Sleep Apnea Devices Market Size, Share, Trends and Forecast by Product Type, End User, and Region, 2026-2034

Sleep Apnea Devices Market Size and Share:

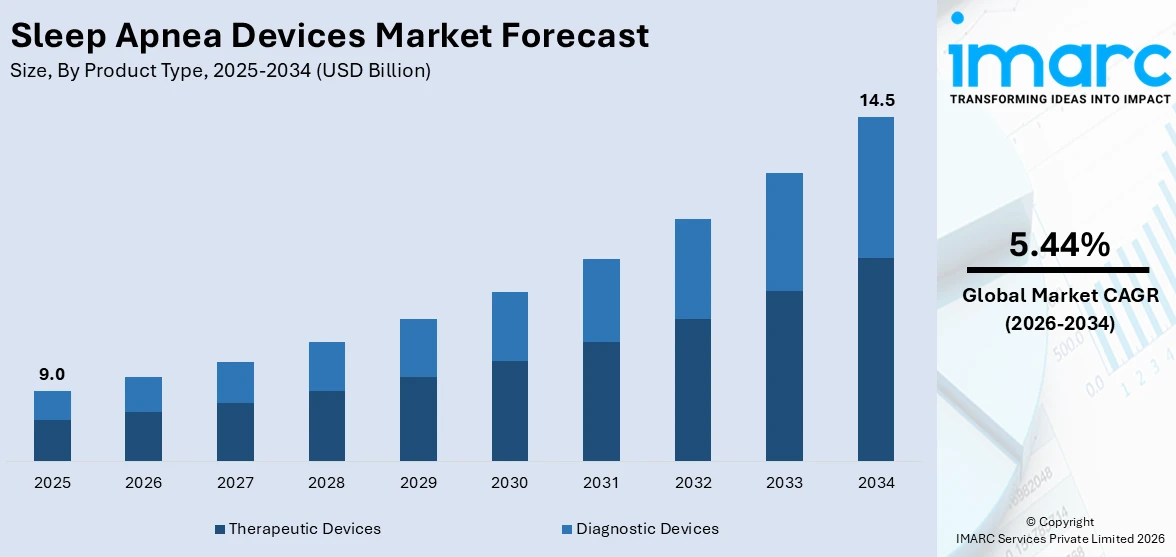

The global sleep apnea devices market size was valued at USD 9.0 Billion in 2025. The market is projected to reach USD 14.5 Billion by 2034, exhibiting a CAGR of 5.44% from 2026-2034. North America currently dominates the market, holding a market share of 49.2% in 2025. With an increasing number of individuals seeking treatment to improve sleep quality and health outcomes, the demand for sleep apnea devices is rising. Product innovations, which aid in tracking therapy effectiveness, are propelling the sleep apnea devices market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 9.0 Billion |

|

Market Forecast in 2034

|

USD 14.5 Billion |

| Market Growth Rate 2026-2034 | 5.44% |

The growing incidence of sleep-related disorders, especially obstructive sleep apnea (OSA), due to factors like obesity, stress, and sedentary lifestyles is catalyzing the demand for devices, such as continuous positive airway pressure (CPAP) machines, masks, and oral appliances. Besides this, rising awareness about the chronic health dangers linked to neglected sleep apnea, including cardiovascular disease, hypertension, and diabetes, is encouraging more patients to seek timely intervention. Expanding healthcare infrastructure and greater accessibility to diagnostic sleep labs are also supporting the market growth. Additionally, technological advancements like portable, user-friendly, and connected devices are improving patient compliance.

To get more information on this market Request Sample

The United States has emerged as a major region in the sleep apnea devices market owing to many factors. Increasing incidence of OSA is fueling the sleep apnea devices market growth. As per a study conducted in the United States, an estimated 80.6 Million people were projected to have OSA in 2024, including 47,623,848 (59%) males and 32,967,117 (41%) females. The heightened consciousness about the dangers linked to untreated aliments, such as cardiovascular disease, stroke, and diabetes, is further catalyzing the demand for diagnostic and therapeutic devices. Insurance coverage and reimbursement policies for CPAP machines, masks, and oral appliances are supporting market accessibility.

