Silicon Wafer Market Size, Share, Trends and Forecast by Wafer Size, Type, Application, End Use, and Region, 2026-2034

Silicon Wafer Market Size and Share:

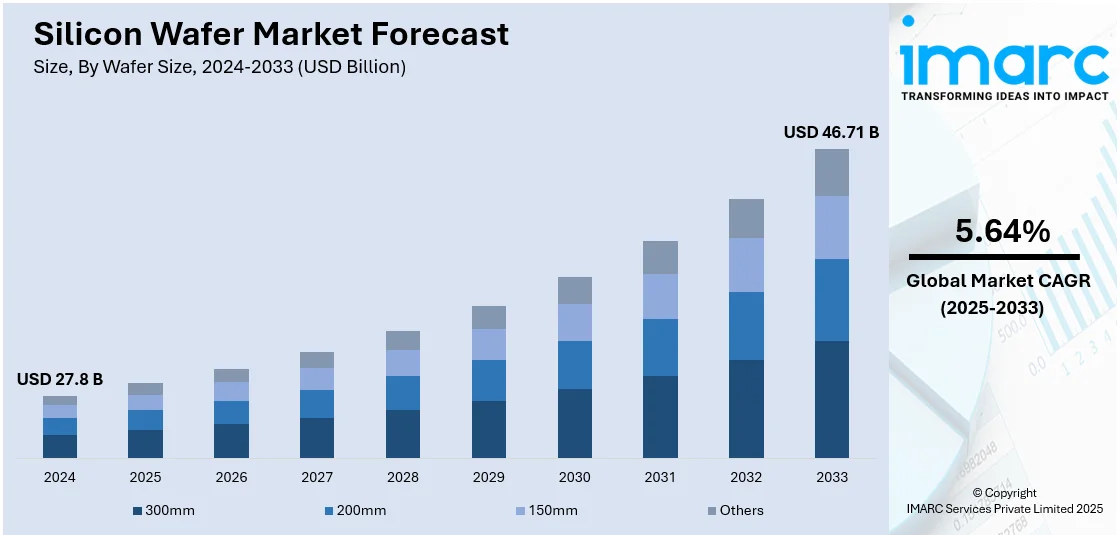

The global silicon wafer market size was valued at USD 27.8 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 46.71 Billion by 2034, exhibiting a CAGR of 5.64% during 2026-2034. Asia Pacific dominated the market, accounting for a share of 68.5% in 2024. The growing environmental concerns about high carbon emissions from fuel-based power plants, the rising installation of solar power plants, and the increasing demand for wireless computing devices represent some of the key factors driving the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 27.8 Billion |

|

Market Forecast in 2034

|

USD 46.71 Billion |

| Market Growth Rate 2026-2034 | 5.64% |

The market is primarily driven by the growing demand for consumer electronics, especially smartphones, laptops, and tablets, which rely on advanced semiconductor chips. The expansion of 5G infrastructure, rising adoption of electric vehicles (EVs), and increased use of Internet of Things (IoT) devices are accelerating the need for more compact and efficient integrated circuits. Rapid advancements in artificial intelligence (AI) and data centers also push demand for high-performance processors and memory chips, boosting silicon wafer consumption. Additionally, the shift toward automation in manufacturing and increased investments in semiconductor fabrication facilities contribute to silicon wafer market growth. The trend toward smaller node technologies in chip design is increasing the usage of larger diameter wafers, further supporting volume growth and economies of scale in wafer production. These factors together are shaping the market’s upward trajectory.

In the United States, growing investments are targeting capacity expansion and technological upgrades in silicon wafer manufacturing to support surging semiconductor demand. The focus is on scaling domestic production and enhancing service capabilities, driven by rising applications in AI, electric vehicles, and high-performance computing, highlighting the strategic importance of silicon wafers in advanced electronics. For instance, in November 2024, ZMC acquired a controlling interest in Pure Wafer, a major U.S.-based provider of silicon wafer solutions and services. The investment aims to expand Pure Wafer's capacity and advance its technology to meet growing semiconductor industry demands.

