Security Information and Event Management (SIEM) Market Size, Share, Trends and Forecast by Component, Deployment Mode, Organization Size, Application, Industry Vertical, and Region, 2026-2034

Security Information and Event Management (SIEM) Market Size and Share:

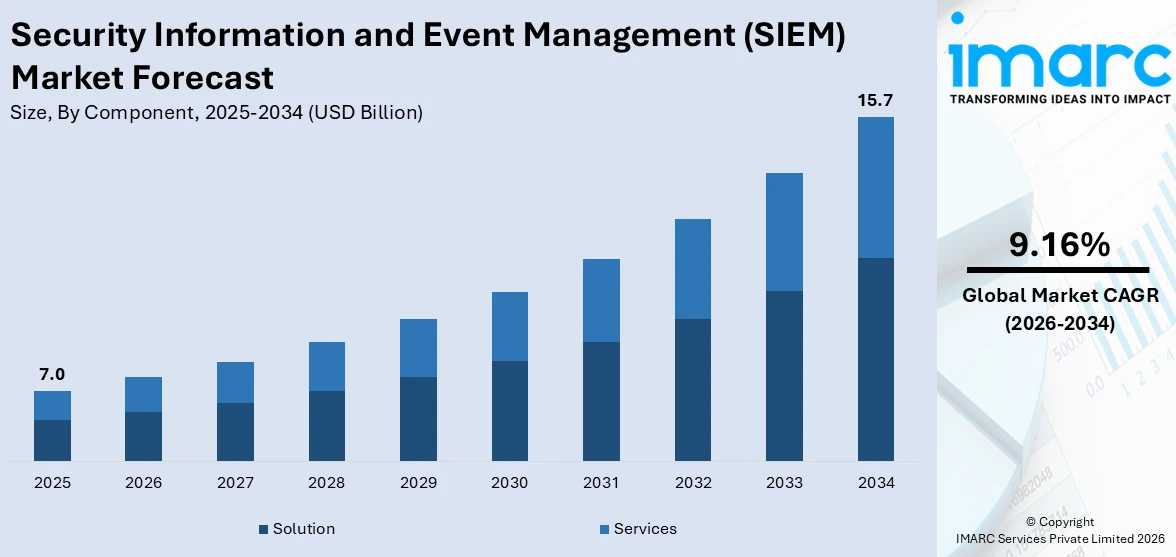

The global security information and event management (SIEM) market size was valued at USD 7.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 15.7 Billion by 2034, exhibiting a CAGR of 9.16% during 2026-2034. North America currently dominates the market, holding a significant market share of over 33.2% in 2025. The market is influenced by rising cyber threats, regulatory compliance mandates, and increasing cloud adoption. Organizations require real-time threat detection, log management, and advanced analytics to combat ransomware, insider threats, and APTs. AI-driven security automation, threat intelligence, and hybrid IT security solutions, accelerating the security information and event management (SIEM) market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 7.0 Billion |

|

Market Forecast in 2034

|

USD 15.7 Billion |

| Market Growth Rate (2026-2034) | 9.16% |

The market is fuled by increasing cyber threats, regulatory compliance mandates, and the need for real-time threat detection. Organizations face rising incidents of ransomware, insider threats, and advanced persistent threats (APTs), necessitating automated security monitoring and incident response. Validity requirements from GDPR and HIPAA and PCI-DSS and SOX push organizations toward implementing SIEM solutions for log management and reporting and auditing needs. The growth of cloud computing, IoT, and hybrid IT infrastructures increases the demand for scalable, AI-driven security solutions. Additionally, advancements in machine learning, behavioral analytics, and threat intelligence enhance SIEM capabilities, helping businesses detect, investigate, and mitigate security risks efficiently, further strengthening their market growth across industries.

