Simulation Software Market Size, Share, Trends and Forecast by Component, Deployment, End Use, and Region, 2025-2033

Simulation Software Market Size and Share:

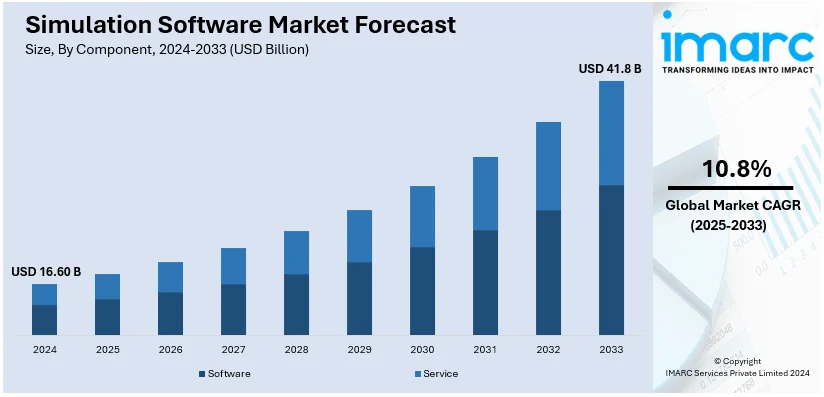

The global simulation software market size was valued at USD 16.60 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 41.8 Billion by 2033, exhibiting a CAGR of 10.8% during 2025-2033. North America currently dominates the market, holding a significant market share of over 35.8% in 2024. The market is primarily driven by the increasing demand for efficient software solutions, the growing need to minimize production expenses and training costs, rising focus on operational optimization and decision-making procedures, and stringent safety and environmental regulations.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 16.60 Billion |

|

Market Forecast in 2033

|

USD 41.8 Billion |

| Market Growth Rate (2025-2033) | 10.8% |

The global market is majorly driven by the increasing adoption of digital twins and advanced technologies such as Artificial Intelligence (AI) and the Internet of Things (IoT). Industries such as automotive, aerospace, healthcare, and manufacturing utilize simulation tools to optimize processes, reduce costs, and enhance product development cycles. The rising demand for predictive analysis to improve efficiency and mitigate risks is also fueling market growth. Furthermore, the growing emphasis on virtual testing, driven by the need to minimize physical prototyping, is accelerating the adoption of simulation software. Advances in cloud-based solutions and increasing investments in research and development further contribute to the market’s expansion, enabling businesses to achieve faster and more accurate results. On 12th February 2024, Cadence Design Systems, Inc. announced, at the 3DEXPERIENCE World, an extension of its strategic partnership with Dassault Systèmes to deploy AI-driven CadenceOrCAD X and Allegro X in combination with Dassault Systèmes' 3DEXPERIENCE Works portfolio for the SOLIDWORKS ecosystem. The cloud-enabled offering extends collaboration from PCB/3D mechanical design up to simulation, offering a cut in design turnaround time down to 5X. This seamless, scalable solution accelerates the development of the end-to-end mechatronics system, enhancing business performance, reliability, manufacturability, and cost for startups to enterprise-scale businesses.

The United States stands out as a key regional market, primarily driven by rapid technological advancements and the growing integration of simulation tools across diverse industries such as defense, energy, and logistics. Increasing demand for enhanced operational efficiency, particularly in high-stakes sectors such as aerospace and military, is propelling the adoption of simulation solutions for training, testing, and performance optimization. Additionally, the rise of smart manufacturing and Industry 4.0 initiatives is fueling the use of simulation software to streamline processes and improve productivity. The expanding application of simulation tools in autonomous systems, including self-driving vehicles and robotics, further supports market growth. Moreover, government investments in digital transformation and R&D initiatives continue to accelerate the adoption of simulation technologies across the U.S. market.

Simulation Software Market Trends:

Increasing Product Adoption in Optimization of Electric Vehicles

One of the most important market drivers is the growing use of simulation software to improve the performance of electric and driverless vehicles. This trend is further fueled by the rising adoption of autonomous and electric vehicles. As per an International Energy Agency (IEA) report, by 2020, the number of electric cars on roads worldwide had surpassed 10 million. Advanced simulation tools are becoming increasingly important as the automobile industry moves toward electric and autonomous technologies to enhance vehicle performance, safety, and design. Key players are adopting simulation software to simulate numerous scenarios, including test functionalities and safety of electric vehicles.