Silicon Wafer Market Trends:

Expanding Use of GPS Tracking Systems

GPS tracking systems rely on GPS receiver chips, which are semiconductor devices manufactured on silicon wafers. The growing adoption of GPS tracking systems across various industries, including transportation, logistics, personal tracking, and sports, is acting as a significant growth-inducing factor. For instance, according to an article published by Lowry Solutions, the widespread implementation of global positioning system (GPS) technology revolutionized the transportation industry. Moreover, the global GPS tracking device market is expected to reach USD 7.80 Billion by 2032, growing at a CAGR of 11.4% during 2024-2032, as per a report by the IMARC Group. As a satellite navigation system, GPS delivers real-time location information upon request and enables the tracking of object movements. The logistics industry can benefit greatly from utilizing GPS tracking software, which includes RFID tracking devices, since it offers numerous advantages. It makes it easier to locate the car on a map, which improves customer satisfaction and operational effectiveness. This, in turn, leads to increased demand for silicon wafers used in the fabrication of these chips. Moreover, the development of more advanced GPS tracking systems requires higher-performance GPS chips with improved accuracy, sensitivity, and power efficiency. Semiconductor manufacturers are continuously innovating and developing new chip designs that utilize advanced manufacturing processes and materials. This drives the demand for specialized silicon wafers capable of meeting the stringent requirements of modern GPS chips. For instance, in January 2024, Nordic Semiconductor introduced a pre-certified development kit and system-in-package (SiP) chip, nRF9161, intended to power 5G non-cellular and cellular IoT technologies. Additionally, it exhibits excellent position tracking, a long battery life, and robust connectivity. It can also connect to LTE-M, NB-IoT, as well as DECT NR+ networks and provides assistance via the Nordic Developer Academy and their nRF Connect SDK. These innovations are expected to escalate the silicon wafer market demand over the forecasted period.

Rising Demand for Semiconductors

Based on the silicon wafer market forecast, the proliferation of smartphones, tablets, laptops, smartwatches, and other consumer electronic devices drives significant demand for semiconductor devices. For instance, according to Statista, the sales for consumer electronics are anticipated to reach approximately 9,014 million pieces by 2028. Moreover, global smartphone mobile network subscriptions accounted for 7 billion in 2023 and are expected to surpass roughly 7.7 billion by 2028. These devices rely heavily on various semiconductor components, such as microprocessors, memory chips, sensors, and connectivity chips, all of which are manufactured on silicon wafers. Apart from this, the growing applications of new technologies, including 5G, IoT, and artificial intelligence, by silicon wafer manufacturers are inflating the need for a diverse range of semiconductor devices. For instance, in March 2024, Cerebras Systems launched Wafer Scale Engine 3 (WSE-3), a revolutionary AI wafer-scale chip alternative to the WSE-2. The device is equipped with four trillion transistors created using TSMS's 5nm-class fabrication method, 44GB of on-chip SRAM, a peak performance of 125 FP16 PetaFLOPS, etc. Cebera’s WSE-3 can be utilized to train some of the industry's most powerful AI models. Besides this, government bodies and companies worldwide are investing extensively in semiconductor manufacturing to enhance domestic capabilities, promote innovation, and address supply chain vulnerabilities. For instance, in March 2024, the government in India approved an investment of about Rs 91,000 Crore to set up the country's first commercial semiconductor fabrication plant or fab unit by a joint venture between Tata Electronics and Taiwan's Powerchip Semiconductor Manufacturing Corp at Dholera in Gujarat. These investments will continue to elevate the adoption of silicon wafers over the foreseeable future.

