Silicon on Insulator Market Report by Wafer Size (300 mm, 200 mm), Wafer Type (FD-SOI, RF-SOI, PD-SOI, and Others), Technology (Smart Cut, BESOI, SiMOX, ELTRAN, SoS), Product (RF FEM Products, MEMS Devices, Power Products, Optical Communication, Image Sensing), Application (Consumer Electronics, Automotive, Datacom and Telecom, Industrial, Photonics, and Others), and Region 2026-2034

Silicon on Insulator Market Size, Share & Growth

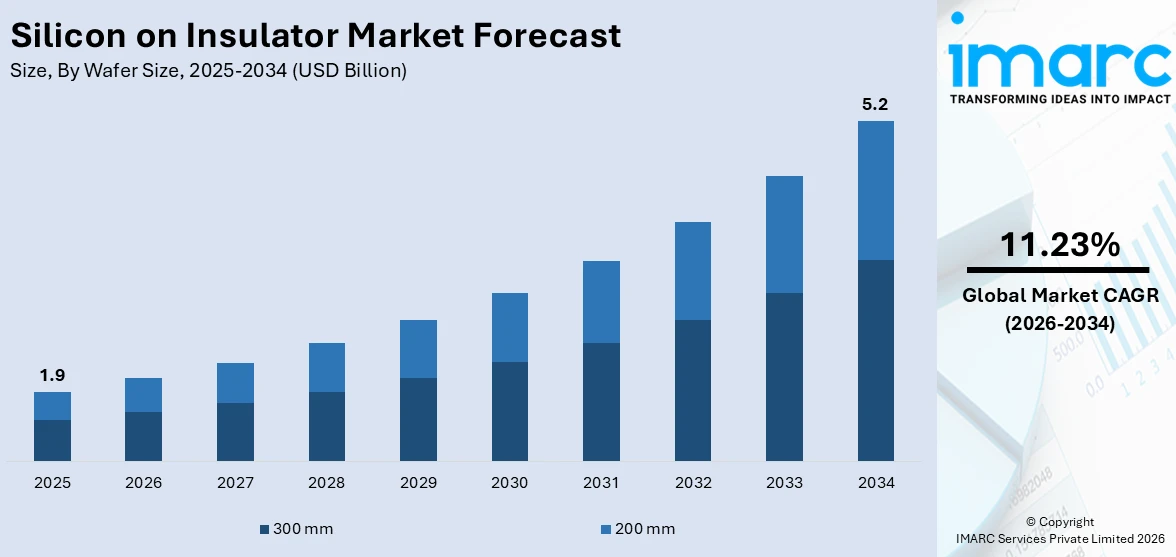

The global silicon on insulator market size reached USD 1.9 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 5.2 Billion by 2034, exhibiting a growth rate (CAGR) of 11.23% during 2026-2034. The market is witnessing substantial growth, mainly driven by amplifying demand across sectors including telecommunications, consumer electronics, and automotive. Moreover, silicon on insulator technology provides improved energy-efficiency, adaptability, and performance, establishing it as a requisite technology for 5G infrastructure and superior semiconductors development globally.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1.9 Billion |

|

Market Forecast in 2034

|

USD 5.2 Billion |

| Market Growth Rate 2026-2034 | 11.23% |

Silicon on Insulator Market Analysis:

- Major Market Drivers: The market is majorly driven by the increasing demand for superior-performance semiconductors across sectors such as telecommunications, consumer electronics, and automotive. The inclination towards the Internet of Things (IoT) devices, electric vehicles (EVs), and 5G services has boosted the adoption of silicon on insulator (SOI) primarily due to their exception processing abilities, improved efficiency, and lowered power consumption. In addition, the escalating requirement for compact as well as energy-saving electronic gadgets has resulted in an elevated investments for the development of silicon on insulator technology, further accelerating the market growth.