To get more information on this market Request Sample

The SIEM market in the United States is propelled by rising cyber threats, increasing cloud adoption, and strict regulatory compliance requirements. Organizations face growing risks from ransomware, insider threats, and advanced persistent threats (APTs), necessitating real-time security monitoring and automated incident response. Regulatory frameworks like HIPAA, PCI-DSS, SOX, and CCPA mandate log management, threat detection, and reporting, boosting SIEM adoption. Additionally, the expansion of cloud computing, IoT, and hybrid IT environments increases the need for AI-driven security analytics and threat intelligence. Government and private sector investments in cybersecurity innovation, automation, and machine learning-based security solutions further strengthen the U.S. SIEM market growth. For instance, in November 2024, Kyndryl, the leading global provider of IT infrastructure services, launched a new range of offerings, created in partnership with Microsoft, aimed at improving cyber resilience for enterprises worldwide. Kyndryl and Microsoft expanded their fruitful, enduring collaboration to create unique, scalable security and resilience services. The new offerings are incorporated into Kyndryl Bridge, the top-tier, AI-driven, open-integration digital business platform in the industry. Merging Kyndryl’s extensive service knowledge with Microsoft’s security solutions offers companies a thorough strategy for protecting their activities against malicious threats and attacks.

Security Information and Event Management (SIEM) Market Trends:

Rising Cybersecurity Threats and Advanced Attacks

The increasing frequency of cyber threats such as phishing, ransomware, insider threats, and advanced persistent threats (APTs) is a key driver of the SIEM market. According to industry reports, in 2023, 66% of organizations experienced ransomware attacks. The exploitation of legitimate credentials represented 44.7% of data breaches. IoT malware attacks surged by 400% across different industries, with the manufacturing sector being the primary target worldwide. Organizations need real-time threat detection, security monitoring, and automated incident response to prevent data breaches and system compromises. SIEM solutions help identify anomalous activities, correlate security events, and provide rapid remediation to mitigate risks. As cybercriminals employ AI-driven attacks and sophisticated hacking techniques, businesses and governments are investing in AI-enhanced SIEM solutions to stay ahead of emerging threats and strengthen their overall cybersecurity posture.

Cloud Adoption and Hybrid IT Infrastructure Growth

The shift to cloud computing, hybrid IT environments, and remote work models has increased the demand for cloud-based SIEM solutions. Organizations using multi-cloud environments (AWS, Azure, Google Cloud) require real-time visibility, threat intelligence, and security orchestration to monitor complex infrastructures. Cloud-native SIEM platforms offer scalability, AI-driven analytics, and automated response capabilities, making them essential for securing hybrid workforces and cloud applications. As businesses continue adopting digital transformation strategies, IoT, and containerized applications, the need for scalable, cloud-integrated SIEM solutions is accelerating, creating a positive security information and event management (SIEM) market outlook. For instance, in July 2023, NTT DATA, a global leader in digital business and IT services, unveiled a new outsourcing service for security management (MDR service1) aimed at preventing incidents and reducing damage if incidents arise. The service will initially launch in Japan in July 2023, with a global rollout anticipated by the end of the fiscal year (March 2024). Through the MDR service, experienced security engineers with over 20 years in incident response from the company's CSIRT2 organization and knowledge gained from the Zero Trust Security Service offered globally by NTT DATA will assist client companies.

AI-Driven Security Analytics and Automation

Advancements in machine learning (ML), artificial intelligence (AI), and behavioral analytics are transforming SIEM capabilities. Modern SIEM platforms integrate AI-driven threat intelligence, anomaly detection, and automated incident response to improve security accuracy and reduce manual workload. AI-based SIEM solutions analyze massive security event logs, enabling proactive threat detection and predictive cybersecurity measures. Automation helps security teams prioritize alerts, detect threats faster, and mitigate risks efficiently, enhancing overall security operations center (SOC) performance. With organizations seeking real-time, AI-powered security analytics, the adoption of intelligent SIEM solutions is rapidly expanding across industries. For instance, in January 2025, TENEX.AI, an AI-driven cybersecurity firm, officially debuted intending to transform enterprise security. The firm receives support from notable investors, such as Andreessen Horowitz (a16z), Shield Capital, and top cybersecurity patrons. Its managed security services combine artificial intelligence, automation, and human expertise to provide cutting-edge security solutions.

Security Information and Event Management (SIEM) Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global security information and event management (SIEM) market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on component, deployment mode, organization size, application, and industry vertical.