Rising Adoption of Simulation Tools in Aerospace and Defense Industries

Simulation technologies are being extensively used by the aerospace and defense industry and other industries to improve decision-making and operational efficiency. Governments across the globe are investing heavily in their defense and aerospace sectors, for instance, in accordance with the restrictions enacted by Congress under the Financial Responsibility Act (FRA) of 2023, the Biden-Harris Administration sent a planned Fiscal Year (FY) 2025 budget proposal of USD 849.8 Billion for the Department of Defense (DoD) to Congress on March 11, 2024. The demand for reduced risk, cost-effectiveness, and enhanced performance is what is driving its adoption.

Increasing Potential for Simulation-Assisted Digital Twins

Another major driver of the simulation software market is the development of digital twins supported by simulation. For instance, with the use of real-time sensor inputs, engineers can construct digital twins of physical assets using the simulation-based software program of Ansys Digital Twin. The behavior and experience of the real assets are mirrored in these virtual representations, or "digital twins," which enable predictive maintenance, operational optimization, and enhanced product performance. Businesses can build virtual copies of real assets or processes using digital twins, which are made possible by simulation software. This allows for real-time optimization, monitoring, and analysis. The potential for predictive maintenance, performance optimization, and operational efficiency is enormous with this technology. Companies are using digital twins to increase overall operational effectiveness, influence innovation, and improve decision-making.

Simulation Software Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global simulation software market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on component, deployment, and end use.

Analysis by Component:

- Software

- Service

Software leads the market with around 70.2% of market share in 2024. Software is essential to allow simulation capabilities across a wide range of industries, thus making the largest portion of the simulation software market. The foundation of simulation tools is software, which offers the user interfaces, modeling capabilities, and algorithms required to efficiently build, run, and analyze simulations. The growing use of simulation software for R&D, operational optimization, and product design highlights the role that software plays in propelling the development and functionality of simulation tools, making it the most important and largest market category. One simulation software company that has updated and improved its software to enhance functionality and meet user demands is Dassault Systems, known widely for its CATIA software suite.

Analysis by Deployment:

- On-premises

- Cloud-based

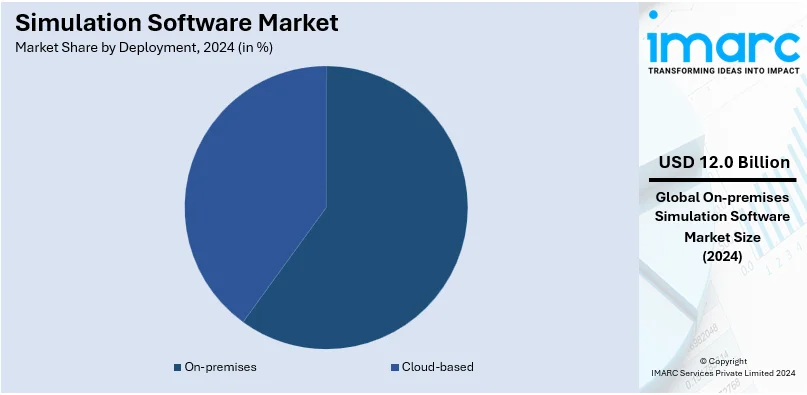

On-premises lead the market with around 72.5% of market share in 2024 due to its superior data control, security, and customization capabilities. Organizations, particularly in industries such as aerospace, defense, and manufacturing, prefer on-premises solutions to safeguard sensitive data and meet compliance requirements. This deployment model offers high performance and reliability for complex simulations, making it ideal for enterprises that require extensive computing power and minimal latency. Additionally, companies with legacy systems often choose on-premises setups to seamlessly integrate with existing infrastructure, ensuring consistent performance.

Analysis by End Use:

- Automotive

- Aerospace and Defense

- Electrical and Electronics

- Industrial Manufacturing

- Healthcare

- Others

Automotive leads the market in 2024. To meet consumer demands for high-performance and creative automobiles while maintaining compliance with strict laws, automotive firms rely extensively on simulation software to improve the safety, efficiency, and reliability of their vehicles. As per the INDIA BRAND EQUITY FOUNDATION (IBEF), the automotive industry in developing nations such as India is growing at a considerable rate, thereby posing a positive future for simulation software market. In November 2023, the total passenger vehicles manufactured in India was 2.22 million units. The ongoing emphasis of the industry on R&D and the requirement for quick technical breakthroughs help to reinforce its position as the market leader for simulation software.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 35.8%. The market for simulation software is dominated by North America for several important reasons. The superior technological infrastructure of the region, the widespread use of simulation tools in industries such as aerospace, automotive, and healthcare, and the substantial investments made in research and development are the reasons behind its strong position. The dominant position of North America in the simulation software industry is further supported by the presence of numerous key players in the region. Altair Engineering Inc., Dassault Systemes, Autodesk, Inc., and ANSYS, Inc. are a few of the major North American players. These businesses are at the forefront of innovation, providing state-of-the-art simulation solutions that meet a variety of industrial demands and stimulate regional market expansion.

