Saudi Arabia Power EPC Market Size, Share, Trends and Forecast by Type and Region, 2026-2034

Saudi Arabia Power EPC Market Summary:

The Saudi Arabia power EPC market size was valued at USD 6.79 Billion in 2025 and is projected to reach USD 9.85 Billion by 2034, growing at a compound annual growth rate of 4.22% from 2026-2034.

The Saudi Arabia power EPC market is experiencing robust expansion as the Kingdom accelerates its energy infrastructure transformation under Vision 2030. Government-led initiatives promoting renewable energy development, smart grid modernization, and strategic partnerships with international firms are driving substantial investments in power generation and distribution projects. Advances in utility-scale solar installations, combined cycle gas turbine plants, and battery energy storage systems are reshaping the energy landscape, positioning the Kingdom as a regional leader in sustainable power infrastructure and strengthening the Saudi Arabia power EPC market share.

Key Takeaways and Insights:

- By Type: Oil and Gas dominate the market with a share of 36% in 2025, reflecting the Kingdom's strategic investments in combined cycle gas turbine power plants that support grid stability while reducing emissions through cleaner fuel alternatives.

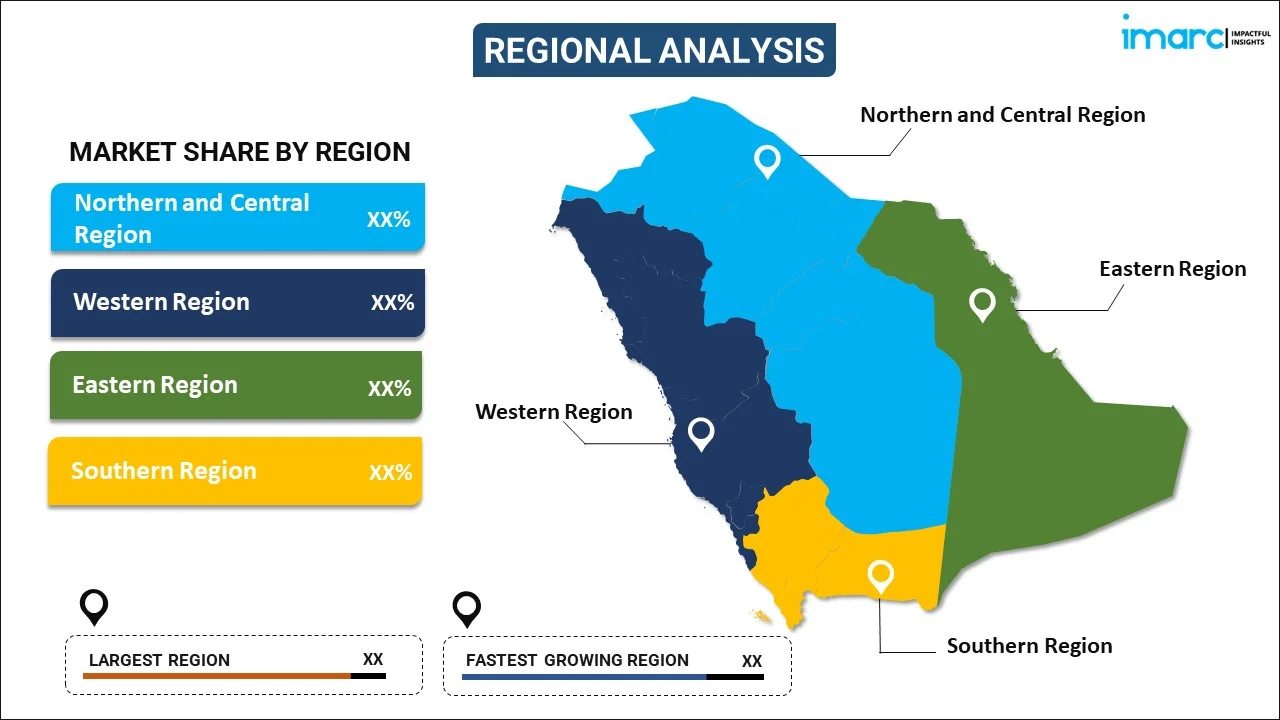

- By Region: Northern and Central region leads the market with a share of 36% in 2025, driven by Riyadh's strategic importance as the capital, concentration of major industrial activities, and significant government infrastructure investment programs.

