Semiconductor Foundry Market Size, Share, Trends and Forecast by Technology Node, Foundry Type, Application, and Region, 2025-2033

Semiconductor Foundry Market Size and Share:

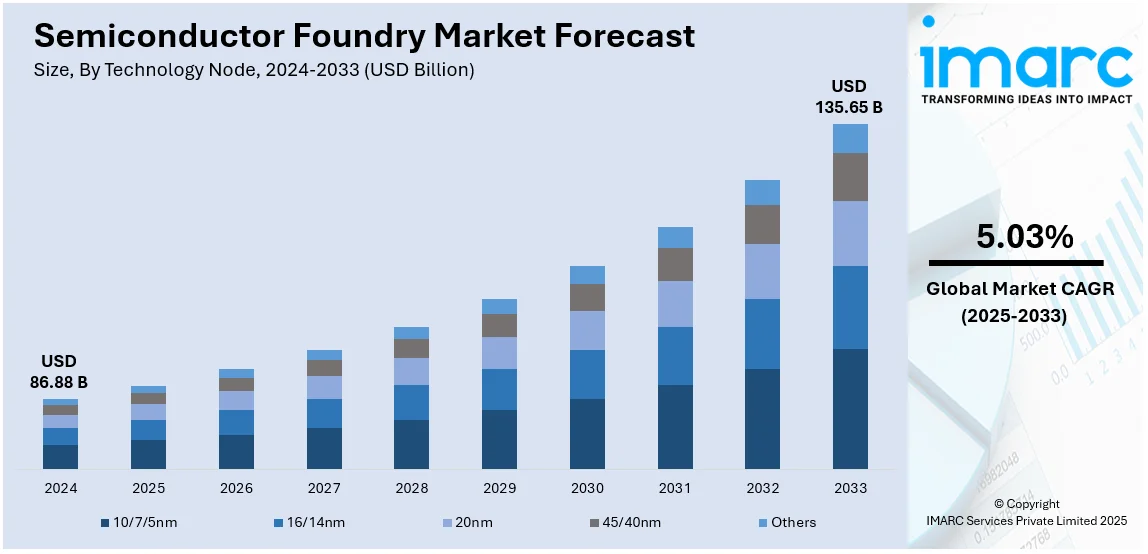

The global semiconductor foundry market size was valued at USD 86.88 Billion in 2024. The market is projected to reach USD 135.65 Billion by 2033, exhibiting a CAGR of 5.03% during 2025-2033. Asia Pacific currently dominates the market holding a significant market share of over 71.2% in 2024. The market is witnessing consistent growth propelled by the increasing need for cutting-edge electronics in diverse sectors such as consumer electronics, automotive and telecommunication, the growing transition towards electric and self-driving vehicles and rising use of AI and machine learning. Additionally, increasing need for next-generation semiconductor technologies within industries such as automotive, telecommunication, and data infrastructure is augmenting the growth of the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Base Year |

2024

|

| Forecast Years | 2025-2033 |

| Historical Years |

2019-2024

|

|

Market Size in 2024

|

USD 86.88 Billion

|

|

Market Forecast in 2033

|

USD 135.65 Billion

|

|

Market Growth Rate (2025-2033)

|

5.03% |

The semiconductor foundry market growth is driven by the rising demand for advanced semiconductors across industries such as consumer electronics, automotive and telecommunications. The surge in adoption of 5G technology, IoT devices and AI applications requires high performance chips fueling foundry growth. For instance, in May 2024, UMC launched the industry’s first 3D IC solution for RFSOI technology significantly reducing die size by over 45% while enhancing RF performance. This innovation facilitates the integration of additional RF components in 5G devices addressing rising frequency demands. Rising investments in chip manufacturing coupled with the shift toward smaller node technologies like 5nm and 3nm enhance efficiency and performance further driving demand. Geopolitical factors and the push for localized semiconductor production bolster market expansion.

