Robotic Vacuum Cleaner Market Size, Share, Trends and Forecast by Type, Type of Charging, Distribution Channel, Application, End User, and Region, 2026-2034

Robotic Vacuum Cleaner Market Size and Share:

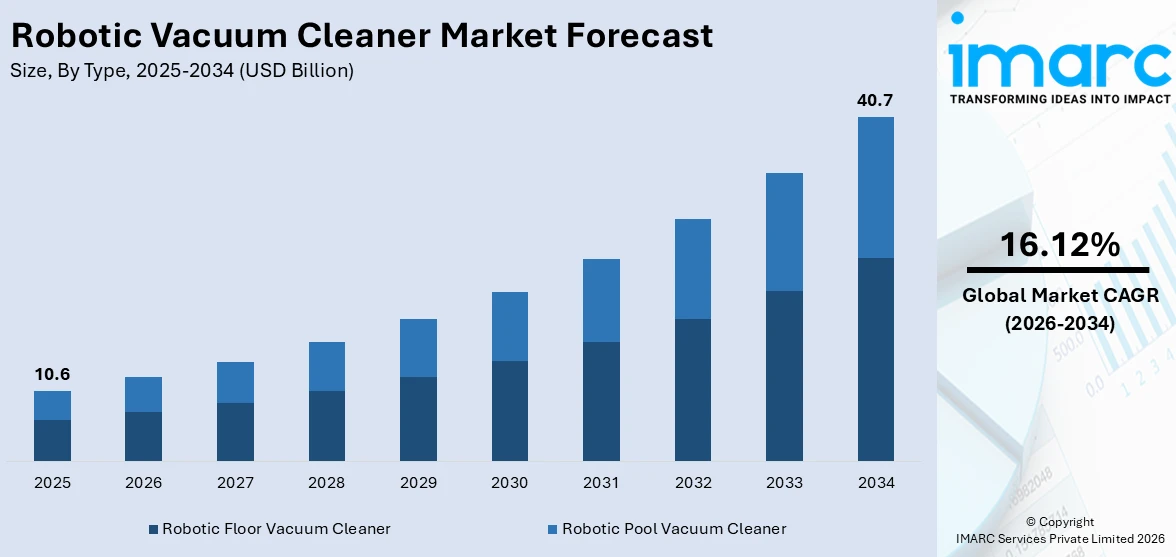

The global robotic vacuum cleaner market size reached USD 10.6 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 40.7 Billion by 2034, exhibiting a growth rate (CAGR) of 16.12% during 2026-2034. Asia Pacific currently dominates the robotic vacuum cleaner market revenue, holding a market share of over 40.8% in 2025. The increasing demand for automated cleaning solutions, rising awareness of time-saving smart home devices, and technological advancements in navigation are some of the factors positively impacting the robotic vacuum cleaner market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 10.6 Billion |

| Market Forecast in 2034 | USD 40.7 Billion |

| Market Growth Rate 2026-2034 | 16.12% |

The robotic vacuum cleaner market is boosted by rising consumer demand for smart home devices offering convenience and automation. Artificial intelligence and IoT adoption in appliances have enhanced robotic vacuum cleaner features such as efficient navigation, remote control and advanced cleaning capabilities. For instance, in September 2024, Dreame Technology launched the X40 Ultra robot vacuum and mop for Indian market. Features include 12,000 Pa suction side reach technology and a 7-in-1 auto base station for self-maintenance. Increasing disposable incomes and busy lifestyles further fuel demand for these time-saving solutions. The rise in pet ownership and heightened awareness of indoor air quality have contributed to their popularity. Ecofriendly designs and technological innovations such as voice command integration are also acting as key factors driving robotic vacuum cleaner market growth.