- Key Market Trends: Some of the key trends include amplified adoption of 5G networks and the rapid incorporation of silicon on insulator in superior automotive electronics. Additionally, the notable shift towards EVs and autonomous vehicles has fueled the need for SOI-based radar systems and sensors. Furthermore, the surge in machine learning (ML) and artificial intelligence (AI) applications is compelling semiconductor producers to leverage silicon on insulator wafers, bolstering their necessity in next-gen computing devices and technologies.

- Geographical Trends: Asia-Pacific is the leading region in the global market primarily due to the presence of robust manufacturing facilities in countries like South Korea and China. Moreover, the region profits from escalating industrialization, significant investments in 5G network infrastructure, and increasing utilization of advanced technologies. In addition, the intensifying need for electric cars and consumer electronics in Asia Pacific region also fuels the SOI market expansion, fortifying the region’s domination in the market. Additionally, the expanding production capacities and continuous research further improves its leadership.

- Competitive Landscape: Some of the major market players in the silicon on insulator industry include GlobalFoundries, GlobalWafers, Murata Manufacturing Co., Ltd., Okmetic, Qorvo, Inc, Shanghai Simgui Technology Co. Ltd., Shin-Etsu Chemical Co., Ltd, Silicon Valley Microelectronics, Inc., Soitec, STMicroelectronics, SUMCO Corporation, and Ultrasil LLC, among many others.

- Challenges and Opportunities: The market experiences challenges, such as sophisticated manufacturing methods and elevated costs of production. Nevertheless, innovation in fabrication methodologies and rising demand for energy-saving and compact electronic gadgets offer substantial growth opportunities. Moreover, the escalating emphasis on sustainable practices and the rapid development of environmentally friendly semiconductors also provide new channels for market propulsion. Additionally, companies can minimize their production cost while sustaining superior product quality to attain a competitive edge in the dynamic silicon on insulator landscape.

To get more information on this market Request Sample

Silicon on Insulator Market Trends:

Increasing Demand for Consumer Electronics

According to the silicon on insulator market research report, the growth is significantly driven by the heightening demand for upgraded consumer electronics, such as smart wearables, tablets, and smartphones. As per industry reports, approximately 4.3 billion individuals worldwide, i.e., 54%, owned a smartphone in 2023.

Silicon on insulator (SOI) technology provides enhanced performance, improved speeds for processing, and minimized power consumption, establishing it as a preferable option for superior-performance applications in advanced gadgets. Moreover, as customers are rapidly seeking more powerful and efficient devices, manufactures are actively adopting silicon on insulators technology to address the intensifying market demands, ultimately supporting the growth of silicon on insulator market across numerous niches of the consumer electronics sector.

Rapid Expansion of 5G Infrastructure

The silicon in insulator market overview indicates that the global implementation of 5G services is substantially bolstering the demand for SOI technology, especially in telecommunications. According to industry reports, more than 30 countries implemented 5G services in the year 2023. Moreover, in emerging economies, particularly India, four more 5G networks are anticipated to be established, adding 145 million new 5G users by the end of 2025. This technology facilitates the manufacturing of components with high-performance radio frequency (RF), that are requisite for 5G connectivity, providing excellent-speed data transmission and reduced signal interference. Moreover, telecom operators are currently extending their 5G infrastructure to cater to the proliferating demands of mobile data, and silicon on insulator wafers are being extensively leveraged in the manufacturing of crucial network components, further driving the market growth with amplified product adoption in communication sector.

Significant Growth of Automotive Electronics

The escalating incorporation of upgraded electronics in automotive solutions, especially in autonomous driving technology and electric vehicles (EVs), is boosting the SOI market. Silicon on insulator-based semiconductors are mostly preferred for their capability to improve performance, power efficiency, and reliability in automotive components, such as radar systems, power managements components, and sensors. Moreover, as the automotive sector is increasingly inclining towards eco-friendly, connected, and smart vehicles, the demand for SOI technology is significantly fueling, facilitating the market expansion within the automotive electronics industry, and ultimately contributing to the optimistic silicon on insulator market outlook. According to the International Energy Agency, 14 million electric cars were sold in 2023, and 95% of these sales were recorded in China, Europe and the Unites States of America.