Analysis by Component:

- Solution

- Services

The solution segment holds the largest share in the Security Information and Event Management (SIEM) market due to the increasing demand for real-time threat detection, incident response, and compliance management. Organizations prioritize automated security solutions to handle growing cyber threats, regulatory requirements, and complex IT infrastructures. SIEM solutions integrate log management, advanced analytics, AI-driven threat intelligence, and anomaly detection, enabling proactive security measures. The rise of cloud-based SIEM platforms, hybrid IT environments, and AI-powered security automation further boosts adoption. Additionally, enterprises prefer scalable, centralized security solutions that streamline security operations, reduce manual workload, and enhance cybersecurity resilience, driving market dominance.

Analysis by Deployment Mode:

- On-premises

- Cloud-based

On-premises leads the market with around 55.0% of the market share in 2025 due to organizations' preference for greater data control, security, and compliance adherence. Industries like banking, healthcare, and government handle sensitive data and require strict regulatory compliance, making on-premises deployments ideal for ensuring data sovereignty and reduced third-party risks. These solutions offer low-latency, real-time threat detection, and customization to meet specific security needs. Additionally, large enterprises with complex IT infrastructures prefer on-premises SIEM for its high-performance capabilities, direct network integration, and enhanced security posture, despite the rise of cloud-based alternatives

Analysis by Organization Size:

- Small and Medium-sized Enterprises

- Large Enterprises

Large enterprises lead the market with around 55.6% of market share in 2025 due to their complex IT environments, vast data volumes, and higher cybersecurity risks. These organizations face advanced persistent threats (APTs), regulatory compliance mandates, and data breach risks, necessitating robust SIEM solutions for real-time threat detection, incident response, and compliance management. Large enterprises also have dedicated security teams and higher budgets, enabling them to invest in AI-driven analytics, machine learning, and automation for proactive security monitoring. Additionally, their global operations, hybrid cloud infrastructures, and stringent governance requirements drive the need for scalable, enterprise-grade SIEM solutions.

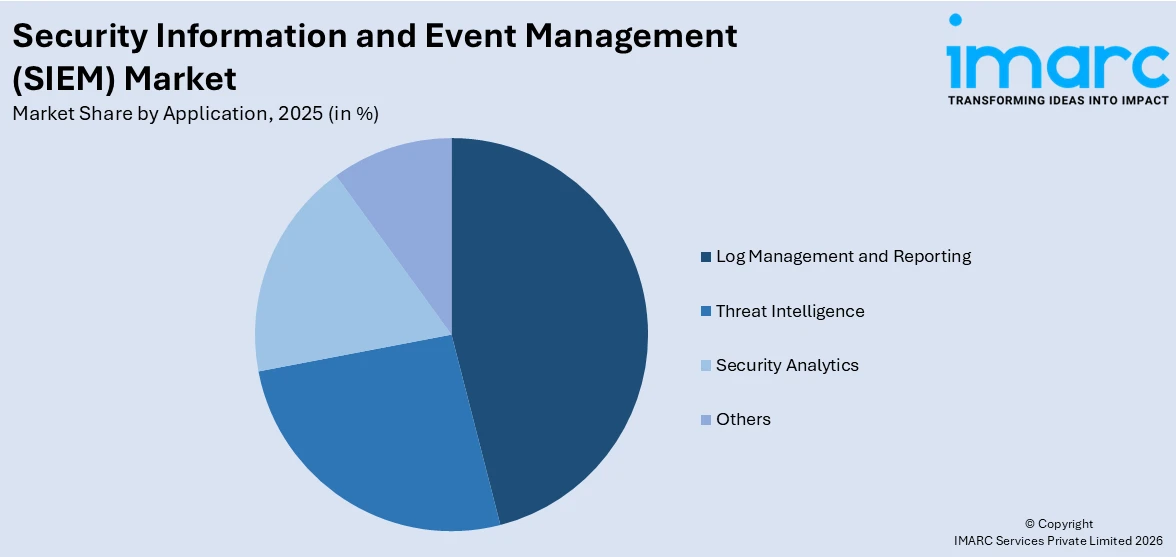

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Log Management and Reporting

- Threat Intelligence

- Security Analytics

- Others

Log management and reporting are expected to hold the largest share of the SIEM market due to the growing need for centralized log collection, storage, and analysis across enterprises. Organizations generate vast amounts of security logs, requiring efficient data aggregation, correlation, and forensic investigation to detect anomalies and security breaches. Compliance mandates like GDPR, PCI-DSS, and HIPAA further drive demand for automated reporting to ensure regulatory adherence. SIEM solutions enhance auditability, incident tracking, and operational visibility, making log management a critical security function.

