Retinoblastoma Treatment Market Size, Share, Trends and Forecast by Type, Treatment Type, Type of Staging, Application, and Region, 2025-2033

Retinoblastoma Treatment Market Size and Share:

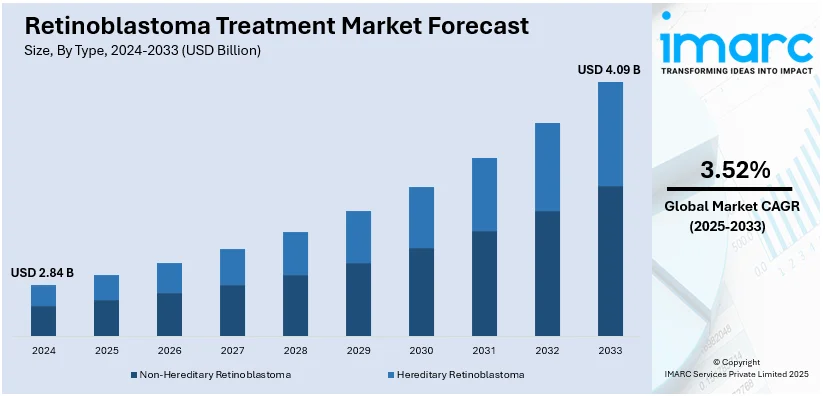

The global retinoblastoma treatment market size was valued at USD 2.95 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 4.09 Billion by 2033, exhibiting a CAGR of 3.52% from 2025-2033. Asia Pacific currently dominates the market. A significant increase in healthcare expenditure for ophthalmic treatment procedures, increased investments in R&D activities on therapies with lower side effects, and the growing health consciousness are some of the major factors driving the market in this region.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 2.95 Billion |

|

Market Forecast in 2033

|

USD 4.09 Billion |

| Market Growth Rate 2025-2033 | 3.52% |

The global retinoblastoma treatment market is experiencing significant growth due to advancements in early detection, improved therapies and increased awareness about the condition. Innovations in genetic testing and imaging technologies have enabled earlier diagnosis leading to better treatment outcomes. The growing availability of targeted therapies and advancements in chemotherapy, radiation and laser treatments have enhanced survival rates and reduced side effects. The rising incidence of retinoblastoma in pediatric populations particularly in emerging markets is also driving market demand. Increasing investments in research and development (R&D) for novel therapies coupled with government initiatives to support pediatric cancer treatment are fueling the market’s expansion. The overall improvement in healthcare infrastructure and access to specialized care further supports the growth trajectory of this market.

The growth of the retinoblastoma treatment market in the USA is being driven by several key factors including advancements in early detection, cutting-edge therapies and increased awareness. Early diagnosis is made possible by improvements in imaging technologies and genetic screening which are critical for managing this rare pediatric cancer. The National Cancer Institute (NCI) reports that retinoblastoma affects approximately 300 new children annually in the U.S. Innovations in treatments such as intra-arterial chemotherapy and targeted therapies are improving outcomes as survival rates for retinoblastoma have risen significantly. The rising prevalence of genetic mutations linked to the disease has spurred the development of personalized medicine options. Government and private sector investments in pediatric oncology research alongside increasing awareness campaigns are also contributing to market growth. As healthcare access improves and precision medicine continues to evolve the retinoblastoma treatment market in the USA is expected to expand further.

Retinoblastoma Treatment Market Trends:

Advancements in Targeted Therapies and Immunotherapies

Retinoblastoma is reported by the National Cancer Institute to be about 1 in 15,000 to 20,000 live births globally, thereby presenting a case for developing alternative treatments. Advancements in targeted therapies and immunotherapies will be prominent enough to propel growth in the retinoblastoma treatment market. In terms of rare cancers, treatments such as drugs like selinexor, branded as Xpovio, and ceritinib, known by its commercial name Zykadia, are further enhancing options. Such targeted therapies for retinoblastoma-related genetic mutations are showing promising outcomes in preclinical settings, and combinations are proving to have enhanced survival advantages. With this in mind, such therapy offers optimism for improved outcome and provides hope in a scenario with limited access to advanced therapy.

