Semiconductor Packaging Market Size, Share, Trends and Forecast by Type, Packaging Material, Technology, End User, and Region, 2025-2033

Semiconductor Packaging Market Size and Share:

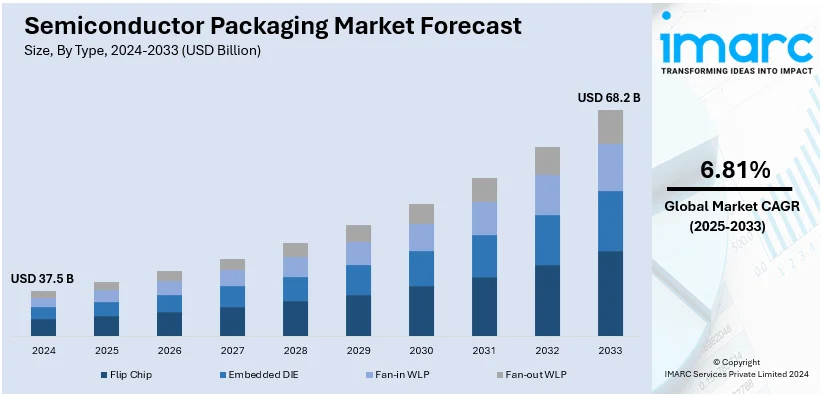

The global semiconductor packaging market size was valued at USD 37.5 Billion in 2024. The market is projected to reach USD 68.2 Billion by 2033, exhibiting a CAGR of 6.81% from 2025-2033. Asia Pacific currently dominates the market, holding a market share of over 54.3% in 2024. Substantial investments in leading-edge packaging technologies, resilient semiconductor manufacturing landscape, and magnifying need for consumer electronics, are contributing to the semiconductor packaging market share expansion.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 37.5 Billion |

|

Market Forecast in 2033

|

USD 68.2 Billion |

| Market Growth Rate (2025-2033) | 6.81% |

The global semiconductor packaging market is driven by the increasing demand for compact and high-performance electronic devices among automotive, consumer electronics, and telecommunications industries. Advancements in technologies like 3D integration, fan-out packaging, and wafer-level packaging are enabling enhanced functionality and energy efficiency. In addition, the rising adoption of IoT, artificial intelligence, and 5G technologies further supports the semiconductor packaging market demand by requiring sophisticated packaging solutions. Moreover, the rapid expansion of automotive electronics, chiefly driven by increasing adoption of electric and autonomous vehicles, and growing investments in semiconductor manufacturing strengthen the market's trajectory globally.

To get more information on this market, Request Sample

The United States plays a significant role in the global semiconductor packaging market, driven by its advanced research and development (R&D) ecosystem and strong presence of key semiconductor companies. The country’s focus on innovation in packaging technologies, such as 3D integration and advanced system-in-package (SiP) solutions, strengthens its position in the global market. Moreover, strategic investments in semiconductor manufacturing and supportive government initiatives, such as the CHIPS Act, further bolster semiconductor packaging market share. For instance, in November 2024, the Department of Commerce allocated a substantial investment of USD 285 Million for the development of Semiconductor Manufacturing and Advanced Research with Twins USA Institute that will emphasize on advanced packaging, semiconductor manufacturing, and testing. Furthermore, the rising demand for high-performance computing, IoT devices, and automotive electronics amplifies the need for cutting-edge packaging solutions, positioning the U.S. as a leader in driving technological advancements within the global market.

Semiconductor Packaging Market Trends:

System-in-Package (SiP) Integration

System-in-Package (SiP) is a growing trend in the market, driven by the demand for miniaturization and increased functionality in electronic devices. As per an industry survey, daily smartphone usage has reached an average of 4 hours and 37 minutes per person. This leads to an increased demand for smaller, more powerful devices. This heightened usage underscores the necessity for advanced semiconductor packaging solutions, such as System-in-Package (SiP), which consolidate various components, including processors, memory, and sensors, into a single, compact package. This allows for greater performance and flexibility while reducing the footprint and power consumption of electronic devices. Moreover, SiP facilitates heterogeneous integration, allowing multiple semiconductor technologies, such as silicon, MEMS, and optoelectronics, to be combined. This trend is likely to persist as manufacturers try to shrink device size and enhance performance without sacrificing cost-effectiveness, and it remains a pivotal evolution in the future of semiconductor packaging.