Silicon on Insulator Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on wafer size, wafer type, technology, product, and application.

Breakup by Wafer Size:

- 300 mm

- 200 mm

300 mm accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the wafer size. This includes 300 mm and 200 mm. According to the report, 300 mm represented the largest segment.

As per the silicon on insulator market forecast, 300 mm is anticipated to sustain its dominance as the most preferred wafer size in the global market, primarily due to their ability to facilitate superior performance, especially in semiconductor production. Such wafers provide elevated production efficacy by adjusting a greater number of chips per wafer, improving overall yield and lowering costs. Moreover, the utilization of 300 mm wafers is mainly boosted by their consumption in advanced memory and processor devices, which are requisite in segments such as telecommunications and consumer electronics, substantially supporting the market growth. For instance, in July 2024, the United States Department of Commerce announced a partnership with GlobalWafers for the development of 300 mm silicon wafers production facility, with a significant investment of USD 400 million.

Breakup by Wafer Type:

- FD-SOI

- RF-SOI

- PD-SOI

- Others

FD-SOI holds the largest share of the industry

A detailed breakup and analysis of the market based on the wafer type have also been provided in the report. This includes FD-SOI, RF-SOI, PD-SOI, and others. According to the report, FD-SOI accounted for the largest market share.

FD-SOI is gaining momentum in the global market chiefly due to its benefits of cost-effectiveness and reduced power consumption. FD-SOI wafers are especially beneficial for applications that demand improved performance with least power usage, establishing them as an ideal wafer type for IoT applications, mobile devices, and automotive components. Additionally, the increasing need for energy-saving devices is bolstering the adoption of FD-SOI, establishing it as a major wafer type in the global market dynamics.

Breakup by Technology:

- Smart Cut

- BESOI

- SiMOX

- ELTRAN

- SoS

Smart cut represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the technology. This includes smart cut, BESOI, SiMOX, ELTRAN, and SoS. According to the report, smart cut represented the largest segment.

Smart cut technology plays a crucial role in the manufacturing if silicon on insulator wafers, facilitating accurate wafer fragmenting and effective reuse of material. This technology lowers the production costs while guaranteeing superior-quality SOI wafers for numerous applications. Moreover, its usage in semiconductor production improves adaptability, wafer yields, and enhances efficacy in mass production, positioning smart cut as a comprehensively leveraged technology that supports the global silicon on insulator market growth significantly.

Breakup by Product:

- RF FEM Products

- MEMS Devices

- Power Products

- Optical Communication

- Image Sensing

RF FEM products exhibit a clear dominance in the market

A detailed breakup and analysis of the market based on the product have also been provided in the report. This includes RF FEM products, MEMS devices, power products, optical communication, and image sensing. According to the report, RF FEM products accounted for the largest market share.

RF FEM, that is RF front-end modules, are rapidly becoming critical products in the market, especially for wireless and telecommunications purposes. Silicon on insulator technology permits RF FEM components to offer exceptional performance with negligible signal interference, which is crucial for 5G infrastructure and services. Moreover, an escalating demand for effective RF solutions in mobile devices as well as communication networks had notably boosted the demand for SOI-based RF FEM products, reinforcing a stable market expansion.