Increasing Incidence Rates

According to the American Cancer Society, about 200 to 300 new cases of retinoblastoma are diagnosed every year in the United States. This is a rising trend that calls for better treatment options, thereby increasing demand and consequently fueling growth in the market. As genetic predispositions to retinoblastoma have become better understood and earlier detection techniques have improved, the importance of targeted therapy has gained more prominence. Early diagnosis enhances the survival chances, and with better screening programs being in place, more and more children are being diagnosed at earlier stages. Thus, this will be more beneficial in treating the condition through intra-arterial chemotherapy, laser therapy, and cryotherapy, etc., which is expected to increase the rate of successful treatment and grow the market. Awareness regarding genetic screening programs is anticipated to spur demand for treatment in the near future.

Growing Focus on Personalized Medicine

The retinoblastoma treatment market is increasingly turning towards personalized medicine. In this context, the focus is more on genetic profiling of patients for designing treatment regimens. As per an industry report, the personalized medicine market was estimated to be approximately USD 512 Billion globally in 2022. The article in the Journal of Clinical Oncology points out that mutations in the RB1 gene are now becoming an important biomarker in developing specific treatment strategies for retinoblastoma. In this direction, pharmaceutical companies are also trying to work on precision therapies so that treatment efficacy can be increased. The use of genetic testing in predicting patient response to chemotherapy and other targeted therapies will be expected to spur the growth of this market. In addition, there are expectations that clinical trials related to RB1 gene therapies and other related technologies will continue to rise in numbers since they are bound to ensure more effective, fewer side effects, treatments that better fit the present-day shift toward precision medicine in various parts of the world.

Retinoblastoma Treatment Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global retinoblastoma treatment market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on type, treatment type, type of staging, and application.

Analysis by Type:

- Non-Hereditary Retinoblastoma

- Hereditary Retinoblastoma

In 2024, non-hereditary retinoblastoma is expected to represent the largest segment of the retinoblastoma treatment market. This is because the non-hereditary form of the disease is more common than the hereditary form, which affects children with no family history of retinoblastoma. Non-hereditary retinoblastoma is usually diagnosed in children under five years of age, and its incidence is increasing due to enhanced diagnostic methods, including advanced imaging and genetic testing. Advances in the availability of targeted therapies and the use of personalized treatment approaches such as chemotherapy, laser therapy, and cryotherapy have been shown to have contributed to improved treatment outcomes, as well as growing demand for the medical treatment involved. Recognition of non-hereditary retinoblastoma and improvements in treatment methods, therefore, should lead to increasing dominance by the segment in 2024, a development reflecting trends in ongoing advancement in pediatric oncology and practices in early detection.

Analysis by Treatment Type:

- Surgery

- Radiation Therapy

- Laser Therapy (Photocoagulation)

- Cryotherapy

- Thermotherapy

- Chemotherapy

- Opthalmic Artery Infusion Chemotherapy

- High-Dose Chemotherapy and Stem Cell Transplant

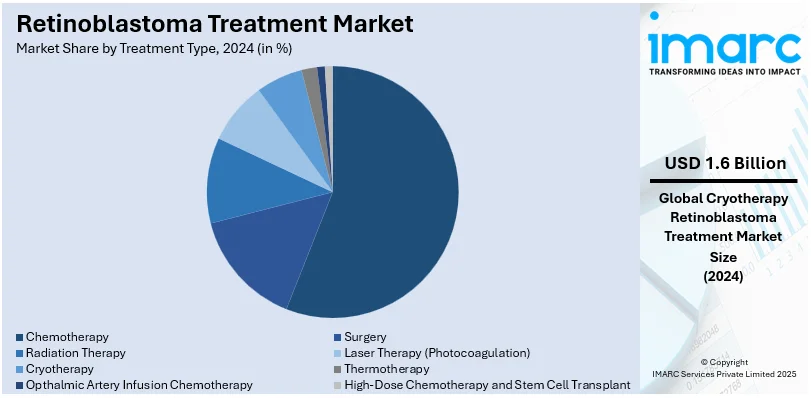

By 2024, chemotherapy is anticipated to have a leading market share of around 55.8% for the retinoblastoma treatment market. To date, it remains the bedrock in both hereditary and non-hereditary retinoblastoma, particularly with tumors too large to be addressed locally with treatments like laser therapy or cryotherapy. Chemotherapy causes tumors to become small enough that they may easily be surgically excised or other treatments administered. Intra-arterial chemotherapy, which focuses on a higher dose delivery into the affected eye, is one of the primary reasons why chemotherapy has taken center stage in this market. More research has continually improved chemotherapy protocols and minimized the side effects that patients suffer while undergoing therapy, making chemotherapy remain the best course of treatment for many. This will strengthen further in 2024, considering that survival rates are rising while the effectiveness of therapy improves.