Growth of 3D Packaging

The growth of 3D packing technology is providing a boost to market development. 3D packaging technology involves stacking multiple semiconductors dies vertically within a single package, creating a more compact and efficient design. 3D packaging has become crucial in high-performance applications, such as data centers, telecommunications, and AI processing. In these fields, the goal is to maximize performance while minimizing size and power consumption. According to an industry report, the global data center market is expected to reach USD 494.5 Billion by 2033, exhibiting a growth rate (CAGR) of 9.29% during 2025-2033. This expansion directly impacts the semiconductor packaging market, as the drive for smaller, more efficient chips aligns perfectly with the capabilities of 3D packaging. As demand for higher computational power and smaller form factors continues to rise, the adoption of 3D packaging technologies is expected to increase, allowing companies to push the limits of semiconductor performance while managing heat dissipation and reliability challenges.

Increasing Demand for Consumer Electronics

The growing demand for consumer electronics, particularly smartphones, wearables, and smart home devices, is positively influencing the semiconductor packaging market growth. As more consumers adopt these technologies, the need for advanced semiconductor components, continues to rise. According to an industry report, smart home devices are in active use across 69.91 million households in the United States as of 2024, marking a 10.2% increase from the 63.43 million recorded in 2023. This surge in adoption highlights the growing reliance on more efficient, compact, and powerful chips, which in turn boosts the demand for innovative packaging solutions. Moreover, the continuous innovations in display technologies, camera sensors, and wireless communication components are fueling the need for advanced packaging solutions. This trend is expected to drive the market further as manufacturers strive to meet the growing need for faster, more powerful, and highly integrated consumer electronics, pushing the development and adoption of new packaging technologies.

Semiconductor Packaging Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global semiconductor packaging market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on type, packaging material, technology, and end user.

Analysis by Type:

- Flip Chip

- Embedded DIE

- Fan-in WLP

- Fan-out WLP

Flip chip exhibits domination as the type segment in the global semiconductor packaging market primarily due to its capability of assisting miniaturization and improving device performance. This type of packaging provides exceptional thermal and electrical performance by adhering semiconductor dies directly to the substrate by leveraging solder bumps. Moreover, its extensive utilization in telecommunications, excellent-performance computing, and upgraded processors boosts demand. The notable emergence of 5G technology, AI, and IoT applications further accelerates the adoption of flip chip packaging. In addition, manufacturers are rapidly shifting towards this type for its elevated output/input/ density and improved resilience. Furthermore, constant advancements in flip chip technologies are guaranteeing their sustained leadership in the global market.

Analysis by Packaging Material:

- Organic Substrate

- Bonding Wire

- Leadframe

- Ceramic Package

- Die Attach Material

- Others

Organic substrate leads the market with around 41.6% of market share in 2024. This segment is mainly influenced by their excellent compatibility with innovative packaging techniques, cost effectiveness, and adaptability. Such material is extensively leveraged in applications demanding flexible as well as lightweighted solutions, like certain compact electronic devices, wearable, or smartphones. In addition to this, organic substrates aid technologies such as flip chip and fan-out packaging, positioning them as requisite part in automotive electronics and high-performance computing. Furthermore, their environmental advantages and ease of mass production also strengthens their market domination. Ongoing advancements in substrate technology are anticipated to further boost the expansion of organic materials in semiconductor packaging.

Analysis by Technology:

- Grid Array

- Small Outline Package

- Flat no-leads Package

- Dual In-Line Package

- Others

The grid array technology segment leads the global semiconductor packaging market, primarily due to its effective thermal management and high input/output density. Variants including pin grid array and ball grid array are comprehensively leveraged in memory modules, innovative processors, and GPUs. Moreover, this technology is preferred for its capability to aid upgraded telecommunications applications and high-performance computing. Additionally, the emergence of AI-based devices and 5G networks boosts the utilization of grid array packaging. Its robustness and flexibility establish it as a preferable option for producers targeting to address the magnifying sophistication of modern electronic devices.