Threat intelligence is a key driver in the SIEM market as organizations face increasingly sophisticated cyber threats such as zero-day attacks, ransomware, and APTs (Advanced Persistent Threats). SIEM platforms integrate real-time threat feeds, behavioral analytics, and machine learning to detect and mitigate risks proactively. By leveraging global threat databases and AI-driven pattern recognition, enterprises can identify malicious activities before they escalate. The demand for advanced threat correlation, automated incident response, and predictive security measures continues to grow, reinforcing threat intelligence as a core SIEM function.

Security analytics holds a significant share in the market due to its ability to provide deep insights into cyber threats, vulnerabilities, and anomalous behaviors. AI and machine learning-driven analytics help detect hidden attack patterns, insider threats, and potential breaches in real-time. Organizations increasingly rely on behavioral analysis, risk scoring, and anomaly detection to strengthen cybersecurity defenses. The rise of cloud security, IoT expansion, and hybrid IT infrastructures further drives demand for predictive and adaptive security analytics, making it an essential component of modern SIEM solutions.

Analysis by Industry Vertical:

- BFSI

- Government

- IT and Telecom

- Manufacturing

- Healthcare

- Retail

- Energy and Utilities

- Others

BFSI leads the market with around 19.9% of the market share in 2025 due to its high vulnerability to cyber threats, regulatory compliance mandates, and critical data protection needs. BFSI institutions handle large volumes of sensitive financial data, making them prime targets for fraud, phishing, ransomware, and insider threats. SIEM solutions help in real-time threat monitoring, anomaly detection, and incident response to safeguard financial transactions and customer information. Regulatory frameworks like PCI-DSS, GDPR, and RBI guidelines further drive SIEM adoption. Additionally, AI-driven fraud detection and advanced security analytics strengthen BFSI cybersecurity defenses.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 33.2%. The market in North America is driven by rising cyber threats, stringent regulatory compliance requirements, and increasing adoption of AI-driven security solutions. Organizations face advanced persistent threats (APTs), ransomware, and insider attacks, necessitating real-time threat detection and response. Compliance frameworks like HIPAA, PCI-DSS, and CCPA mandate robust log management, reporting, and security analytics. The region’s high cloud adoption, digital transformation, and IoT expansion further drive SIEM demand. Additionally, growing investments in AI-powered cybersecurity, automation, and threat intelligence strengthen market growth, as enterprises seek scalable, proactive security solutions to mitigate evolving risks.

Key Regional Takeaways:

United States Security Information and Event Management (SIEM) Market Analysis

In 2025, the United States accounted for over 85.00% of the security information and event management (SIEM) market in North America. The growing security information and event management (SIEM) adoption due to the growing penetration of cloud-based technology is significantly shaping the cybersecurity landscape. According to reports, 98% of U.S. organizations have adopted cloud technology for business operations. The increasing demand for cloud-driven security solutions is driving organizations to enhance real-time threat detection and compliance management. As businesses transition their operations to cloud-based environments, security information and event management (SIEM) adoption continues to rise, ensuring robust data security across dynamic IT infrastructures. Advanced cloud-native security information and event management (SIEM) platforms are enabling automated threat analysis and rapid incident response, reducing cyberattack risks. The need for scalable and integrated cybersecurity frameworks is fuelling investments in security information and event management (SIEM), enhancing network visibility and proactive risk mitigation. Regulatory compliance requirements and growing sophistication in cyber threats are pushing enterprises toward comprehensive security information and event management (SIEM) adoption. The evolving hybrid work model further accelerates the necessity for security information and event management (SIEM) to safeguard remote and distributed cloud-based operations.

