through a national distributor network and direct project sales.

- Product Portfolio: The company offers Carbon Steel Grating and Stainless Steel Grating.

- Recent Developments: The company strengthened its distributor network to capture construction growth driven by semiconductor and energy facility construction.

- Strategic Focus: Ohio Gratings focuses on service reliability, short lead times, consistent quality, and responsive technical support, as its primary competitive differentiator in the price-competitive US industrial grating market, supplemented by a broad product range that covers the majority of standard specification requirements without custom engineering.

Market Concentration Analysis

The global steel grating market is moderately fragmented at the global level, reflecting significant regional concentration among national or regional leaders, with no single company holding more than 5-8% of total global market revenue. Asia-Pacific, which represents 66.3% of the market, is served primarily by domestic Chinese and Australian manufacturers, while North American and European markets have their own distinct competitive ecosystems.

Consolidation at the regional level is more advanced than global consolidation suggests. Valmont Industries' Webforge division, through its multi-country Asia-Pacific manufacturing network, holds a disproportionate value share of the Australian, New Zealand, and Southeast Asian markets. Global consolidation through M&A is occurring primarily through large industrial conglomerates acquiring regional grating specialists as strategic bolt-on additions.

Investment & Growth Opportunities

Fastest-Growing Segments

Stainless steel grating at ~4.8% CAGR through 2034 is the highest-growth material segment, driven by offshore wind, pharmaceutical, and chemical processing applications where corrosion resistance is non-negotiable. Infrastructure and power applications growing at ~4.5% CAGR through 2034 represent the broadest-based growth opportunity.

Emerging Markets

The Middle East and Africa at ~4.1% CAGR is the fastest-growing region for steel grating through 2034. Saudi Arabia's NEOM project (USD 500 Billion) and Vision 2030 industrial diversification, UAE's industrial zone expansion, and Egyptian mega-project investment are creating large-scale grating procurement from a region with limited domestic grating manufacturing capacity.

Venture & Investment Trends

Private equity interest in consolidating fragmented regional grating markets is growing: European and North American PE firms have been active in industrial building products consolidation, and steel grating's recurring infrastructure maintenance demand and defensible regional market positions make specialist grating manufacturers attractive platform investment targets. Green steel certification investment, enabling LEED Material & Resources credit documentation for recycled content, is generating measurable sales premium in US government and institutional construction procurement.

Future Market Outlook (2026-2034)

The global steel grating market is forecast to expand from USD 227.0 Billion in 2025 to USD 315.3 Billion by 2034 at a CAGR of 3.61%, adding USD 88.3 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's infrastructure-linked, non-discretionary demand characteristics.

Three technological forces will most significantly shape the steel grating industry landscape through 2034. Green hydrogen production infrastructure, with USD 15 Trillion in cumulative clean hydrogen investment through 2050, will generate specialized grating demand for electrolysis plant platforms, hydrogen storage facility access systems, and distribution infrastructure.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews in 2024-2025 with steel grating industry stakeholders, including senior commercial managers, EPC procurement specialists, structural engineers, World Steel Association data team members, and industrial distribution professionals at Metals USA and Ryerson. Primary data validated market sizing, material type and fabrication segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include World Steel Association Steel Statistical Yearbook (2020-2024), IEA World Energy Investment Report (2024), G20 Infrastructure Investment Hub Global Infrastructure Outlook, GWEC Global Wind Report (2024), US Census Bureau construction spending data, ASTM International steel product standards publications, EN ISO steel product standards documentation, NAAMM Metal Bar Grating Manual, and trade publications including Metal Bulletin, American Metal Market, and Steel Times International.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Steel Grating Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered | Carbon Steel Grating, Stainless Steel Grating, Mild Steel Grating |

| Fabrications Covered | Welded Steel Grating, Swage Locked Grating, Press Locked Grating, Riveted Grating, Close Mesh Steel Grating |

| Surface Types Covered | Serrated Steel Grating, Plain Steel Grating |

| Applications Covered | Walkaways, Stair Threads, Platforms, Security Fence, Drainage Covers, Trench Covers, Others |

| End Use Industries Covered | Oil and Gas, Food Processing, Pharmaceuticals, Cement, Chemical, Mining, Marine, Civil Engineering, Wastewater Treatment, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AMICO, Anping Enzar Metal Products Co. Ltd., Gebrüder MEISER GmbH, IKG (Harsco), Lichtgitter GmbH, Lionweld Kennedy, Nucor Corporation, Ohio Gratings Inc., P&R Metals Inc., Webforge Locker (Valmont Industries Inc.), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the steel grating market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global steel grating market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the steel grating industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Steel Grating Market Report

The global steel grating market reached USD 227.0 Billion in 2025, reflecting consistent demand from global infrastructure investment, industrial construction, and oil and gas expansion.

The market is projected to reach USD 315.3 Billion by 2034, growing at a CAGR of 3.61% during 2026-2034, driven by Asia-Pacific construction, global energy transition infrastructure, and semiconductor manufacturing facility investment.

Carbon steel grating leads with a 68.2% material share in 2025, valued for its superior cost-to-strength ratio and broad availability, serving the majority of industrial flooring, platform, and drainage applications globally.

Welded steel grating leads at 33.5% in 2025, representing the most cost-efficient and specification-flexible production method, enabling stock availability across distributor networks for rapid industrial and infrastructure project supply.

Asia-Pacific commands a dominant 66.3% market share in 2025, driven by China's high steel output, India's National Infrastructure Pipeline, and ASEAN industrialization generating unparalleled construction and industrial grating demand.

Stainless steel grating is the fastest-growing material at ~4.8% CAGR through 2034, driven by offshore wind, pharmaceutical, and chemical processing facilities demanding corrosion-resistant safety platforms and walkways.

Leading companies include AMICO, Anping Enzar Metal Products Co. Ltd., Gebrüder MEISER GmbH, IKG (Harsco), Lichtgitter GmbH, Lionweld Kennedy, Nucor Corporation, Ohio Gratings Inc., P&R Metals Inc., and Webforge Locker (Valmont Industries Inc.).

Key applications include industrial walkways and platforms, drainage covers, stair treads, security fencing, and structural flooring across oil and gas, petrochemical, power generation, mining, manufacturing, and transportation infrastructure.

Offshore wind platform construction (GWEC forecasts 380 GW new capacity by 2032) and hydrogen production facilities are generating specialized marine-grade and stainless steel grating demand, growing at 2-3x standard industrial grating value per tonne.

Welded grating uses resistance welding to permanently join bearing bars and cross rods. Press-locked grating mechanically presses cross bars through slots in bearing bars for a flush, aesthetically cleaner surface preferred in architectural applications.

China produces over 50% of global crude steel, hosts the world's largest grating manufacturing cluster in Anping County, and combines this supply base with the world's largest construction investment, creating unparalleled market scale.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)