Sleep Apnea Devices Market Trends:

Growing incidence of sleep apnea cases

The high prevalence of sleep apnea cases is offering a favorable sleep apnea devices market outlook, as rising numbers of patients require timely diagnosis and effective treatment. NCBI reports that in 2025, OSA is set to impact around 936 Million adults globally aged 30 to 69. Lifestyle factors, such as obesity, stress, and sedentary routines, significantly increase the risk of OSA, leading to higher demand for therapeutic devices like CPAP and bilevel positive airway pressure (BiPAP) machines. Left untreated, sleep apnea can result in severe health complications, including hypertension, cardiovascular disease, diabetes, and reduced productivity, which is leading patients and healthcare providers towards early intervention. The growing awareness campaigns by medical associations and healthcare institutions have improved diagnosis rates, thereby expanding the patient base for device adoption.

Innovations in products

Product innovations, including out-of-center (OOC) testing devices that examine sleep patterns and respiratory parameters for the diagnosis of OSA, are among the major sleep apnea devices market trends. In January 2025, NICE endorsed the AcuPebble device from Acurable for NHS implementation, allowing at-home automated diagnosis of OSA and lessening dependence on in-clinic sleep assessments. Modern devices feature quieter motors, ergonomic mask designs, portable structures, and wireless connectivity, enabling remote monitoring and integration with digital health platforms. These features enhance patient adherence and allow physicians to track therapy effectiveness in real-time. Companies are also investing in miniaturized devices for travel use and hybrid solutions combining diagnostics and therapy in one system. Such product innovations are not only improving patient experiences but also expanding the market by attracting more individuals to adopt treatment.

Rising implementation of government regulations

Stringent regulations by governments are ensuring product safety, quality, and effectiveness, which is boosting patient and physician trust. Regulatory bodies mandate compliance with stringent guidelines for device performance, hygiene, and user safety, encouraging manufacturers to innovate and maintain high standards. In April 2025, Resmed launched NightOwl, an FDA-cleared home sleep apnea test across the US. The fingertip sensor device offered auto-scored results, remote analysis, and simplified OSA diagnosis. Stringent guidelines on infection control, clinical trials, and post-market surveillance safeguard patient well-being while preventing substandard products from entering the market. Compliance helps build credibility for trusted brands and expands adoption in hospitals, clinics, and homecare settings. Overall, government regulations are strengthening the overall market by driving innovations and enhancing the safety of sleep apnea therapies.

Sleep Apnea Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global sleep apnea devices market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type and end user.

Analysis by Product Type:

- Therapeutic Devices

- Positive Airway Pressure (PAP) Devices

- Oral Devices

- Nasal Devices

- Chin Straps

- Others

- Diagnostic Devices

- Actigraphs

- Polysomnography Devices

- Sleep Screening Devices

- Others

Therapeutic devices (positive airway pressure (PAP) devices, oral devices, nasal devices, chin straps, and others) held 76.8% of the market share in 2025. They directly address the core need of treating and managing sleep apnea effectively. Devices, such as PAP machines, along with their accompanying masks and accessories, are the primary treatment options recommended by healthcare professionals for OSA. Their ability to provide immediate symptom relief by maintaining airway patency during sleep makes them indispensable for patients. Compared to diagnostic devices, which are used only at initial stages for identifying the disorder, therapeutic devices ensure long-term management, resulting in recurring and consistent demand. Continuous advancements, such as quieter machines, wireless connectivity, portable designs, and more comfortable mask options, also improve patient compliance and adoption. Furthermore, increasing reimbursement support for therapeutic devices in many countries is enhancing affordability and accessibility. As awareness about the health risks of untreated sleep apnea is rising, therapeutic devices remain the cornerstone of treatment, ensuring their dominance in the market.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals and Clinics