Asia Pacific Security Information and Event Management (SIEM) Market Analysis

Growing security information and event management (SIEM) adoption due to growing small and medium-sized enterprises is intensifying cybersecurity strategies across expanding digital ecosystems. According to India Brand Equity Foundation, the number of MSMEs in the country is projected to grow from 6.3 crore to around 7.5 crore at a CAGR of 2.5%. The rapid digitalization of Small and Medium-sized Enterprises necessitates scalable security solutions, driving the security information and event management (SIEM) demand to address rising cyber risks. As Small and Medium-sized Enterprises increasingly integrate cloud-based operations and digital platforms, security information and event management (SIEM) adoption are becoming a fundamental component of cybersecurity strategies. The need for real-time monitoring, compliance adherence, and automated threat detection is propelling Small and Medium-sized Enterprises to invest in security information and event management (SIEM) solutions. Heightened cyber vulnerabilities due to limited in-house IT security expertise are further accelerating security information and event management (SIEM) adoption. Cost-effective, cloud-based security information and event management (SIEM) offerings are catering to Small and Medium-sized Enterprises, enhancing cybersecurity postures while optimizing operational efficiencies.

Europe Security Information and Event Management (SIEM) Market Analysis

Growing security information and event management (SIEM) adoption due to growing BFSI facilities is significantly transforming cybersecurity frameworks. According to reports, in 2021, the EU had 784 branches of foreign banks, with 619 originating from other EU Member States and 165 from non-EU countries. The expansion of BFSI facilities necessitates stringent security measures to combat sophisticated cyber threats and ensure regulatory compliance. Security information and event management (SIEM) solutions are being widely implemented across BFSI facilities to enhance fraud detection, secure digital transactions, and monitor real-time financial data. The increasing digital transformation of BFSI facilities is driving investments in security information and event management (SIEM), enabling automated risk assessment and anomaly detection. Growing reliance on digital banking and online financial services is escalating cybersecurity concerns, fuelling security information and event management (SIEM) adoption to safeguard sensitive financial data. With BFSI facilities handling vast volumes of transactions, security information and event management (SIEM) adoption is critical in minimizing financial fraud and ensuring compliance with stringent regulatory mandates.

Latin America Security Information and Event Management (SIEM) Market Analysis

Growing security information and event management (SIEM) adoption due to growing Infrastructure due to growing Healthcare sector is transforming cybersecurity dynamics. As reported by the Brazilian Federation of Hospitals (FBH) and the National Confederation of Health (CNSaúde), out of Brazil's 7,191 hospitals, 62% are privately owned. The expansion of healthcare sector infrastructure demands enhanced security information and event management (SIEM) solutions to mitigate cyber threats and safeguard critical patient data. The increasing digitalization of healthcare sector services necessitates real-time security monitoring and automated incident response, accelerating security information and event management (SIEM) adoption. Advanced security information and event management (SIEM) platforms are enabling proactive threat detection, ensuring compliance with evolving cybersecurity regulations. The growing integration of cloud-based medical systems and telehealth services is further driving security information and event management (SIEM) demand.

Middle East and Africa Security Information and Event Management (SIEM) Market Analysis

Growing security information and event management (SIEM) adoption due to growing investment in IT and Telecom is reshaping cybersecurity measures. For instance, total expenditure on information and communications technology (ICT) in the Middle East, Türkiye, and Africa (META) will exceed USD 238 Billion this year, reflecting a 4.5% rise compared to 2023. Expanding IT and Telecom investments necessitate security information and event management (SIEM) solutions to address evolving cyber threats and regulatory compliance requirements. The rapid deployment of digital infrastructure and 5G networks is amplifying security vulnerabilities, and accelerating security information and event management (SIEM) adoption. Increased investment in cloud computing and data centers is further driving the demand for security information and event management (SIEM), ensuring real-time security monitoring.

Competitive Landscape:

The security information and event management (SIEM) market is highly competitive, with key players focusing on AI-driven analytics, cloud-based SIEM solutions, and real-time threat intelligence. Leading vendors include International Business Machines Corporation, Splunk LLC, Sumo Logic, and Exabeam. These companies compete on advanced security automation, compliance management, scalability, and integration capabilities. With rising cyber threats, regulatory mandates, and cloud adoption, vendors are enhancing machine learning, behavioral analytics, and hybrid IT security features. Startups and niche players are disrupting the market with cost-effective, AI-powered solutions. Partnerships and acquisitions further shape the competitive landscape, as companies aim to strengthen their SIEM offerings amid growing cybersecurity demands.