Analysis by End User:

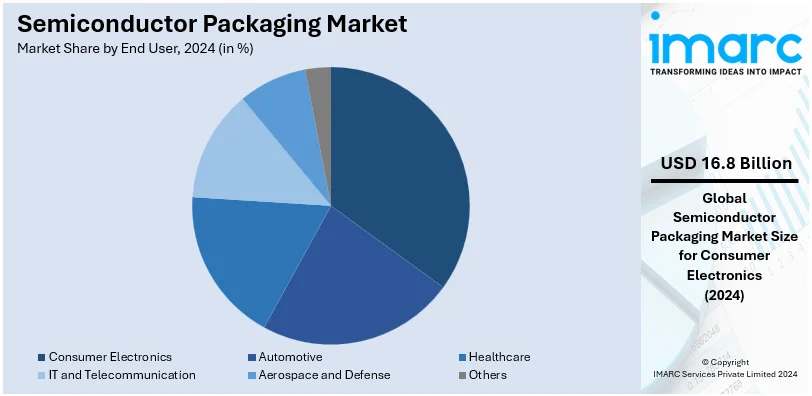

- Consumer Electronics

- Automotive

- Healthcare

- IT and Telecommunication

- Aerospace and Defense

- Others

Consumer electronics leads the market with around 44.8% of market share in 2024. This end user is principally driven by the amplifying requirement for excellent-performance, compact devices, mainly encompassing wearables, smartphones, and tablets. The increasing revolution smart home technologies and IoT further accelerates the adoption of cutting-edge semiconductor packaging solutions. Furthermore, growing trend of miniaturization and the notable demand for energy-saving components have magnified the need for intricated packaging techniques in consumer electronics. Additionally, major players are actively emphasizing on advancement initiatives to cater to the fueling performance expectations of end-users. Moreover, with steady innovations in consumer electronics, this segment remains a crucial contributor to the expansion of semiconductor packaging market.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, Asia-Pacific accounted for the largest market share of over 54.3%. APAC is known for its competitive manufacturing environment and cost-effectiveness. Technologies for semiconductor packaging enhance compact designs and increased functionality in electronics, which in turn is appealing tech-oriented demographic and significant smartphone use. The region serves as a center for outsourced semiconductor assembly and test (OSAT) services, bolstered by a skilled workforce and extensive production capacities. New opportunities arise from the escalating use of smart devices, automotive electronics, and renewable energy technologies. For example, in March 2024, China's position in renewable energy, with an anticipated 1,000 GW of solar capacity by 2026, highlights its swift transition from fossil fuels, which now comprise less than 50% of overall power capacity. This extraordinary growth propels innovation in semiconductor packaging, utilizing renewable energy for efficient and sustainable manufacturing processes, in line with global climate objectives. An increase in investment in packaging innovation corresponds with the need for greater speed and connectivity. Furthermore, partnerships between international semiconductor companies and local entities encourage progress in heterogeneous integration, allowing the Asia-Pacific region to meet changing industry demands.

Key Regional Takeaways:

United States Semiconductor Packaging Market Analysis

In North America, the United States accounted for 70.00% of the total market share due to groundbreaking innovations and strong research capabilities. Apart from this, the market is significantly being propelled by supportive government policies such as CHIPS and Science Act which is fostering local semiconductor production in the country which in turn is reducing the reliance on China. The packaging technologies available here improve device efficiency, which in turn is aiding the end use industries. This swift growth propels advancements in semiconductor packaging, allowing for smaller, high-performance components that support applications such as IoT and AR. The existence of top semiconductor firms and a talented workforce stimulates rapid innovation. Semiconductor packaging aids in miniaturization while enhancing performance and thermal management, which are critical for AI and high-performance computing. Amidst US- China chip war, opportunities are emerging in the country from substantial investments in semiconductor manufacturing and packaging facilities, bolstered by government initiatives that advocate for domestic production. The surge in consumer electronics and data centres also opens pathways for companies that provide advanced packaging techniques.

Europe Semiconductor Packaging Market Analysis

Europe’s semiconductor packaging market is influenced by robust demand within the automotive and industrial sectors. Packaging solutions improve the reliability and functionality of semiconductors in electric vehicles and autonomous systems. The region is embracing advanced packaging technologies, such as fan-out wafer-level packaging, to satisfy the needs of emerging applications like renewable energy storage and industrial automation. In August 2024, a recent survey conducted by Reichelt Elektronik emphasizes Europe's strides in industrial automation, with Germany and the Netherlands spearheading automation rates at 43% and 41%, respectively. Industrial IoT adoption reaches a peak of 48% in the Netherlands, demonstrating its capacity to improve processes such as semiconductor packaging. With 60% of businesses anticipating complete manufacturing automation within five years, automation becomes vital for sustaining competitiveness. These advancements highlight the transformative effect of automation on Europe's industrial sector. Opportunities are increasing as European governments emphasize semiconductor supply chain resilience and invest in domestic chip manufacturing. Furthermore, the region’s emphasis on sustainability encourages interest in eco-friendly packaging materials and methods. Europe also acts as a center for collaboration between research institutions and industry players, promoting innovation and bolstering its global competitiveness in advanced packaging.