- Key Players: The Saudi Arabia power EPC market exhibits a dynamic competitive landscape with international engineering giants, regional contractors, and specialized energy firms actively participating. Companies are leveraging strategic partnerships, advanced technologies, and localization initiatives to secure major contracts across thermal, renewable, and energy storage projects throughout the Kingdom.

The Saudi Arabia power EPC market is advancing rapidly as the government prioritizes energy infrastructure modernization and diversification. Rising electricity demand, driven by population growth and industrial expansion, continues to fuel investment in new power generation capacity. The National Renewable Energy Program is accelerating the deployment of utility-scale solar and wind projects, while smart grid initiatives enhance distribution network efficiency. For instance, in July 2025, ACWA Power, Badeel, and Saudi Aramco Power Company signed power purchase agreements for seven renewable energy projects totaling 15 GW of combined solar and wind capacity, representing an investment of approximately USD 8.3 billion. This landmark initiative demonstrates the scale of ongoing EPC opportunities as the Kingdom pursues its target of generating half its electricity from renewables and half from gas by 2030, transforming the energy sector through sustainable infrastructure development.

Saudi Arabia Power EPC Market Trends:

Rapid Expansion of Utility-Scale Renewable Energy Projects

The Kingdom is witnessing unprecedented growth in utility-scale solar and wind installations as part of its energy transition strategy. Large-scale photovoltaic plants and onshore wind farms are being developed across multiple provinces, supported by favorable solar irradiance conditions and competitive land costs. The government's streamlined procurement processes are attracting international EPC contractors seeking to capitalize on gigawatt-scale project opportunities. In September 2025, Saudi Arabia launched a 5.3 GW renewable energy tender under Round 7 of the National Renewable Energy Program, driving competition and innovation among EPC contractors across solar and wind sectors.

Smart Grid Modernization and Digital Transformation

Saudi Arabia is investing heavily in smart grid technologies to enhance energy management and grid reliability. Advanced metering infrastructure, automation systems, and digital monitoring solutions are being integrated across the national electricity network. These initiatives support renewable energy integration while improving operational efficiency and reducing transmission losses. By the end of 2025, distribution network automation reached approximately 40%, with plans to develop nine advanced control centers by 2026, supporting the Saudi Arabia power EPC market growth through comprehensive infrastructure upgrades.

Battery Energy Storage System Integration

Energy storage deployment is gaining momentum as Saudi Arabia strengthens grid stability and addresses the intermittency of renewable energy generation. Large-scale battery storage systems are being adopted to support peak load management and improve the overall reliability of electricity supply. This shift is expanding the role of EPC contractors, who are increasingly responsible for the design, construction, and commissioning of integrated energy storage solutions. As storage becomes a core component of power infrastructure planning, EPC capabilities are evolving to deliver flexible, resilient, and future-ready grid systems aligned with the Kingdom’s long-term energy transition objectives. For instance, in December 2025, Technology firm Sungrow announced that three battery energy storage system projects with a combined capacity of 7.8 GWh are now operational on Saudi Arabia’s power grid. Located in Najran, Khamis Mushait, and Madaya, the projects use more than 1,500 PowerTitan 2.0 units and were delivered in partnership with EPC contractor Algihaz Holding.

How Vision 2030 is Transforming the Saudi Arabia Power EPC Market:

Saudi Arabia’s Vision 2030 is reshaping the power EPC market by accelerating diversification, sustainability, and private-sector participation. Large-scale investments in renewable energy, particularly solar and wind, are driving demand for advanced EPC capabilities, supported by programs such as the National Renewable Energy Program (NREP). Simultaneously, grid modernization, energy storage projects, and smart transmission infrastructure are expanding EPC scopes beyond conventional thermal power. Vision 2030’s localization goals are encouraging technology transfer, local manufacturing, and workforce development, increasing competition among domestic and international EPC players. Public–private partnerships, regulatory reforms, and long-term power purchase agreements are further improving project bankability, positioning the Saudi power EPC market for sustained growth. For instance, in June 2024, as part of its Vision 2030 agenda, Saudi Arabia finalized multiple major power purchase agreements for large-scale solar developments. These agreements represent an important step in the Kingdom’s strategy to diversify its energy mix, lower dependence on fossil fuels, and strengthen its role in the global transition toward renewable energy.