Analysis by Type of Staging:

- Intraocular Retinoblastoma

- Extraocular Retinoblastoma

Intraocular retinoblastoma is likely to be the most common retinoblastoma treatment which holds the highest market share in 2024. It is the most common presentation, especially at an early stage of diagnosis, wherein the tumor remains confined to the eye without spreading to other parts of the body. Intraocular retinoblastoma is generally associated with higher survival rates and better treatment outcomes because it can often be treated effectively with localized therapies such as chemotherapy, laser therapy, and cryotherapy. Advances in early detection methods, including genetic screening and advanced imaging techniques, have led to more cases being identified in their intraocular stage, further driving its dominance in the market. Preservation of vision along with minimizing the side effects on children has further led to high demand for the treatments specific to intraocular retinoblastoma, hence solidifying it as the biggest market segment.

Analysis by Application:

- Hospitals

- Cancer Institutes

- Others

The biggest segment in the retinoblastoma treatment market is hospitals that provide all aspects of diagnosis, treatment, and follow-up. Hospitals are provided with modern diagnostic equipment and have multidisciplinary teams for wide-ranging therapies: chemotherapy, laser treatment, and surgery.

The institutes specialize in rare cancers, such as retinoblastoma, and offer advanced therapies and individualized care. These institutions are focused on research, early detection, and advanced treatment options and often provide clinical trials for innovative therapies, thereby driving significant market growth.

The other category includes outpatient clinics, ambulatory surgical centers, and specialized pediatric care centers. These provide alternate or supplemental therapy to retinoblastoma patients and mainly involve less aggressive therapies, rehabilitation, and after-care services for patients.

Regional Analysis:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

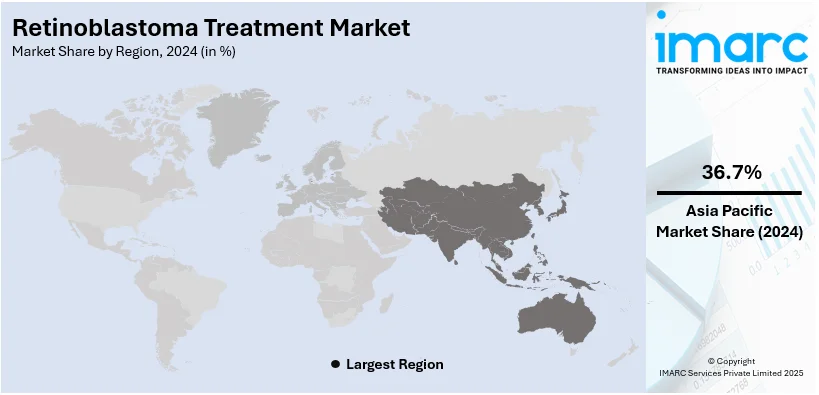

In 2024, Asia Pacific accounted for the largest market share. This growth is primarily driven by the large pediatric population in the region, increasing awareness of retinoblastoma, and improvements in healthcare infrastructure. Emerging economies like China, India, and Southeast Asian countries are witnessing enhanced access to advanced diagnostic and treatment facilities, boosting early detection and treatment of retinoblastoma. The increased prevalence of pediatric cancers in these countries, and the government efforts made to better cancer care, are advancing this market. In addition, affordable treatment options, alongside growing medical research, will further propel the region to dominance. Combined with these factors, Asia Pacific is an important market for retinoblastoma treatment, with a rapidly increasing demand for expertise in pediatrics and oncology.