Key Regional Takeaways:

United States Simulation Software Market Analysis

In 2024, the US accounted for around 89.20% of the total North America simulation software market. The U.S. market for simulation software is continuously growing due to innovation happening in defense, automotive healthcare, and other sectors. The Congressional Budget Office, for instance, reported USD 820.3 Billion in the defense budget allocated for 2023 to include huge portions of that budget to enhance military preparedness, training, and cost efficiency through simulation. The automotive industry is increasingly using simulation software for designing and testing autonomous vehicles, which form part of a global market worth USD 100 billion in 2023. Healthcare applications, including surgical training, treatment planning, and medical device testing, are also important growth drivers. Market leaders include Ansys and MathWorks, which have the most advanced solutions. Government funding for R&D, along with the development of cloud-based simulation platforms, has increased adoption across industries. Companies based in the United States are also entering international markets, using their technological prowess to capitalize on the growing global demand, which further cements the country's position as a leader in simulation technology.

Europe Simulation Software Market Analysis

Europe's simulation software market is on the growth path due to huge investments in industrial R&D, defense modernization, and renewable energy projects. According to Eurostat, the region's industrial R&D spending reached EURO 352 Billion (USD 369.68 Billion) in 2022, thereby fueling innovation in simulation tools for the manufacturing and energy sectors. Germany's USD 107.2 Billion defense modernization fund announced in 2022 focuses on simulation technologies for training and operational planning. Offshore wind farms, and renewable energy projects, are highly dependent on simulation software for effective design and optimization. The automobile industry also employs the same in the testing and production improvement of vehicles. Siemens Digital Industries Software is the leader in technological advancements, especially in smart manufacturing. EU sustainability regulations promote green simulation technologies, fostering eco-friendly solutions. Government-funded R&D programs in the European region, such as those conducted in France and the UK, guarantee Europe's top spot in simulation software development. The region can then easily compete globally.

Asia Pacific Simulation Software Market Analysis

Asia Pacific's simulation software market is growing rapidly in defense, manufacturing, and education. As per the Chinese Ministry of Finance, China has allocated USD 230 Billion for its defense budget in 2022 and is emphasizing simulation technologies in military training and testing advanced equipment. India, with a defence budget of USD 72.6 Billion for 2023-2024, places importance on locally developed simulation tools as part of the "Make in India" initiative. In manufacturing, Japan and South Korea utilize simulation for robotics, smart factories, and process optimization. Even the education sector is using simulation-based platforms, mainly in areas including STEM learning and virtual labs. The collaboration of global leaders such as Dassault Systèmes with regional firms creates opportunities for innovation and technology transfer. Increased government support for simulation R&D and the focus by the region on industrial digitization place Asia Pacific in the rising leader position regarding the adoption of simulation software across the globe and the technological development for it.

Latin America Simulation Software Market Analysis

Latin America's simulation software market is diversifying in applications in defense, automotive, education, and industrial sectors. According to an industry report, Brazil's defense budget in 2022 was USD 21.8 Billion, with growing investments in simulation technologies to modernize military training and equipment testing. Automotive simulation tools are used to optimize the production process and to design new models, backed by liberalized trade policies in the region. Countries such as Mexico are embracing simulation-based platforms such as virtual labs and STEM learning tools to improve educational outcomes. The local companies have collaborations with international players for technology transfer and innovation that enhances the simulation capabilities. Cloud-based simulation solutions are on the rise due to their cost-effectiveness and scalability. Brazil is at the top of the regional market, with government-backed R&D initiatives, focusing on local development and export opportunities, making it a hub for simulation software innovation in Latin America.

Middle East and Africa Simulation Software Market Analysis

Simulation software in the Middle East and Africa is now growing in its adoption across the defense, energy, healthcare, and industrial sectors. In 2022, the International Trade Administration reported that Saudi Arabia has allocated USD 75 Billion to its defense budget and invested in simulation technologies in the military's training and planning operations. Simulation tools have now been used in Africa across the mining and agricultural industries for greater productivity and risks reduction. South Africa is another remarkable user of simulation technologies in renewable energy projects, through the incentives provided by the government toward green and sustainable solutions. Healthcare providers within this region are now making good use of simulation tools to aid in surgical planning, diagnostics, and medical training. Collaboration among global and local companies enables technology transfer and skills building; smart city and infrastructure projects generate supplementary demand. These advancements position the Middle East and Africa as emerging market for simulation software, with diverse applications that drive growth.