Applications in Automotive Industry

The rising demand for silicon wafers in the automotive industry is one of the key factors adding to the market growth. The transition toward electric vehicles and the development of autonomous driving technology require advanced semiconductor components. According to the International Energy Agency, approximately 14 million electric cars were sold in 2023, recording an increase of 35% in comparison to the previous year. Silicon wafers are essential for manufacturing the semiconductor devices used in electric vehicle powertrains, battery management systems, sensor arrays, and onboard computing systems for autonomous driving. For instance, according to an article published by Wafer World, the production of integrated circuits (ICs) for ADAS components, including cameras, LiDAR systems, and radar sensors, depends heavily on silicon wafers. These parts allow functions that make electric vehicles safer and more appealing to buyers, like autonomous emergency braking, adaptive cruise control, lane-keeping assistance, and pedestrian recognition. Apart from this, regulatory authorities around the world are implementing various regulations to boost the production and adoption of electric vehicles (EVs), which further drives the demand for silicon wafers used in EV components. In addition, they also offer subsidies, loans, tax credits, or rebates to manufacturers, which positively influence the silicon wafer price trends. For instance, in February 2024, the U.S. Department of Energy’s (DOE) Loan Programs Office (LPO) announced a conditional commitment to SK Siltron CSS, LLC for an approximately USD 544 Million loan to expand manufacturing of high-quality silicon carbide (SiC) wafers for electric vehicle (EV) power electronics in the U.S.

Silicon Wafer Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global silicon wafer market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on wafer size, type, application, and end use.

Analysis by Wafer Size:

- 300mm

- 200mm

- 100mm

- Others

300mm stands as the largest component in 2024, holding around 68.3% of the market. According to the silicon wafer market statistics, driven by the increasing demand for higher-performance semiconductors, which are essential for industries like electronics, automotive, and consumer goods. The 300mm wafers enable manufacturers to produce more chips per wafer, resulting in improved cost-efficiency and higher yields. Technological advancements in fabrication processes further support the growth of 300mm wafers, as they are compatible with the latest generation of integrated circuits and advanced packaging technologies. In April 2024, Renesas Electronics Corporation started its 300mm wafer fab for power semiconductors operations at its Kofu Factory, located in Kai City, Japan.

Analysis by Type:

- P-type

- N-type

P-type leads the market with around 57.1% of the silicon wafer market share in 2024. P-type silicon wafers serve as the substrate for manufacturing integrated circuits (ICs). Additionally, these ICs are fundamental components in electronic devices, such as smartphones, computers, automotive electronics, etc. P-type wafers also provide the foundation for creating the necessary circuitry on the semiconductor material. The adoption of technologies, including electric vehicles (EVs), autonomous driving systems, and advanced driver assistance systems (ADAS), that rely on semiconductor components is bolstering the segment's growth. For instance, in March 2024, Imperial Solar Star, one of the solar manufacturers based in Cambodia, launched a P-type silicon wafer manufacturing plant.

Analysis by Application:

- Integrated Circuits

- Solar Cells

- Others

Integrated circuits led the market with around 50.1% of the market share in 2024 due to their crucial role in modern electronic devices. As the demand for electronics like smartphones, computers, and consumer appliances increases, ICs are central to powering these technologies. Silicon wafers serve as the foundation for IC production, and their versatility in producing high-performance chips makes them indispensable. The rise of emerging technologies such as artificial intelligence, 5G, and the Internet of Things further drives the need for advanced ICs, which in turn boosts the demand for silicon wafers.