Key Regional Takeaways:

North America Retinoblastoma Treatment Market Analysis

The growth of the retinoblastoma treatment market in North America is driven by the progress in early diagnosis, improved treatment options, and high healthcare spending. In particular, the United States benefits from cutting-edge technologies such as genetic screening and advanced imaging, which enable early detection and more effective treatment of retinoblastoma. According to the American Cancer Society, retinoblastoma affects approximately 250-350 children annually in the U.S.. Moreover, the availability of advanced treatments such as intra-arterial chemotherapy and targeted therapies has improved survival rates and minimized long-term side effects. The U.S. also has a strong focus on pediatric cancer research, with significant funding from organizations like the National Cancer Institute (NCI), which supports innovation in retinoblastoma care. High standards of healthcare, availability of specialized pediatric oncology centers, and government initiatives to improve the infrastructure for cancer care further propel the growth of the market in North America, making it a leading region for retinoblastoma treatment.

United States Retinoblastoma Treatment Market Analysis

The U.S. retinoblastoma treatment market is constantly increasing due to medical technology upgrades and increased awareness of earlier diagnoses. According to the American Cancer Society, in 2023, there was a total of around 200 new cases of retinoblastoma a year in the U.S. This rare pediatric form of cancer creates demand for unique forms of treatment, with the most common being chemotherapy, laser therapy, and gene therapy. The FDA approvals of new targeted therapies and emerging immunotherapies have created huge growth in the market further. The main players engaged within the U.S. marketplace includes Novartis along with Regeneron Pharmaceuticals engaged in research for newest developments. The ongoing studies through clinical trials are finding some personalized treatments, enriching the whole treatment panorama, and increased research funding accompanied with a specific focus upon pediatrics and oncology drives further development. Finally, precision medicine will power next growth.

Europe Retinoblastoma Treatment Market Analysis

The retinoblastoma treatment market in Europe is continuously growing due to improvements in the early diagnosis and better treatment avenues. According to American Academy of Ophthalmology, the number of live births affected by retinoblastoma has only slightly increased from 1 in every 15,000–18,000 to 1 in every 14,000 in Europe; this trend is resulting in a higher demand for treatments that are specialized, and chemotherapy, laser therapy, and gene therapy are emerging as some of the most important solutions. In the last few years, the European Medicines Agency has approved several innovative treatments, thereby increasing the availability of treatments. Moreover, an increasing academic-industry collaboration is currently driving innovative therapies, and such therapies include gene therapy and new chemotherapeutic regimens. As such, the adoption of severe healthcare regulations by European countries has increased patient access to innovative treatments, thereby allowing the market to grow.

Asia Pacific Retinoblastoma Treatment Market Analysis

According to a research article, the Asia Pacific region bears a significant global burden of retinoblastoma, with approximately 43% (3,452 of 8,099 children) of the global RB burden residing in six countries within the region. In India, there are 1,486 children diagnosed with RB, followed by China with 1,103 children, Indonesia with 277 children, Pakistan with 260 children, Bangladesh with 184 children, and the Philippines with 142 children. This region has disparities in the technological and socio-economic factors. As a result, it leads to different clinical presentations and survival rates. This is not only true for technology but also in the social aspects in developing nations. This provides opportunities for research, especially in studying these socio-economic aspects to come up with culturally relevant and economically feasible interventions. These include education about the disease, universal screening, subsidized treatment for the poor, and developing specialty centers with tele-ophthalmology services.

Latin America Retinoblastoma Treatment Market Analysis

The Latin American retinoblastoma treatment market is growing, primarily driven by improved access to health care and the growing prevalence of pediatric cancer. According to 28 Population-Based Cancer Registries (PBCR) in Brazil, from 2000 to 2018, a total of 675 children and adolescents aged 0 to 19 years received a diagnosis of retinoblastoma, making up 2.2% of all cancer diagnoses in that age group. This highlights a vast burden of retinoblastoma in this area, especially in Brazil. The growing access of initial diagnostic tools such as an eye screening program allows increased treatment success rates with added market potential. Another good reason is the rising interest between local pharmaceutical firms and some international players for research towards affordable therapies in place and chemotherapy and laser treatment as alternatives. Governments in Brazil and Argentina are investing in specialized healthcare infrastructure to enhance patient access to care, thus making a positive outlook for the retinoblastoma treatment market in the region.