- Sleep Laboratories

- Homecare Settings

- Others

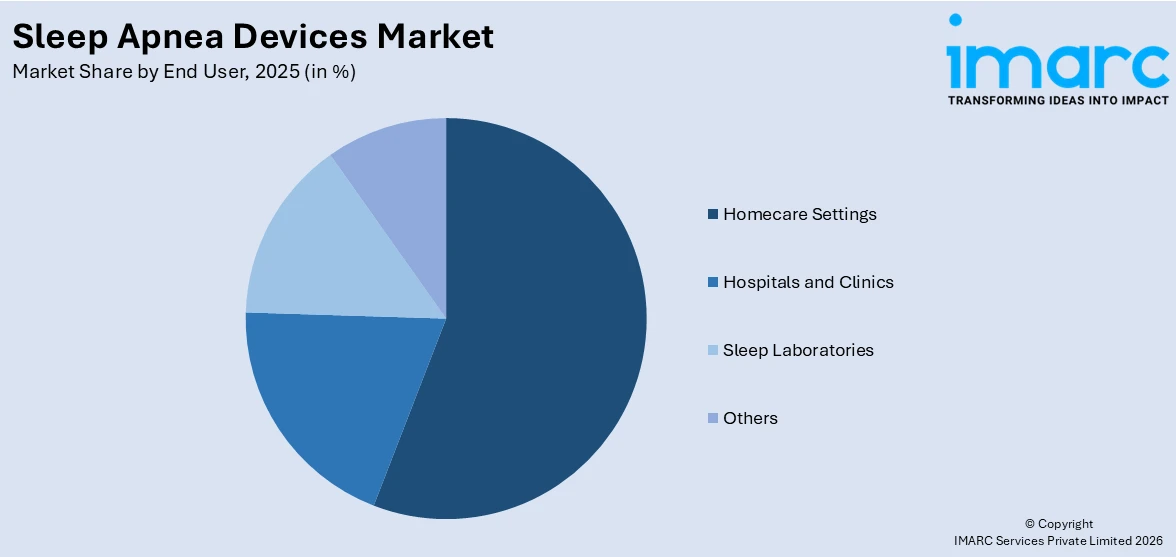

Homecare settings account for 56.9% of the market share. They provide patients with greater convenience, comfort, and independence in managing their condition. Sleep apnea often requires long-term therapy, and patients prefer using CPAP machines, masks, and oral appliances at home rather than making repeated hospital visits. Advancements in device design, including portability, quiet operation, and digital connectivity for remote monitoring, have further made home use simple and effective. This approach also reduces healthcare costs and eases the burden on hospitals and sleep clinics. Insurance coverage and reimbursement for home-use devices have encouraged the adoption, making them accessible to a wider population. Additionally, rising health awareness and the growing importance of preventive care are motivating individuals to integrate therapy into their daily routines at home. As per the sleep apnea devices market forecast, with the ongoing shift towards patient-centric healthcare and increasing aging population, homecare settings will continue to remain the dominant end user segment in the industry.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Peru

- Others

- Middle East and Africa

- Turkey

- Saudi Arabia

- Iran

- United Arab Emirates

- Others

North America, accounting for a share of 49.2%, enjoys the leading position in the market. The region has a large population suffering from obesity and related lifestyle disorders, which is significantly increasing the incidence of sleep apnea. According to a 2024 study published in the medical journal ‘The Lancet’, around 3 out of 4 adults in the US were classified as overweight or obese. Widespread awareness about sleep apnea and its health risks, supported by extensive patient education programs, is leading to higher diagnosis and treatment rates compared to other regions. The presence of well-established sleep clinics, research institutions, and specialized healthcare professionals is further strengthening the ecosystem for effective care delivery. In addition, favorable reimbursement policies and broad insurance coverage are making advanced devices like CPAP machines and oral appliances more accessible to patients. Key global players have their headquarters or major operations in North America, enabling faster innovations, product launches, and clinical trials.

Key Regional Takeaways:

United States Sleep Apnea Devices Market Analysis

The United States sleep apnea devices market, holding a share of 87%, is primarily driven by the growing public awareness initiatives led by healthcare providers and advocacy organizations. In accordance with this, the rapid integration of artificial intelligence (AI)-based analytics in diagnostic equipment is enabling real-time data interpretation and personalized treatment strategies, enhancing patient outcomes. Similarly, the expansion of insurance coverage and favorable reimbursement policies is improving access to diagnostic and therapeutic devices. The rise of remote monitoring platforms, which aid in facilitating sleep apnea care delivery in rural and underserved communities, is driving the market expansion. Additionally, the increasing prevalence of lifestyle-related conditions, such as obesity and hypertension, is catalyzing the demand for sleep apnea management. According to the CDC, from August 2021 to August 2023, 40.3% of adults in the United States were categorized as obese, showing no significant difference between genders. The highest obesity rates were found in adults aged 40–59, in contrast to those aged 20–39 or 60 and above. The numerous collaborations between primary care providers and sleep specialists are strengthening referral networks and fueling the market development. Furthermore, continual advancements in device comfort and usability, which improve patient adherence and therapy success, are impacting the market trends.