To get more information on this market Request Sample

The United States robotic vacuum cleaner market is driven by the rising requirement for smart home technologies and automation solutions supported by advancements in artificial intelligence and IoT. Increasing adoption of these devices is linked to busy lifestyles, growing pet ownership and heightened awareness of indoor cleanliness and air quality. For instance, in March 2024, Dyson's new robot vacuum the 360 Vis Nav launched in the US. It boasts 65 air watts of suction and a 360-degree camera for navigation and HEPA filtration. Enhanced features such as voice command compatibility, efficient navigation systems, and self-charging capabilities appeal to tech-savvy consumers. Furthermore, a growing focus on sustainability and energy efficiency aligns with consumer preferences contributing to the adoption of robotic vacuum cleaners across the U.S.

Robotic Vacuum Cleaner Market Trends:

Rising Demand for Convenience

The growing need for convenience in their daily lives is increasing the robotic vacuum cleaner market demand. Due to frequent time constraints, modern customers look for automated solutions to make their domestic activities easier. An easy and efficient way to clean is using a robotic cleaner. When their batteries run low, they may automatically return to their docking stations, traverse across areas, and clean various floor surfaces. Unprecedented convenience is offered by the ability to remotely operate these devices and schedule cleanings through smartphone apps. The adoption of these devices is being driven by the increasing demand for a hands-free and effective cleaning solution, especially from busy homes and working professionals with demanding schedules. Moreover, An industrial report suggests that the global workforce is projected to increase by 1.1% in 2024, which is also infusing the demand.

Rapid Advancements in Technology

Continual technological advancements are enhancing the robotic vacuum cleaner market outlook. The parts and functionalities of these devices are actively being advanced by the manufacturers. Precise and effective cleaning patterns are made possible by sophisticated positioning systems like simultaneous localization and mapping (SLAM) and laser mapping. Additionally, enhanced sensor technology helps robots recognize obstacles and avoid collisions. Algorithms using artificial intelligence (AI) can evaluate data to customize cleaning paths and adjust to various floor types. Better user experiences are also enhanced by inventions like self-emptying trash cans and longer-lasting batteries. These cleaners are now more user-friendly and appealing to a larger audience due to technical advancements that also increase cleaning performance overall and promote market growth. To save even more time and convenience, some of the newest robot vacuums now mop as they vacuum. For instance, Roborock's, a company manufacturing robot vacuums announced that vacuum cleaners come with vibrating mop pads that employ "sonic technology to scrub floors up to 3,000 times per minute."

Increasing hygiene and health awareness

There was an outgrowing necessity to ensure hygiene and health owing to the COVID-19 pandemic which is a significant robotic vacuum cleaner market growth driver. As a result, people started to ensure a safe and healthy environment in both their homes and working spaces. The most useful and productive tool for ensuring timely and consistent cleaning to preserve hygiene and health is a robotic vacuum cleaner. These tools are useful for eliminating stains, dust, allergies, and much more from indoor spaces. Moreover, it offers a versatile hands-free operational feature that prevents coming in direct contact with contaminated surroundings. The robotic vacuum cleaners have become an essential tool in our daily lives to maintain sanitation and hygiene in the working and personal space, increasing their usage for residential and commercial purposes. Multiple organizations are working in this field. UNICEF’s 2030 Agenda for Sustainable Development calls on UN member states to take decisive action to "no one will be left behind," "realise the human rights of all," "shift the world onto a sustainable and resilient path," and "end poverty in all its forms."

Robotic Vacuum Cleaner Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, and regional levels for 2026-2034. Our report has categorized the robotic vacuum cleaner market segmentation based on type, type of charging, distribution channel, application, and end user.

Analysis by Type:

- Robotic Floor Vacuum Cleaner

- Robotic Pool Vacuum Cleaner

Robotic vacuum cleaner leads the market with around 60.7% of the market share in 2025.