Middle East and Africa Retinoblastoma Treatment Market Analysis

In the Middle East and Africa, the retinoblastoma treatment market is expanding steadily, boosted by improvement in pediatric oncology care and an increase in health care access. According to a research article, an estimated 9,000 new cases of retinoblastoma are diagnosed annually in Africa, which depicts a massive burden of this disease in the region. Countries such as South Africa and the UAE have developed healthcare infrastructure much better than before, which can help detect the disease much earlier and also access more treatment options. However, in rural areas, the accessibility of proper care is lacking. The government and NGOs are working towards creating awareness and providing all the necessary requirements for the treatment. Advanced therapies such as gene therapies and novel chemotherapies, which have been on an investment trend, will also boost future growth in the Middle East and African markets.

Competitive Landscape:

The competitive landscape of the retinoblastoma treatment market is marked by a mix of established pharmaceutical companies, emerging biotech firms, and research institutions focused on innovative therapies. Traditional treatments, such as chemotherapy, laser therapy, and cryotherapy, continue to dominate the market, with leading players like Roche and Novartis offering chemotherapy regimens. However, there is a growing shift toward targeted therapies, gene therapy, and immunotherapies, which are expected to drive market growth in the coming years. Companies are exploring novel approaches to improve survival rates and reduce long-term complications. Additionally, collaborations between academic institutions and biotech companies are accelerating the development of new treatments. While access to specialized care remains a challenge in developing regions, early diagnosis and advancements in treatment options are boosting the market’s potential.

The report provides a comprehensive analysis of the competitive landscape in the retinoblastoma treatment market with detailed profiles of all major companies, including:

- Bristol Myers Squibb Company

- Pfizer Inc.

- Teva Canada Limited (Teva Pharmaceutical Industries Ltd.)

Latest News and Developments:

- October 2024: Aileron Therapeutics and Advancium Health Network have agreed to exclusively acquire ALRN-6924, and the respective option agreement was signed on October 31, 2024. Advancium will study the medicine as a future treatment for the rare pediatric eye cancer retinoblastoma.

- August 2024: VCN-01 received the rare pediatric disease designation of the FDA for the treatment of the orphaned eye cancer, retinoblastoma. Previous to this, VCN-01 received orphan drug designation for this indication as a stroma-degrading oncolytic adenovirus.

- June 2024: Scientists at the Optics and Photonics Research Center in Brazil, along with scientists at the University of Toronto and Princess Margaret Cancer Center, reported that pulsed laser phototherapy successfully eliminated ocular melanoma in mice. It works by giving a drug that is activated with short pulses of intense light.

Retinoblastoma Treatment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Non-Hereditary Retinoblastoma, Hereditary Retinoblastoma |

| Treatment Types Covered | Surgery, Radiation Therapy, Laser Therapy (Photocoagulation), Cryotherapy, Thermotherapy, Chemotherapy, Opthalmic Artery Infusion Chemotherapy, High-Dose Chemotherapy and Stem Cell Transplant |

| Type of Stagings Covered | Intraocular Retinoblastoma, Extraocular Retinoblastoma |

| Applications | Hospitals, Cancer Institutes, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bristol Myers Squibb Company, Pfizer Inc., Teva Canada Limited (Teva Pharmaceutical Industries Ltd.), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the retinoblastoma treatment market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global retinoblastoma treatment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the retinoblastoma treatment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The retinoblastoma treatment market was valued at USD 2.95 Billion in 2024.

The retinoblastoma treatment market is projected to exhibit a CAGR of 3.52% during 2025-2033.

A considerable rise in healthcare expenditure for ophthalmic treatment procedures, increasing investments in research and development (R&D) activities on therapies with lower side effects, and the increasing health consciousness represent some of the key factors driving the market.

Asia Pacific currently dominates the market, driven by the growing rates of recurrence of retinoblastoma, higher diagnosis and treatment rates due to the increasing awareness regarding different types of cancers, the presence of several key players in the region, etc.

Some of the major players in the retinoblastoma treatment market include Bristol Myers Squibb Company, Pfizer Inc., Teva Canada Limited (Teva Pharmaceutical Industries Ltd.), etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)