The increasing demand for advanced chips across sectors, such as defense, automotive, and consumer electronics represents one of the key semiconductor foundry market trends in the United States. The push for domestic chip production supported by initiatives like the CHIPS Act aims to reduce reliance on foreign supply chains. For example, in December 2024, the Biden-Harris administration allocated up to $1.61 billion to Texas Instruments under the CHIPS Incentives Program enhancing U.S. semiconductor production. This funding supports TI's $18 billion investment in three facilities two in Texas and one in Utah. Such rapid growth from AI, 5G and IoT technologies fosters a drive for high performance semiconductors. Additionally, the rising automotive sector where electric and self-driving vehicles replace the old fuels increase the need for special chips with an elevated level of growth prospect.

Semiconductor Foundry Market Trends:

Rising Demand for Advanced Electronics

The global market is significantly driven by the escalating demand for advanced electronic devices including smartphones, computers and IoT devices. The global IoT market size reached USD 1,022.6 Billion in 2024. This rise is fueled by technological advancements and the proliferation of high speed internet services. With these technologies becoming an integral part of daily life and business there is an increased demand for more complex and highly powerful semiconductors. The needs for developing 5G technology and AI require the most advanced chipsets. The automotive industry's shift towards electric and autonomous vehicles is further driving the demand for high performance semiconductors thereby fueling the growth of semiconductor foundries that manufacture these complex components.

Technological Advancements in Semiconductor Manufacturing

Technological innovation in semiconductor manufacturing processes has become a driving force for the growth of the global market. The replacement of traditional lithography with extreme ultraviolet lithography makes it possible to manufacture smaller more efficient and more powerful semiconductors. This advancement is essential to meet the growing demand for high-performance chips across consumer electronics, automotive and industrial applications. According to a report from the Semiconductor Industry Association (SIA), semiconductor exports added $62 billion to the U.S. economy in 2021 placing it among the leading export categories, which also include refined oil, aircraft, crude oil and natural gas. Continuous research and development of semiconductor materials including silicon carbide (SiC) and gallium nitride (GaN) are contributing to ongoing new potential developments in applications for power electronics and radio frequency. These technological advancements are the catalysts for innovation and cost reduction for manufacturing which in turn propels the market growth.

Global Supply Chain Realignment and Expansion

The market is also influenced by the evolving dynamics of the global supply chain. The global market for supply chain analytics was valued at USD 9.39 billion in 2024. In recent years, geopolitical tensions and trade disputes have led many countries and companies to rethink their reliance on specific regions for critical semiconductor supplies. This shift is resulting in the realignment of the global semiconductor supply chain toward more diversified production locations and increased investment in domestic manufacturing capabilities. The COVID-19 pandemic highlighted vulnerabilities in highly concentrated supply chains which is hastening the effort toward geographic diversification. This scenario is encouraging investments in new foundry capacities outside traditional hubs such as Taiwan and South Korea and is fostering the growth of the semiconductor foundry market by creating new regional players and expanding production capabilities to meet the global demand.

Rising Demand and Investment in the Market

The industry is witnessing consistent growth, driven by the rapid growth of the digital economy. Widespread use of digital technologies in sectors like finance, healthcare, retail, and manufacturing has boosted the demand for high-performance yet energy-efficient chips. Along with this, cloud computing, AI, IoT, and 5G infrastructure further are driving demand for advanced node semiconductors, compelling design houses to outsource manufacturing to foundries with leading-edge capability. Concurrently, the semiconductor foundry industry is witnessing appreciable capital inflows from governments and private companies alike. These investments aim to counteract geopolitical tensions and minimize reliance on cross-border supply chains. In response, countries are prioritizing the development of domestic foundry capabilities, viewing them as critical to national security and economic resilience. The global industry is entering a major investment cycle, with spending about USD 400 Billion to redefine global 300mm fab production by 2027. This increased funding is facilitating the development of new fabrication facilities, especially in areas aiming to develop or grow their own local semiconductor ecosystems. These initiatives are transforming the semiconductor foundry landscape, making production more geographically diversified.

Semiconductor Foundry Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global semiconductor foundry market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on technology node, foundry type and application.

