Residential Energy Storage System Market Size, Share, Trends and Forecast by Technology Type, Power Rating, Ownership Type, Connectivity Type, and Region, 2026-2034

Global Residential Energy Storage System Market Size, Share, Trends & Forecast (2026-2034)

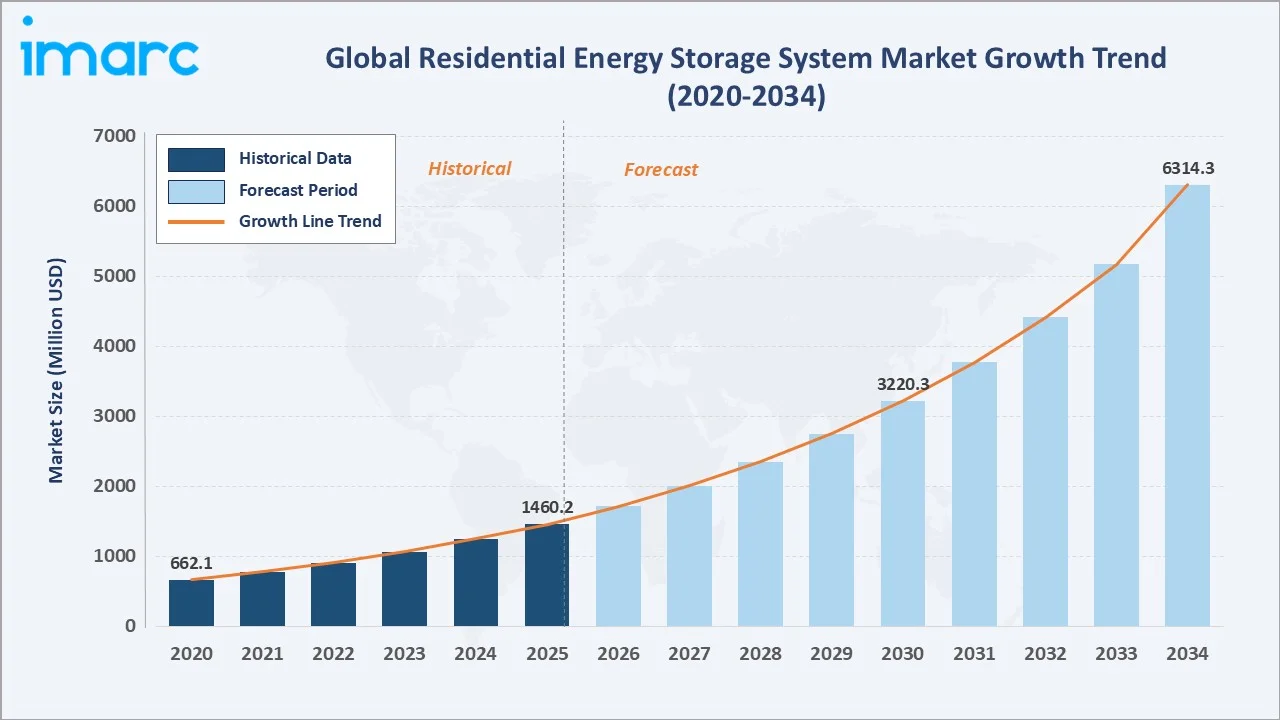

The global residential energy storage system market was valued at USD 1,460.2 Million in 2025 and is projected to reach USD 6,314.3 Million by 2034, exhibiting a CAGR of 17.14% during 2026-2034. Rapid rooftop solar adoption with around 24 lakh homes covered under PM Surya Ghar in India by December 2025, falling lithium-ion battery costs, rising grid tariffs, time-of-use billing, and residential clean-energy incentives are the primary drivers shaping the market growth.