Robotic floor vacuums are home cleaning tools made to extract dust, debris, and allergens from a variety of floor types, including tile, hardwood, and carpet. Conventional floor vacuums usually need to be operated by hand, which involves moving the appliance across the floor and pushing it. Furthermore, the need for automation and ease in cleaning procedures has contributed to the growth of robotic vacuum cleaners. These cleaners are self-contained appliances with sensors, artificial intelligence algorithms, and brushes that can move about and clean floors without the need for human assistance. The market has expanded due to this shift in cleaning practices towards automation. Customers want these gadgets as they can plan cleanings, operate them from a distance, and take advantage of hands-free floor cleaning, all of which save time and hassle. Modern homes are increasingly choosing these cleaners due to their increased efficiency and convenience, leading to widespread adoption.

Analysis by Type of Charging:

- Manual Charging

- Automatic Charging

Manual charging lead the market with around 63.0% of the market share in 2025. Manual recharging in the robotic vacuum cleaner industry is a basic version of charging, mostly in entry-level products. The device requires a user to manually connect it to the recharging station, which does not have an auto-recharge feature. It cuts down the overall cost and thus is a popular option for budget-conscious buyers. They are also generally more compact as they do not need docking stations, which makes them suitable for smaller living spaces. These models are often more affordable and suited for users who don't mind actively monitoring battery levels. While they lack the convenience of automated systems, manual charging vacuums are reliable and straightforward. They are popular among cost-conscious consumers who prioritize simplicity over advanced features, making them a practical option for smaller homes or less frequent cleaning needs.

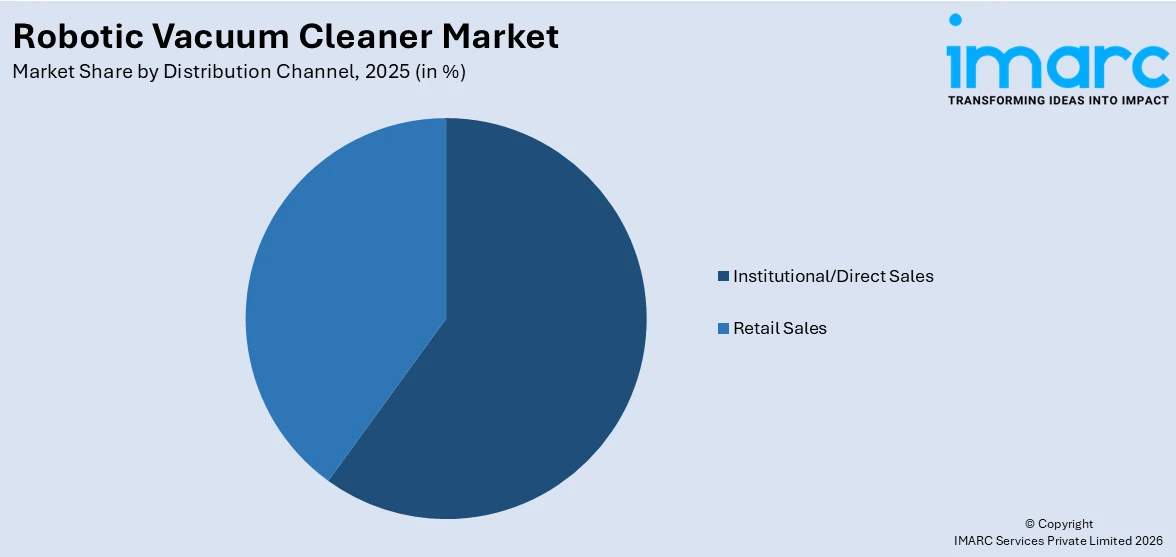

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Institutional/Direct Sales

- Retail Sales

Institutional or direct sales channels involve selling robotic vacuum cleaners directly to businesses, organizations, or consumers without intermediaries. This approach is common for bulk orders by hotels, offices, or large institutions needing customized cleaning solutions. Direct sales allow manufacturers to maintain control over pricing, branding, and customer relationships, offering tailored packages or post-sale services. While more common in commercial applications, this channel appeals to consumers seeking personalized purchasing experiences or deals unavailable through traditional retail outlets.