Europe Sleep Apnea Devices Market Analysis

The Europe sleep apnea devices market is experiencing growth due to the rising elderly population, which is more prone to sleep-related conditions. In line with this, increasing cases of diabetes and chronic respiratory illnesses contributing to higher rates of undiagnosed OSA are impelling the market growth. The International Diabetes Federation reported a 9.8% diabetes incidence in the EUR Region, affecting 66 Million people in 2024, with an anticipated 10% rise by 2050. The region also had the highest global number of type 1 diabetes cases, including 419,000 individuals under 20 years. Furthermore, increasing government-backed funding for sleep health programs across the EU is enhancing access to diagnostic services. Rising adoption of mobile health apps and wearable devices, which extend patient self-monitoring, is strengthening the market growth. Additionally, updated workplace safety mandates in the transportation and logistics sectors, encouraging regular sleep assessments, are fostering the market expansion. The growth of dedicated sleep clinics and multilingual telehealth platforms is further improving market accessibility.

Asia-Pacific Sleep Apnea Devices Market Analysis

The Asia-Pacific market is largely influenced by rising urbanization and lifestyle shifts that have led to an increased incidence of sleep-related disorders. An industry analysis revealed that in 2023, approximately 11% of Indian adults suffered from OSA, with 5% experiencing moderate-to-severe forms of the condition. The occurrence was significantly greater in cities, hitting as high as 19.5%, in contrast to reduced rates in rural areas. In addition to this, escalating air pollution across metropolitan areas is aggravating respiratory conditions, catalyzing the demand for sleep apnea diagnostics and treatment. Similarly, the expansion of private sleep clinics and the adoption of home-based testing services are improving access among middle-income populations. Likewise, the emergence of multilingual digital health platforms supporting higher treatment adherence across linguistically diverse regions is expanding the market scope.

Latin America Sleep Apnea Devices Market Analysis

The Latin America sleep apnea devices market is advancing due to increasing obesity rates, which are a major risk factor for OSA across several countries in the region. According to NCBI, as of July 2025, 57.5% of men and 62.6% of women were classified as overweight in Brazil, underscoring the growing concern about obesity as a significant public health challenge. Furthermore, the expansion of private healthcare infrastructure is improving access to diagnostic and therapeutic services. The growth in health insurance coverage across urban populations is also enabling more patients to seek timely evaluation and treatment for sleep disorders. Moreover, the ongoing educational initiatives by respiratory health organizations are enhancing physician training and public awareness, fostering early diagnosis and the implementation of effective treatment strategies.

Middle East and Africa Sleep Apnea Devices Market Analysis

The Middle East and Africa market is gaining traction due to the rising burden of non-communicable diseases, such as diabetes and hypertension, which are strongly associated with sleep apnea. According to an industry analysis, the MENA region had a hypertension prevalence rate of 26.2% in 2024. Similarly, increasing investments in healthcare infrastructure, especially in Gulf Cooperation Council (GCC) countries, and enhancing diagnostic capabilities are supporting the market development. The growing presence of international medical device manufacturers through distribution partnerships is improving product availability across the region. Apart from this, the ongoing shift towards telehealth and mobile health solutions is broadening the access to sleep apnea screening and follow-up care in remote and underserved areas.

Competitive Landscape:

Key players are investing heavily in research and working to expand the access to advanced treatment solutions. Leading companies continuously introduce improved CPAP machines, masks, and oral appliances that focus on comfort, portability, and digital connectivity to enhance patient compliance. Their strong distribution networks and partnerships with hospitals, sleep clinics, and healthcare providers ensure wide product availability and adoption. Through marketing campaigns and patient education initiatives, they are also generating awareness about sleep apnea and the benefits of timely treatment. Additionally, key players are collaborating with insurance providers to improve reimbursement frameworks, making therapies more affordable. By setting industry standards, spending on training programs, and exploring new markets, these companies are significantly shaping the market growth and strengthening the global sleep apnea devices landscape. For instance, in August 2024, Inspire Medical Systems gained FDA approval for its Inspire V neurostimulator designed for OSA. The implant boosted efficiency by shortening procedure duration and allowing firmware upgrades. The launch was scheduled for late 2024, followed by a complete rollout in 2025.