Competitive Landscape:

Major simulation software firms including Siemens AG, ANSYS Inc., Dassault Systemes, Autodesk Inc., and Altair Engineering Inc. are aggressively growing the range of solutions they offer to improve their standing in the business. To improve the functionality of their platforms, these industry giants are investing in cutting-edge technologies such as artificial intelligence (AI), machine learning, cloud computing, virtual reality, and augmented reality. Through the implementation of tactics including joint ventures, alliances, mergers, and acquisitions, these businesses are growing their market share and meeting the changing demands of different sectors. Siemens, for instance, has been modeling factories for businesses such as Electrolux in order to improve operational efficiency.

The report provides a comprehensive analysis of the competitive landscape in the simulation software market with detailed profiles of all major companies, including:

- Altair Engineering Inc.

- Ansys Inc.

- Autodesk Inc.

- Bentley Systems Incorporated

- Dassault Systèmes

- PTC Inc.

- Rockwell Automation Inc.

- Siemens AG

- Simul8 Corporation

- The AnyLogic Company

- The MathWorks Inc.

Latest News and Developments:

- December 2024: The SimScale and PTC partnership gives free, three-month access to the SimScale cloud-native simulation platform to start-ups. Collaboration through PTC's Onshape Start-Up Program means entrepreneurs can now analyze and optimize CAD designs much more rapidly to improve product innovation and faster market launches.

- November 2024: Siemens announced the acquisition of Altair Engineering for USD 10 billion to advance its industrial software and AI portfolio. This strategic acquisition, providing USD 113 per share for Altair shareholders, further consolidates Siemens' leadership in AI-powered design and simulation as Altair's capabilities in simulation, HPC, and data science merge with Siemens' Xcelerator.

- October 2024: Autodesk announced that they have signed an agreement to acquire FlexSim, a provider of factory and logistics simulation technology. The acquisition is expected to enhance Autodesk's factory design tools with simulation capabilities that will optimize production flow, improve operational efficiency, and enable better decision-making. With the acquisition, FlexSim's technology will integrate with Autodesk's cloud-connected solutions to make more precise factory planning possible and avoid costly mistakes.

- April 2024: ANSYS Optics enhances simulation capabilities for optics and photonics designers. The update introduces advanced features for efficient multiscale optics simulation and analysis, such as metalens simulation, optimized straylight analysis, and seamless integration with other Ansys products.

- Feb 2024: Dassault Systemes announced its collaboration with BMW Group to establish vehicle development programs with increased efficiency. The outcome of this collaboration was the creation of a process-oriented, industry-ready stamping die design and stamped sheet metal component definition solution.

Simulation Software Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Service |

| Deployments Covered | On-Premises, Cloud-Based |

| End Uses Covered | Automotive, Aerospace and Defense, Electrical and Electronics, Industrial Manufacturing, Healthcare, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Altair Engineering Inc., Ansys Inc., Autodesk Inc., Bentley Systems Incorporated, Dassault Systèmes, PTC Inc., Rockwell Automation Inc., Siemens AG, Simul8 Corporation, The AnyLogic Company, The MathWorks Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the simulation software market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global simulation software market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the simulation software industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

Simulation software is a tool that allows users to model real-world processes, systems, or environments in a virtual space. It enables testing, analysis, and optimization of various scenarios to improve efficiency, reduce costs, and minimize risks across industries including automotive, aerospace, and healthcare.

The simulation software market was valued at USD 16.60 Billion in 2024.

IMARC estimates the global simulation software market to exhibit a CAGR of 10.8% during 2025-2033.

The market is driven by the growing adoption of digital twins, integration of AI and IoT, rising demand for predictive analysis, need to minimize production costs and physical prototyping, and increasing focus on operational optimization across industries such as automotive, aerospace, and healthcare.

Software represented the largest segment by component, driven by its critical role in enabling modeling, analysis, and optimization across various industries.

On-premises lead the market by deployment due to its preference among large enterprises requiring direct control over data, infrastructure, and stringent security compliance.

The automotive segment is the leading segment by end-use, driven by the growing need to optimize vehicle safety, performance, and design amid the rising adoption of electric and autonomous vehicles.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein North America currently dominates the market.

Some of the major players in the global simulation software market include Altair Engineering Inc., Ansys Inc., Autodesk Inc., Bentley Systems Incorporated, Dassault Systèmes, PTC Inc., Rockwell Automation Inc., Siemens AG, Simul8 Corporation, The AnyLogic Company, and The MathWorks Inc., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)