Retail sales involve distributing robotic vacuum cleaners through authorized dealers, physical stores, and e-commerce platforms. This channel provides broad market accessibility, enabling consumers to compare brands, features, and prices conveniently. Retail sales dominate the consumer segment, as they cater to individual buyers looking for quick and straightforward purchasing options. With advancements in online shopping, e-commerce platforms have significantly expanded the reach of robotic vacuums, offering discounts, user reviews, and doorstep delivery, making them a popular choice for modern shoppers.

Analysis by Application:

- Vacuum Cleaning Only

- Vacuum Cleaning and Mopping

Robotic vacuum cleaners designed solely for vacuuming focus on efficiently removing dirt, dust, and debris from various floor types. These models often come with powerful suction, advanced navigation, and programmable cleaning schedules, making them ideal for routine maintenance in homes or offices. Without additional features like mopping, they are generally more cost effective and elementary to operate. Their simplicity appeals to users who prioritize effective vacuum cleaning over multifunctionality, making them a practical choice for those with primarily carpeted or hard floors.

Robotic vacuum cleaners with both vacuuming and mopping capabilities offer an all-in-one solution for maintaining clean floors. These models can vacuum dirt and debris while also mopping away spills and stains, making them suitable for homes with hard flooring. Equipped with dual functionalities, they provide a deeper clean, saving time and effort. Popular among households with children or pets, these versatile devices are ideal for those seeking comprehensive cleaning solutions, although they typically come at a higher price point.

Analysis by End User:

- Residential

- Commercial

- Hospitality

- Offices

- Healthcare

- Retail

- Others

Residential leads the market with around 68.9% of the market share in 2025 as consumers are increasingly demanding convenience, automation, and smart home integration. The residential market caters to households seeking automated cleaning solutions for daily maintenance. These devices are designed to handle a variety of surfaces, including carpets, hardwood, and tile floors, making them ideal for homes with children or pets. Features like scheduled cleaning, app control, and compact designs add convenience for busy homeowners. With affordability and ease of use driving demand, robotic vacuums are becoming a popular choice for enhancing cleanliness without the need for manual effort. The numerous improvements in artificial intelligence (AI), app controls, and voice assistant compatibility increase the adoption rate. Rising disposable incomes and urbanization boost the market, especially in areas with a higher proportion of dual-income households. The segment expands further as people seek convenience, efficiency, and hygiene, supporting the role of robotic vacuum cleaners in modern household maintenance.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- Europe

- North America

- Asia Pacific

- Middle East and Africa

- Latin America

In 2025, Asia Pacific accounted for the largest robotic vacuum cleaner market share of over 40.8%.

Asia Pacific held the largest market share. This is due to the region's rapid urbanization and growing middle class, which raises demand for contemporary home appliances that provide convenience and time-saving benefits. robotic vacuum cleaners are a popular option for busy urban lifestyles. The demand of these devices in residential and commercial places has increased due to the growing awareness of cleanliness and hygiene. In addition, competitive pricing by the robotic vacuum cleaner industry top manufacturers in several Asia Pacific nations, such as China and South Korea, has made these cleaners more affordable for a wider range of consumers. Furthermore, technological developments, especially in the areas of AI and sensors, are propelling product innovation and improving cleaning effectiveness, which is supporting market expansion in the Asia Pacific area.

Key Regional Takeaways:

North America Robotic Vacuum Cleaner Market Analysis

The North American robotic vacuum cleaner market is driven by rising consumer demand for convenience, increasing adoption of smart home technology, and robust disposable incomes. The region's tech-savvy population embraces advanced features like AI-based navigation, LiDAR mapping, and voice control through Alexa or Google Home. The surge in dual-income households necessitates time-saving automated cleaning solutions. Additionally, rising pet ownership and allergy concerns are fueling the demand for pet-friendly and HEPA-filter-equipped robotic vacuums. Online retail channels dominate sales due to competitive pricing and convenience, further supporting market growth in North America.