The report provides a comprehensive analysis of the competitive landscape in the security information and event management (SIEM) market with detailed profiles of all major companies, including:

- CrowdStrike

- Elasticsearch B.V.

- Exabeam

- Fortinet, Inc.

- International Business Machines Corporation

- Logpoint

- OpenText Corporation

- Securonix

- SolarWinds Worldwide, LLC

- Splunk LLC

- Sumo Logic

- Trend Micro Incorporated

Latest News and Developments:

- February 2025: SentinelOne is expanding its AI-powered SIEM strategy, partnering to drive growth in cloud and data security. Channel Chief Brian Lanigan highlights a unique approach differentiating it from competitors. The company is rapidly evolving beyond endpoint security into broader security operations.

- December 2024: Datadog unveiled its modern Cloud SIEM, enhancing risk-based insights, scalability, and real-time threat detection. Unlike traditional SIEMs, it eliminates the need for dedicated staff, streamlining security operations. By leveraging machine learning and modern architectures, it reduces alert fatigue and operational costs. This approach democratizes security practices, making cloud-scale threat management more efficient.

- October 2024: Exabeam, the leading pure-play SIEM vendor, unveiled LogRhythm Intelligence, combining AI-driven analytics with its self-hosted SIEM for enhanced threat detection. The latest release offers flexibility across self-hosted, cloud-native, and hybrid environments, accelerating security teams’ workflows. Exabeam’s commitment to innovation ensures global organizations stay ahead of evolving cyber threats.

- August 2024: Kyndryl has launched a Security Operations Center (SOC) in Bengaluru, India, offering advanced cyber threat protection with AI-driven automation. The SOC features SIEM for real-time security event monitoring, threat hunting, and compliance support. As India's cyber risks grow, Kyndryl’s hybrid model allows businesses to selectively or fully outsource cybersecurity operations.

- August 2024: Securonix has launched Cyber Data Fabric and Noise Canceling SIEM within its AI-Reinforced EON suite to enhance cyber threat response. These innovations empower security teams to streamline operations, reduce costs, and counter AI-powered attacks effectively. As the first AI-Reinforced SIEM provider, Securonix aims to improve speed, precision, and efficiency in cybersecurity.

Security Information and Event Management (SIEM) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solution, Services |

| Deployment Modes Covered | On-premises, Cloud-based |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Applications Covered | Log Management and Reporting, Threat Intelligence, Security Analytics, and Others |

| Industry Verticals Covered | BFSI, Government, IT and Telecom, Manufacturing, Healthcare, Retail, Energy and Utilities, and Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | CrowdStrike, Elasticsearch B.V., Exabeam, Fortinet, Inc., International Business Machines Corporation, Logpoint, OpenText Corporation, Securonix, SolarWinds Worldwide, LLC, Splunk LLC, Sumo Logic, Trend Micro Incorporated, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the security information and event management (SIEM) market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global security information and event management (SIEM) market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the security information and event management (SIEM) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Security Information and Event Management (SIEM) Market Report

The security information and event management (SIEM) market was valued at USD 7.0 Billion in 2025.

The security information and event management (SIEM) market is projected to exhibit a CAGR of 9.16% during 2026-2034, reaching a value of USD 15.7 Billion by 2034.

The market is driven by rising cyber threats, regulatory compliance requirements, and increasing cloud adoption. Organizations need real-time threat detection, AI-driven security analytics, and automated incident response. Additionally, the demand for hybrid IT security, managed security services, and advanced threat intelligence is accelerating SIEM adoption across industries globally.

North America currently dominates the security information and event management (SIEM) market, accounting for a share of 33.2%. The market is driven by rising cyber threats, regulatory compliance, AI-driven analytics, cloud adoption, and automated threat detection.

Some of the major players in the security information and event management (SIEM) market include CrowdStrike, Elasticsearch B.V., Exabeam, Fortinet, Inc., International Business Machines Corporation, Logpoint, OpenText Corporation, Securonix, SolarWinds Worldwide, LLC, Splunk LLC, Sumo Logic and Trend Micro Incorporated.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)