Latin America Semiconductor Packaging Market Analysis

In Latin America, the semiconductor packaging sector is benefiting from the rising utilization of electronics in the industrial, automotive, and consumer sectors. Cutting-edge packaging technologies improve device functionality and energy efficiency, catering to the increasing demand for compact and multifunctional devices. There exist prospects as governments in the region invest in local semiconductor ecosystems, promoting technology transfer and industrial advancement. For instance, Brazil’s semiconductor sector is quickly growing, supported by investments such as USD 425 Million from the 2024 New Industrial Policy . This growth enhances semiconductor packaging capabilities, leveraging Brazil's sophisticated renewable energy infrastructure and broadening research and development prospects. Latin America is also emerging as a viable site for nearshoring by international semiconductor companies, reducing dependency on lengthy supply chains. Collaborations with global entities enable the region to adopt advanced manufacturing techniques, generating growth prospects in packaging solutions that promote IoT, renewable energy, and telecommunications advancements.

Middle East and Africa Semiconductor Packaging Market Analysis

The Middle East and Africa are experiencing a rising interest in semiconductor technologies to aid the growth of smart cities and digital infrastructures. Sophisticated packaging solutions play a role in creating sturdy and high-performing devices capable of enduring extreme conditions. As government emphasis on local technology manufacturing and the formation of semiconductor hubs intensifies, new possibilities are emerging. For example, Saudi Arabia's National Semiconductor Hub aims to create 50 semiconductor design firms and educate 5,000 engineers by 2030, backed by a venture capital fund of about USD 266 Million and nearly USD 39. 9 Million in resources. This initiative enhances semiconductor packaging capabilities by cultivating a localized ecosystem anticipated to generate approximately USD 13. 3 Billion for the Kingdom's economy. The surge in the adoption of renewable energy technologies and electric vehicles further increases the need for specialized packaging. Investments in technology parks and research institutions are encouraging innovation in packaging and integration, positioning the area for expansion in the global semiconductor market.

Competitive Landscape:

The market exhibits intense competition, driven by the presence of established players and emerging innovators. Key companies focus on developing advanced packaging technologies such as 3D integration, fan-out, and wafer-level packaging to maintain their market position. Furthermore, strategic collaborations, mergers, and acquisitions are common as companies aim to enhance their technological capabilities and expand global footprints. For instance, in September 20204, Tata Electronics announced partnership with ASMPT Singapore to develop both solutions and infrastructure for semiconductor assembly equipment at its chip packaging plants in India. Under this pact, ASMPT will aid Tata Electronics in bolstering research and developments projects, crew training, enhancing service engineering capabilities for flip chip, wire bonding, cutting-edge integrated system packaging technologies. The market also benefits from significant investments in research and development to meet the growing demand for high-performance, energy-efficient semiconductor solutions. In addition, leading players are addressing industry trends like miniaturization, IoT proliferation, and AI adoption. Moreover, strong regional players and startups contribute significantly to competitive dynamics.

The report provides a comprehensive analysis of the competitive landscape in the semiconductor packaging market with detailed profiles of all major companies, including:

- Amkor Technology

- ASE

- CHIPBOND Technology Corporation

- Intel Corporation

- International Business Machines Corporation

- JCET Group

- Nepes Corporation

- Powertech Technology Inc.

- Shinko Electric Industries Co., Ltd.

- Siliconware Precision Industries Co., Ltd

- STMicroelectronics

- Taiwan Semiconductor Manufacturing Company Limited

- Texas Instruments Incorporated

Latest News and Developments:

- March 2024: the U.S. Department of Commerce and Intel Corporation entered into a non-binding preliminary memorandum of terms (PMT). This agreement allocates USD 8.5 Billion in direct funding to Intel Corporation for commercial semiconductor projects under the CHIPS and Science Act. The funding aims to bolster domestic semiconductor manufacturing and packaging capabilities, enhancing the competitiveness of the U.S. semiconductor industry. This initiative is expected to drive significant advancements in semiconductor packaging technologies.