United States Robotic Vacuum Cleaner Market Analysis

In 2025, the United States captured 87.90% of the North American market. Rising demand for convenience among US customers, adoption of smart home technology, and high disposable income drive the market for robotic vacuum cleaners in the United States. Robotic vacuums are one of the most common types of smart home appliances, with about 70% of American homes owning one, according to data from key market player Evovacs. More than half of robotic vacuum owners in the United States reported that time saving was the reason for buying this product as of 2023. According to an industrial report, rising dual-income households account for 53% of married families in 2019, and such families face a need for automated cleaning solutions. Functional innovations including voice control compatibility with Alexa and Google Home, LiDAR mapping, and AI integration, attract and appeal to the most technically savvy consumers. Furthermore, HEPA-filtering robotic vacuums are becoming more and more popular, meeting the needs of the 60 million Americans who have allergies, as per the data by Centre for Disease Control and Prevention. The need for vacuums made to manage pet hair has increased due to the growing trend of pet ownership, with 70% of American homes keeping pets, as per the data by American Pet Products Association. More and more, most sales of the robotic vacuum are going through e-commerce sites as these give a convenient competitive price.

Europe Robotic Vacuum Cleaner Market Analysis

The growth of the robotic vacuum cleaner market in Europe is driven primarily by the increasing urbanisation of the region, increasing demands for eco-friendly energy-saving solutions, and increased smart home appliances popularity. With more than 75% of the population living in cities, Europe has one of the greatest rates of urbanisation in the world, which has raised demand for portable and effective cleaning products. European consumers are more concerned about the environment, which has led to a desire for energy-efficient robotic vacuums that are frequently certified by the EU's Eco-label. Industry reports suggest that penetration rates for smart home technologies are more than 30% in countries such as Germany and the UK. With such massive market penetration, there is an immense demand for smart, high-tech robotic vacuums that come equipped with features like LiDAR and AI-based obstacle detection. Moreover, the ease and less physical straining in terms of time for cleaning aspects are some significant factors driving Europe's acceptance, where more than 20% have crossed the age of 65.

Latin America Robotic Vacuum Cleaner Market Analysis

Urbanization, additional disposable income, and growing awareness of smart home technology are the main drivers for the Latin American robotic vacuum cleaner industry. For countries such as Brazil and Mexico, where more than 80% of the population stays in cities, small, efficient cleaning solutions for apartment dwellers become essential. According to an industrial report, the sales of e-commerce robotic vacuum increased by 25% year over year due to webstores like MercadoLibre. With the surge in middle-class income levels, premium cars with advance features like smartphone control or AI navigation have become easy to afford. The popularity of pet-friendly models also caters to the needs of pet-owning households, which account for half the families in the region.

Middle East and Africa Robotic Vacuum Cleaner Market Analysis

The primary drivers of growth for the robotic vacuum cleaner market in the Middle East and Africa are growing urbanization, the adoption of smart homes, and demand for automated solutions. According to several reports, smart home actions for almost 130 million were performed; over 100 million requests, such as to listen to music, Quran, or podcasts, Alexa users had for KSA and UAE alone in the year 2023 itself, thus achieving over 70 million hours of listening. Africa's urbanization rates, which will reach 50% and 60% by 2030 and 2050 respectively, according to African Development Bank statistics, are pushing demand for modern cleaning products. Pet-friendly vacuum models also become popular due to the increasing rate of pet ownership in the region. In addition, robotic vacuum cleaners become more accessible because of increasing online retail outlets like Jumia and Noon.

Competitive Landscape:

Due to the outstanding developments launched by major players in the robotic vacuum cleaner business to improve this cleaning equipment, the market is growing steadily. The development of sophisticated AI-driven navigation systems allows robots to mop and clean floors more quickly while skillfully dodging obstacles. Self-emptying dustbins on some versions eliminates the requirement for regular user interaction. Furthermore, these cleaners can also be blended with voice assistants, smartphone apps, and smart home ecosystems, offering consumers more ease of use and control. Intelligent navigation and cleaning of various spots within a home have been made possible by robots equipped with room recognition and multi-floor mapping technologies. Besides, enhancements in battery technology have resulted in longer runtimes and quicker charging periods. Together, these cutting-edge characteristics improve the robotic cleaners' performance, adaptability, and user-friendliness, thereby solidifying their position as essential household cleaning appliances.