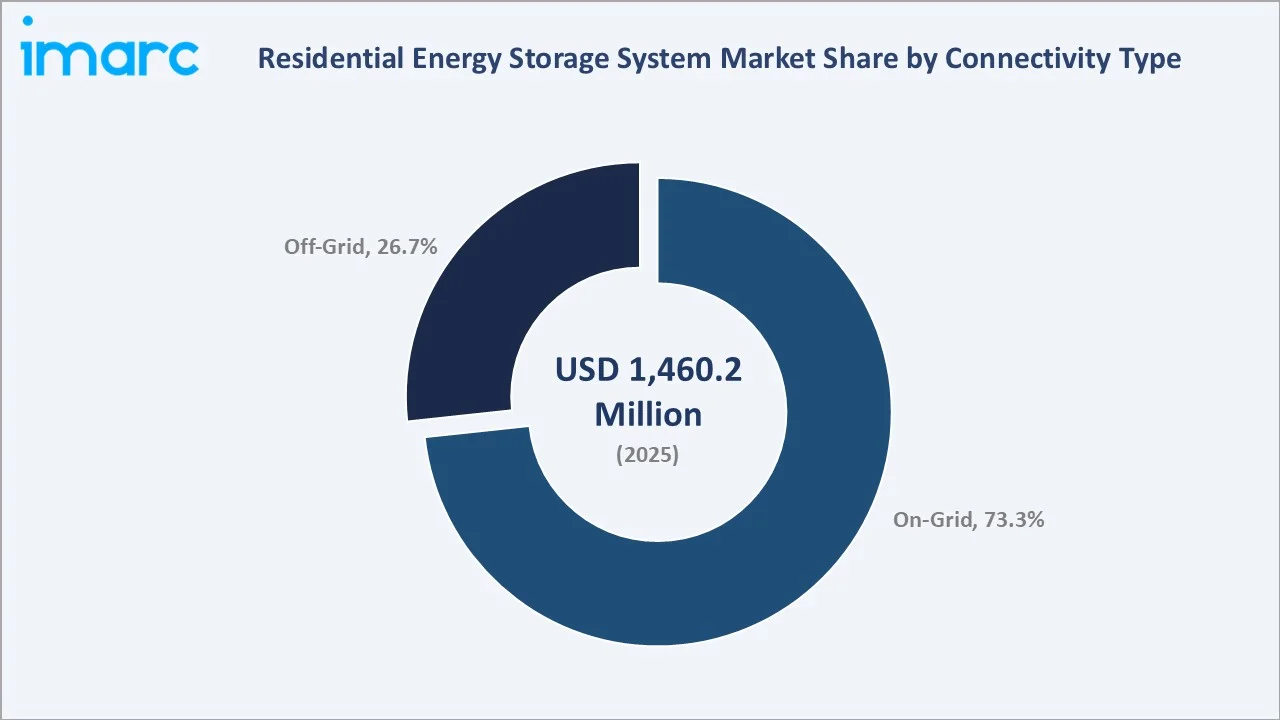

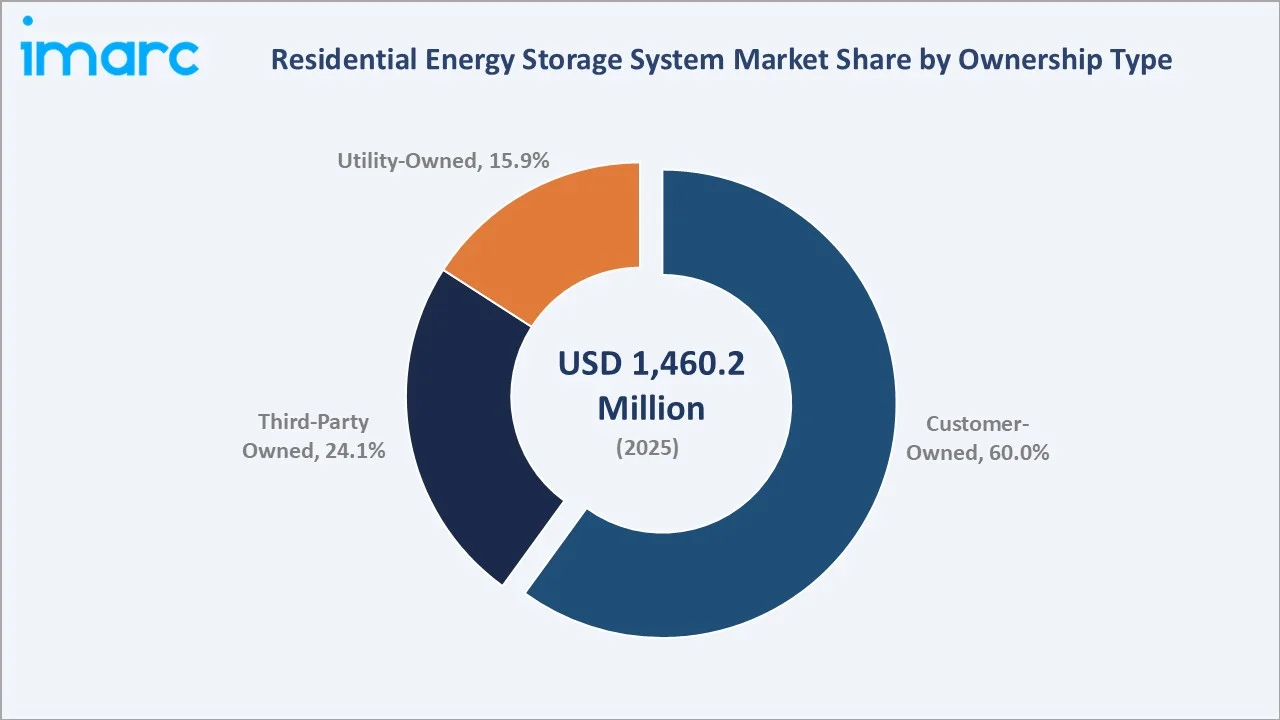

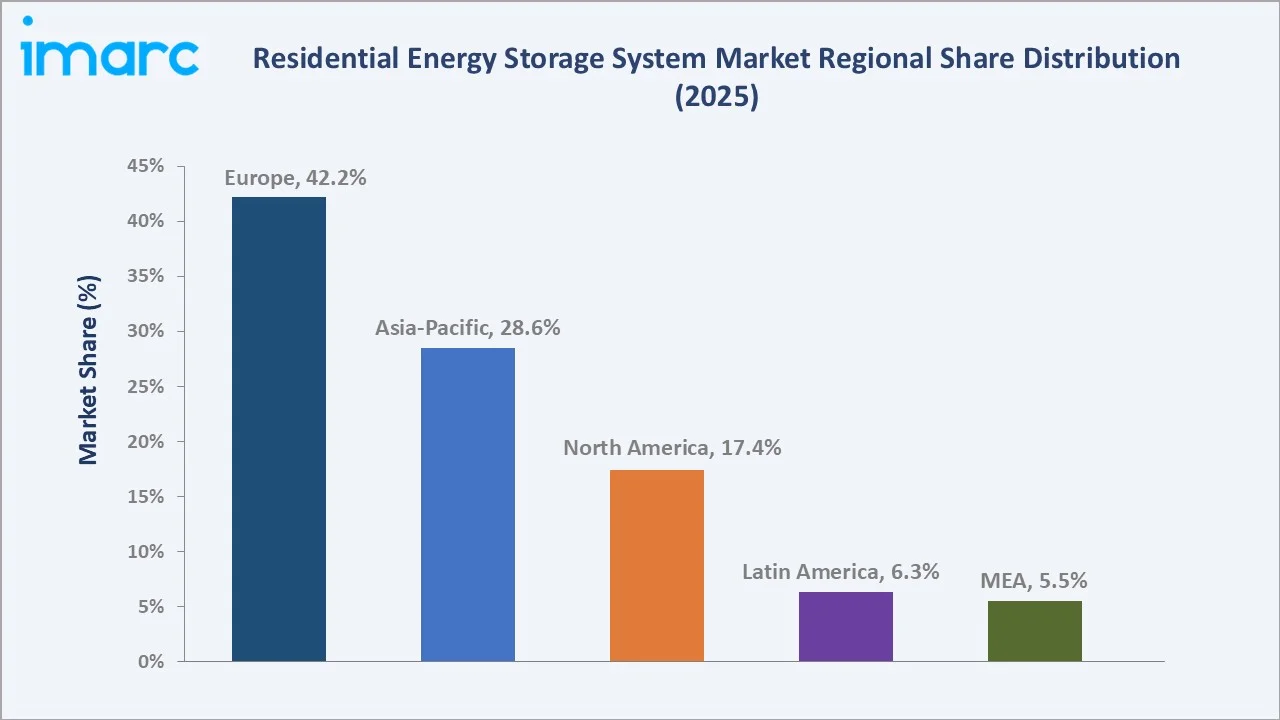

On-grid leads the connectivity type segment at 73.3%, customer-owned dominates the ownership type segment at 60.0%, and Europe commands 42.2% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,460.2 Million |