- March 2024: Taiwan Semiconductor Manufacturing Company (TSMC) revealed plans to build a cutting-edge semiconductor packaging facility in Japan. The facility will focus on implementing TSMC's innovative chip-on-wafer-on-substrate (CoWoS) technology, which integrates stacked chip designs. This advanced packaging method improves processing performance while reducing energy consumption in semiconductor chips. TSMC's investment highlights its commitment to strengthening its presence in the global semiconductor supply chain.

- October 2023: Amkor Technology Inc. inaugurated their latest factory in Vietnam. The USD 1.6 Billion chip factory will become Amkor’s most advanced facility, delivering next-generation semiconductor packaging capabilities. The plant spans a significant 57-acre area within the Yen Phong 2C Industrial Park and includes 200,000 square meters dedicated to cleanroom space.

- October 2023: ASE Group announced the launch of its Integrated Design Ecosystem™ (IDE), a collaborative design toolset optimized to systematically boost advanced package architecture across its VIPack™ platform. This advanced method enables a smooth shift from single-die SoCs to multi-die disaggregated IP modules, such as chiplets and memory, for incorporation through cutting-edge fan-out architectures or 2.5D.

- December 2023: ChipMOS Technologies Inc. received approval from its Board of Directors to sell its 45.0% equity interests in Unimos Microelectronics (Shanghai) Co., Ltd. for approximately USD 137.1 Million. This move aligns with ChipMOS' strategy to focus on higher growth markets and strengthen its financial position for future development, with the transaction proceeds earmarked for operational enhancements and investments in R&D to meet evolving customer needs in sectors such as automotive electronics, 5G, intelligent home devices, and AI applications.

Semiconductor Packaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Flip Chip, Embedded DIE, Fan-in WLP, Fan-out WLP |

| Packaging Materials Covered | Organic Substrate, Bonding Wire, Leadframe, Ceramic Package, Die Attach Material, Others |

| Technologies Covered | Grid Array, Small Outline Package, Flat no-leads Package, Dual In-Line Package, Others |

| End Users Covered | Consumer Electronics, Automotive, Healthcare, IT and Telecommunicaton, Aerospace and Defense, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amkor Technology, ASE, CHIPBOND Technology Corporation, Intel Corporation, International Business Machines Corporation, JCET Group, Nepes Corporation, Powertech Technology Inc., Shinko Electric Industries Co., Ltd., Siliconware Precision Industries Co., Ltd, STMicroelectronics, Taiwan Semiconductor Manufacturing Company Limited, Texas Instruments Incorporated, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the semiconductor packaging market from 2019-2033.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global semiconductor packaging market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the semiconductor packaging industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The semiconductor packaging market was valued at USD 37.5 Billion in 2024.

The semiconductor packaging market is projected to exhibit a CAGR of 6.81% during 2025-2033, reaching a value of USD 68.2 Billion by 2033.

In the semiconductor industry, packaging refers to the process of enclosing integrated circuits (ICs) in protective materials to ensure their functionality, reliability, and performance. This structure ensures electrical connections, thermal dissipation, and mechanical support. Further, packaging protects the chip from environmental factors and facilitates its integration into electronic systems.

The semiconductor packaging market is majorly driven by increasing demand for miniaturized electronic devices, advancements in packaging technologies such as 3D and fan-out, and the rising adoption of IoT and AI-enabled devices, and growing applications in automotive electronics and high-performance computing.

Asia Pacific currently dominates the market, accounting for a share of around 54.3%. The dominance is driven by rapid technological advancements, increasing demand for consumer electronics, robust manufacturing capabilities, government support, expanding IoT adoption, and growing automotive and telecommunications industries.

Some of the major players in the semiconductor packaging market include Amkor Technology, ASE, CHIPBOND Technology Corporation, Intel Corporation, International Business Machines Corporation, JCET Group, Nepes Corporation, Powertech Technology Inc., Shinko Electric Industries Co., Ltd., Siliconware Precision Industries Co., Ltd, STMicroelectronics, Taiwan Semiconductor Manufacturing Company Limited, and Texas Instruments Incorporated, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)