Analysis by Technology Node:

- 10/7/5nm

- 16/14nm

- 20nm

- 45/40nm

- Others

10/7/5nm stand as the largest technology node in 2024, holding around 36.2% of the market. The 10/7/5nm node is the most advanced technology node in the market and currently has the largest market share. It serves high performance applications in such areas as smartphone, high end computing and data center where the efficiency of energy and processing power is involved. The chips manufactured at this node are replete with high transistor density that highly enhances their performance and energy efficiency. The demand in this segment is driven by the continuous need for more powerful and efficient processors in consumer electronics and the growing interest in artificial intelligence and machine learning applications which require cutting edge processing capabilities.

Analysis by Foundry Type:

- Pure Play Foundry

- IDMs

IDMs leads the market with around 63.7% of the total semiconductor foundry market share in 2024. Integrated Device Manufacturers (IDMs) represent the largest segment in the semiconductor foundry market. IDMs are firms that take on the entire semiconductor production process, from design to manufacturing and even distribution. The reason for the dominance of this segment is due to the full control it exerts over the semiconductor manufacturing process which offers greater quality assurance, supply chain management and product customization. IDMs are very prominent in markets where high degrees of integration between design and manufacturing are crucial such as in advanced computing, automotive and high-end consumer electronics. IDMs receive significant investments in research and development at scale enabling them to innovate rapidly and maintain technological leadership. Their capability to manufacture proprietary chips also offers a competitive advantage by ensuring high performance and reliability which is necessary for industries requiring cutting-edge semiconductor solutions.

Analysis by Application:

- Communication

- Consumer Electronics

- Computer

- Automotive

- Others

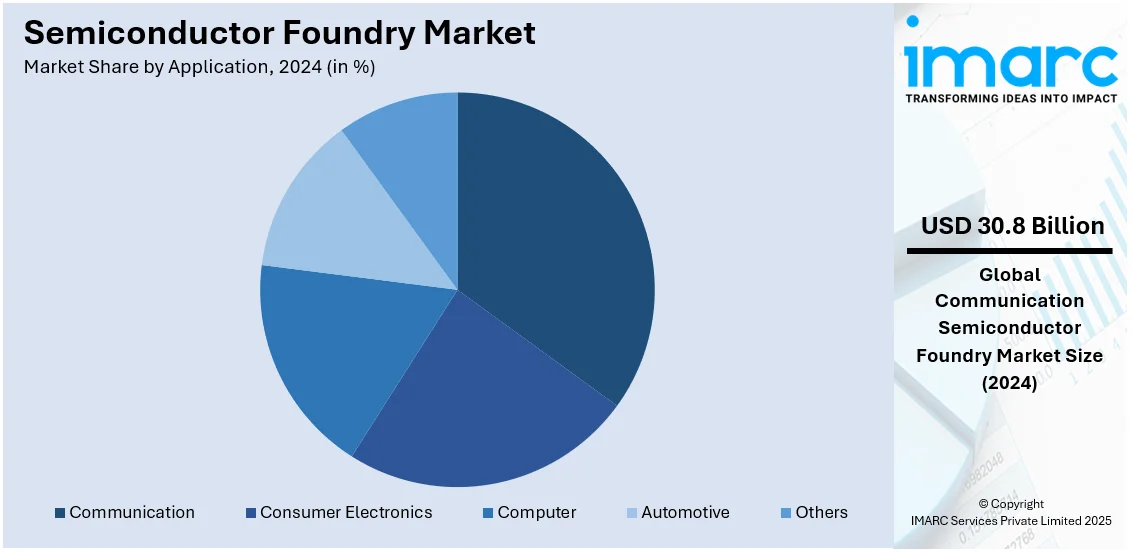

Communication leads the market with around 35.4% of market share in 2024. The communication segment holds the largest share of the market mainly driven by rapid growth in telecommunications infrastructure and rising penetration of smartphones and other communication devices across the globe. This segment benefits from the ongoing rollout of 5G technology requiring advanced semiconductor components for both infrastructure and end user devices. This demand in this segment is characterized by the need for high speed, high capacity and energy efficient semiconductor solutions that can support the ever-increasing data and connectivity requirements of modern communication systems.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