Market Outlook 2026-2034:

The Saudi Arabia power EPC market outlook remains highly positive as the Kingdom continues its ambitious energy transformation agenda. Ongoing investments in renewable energy generation, combined cycle gas turbine facilities, and power grid infrastructure are expected to maintain a strong pipeline of projects. The government’s long-term clean energy transition goals are creating significant opportunities for EPC companies across engineering, procurement, and construction activities. In parallel, the growing integration of energy storage solutions is expanding project scope and complexity, allowing EPC players to diversify their portfolios while supporting grid flexibility, reliability, and the evolving needs of the national power system. The market generated a revenue of USD 6.79 Billion in 2025 and is projected to reach a revenue of USD 9.85 Billion by 2034, growing at a compound annual growth rate of 4.22% from 2026-2034.

Saudi Arabia Power EPC Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Oil and Gas |

36% |

|

Region |

Northern and Central Region |

36% |

Type Insights:

To get Detailed analysis of this market, Request Sample

- Thermal

- Oil and Gas

- Renewable

- Nuclear

- Others

Oil and gas dominates with a market share of 36% of the total Saudi Arabia power EPC market in 2025.

The oil and gas segment maintains its dominant position in the Saudi Arabia power EPC market through ongoing investments in combined cycle gas turbine power plants. These efficient facilities are replacing aging oil-fired stations while supporting the Kingdom's goal of transitioning to gas and renewables for electricity generation. EPC contractors are executing major projects featuring advanced turbine technologies that enhance operational efficiency and reduce carbon emissions. In March 2025, Siemens Energy secured a USD 1.6 billion project to provide key technologies for the Rumah 2 and Nairyah 2 gas-fired power plants, adding 3.6 gigawatts of capacity to the national grid.

Gas-fired power generation continues to attract substantial EPC investment as the Kingdom develops its natural gas resources and infrastructure. Projects under the Master Gas System expansion are enhancing fuel supply capabilities while new combined cycle plants are being constructed in strategic locations across the country. These developments align with Saudi Arabia's strategy to reduce liquid fuel consumption in electricity generation and optimize the energy mix. The ongoing development of the Jafurah unconventional gas field, expected to produce 2 billion cubic feet per day by 2030, will further strengthen the gas-to-power segment.

Regional Insights:

To get Detailed analysis of this market, Request Sample

- Northern and Central Region

- Western Region

- Eastern Region

- Southern Region

The Northern and Central region leads with a share of 36% of the total Saudi Arabia power EPC market in 2025.

The Northern and Central region maintains market leadership driven by Riyadh's strategic importance as the national capital and primary economic hub. The concentration of industrial activities, government institutions, and residential developments creates sustained demand for power infrastructure investment. Major power generation and transmission projects are being executed in this region to meet growing electricity consumption. The Rumah combined cycle power plant project, located in Riyadh Province, exemplifies the scale of ongoing EPC activities, with construction underway on facilities designed to enhance grid capacity and reliability.

Infrastructure development initiatives under Vision 2030 are concentrated in the central provinces, driving substantial EPC contract awards for both conventional and renewable power projects. The region is also witnessing the deployment of advanced grid infrastructure, including smart meters and automated distribution systems. Major renewable energy projects, including the Afif 1, Afif 2, Starah, and Shaqra solar and wind plants in Riyadh Province, representing a combined capacity exceeding 7 GW, demonstrate the region's growing role in sustainable energy development.

Market Dynamics:

Growth Drivers:

Why is the Saudi Arabia Power EPC Market Growing?

Vision 2030 Energy Diversification Strategy

Saudi Arabia’s Vision 2030 is reshaping the energy sector by prioritizing renewable energy expansion and improved energy efficiency. Through the National Renewable Energy Program, the government is steering the transition toward cleaner power sources, creating strong momentum for large-scale renewable projects. This strategic focus is driving significant EPC opportunities in utility-scale solar installations, onshore wind developments, and associated grid and support infrastructure, positioning EPC contractors at the center of the Kingdom’s long-term energy transformation. Government procurement programs are streamlining project development while attracting international investment. In July 2025, the Saudi Power Procurement Company tendered projects totaling 43.2 GW, with 38.7 GW of power purchase agreements signed, demonstrating the program's momentum.

Rising Electricity Demand and Grid Expansion

Saudi Arabia is experiencing sustained growth in electricity consumption driven by population expansion, urbanization, and industrial development. Peak electricity demand has been growing at rates between seven and nine percent annually, necessitating continuous investment in new generation capacity and grid infrastructure. The government is investing in transmission network expansion and distribution system upgrades to ensure reliable power delivery across the Kingdom. Smart grid technologies are being deployed to optimize energy management and integrate variable renewable generation. By 2024, Saudi Arabia had installed over 11 million smart meters across the Kingdom since 2021, contributing to improved energy efficiency and enabling consumers to monitor consumption patterns.