The robotic vacuum cleaner forecast report has provided a comprehensive analysis of the competitive landscape. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- iRobot Corporation

- ECOVACS ROBOTICS

- Neato Robotics

- Dyson Ltd.

- Samsung Electronics Co. Ltd.

- Maytronics Ltd.

- Metapo, Inc

- Koninklijke Philips N.V.

- LG Electronics Inc.

- Panasonic Corporation

- Miele & Cie. KG

- Hayward Industries, Inc.

- Haier Electronics Group Co Ltd

- Sharp Corporation

- ILIFE Robotics Technology

- Vorwerk & Co. KG

- Taurus Group

- Groupe Seb Deutschland Gmbh

- Pentair plc

- bObsweep Inc.

Latest News and Developments:

- October 2024: Kärcher has introduced autonomous cleaning devices, including robotic vacuum cleaners, as part of its strategy to expand its operations in India. With the use of automation and smart technological developments, the company hopes to meet the region's increasing need for creative cleaning solutions.

- January 2024: iRobot Corporation and Amazon have announced that they have mutually decided to cancel their earlier announced acquisition agreement, which was initially signed on August 4, 2022.

- January 2024: ECOVACS ROBOTICS introduced the next generation of comprehensive home robotics, featuring groundbreaking robots designed for maintaining floors, air, ceilings, windows, and lawns.

Robotic Vacuum Cleaner Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Robotic Floor Vacuum Cleaner, Robotic Pool Vacuum Cleaner |

| Types of Charging Covered | Automatic Charging, Manual Charging |

| Distribution Channels Covered | Institutional/Direct Sales, Retail Sales |

| Applications Covered | Vacuum Cleaning Only, Vacuum Cleaning and Mopping |

| End Users Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | iRobot Corporation, ECOVACS ROBOTICS, Neato Robotics, Dyson Ltd., Samsung Electronics Co. Ltd., Maytronics Ltd., Metapo, Inc, Koninklijke Philips N.V., LG Electronics Inc., Panasonic Corporation, Miele & Cie. KG, Hayward Industries, Inc., Haier Electronics Group Co Ltd, Sharp Corporation, ILIFE Robotics Technology, Vorwerk & Co. KG, Taurus Group, Groupe Seb Deutschland Gmbh, Pentair plc, bObsweep Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, robotic vacuum cleaner market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global robotic vacuum cleaner market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the robotic vacuum cleaner industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The robotic vacuum cleaner market was valued at USD 10.6 Billion in 2025.

The robotic vacuum cleaner market is projected to exhibit a CAGR of 16.12% during 2026-2034, reaching a value of USD 40.7 Billion by 2034.

The market is driven by the increasing demand for smart home devices, advancements in automation technology, and the growing need for convenience in daily cleaning tasks. Additionally, improvements in battery life, suction power, and affordability are further fueling market growth.

Asia Pacific currently dominates the robotic vacuum cleaner market, accounting for a share of 40.8% in 2025. The dominance is fueled by high adoption rates in countries like Japan and China, growing urbanization, increasing disposable income, and rising demand for automated home appliances in the region.

Some of the major players in the robotic vacuum cleaner market include iRobot Corporation, ECOVACS ROBOTICS, Neato Robotics, Dyson Ltd., Samsung Electronics Co. Ltd., Maytronics Ltd., Metapo, Inc, Koninklijke Philips N.V., LG Electronics Inc., Panasonic Corporation, Miele & Cie. KG, Hayward Industries, Inc., Haier Electronics Group Co Ltd, Sharp Corporation, ILIFE Robotics Technology, Vorwerk & Co. KG, Taurus Group, Groupe Seb Deutschland Gmbh, Pentair plc, bObsweep Inc., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)