The report provides a comprehensive analysis of the competitive landscape in the sleep apnea devices market with detailed profiles of all major companies, including:

- BMC Medical Co.

- Braebon Medical Corporation

- Cadwell Laboratories Inc.

- CareFusion Corp.

- Curative Medical Inc.

- Devilbiss Healthcare

- Fisher & Paykel Healthcare

- GE Healthcare

- Invacare

- Oventus Medical

- Panthera Dental

- ResMed

- Somnomed Ltd.

- Vyaire Medical Inc.

- Whole You Inc.

Latest News and Developments:

- April 2025: Vivos Therapeutics entered into a final agreement to purchase The Sleep Center of Nevada, the largest sleep clinic operator in the state. The USD 9 Million agreement sought to improve access to Vivos’ FDA-approved oral appliance therapies for OSA, increasing patient reach, services, and revenue in the Las Vegas area.

- March 2025: Signifier Medical introduced an updated version of its eXciteOSA device, featuring a hardware remote, to comply with Medicare and Medicaid reimbursement standards. The update guaranteed wider accessibility for sleep apnea patients, preserving the device’s clinical efficacy and complying with CMS standards for durable medical equipment coverage.

- March 2025: Fisher & Paykel Healthcare unveiled the F&P Nova Nasal mask in New Zealand and Australia for treating OSA. The mask incorporated SwingFit headgear, a RollFit cushion, and a washable diffuser, ensuring comfort, silent operation, and a snug fit. Clinical trials demonstrated excellent results and high user satisfaction.

- January 2025: ResMed introduced the AirSense 11 CPAP machine in India to aid patients with OSA. It included personal therapy assistant, care check-in, and remote updates. It connected with the myAir and AirView platforms to enhance therapy adherence and patient tracking.

- September 2024: Apple launched sleep apnea alerts on Apple Watch and a hearing assistance capability in AirPods Pro 2. The updates featured tracking for Breathing Disturbances, a clinical-level hearing assessment, and Loud Sound Mitigation. These characteristics strive to enhance overall sleep and auditory well-being with extensive accessibility and safeguards for privacy.

Sleep Apnea Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| End Users Covered | Hospitals and Clinics, Sleep Laboratories, Homecare Settings, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | BMC Medical Co., Braebon Medical Corporation, Cadwell Laboratories, CareFusion Corp., Curative Medical, Devilbiss Healthcare, Fisher & Paykel Healthcare, GE Healthcare, Invacare, Oventus Medical, Panthera Dental, ResMed, Somnomed Ltd., Vyaire Medical Inc. and Whole You Inc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the sleep apnea devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global sleep apnea devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the sleep apnea devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Sleep Apnea Devices Market Report

The sleep apnea devices market was valued at USD 9.0 Billion in 2025.

The sleep apnea devices market is projected to exhibit a CAGR of 5.44% during 2026-2034, reaching a value of USD 14.5 Billion by 2034.

Rising awareness about the dangers linked to neglected sleep apnea, including cardiovascular complications, diabetes, and daytime fatigue, is encouraging more patients to seek medical help. Technological innovations are another major driver, with portable, quieter, and more comfortable devices improving user compliance and boosting adoption. Expanding sleep diagnostics, higher diagnosis rates, and physician referrals are also creating a steady patient pipeline.

North America currently dominates the sleep apnea devices market, accounting for a share of 49.2% in 2025, due to high disease prevalence linked to obesity, strong healthcare infrastructure, and broad insurance coverage. Widespread awareness, higher diagnosis rates, and the availability of advanced sleep clinics are fueling the market growth across the region.

Some of the major players in the sleep apnea devices market include BMC Medical Co., Braebon Medical Corporation, Cadwell Laboratories, CareFusion Corp., Curative Medical, Devilbiss Healthcare, Fisher & Paykel Healthcare, GE Healthcare, Invacare, Oventus Medical, Panthera Dental, ResMed, Somnomed Ltd., Vyaire Medical Inc., Whole You Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)