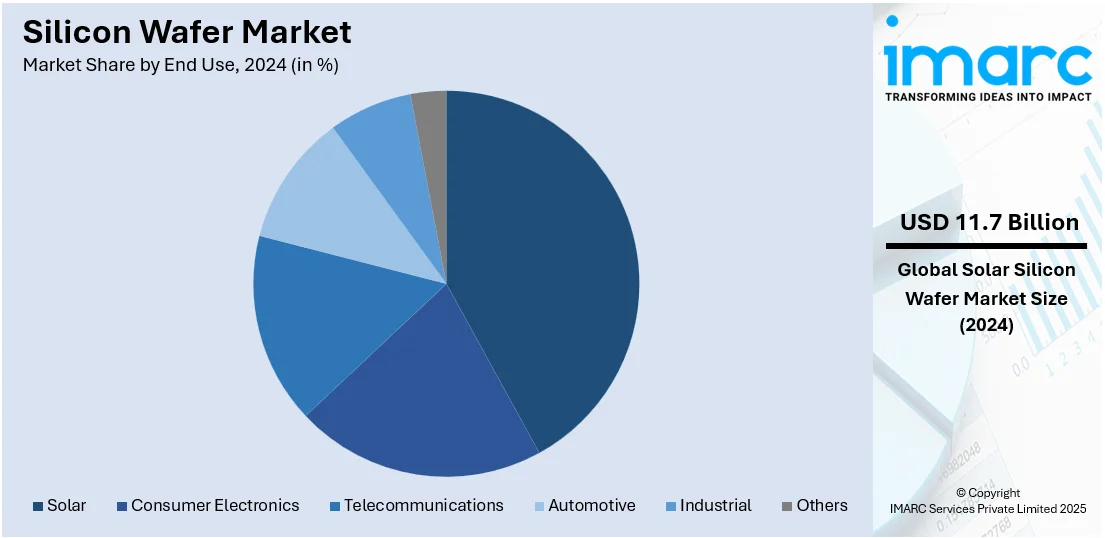

Analysis by End Use:

- Solar

- Consumer Electronics

- Telecommunications

- Automotive

- Industrial

- Others

Solar leads the market with around 42.1% of the market share in 2024 due to the growing demand for renewable energy solutions. Silicon wafers are essential in the production of photovoltaic (PV) cells, which are the core components of solar panels. As global efforts to reduce carbon emissions intensify, the adoption of solar energy has surged, boosting the demand for high-quality silicon wafers. Technological advancements in solar cell efficiency and the scaling up of solar power installations worldwide further amplify this demand.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, Asia Pacific accounted for the largest silicon wafer market share of over 68.5%. According to the silicon wafer market outlook, the Asia Pacific region has been witnessing rapid industrialization and urbanization. This has led to an increased demand for electronic devices, semiconductors, and photovoltaic products. Moreover, the rising number of semiconductor manufacturing facilities and suppliers is also acting as another significant growth-inducing factor. For example, in February 2024, the Union Cabinet, chaired by the Prime Minister of India, approved the establishment of three semiconductor units under the Development of Semiconductors and Display Manufacturing Ecosystems in India. With the widespread adoption of advanced technologies, such as 5G, the Internet of Things (IoT), artificial intelligence (AI), and automotive electronics, there is a growing requirement for silicon wafers to produce integrated circuits, memory chips, sensors, and other semiconductor devices. For instance, in April 2024, Gstar launched the construction of a new silicon wafer facility in Jakarta, Indonesia, to drive technological innovation in the development of large-sized, thin-film, and fine-line silicon wafers.

Key Regional Takeaways:

United States Silicon Wafer Market Analysis

In 2024, the United States accounted for 84.4% of the market share in North America. The United States silicon wafer market is primarily driven by the growing demand for semiconductor devices across various industries such as electronics, automotive, telecommunications, and consumer goods. The increasing adoption of technologies such as artificial intelligence (AI) and the Internet of Things (IoT) has also significantly boosted the need for advanced semiconductors, which, in turn, fuels the demand for high-quality silicon wafers. Furthermore, the ongoing shift toward electric vehicles (EVs) and renewable energy systems, which require sophisticated power electronics, is significantly propelling industry expansion. According to recent industry reports, it is estimated that nearly 10% of the vehicles on American roads will be electric by 2030, equating to about 26.4 million EVs. Additionally, government initiatives aimed at strengthening domestic semiconductor production, such as the CHIPS Act, which provides incentives for U.S.-based semiconductor manufacturing, are expected to further enhance market development. Technological advancements in wafer production, including the development of larger-diameter wafers and the improvement of wafer-slicing techniques, are also contributing to industry expansion. Moreover, the increasing reliance on smartphones, computers, and consumer electronics, all of which depend on silicon-based components, continues to drive demand. As the global supply chain for semiconductors becomes more localized, the U.S. market is poised to see further growth.