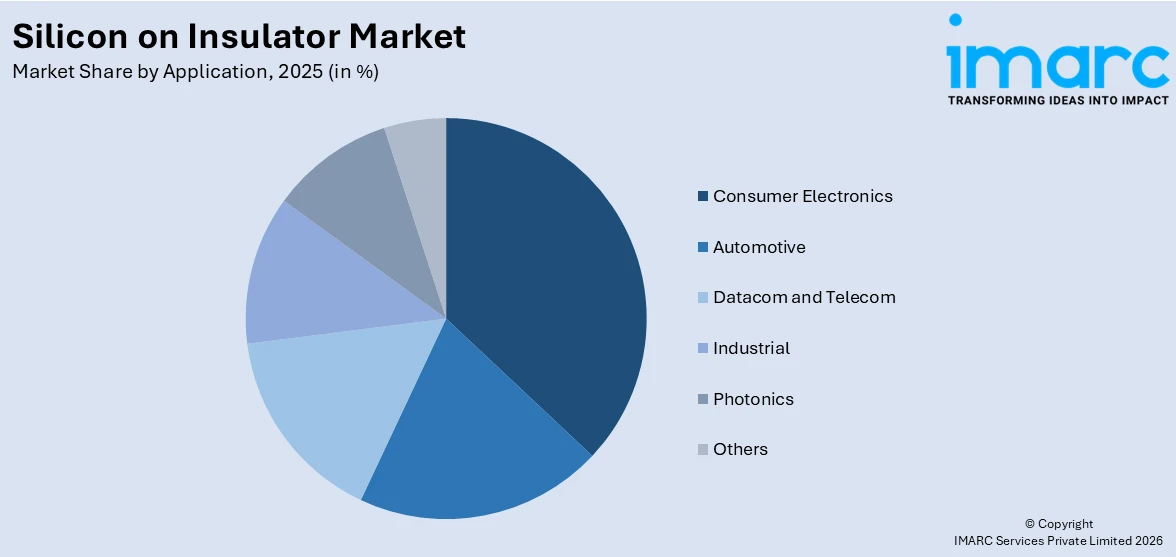

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Consumer Electronics

- Automotive

- Datacom and Telecom

- Industrial

- Photonics

- Others

Consumer electronics dominate the market

The report has provided a detailed breakup and analysis of the market based on the application. This includes consumer electronics, automotive, datacom and telecom, industrial, photonics, and others. According to the report, consumer electronics represented the largest segment.

Consumer electronics accounts for the leading application segment in the global market for silicon on insulator, principally driven by the heightening demand for energy-saving, superior-performing devices. Silicon on insulators improve the performance of memory chips as well as processors, facilitating more credible and faster consumer devices such as tablets, wearables, and smartphones. As per recent industry data, global smartwatch market is anticipated to witness a surge of 17%, with 83 million units projected to be shipped, in 2024. Moreover, the rapid advancements in consumer electronics, combined with increasing customer demand for upgraded features, aids in sustaining the dominance of this segment, ultimately driving the silicon on insulator market growth.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest silicon on insulator market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for silicon on insulator.

Asia Pacific is the dominant region in the global silicon on insulator market, primarily driven by accelerating technological advancements and the robust presence of expansive manufacturing countries, particularly in countries such as South Korea, Japan, and China. For instance, in June 2023, STMicroelectronics signed an agreement with Sanan Optoelectronics, a China-based producer of semiconductors and chips, for developing a new production facility of 200 mm silicon carbide in China. The facility is anticipated to initiate production in late 2025. Moreover, the region’s vast sectors of telecommunications and electronics, coupled with escalating adoption of EVs and 5G, further bolster requirement for silicon on insulator technology. In addition, the heightening investment in research and development by major players improve the region’s foothold and as well as dominance in the global market.

Competitive Landscape:

The global market is witnessing intense competition, with major players leading in production capacities and innovations. Moreover, numerous companies are currently emphasizing on strategic partnerships, acquisitions, and mergers to expand their market foothold and produce advanced silicon on insulator technologies. For instance, in June 2024, Soitec announced a strategic collaboration with UMC to develop a 3D IC solution for RF-SOI technology for 5G services. This technology will minimize the die size by 45% or more, allowing the integration of high number of radio frequency components to cater to the escalating demand for greater bandwidth. Additionally, cost-efficient manufacturing methods and technological advancements are crucial in sustaining a competitive edge, as the requirement for SOI continues to soar across sectors such as consumer electronics, telecommunications, and automotive.