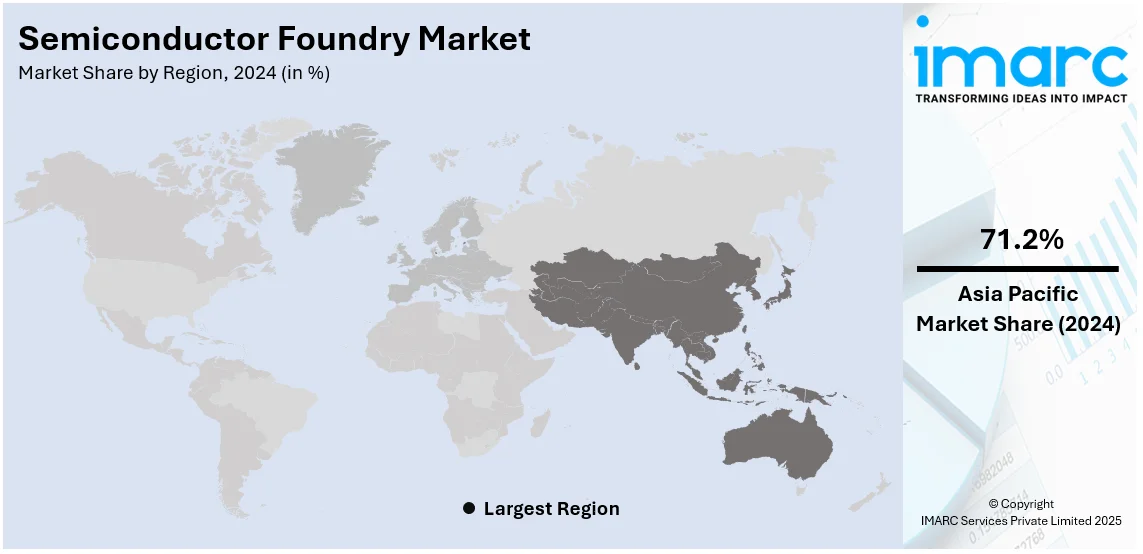

In 2024, Asia Pacific accounted for the largest market share of over 71.2%. The Asia Pacific region dominates the semiconductor foundry market mainly due to the availability of key manufacturing hubs and a strong electronics manufacturing ecosystem in countries like Taiwan, South Korea and China. The region is known for its broad semiconductor manufacturing capabilities, high investment in R&D and is home to the top semiconductor companies. Growth in the segment is driven further by rising consumer electronics demand and rapid communication infrastructure development in the region. Government initiatives and policies in these countries, aimed at enhancing the semiconductor industry play a significant role in maintaining Asia Pacific's leading position in the global market.

Key Regional Takeaways:

North America Semiconductor Foundry Market Analysis

The North American semiconductor foundry market is experiencing significant growth fueled by advancements in 5G, AI and cloud computing technologies. The region's strong presence in tech innovation particularly in the United States and Canada underpins the demand for high performance chips in industries such as telecommunications, automotive and data centers. Government initiatives such as the CHIPS Act in the U.S. are encouraging local manufacturing and import dependency reduction which is also driving the foundry ecosystem in the region. The automotive sector's shift toward electric and autonomous vehicles further increases the demand for specialized semiconductors in battery management and driver assistance systems. North America's R&D capabilities and investments in advanced chip technologies ensure leadership in the global semiconductor landscape.

United States Semiconductor Foundry Market Analysis

In 2024, the United States captured 88.90% of revenue in the North American market. The United States has been one of the greatest hubs for AI innovation with the ecosystem of startup companies propelling technological progress in the country. From 2013 to 2022, the country was home to 4,633 AI startups, demonstrating its leadership in the AI sector compared to other nations. An increase in AI entrepreneurship increases demand for more sophisticated semiconductors since the technologies depend on powerful chips. The rapid growth of 5G technology, cloud computing and AI applications is driving the semiconductor foundry market with sectors such as telecommunications, automotive and data centers demanding increasingly sophisticated semiconductors. The growth in electric vehicles and autonomous driving technology also contributes significantly to the demand for dedicated chips thereby creating a positive outlook for the market growth. AI, automation and advanced semiconductor technologies collectively are placing the U.S. at a competitive advantage both in the semiconductor foundry services and in AI development supported by private investments and governmental policies promoting long-term growth in the sector.