Strategic International Partnerships and Technology Transfer

The Saudi Arabia power EPC market benefits from extensive collaboration between domestic entities and leading international technology providers. Strategic partnerships facilitate access to advanced engineering capabilities, modern construction methodologies, and cutting-edge power generation technologies. Foreign direct investment in the energy sector supports knowledge transfer and local workforce development. These collaborations are enabling execution of increasingly complex megaprojects while building in-country capabilities. In October 2025, Energy China and PowerChina secured EPC contracts valued at USD 4.3 billion for gigawatt-scale renewable energy projects in Saudi Arabia, reflecting the scale of international partnership opportunities.

Market Restraints:

What Challenges the Saudi Arabia Power EPC Market is Facing?

High Initial Capital Investment Requirements

Large-scale power EPC projects in Saudi Arabia require substantial upfront capital investment, often exceeding one billion dollars for major facilities. Securing project financing can present challenges, particularly during periods of economic uncertainty. High capital costs can limit market entry for smaller EPC contractors and affect project timelines when funding arrangements require extended negotiation periods.

Skilled Workforce Availability

The booming growth in power infrastructure development also poses a great need for well-qualified engineers, technicians, and construction professionals. The shortage of specialized local talent forces contractors to employ an expatriate labor force as they invest in training and development schemes. The development of local domestic technical capacity is an ongoing process, which localization efforts aim to accomplish, albeit in the long run.

Supply Chain and Regulatory Complexities

Global supply chain disruptions can affect procurement timelines and equipment costs for power EPC projects. Navigating the complex regulatory landscape, which includes environmental compliance, permitting requirements, and local content mandates, requires significant administrative resources. These factors can impact project schedules and require comprehensive risk management strategies from EPC contractors.

Competitive Landscape:

The Saudi Arabia power EPC market features intense competition among domestic contractors, regional engineering firms, and international conglomerates. Market participants are differentiating through technological capabilities, project execution track records, and strategic partnerships. Companies are actively pursuing localization strategies to meet in-Kingdom value-add requirements while building local supply chains and workforce capabilities. Joint ventures between international technology providers and Saudi firms are increasingly common, combining global expertise with local market knowledge. Competition is particularly strong in renewable energy segments where multiple contractors are vying for utility-scale solar and wind project awards, while established players maintain positions in conventional thermal power generation through long-standing relationships and proven performance.

Recent Developments:

- November 2025: At ADIPEC 2025, GE Vernova Inc. (NYSE: GEV) announced that the Jafurah Cogeneration Independent Steam and Power Plant (ISPP), situated about 125 kilometers southeast of Dammam, Saudi Arabia, has commenced commercial operations. GE Vernova delivered a comprehensive solution, supplying the plant’s core power equipment, including its 7HA.01 gas turbine, along with a 20-year service agreement covering maintenance, parts supply, and full lifecycle management of the turbine.

- February 2025: BYD Energy Storage signed contracts with Saudi Electricity Company to deliver 12.5 GWh across five battery storage projects, marking the world's largest grid-scale storage deployment. The systems will be installed using BYD's MC Cube-T energy storage system with Cell-to-System technology.

Saudi Arabia Power EPC Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Thermal, Oil and Gas, Renewable, Nuclear, Others |

| Regions Covered | Northern and Central Region, Western Region, Eastern Region, Southern Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The Saudi Arabia power EPC market size was valued at USD 6.79 Billion in 2025.

The Saudi Arabia power EPC market is expected to grow at a compound annual growth rate of 4.22% from 2026-2034 to reach USD 9.85 Billion by 2034.

Oil and gas represent the largest revenue share of 36% in 2025, driven by ongoing investments in combined cycle gas turbine power plants that support grid stability, improve generation efficiency, and align with the Kingdom's strategy to transition from oil-fired power generation.

Key factors driving the Saudi Arabia power EPC market include Vision 2030 energy diversification initiatives, rising electricity demand from population and industrial growth, expanding renewable energy capacity, smart grid modernization investments, and strategic international partnerships enabling technology transfer.

Major challenges include high initial capital investment requirements for large-scale projects, limited availability of skilled local workforce requiring training investments, supply chain disruptions affecting equipment procurement, and regulatory complexities involving environmental compliance and permitting processes.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)