Asia Pacific Silicon Wafer Market Analysis

The Asia Pacific silicon wafer market is expanding due to the region’s increasing integration of advanced manufacturing techniques and automation in industries such as automotive, consumer electronics, and telecommunications. As automation and robotics become more prevalent, there is a rising demand for semiconductors that are essential for these technologies. For instance, in 2023, Asia accounted for 70% of all newly installed robots worldwide, as per the International Federation of Robotics (IFR). The robust expansion of the electric vehicle (EV) market in countries such as China and Japan is further boosting the demand for silicon wafers, as EVs rely heavily on power electronics. Additionally, the shift toward a more sustainable economy is also contributing to the growth of renewable energy solutions, which rely on advanced power management semiconductors made from silicon wafers. These factors, combined with the region's strategic supply chain and manufacturing dominance, continue to drive the market forward.

Europe Silicon Wafer Market Analysis

The Europe silicon wafer market is experiencing growth, fueled by the increasing demand for high-performance chips used in various applications such as automotive, medical devices, and renewable energy. One key driver is the shift toward the electrification of transportation, where silicon wafers are integral to power management systems in electric vehicles (EVs) and charging infrastructure. Moreover, Europe’s strong commitment to sustainability and its goal to reduce carbon emissions has led to a higher demand for energy-efficient semiconductor devices, particularly in the context of smart grids and solar energy systems. The expansion of data centers and the growing need for energy-efficient devices in consumer electronics also contribute to industry expansion. According to a report published by the IMARC Group, the Europe data center market size is forecasted to grow at a CAGR of 9.23% during 2025-2033. Additionally, the rising trend of miniaturization in electronic devices is also contributing to the need for advanced silicon wafer technologies, as smaller and more efficient wafers are required for compact gadgets and wearables. The increasing focus on developing semiconductor fabrication capabilities within Europe, bolstered by public and private investments, is also helping to meet the region’s demand and reduce reliance on external suppliers, thus supporting the expansion of the silicon wafer market in Europe.

Latin America Silicon Wafer Market Analysis

The Latin America silicon wafer market is significantly influenced by the region’s expanding manufacturing and electronics industries. The rise in local production of consumer electronics, including smartphones, laptops, and wearables, is driving the demand for silicon wafers used in chips and processors. Additionally, the expansion of telecommunications infrastructure, particularly with the rollout of 5G networks, is increasing the demand for advanced semiconductors. As per recent industry reports, in Q3 2024, the number of 5G network connections in Latin America reached 67 million, recording a growth rate of 19%. Additionally, numerous governments in the region are promoting the development of the semiconductor industry through investments and incentives, supporting local manufacturing and reducing dependency on imports, which is further stimulating the Latin American silicon wafer market.

Middle East and Africa Silicon Wafer Market Analysis

The Middle East and Africa silicon wafer market is being propelled by growing investments in infrastructure and technology development across the region. As countries like the UAE and Saudi Arabia focus on diversifying their economies through digital transformation and smart cities, the demand for semiconductors, including silicon wafers, is rising. For instance, according to the IMARC Group, the Saudi Arabia smart cities market is expected to grow at a CAGR of 9.2% during 2025-2033. Additionally, increasing initiatives in renewable energy, particularly solar power, demand efficient power management systems, driving the need for advanced semiconductor components. As such, the Middle East renewable energy market is projected to grow at a CAGR of 13.53% during 2024-2032. Government-backed projects and investments in technology innovation hubs, stimulating the semiconductor industry in the region, are also among the significant silicon wafer market trends.