Europe Semiconductor Foundry Market Analysis

The European semiconductor foundry market is propelled by a growing demand across various sectors including automotive, industrial automation, consumer electronics and telecommunications. One of the key drivers for the market is the automotive industry's trend toward electric vehicles. For instance, in 2023 new car registrations in Europe reached approximately 3.2 million reflecting a 20% increase compared to 2022. Within the European Union sales climbed to 2.4 million indicating a similar growth pattern. This surge in EV adoption drives the demand for semiconductors, power management, ADAS and battery systems. The European Union's efforts to strengthen the semiconductor supply chain as in the European Chips Act promote investments in local manufacturing capabilities and reduce dependence on external sources. Coupled with 5G, IoT and sustainability related advancements this places Europe on a strong footing within the global semiconductor foundry market. Collaboration among European nations and semiconductor firms should further cement this region's presence in this still-growth industry.

Latin America Semiconductor Foundry Market Analysis

Latin America semiconductor foundry market is experiencing substantial growth mainly due to adoption of electronic devices, automotive technologies and improvement in telecommunication. As reported by GSMA, mobile technologies and services contributed 8% to the GDP of Latin America in 2023 resulting in an economic value of USD 520 billion. Such growth in consumer electronics and automotive sectors boosts demand for semiconductors. Government programs that are designed to stimulate technological innovations and upgrade infrastructures support the growth of the semiconductor industry. The region's developing manufacturing abilities and proximity to key markets further support the semiconductor foundry market of the region.

Middle East and Africa Semiconductor Foundry Market Analysis

The Middle East and Africa (MEA) semiconductor foundry market is witnessing growth due to the increasing adoption of electronic devices in the region. According to industry reports, as of 2023, the Middle East and North Africa (MENA) region had 0.28 billion Internet of Things (IoT) devices. The growing use of IoT along with mobile network expansion and smart city projects is driving demand for semiconductors. Investments in infrastructure and technology development, especially in the Middle East are further contributing to this market's growth.

Competitive Landscape:

The semiconductor foundry market is highly competitive as established players face new entrants which have been spurred by the advancement of the manufacturing process and growing demand for specialized chips. Companies are targeting the development of smaller node technologies such as 5nm, 4nm and 3nm in order to boost performance and efficiency in energy use. For example, in December 2024, TSMC announced the commencement of mass production of advanced chips at its Phoenix, Arizona facility in 2025 using 4-nanometer technology. Strategic partnerships with the tech firms as well as government collaborations are important in expanding production capacity and meeting growth in demand for industries such as AI, 5G and automotive. According to the semiconductor foundry market forecast, the rising investments in ecofriendly manufacturing and localized supply chains is expected to influence market competition further, thereby ensuring long term resilience and innovation.

The report provides a comprehensive analysis of the competitive landscape in the semiconductor foundry market with detailed profiles of all major companies, including:

- DB HiTek

- GlobalFoundries

- Hua Hong Semiconductor Limited

- Intel Corporation

- Powerchip Semiconductor Manufacturing Corporation

- Samsung Semiconductor, Inc.

- Semiconductor Manufacturing International Corporation

- Taiwan Semiconductor Manufacturing Company Limited

- Tower Semiconductor Ltd.

- United Microelectronics Corporation

- X-FAB Silicon Foundries SE

Latest News and Developments:

- June 2025: GlobalFoundries announced a USD 16 Billion investment to strengthen domestic semiconductor manufacturing and support the growing demand for AI technologies. The initiative includes approximately USD 13 Billion to expand and modernize its existing fabrication facilities in New York and Vermont, and USD 3 Billion for research and development (R&D) focused on advanced packaging, silicon photonics, and gallium nitride technologies. This strategic move aims to bolster U.S. semiconductor supply chain resilience and accelerate leadership in AI hardware.