The report provides a comprehensive analysis of the competitive landscape in the global silicon on insulator market with detailed profiles of all major companies, including:

- GlobalFoundries

- GlobalWafers

- Murata Manufacturing Co., Ltd.

- Okmetic

- Qorvo, Inc

- Shanghai Simgui Technology Co. Ltd.

- Shin-Etsu Chemical Co., Ltd

- Silicon Valley Microelectronics, Inc.

- Soitec

- STMicroelectronics

- SUMCO Corporation

- Ultrasil LLC

Silicon on Insulator Market News:

- In March 2024, STMicroelectronics, one of the major semiconductor companies, announced to switch to its new 18 nm FD-SOI process technology, developed in collaboration with Samsung, for its upcoming STM32 microcontrollers. This new technology will offer extended memory capacity, minimized power consumption, and improved performance.

- In June 2024, CEA-Leti, a prominent nanotechnology and microelectronics organization, introduced the FAMES pilot line, designed for Fully Depleted Silicon on Insulator (FD-SOI) technology. This initiative aims to support a wide range of applications, including RF components, 3D integration, and integrated circuit power management. The project focuses on advancing microelectronics for European regions, enhancing their technological infrastructure in various sectors.

Silicon on Insulator Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Wafer Sizes Covered | 300 mm, 200 mm |

| Wafer Types Covered | FD-SOI, RF-SOI, PD-SOI, Others |

| Technologies Covered | Smart Cut, BESOI, SiMOX, ELTRAN, SoS |

| Products Covered | RF FEM Products, MEMS Devices, Power Products, Optical Communication, Image Sensing |

| Applications Covered | Consumer Electronics, Automotive, Datacom and Telecom, Industrial, Photonics, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | GlobalFoundries, GlobalWafers, Murata Manufacturing Co., Ltd., Okmetic, Qorvo, Inc, Shanghai Simgui Technology Co. Ltd., Shin-Etsu Chemical Co., Ltd, Silicon Valley Microelectronics, Inc., Soitec, STMicroelectronics, SUMCO Corporation, Ultrasil LLC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the silicon on insulator market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global silicon on insulator market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the silicon on insulator industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global silicon on insulator market was valued at USD 1.9 Billion in 2025.

We expect the global silicon on insulator market to exhibit a CAGR of 11.23% during 2026-2034.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations resulting in the temporary closure of numerous manufacturing units for silicon on insulator.

The rising demand for silicon on insulator in reducing junction capacitance, that results in higher speed, eliminate charge leakage, and optimize the performance of SOI-based devices, while ensuring minimal power consumption, is primarily driving the global silicon on insulator market.

Based on the wafer size, the global silicon on insulator market can be segmented into 300 mm and 200 mm, where 300 mm currently holds the majority of the total market share.

Based on the wafer type, the global silicon on insulator market has been divided into FD-SOI, RF-SOI, PD-SOI, and others. Among these, FD-SOI exhibits a clear dominance in the market.

Based on the technology, the global silicon on insulator market can be categorized into smart cut, BESOI, SiMOX, ELTRAN, and SoS. Currently, smart cut accounts for the majority of the global market share.

Based on the product, the global silicon on insulator market has been segregated into RF FEM products, MEMS devices, power products, optical communication, and image sensing. Among these, RF FEM products currently hold the largest market share.

Based on the application, the global silicon on insulator market can be bifurcated into consumer electronics, automotive, datacom and telecom, industrial, photonics, and others. Currently, consumer electronics exhibit a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global silicon on insulator market include GlobalFoundries, GlobalWafers, Murata Manufacturing Co., Ltd., Okmetic, Qorvo, Inc, Shanghai Simgui Technology Co. Ltd., Shin-Etsu Chemical Co., Ltd, Silicon Valley Microelectronics, Inc., Soitec, STMicroelectronics, SUMCO Corporation, and Ultrasil LLC.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)