Competitive Landscape:

Government initiatives, particularly in the form of subsidies and funding to bolster domestic semiconductor manufacturing, have become increasingly common. These efforts aim to strengthen supply chains and reduce reliance on foreign production. For instance, in December 2024, In December 2024, the U.S. finalized USD 406 Million in subsidies for GlobalWafers to enhance silicon wafer production, supporting nearly USD 4 Billion in investments and creating approximately 2,580 jobs. The report provides a comprehensive analysis of the competitive landscape in the silicon wafer market with detailed profiles of all major companies, including:

- GlobalWafers Singapore Pte. Ltd.

- Okmetic Oy

- Shanghai Simgui Technology Co. Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Silicon Materials, Inc.

- Siltronic AG

- SK Siltron Co., Ltd.

- Sumco Corporation

- Tokuyama Corporation

- Virginia Semiconductor, Inc.

- Wafer Works Corporation

Latest News and Developments:

- October 2024: Infineon Technologies unveiled the thinnest silicon power wafer ever developed, which is only 20 micrometers thick and has a diameter of 300 millimeters. The silicon wafers, which are just half the thickness of the most recent generation of wafers, are a revolutionary breakthrough in the semiconductor industry.

- September 2024: Mitsubishi Electric Corporation announced that the Fukuyama Factory of its Power Device Works started producing power semiconductor chips on an immense scale using 12-inch silicon wafers. These devices will be used in semiconductor module assembly.

- September 2024: Polymatech, a global leader in the semiconductor industry, signed a Memorandum of Understanding (MoU) with ECM Group for the establishment of a joint venture company in France. The facility will focus on the production of silicon wafers, silicon carbide, and sapphire wafers.

- April 2024: Gstar began the construction of its silicon wafer and silicon rod factory in Jakarta, Indonesia. Spanning 60,000 square meters, the factory will incorporate cutting-edge machinery and technology with completely digital and autonomous manufacturing methods.

- June 2024: Canon developed chipmaking equipment that stamps designs onto silicon wafers.

- April 2024: LONGi launched its novel Tairay silicon wafers for solar technologies, including back contact cells (BC), heterojunction (HJT), and TOPCon.

- March 2024: Imperial Solar Star, a solar manufacturer based in Cambodia, introduced a silicon wafer manufacturing plant catering to p-type.

Silicon Wafer Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Wafer Sizes Covered | 300mm, 200mm, 150mm, Others |

| Types Covered | P-type, N-type |

| Applications Covered | Integrated Circuits, Solar Cells, Others |

| End Uses Covered | Solar, Consumer Electronics, Telecommunications, Automotive, Industrial, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | GlobalWafers Singapore Pte. Ltd, Okmetic Oy, Shanghai Simgui Technology Co. Ltd., Shin-Etsu Chemical Co., Ltd, Silicon Materials Inc, Siltronic AG, SK Siltron Co., Ltd., Sumco Corporation, Tokuyama Corporation., Virginia Semiconductor, Inc., Wafer Works Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the silicon wafer market from 2020-2034.

- The silicon wafer market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the silicon wafer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The silicon wafer market was valued at USD 27.8 Billion in 2024.

The silicon wafer market is projected to exhibit a CAGR of 5.64% during 2025-2033, reaching a value of USD 46.71 Billion by 2033.

Key factors driving the silicon wafer market include rising semiconductor demand, growth in consumer electronics, advancements in AI and 5G technologies, increasing automotive electronics usage, and expansion of data centers. Additionally, trends in miniaturization, chip performance improvements, and investments in fabs and foundries further support market growth.

Asia Pacific currently dominates the silicon wafer market, accounting for a share of 68.5% in 2024 due to strong semiconductor manufacturing, technological advancements, robust demand from electronics and automotive industries, and favorable government initiatives promoting innovation.

Global Wafers Singapore Pte. Ltd, Okmetic Oy, Shanghai Simgui Technology Co. Ltd., Shin-Etsu Chemical Co., Ltd, Silicon Materials Inc, Siltronic AG, SK Siltron Co., Ltd., Sumco Corporation, Tokuyama Corporation., Virginia Semiconductor, Inc., Wafer Works Corporation, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)