- April 2025: United Microelectronics Corporation (UMC) officially inaugurated a new state-of-the-art fab expansion in Singapore’s Pasir Ris Wafer Fab Park. The initial phase, supported by up to USD 5 Billion investment, is scheduled to commence volume production in 2026 with a capacity of 30,000 wafers per month, supplementing UMC’s overall Singapore output to over one million wafers annually. Equipped with advanced 22nm and 28nm process technologies and GREEN Mark GoldPlus sustainability features, the facility strengthens UMC’s capability in serving AI, automotive, IoT, and communications markets.

- March 2025: TSMC announced plans to expand its U.S. semiconductor investments by an additional USD 100 Billion, bringing its total commitment to approximately USD 165 Billion. The additional funding will go toward building three new fabrication plants, two advanced packaging sites, and a large R&D center. The project is projected to create tens of thousands of high-tech jobs, create significant economic impact across Arizona and beyond, and reinforce U.S. leadership in the semiconductor supply chain.

- September 2024: India, in collaboration with the United States inaugurated its first semiconductor fabrication plant focused on national security aimed at producing chips for defense technologies and essential telecommunications. This initiative was revealed following discussions between Prime Minister Narendra Modi and U.S. President Joe Biden on September 21, 2024.

- September 2024: Tata Electronics is working on the development of two new semiconductor fabrication facilities in Dholera, Gujarat to enhance its chip manufacturing capabilities. The first facility, which has been under construction since March is set to commence operations in 2026 and will manufacture up to 50,000 wafers monthly for industries such as automotive, AI and wireless communication.

- November 2023: DB HiTek announced its entry into the ultra-high voltage (UHV) power semiconductor market by upgrading its UHV power semiconductor processing technology.

- October 2023: Fujitsu Semiconductor confirmed the successful establishment of the RIKEN RQC-Fujitsu Collaboration Center which has completed a new 64 qubit superconducting quantum computer.

- July 2023: TSMC celebrated the opening of its global research and development center in Hsinchu, Taiwan. The ceremony featured participation from customers, industry and academic R&D collaborators, design ecosystem partners and high-ranking government officials all gathered to commemorate the launch of the company's latest hub for advancing semiconductor technology.

Semiconductor Foundry Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technology Nodes Covered | 10/7/5nm, 16/14nm, 20nm, 45/40nm, Others |

| Foundry Types Covered | Pure Play Foundry, IDMs |

| Applications Covered | Communication, Consumer Electronics, Computer, Automotive, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | DB HiTek, GlobalFoundries, Hua Hong Semiconductor Limited, Intel Corporation, Powerchip Semiconductor Manufacturing Corporation, Samsung Semiconductor, Inc., Semiconductor Manufacturing International Corporation, Taiwan Semiconductor Manufacturing Company Limited, Tower Semiconductor Ltd., United Microelectronics Corporation, X-FAB Silicon Foundries SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the semiconductor foundry market from 2019-2033.

- The semiconductor foundry market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the semiconductor foundry industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The semiconductor foundry market was valued at USD 86.88 Billion in 2024.

IMARC estimates the semiconductor foundry market to reach USD 135.65 Billion exhibit a CAGR of 5.03% during 2025-2033.

Key drivers include rising demand for advanced electronics, adoption of 5G, AI, and IoT technologies, and the shift towards electric and autonomous vehicles. Government initiatives for localized production and advancements in smaller node technologies are creating a positive semiconductor foundry market outlook.

In 2024, Asia Pacific held the largest share of the Semiconductor Foundry Market, accounting for over 71.2%. This dominance is driven by the strong presence of major semiconductor manufacturers in countries like Taiwan, South Korea, and China, which are key hubs for semiconductor production and innovation.

Some of the major players in the semiconductor foundry market include DB HiTek, GlobalFoundries, Hua Hong Semiconductor Limited, Intel Corporation, Powerchip Semiconductor Manufacturing Corporation, Samsung Semiconductor, Inc., Semiconductor Manufacturing International Corporation, Taiwan Semiconductor Manufacturing Company Limited, Tower Semiconductor Ltd., United Microelectronics Corporation, X-FAB Silicon Foundries SE, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)