|

Forecast Market Size (2034) |

USD 6,314.3 Million |

|

CAGR (2026-2034) |

17.14% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (42.2%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (28.6%, 2025) |

|

Leading Connectivity Type |

On-Grid (73.3%, 2025) |

|

Leading Ownership Type |

Customer-owned (60.0%, 2025) |

The global residential energy storage system market expanded from USD 662.1 Million in 2020 to USD 1,460.2 Million in 2025, driven by increasing rooftop solar adoption, falling battery costs, and supportive residential energy policies. Anchored at USD 3220.3 Million in 2030, the forecast to USD 6,314.3 Million by 2034 is supported by growing demand for energy independence and grid resilience.

To get more information on this market, Request Sample

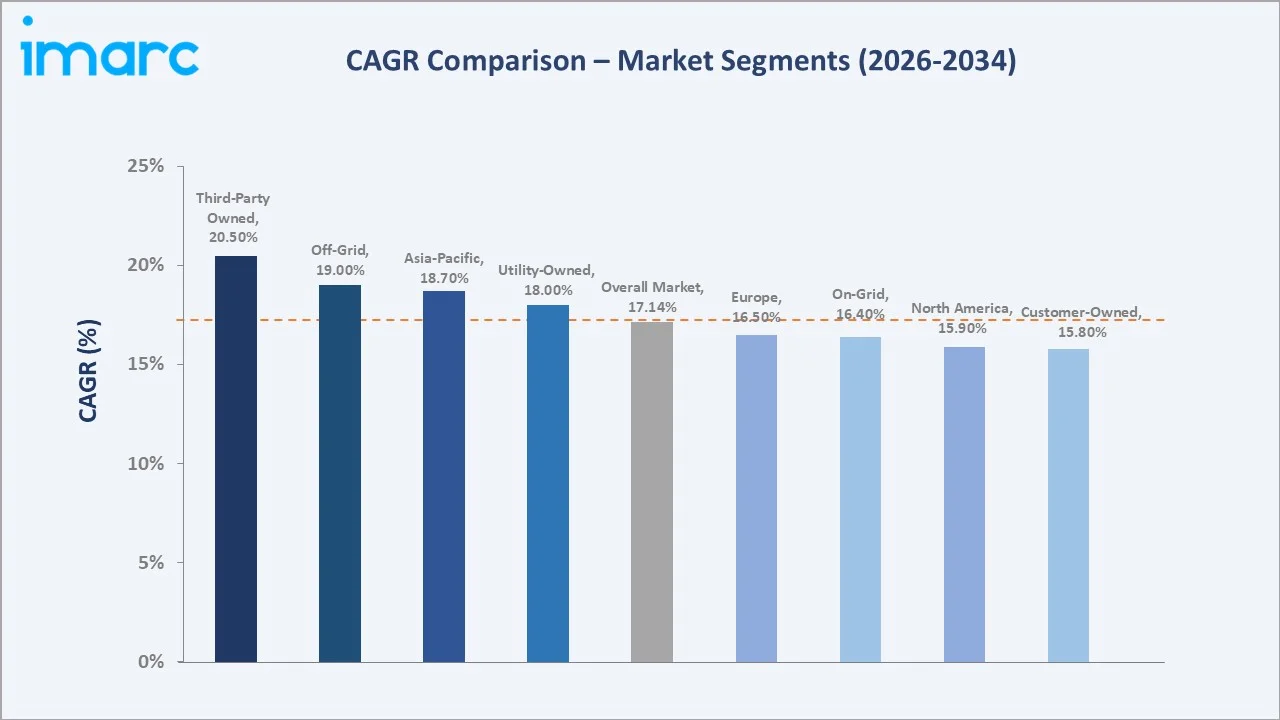

CAGR trajectories across connectivity type and ownership type sub-segments show off-grid and third-party owned systems expanding faster than the overall 17.14% market CAGR, driven by energy-as-a-service models and rural electrification needs.

Executive Summary

The global residential energy storage system market is on a strong growth path from USD 662.1 Million in 2020 to USD 6,314.3 Million by 2034. Home batteries have shifted from a premium niche to a mainstream upgrade for rooftop solar households. Falling battery costs and time-of-use tariffs are encouraging households to store and optimize electricity consumption. Policy incentives and grid reliability concerns are further supporting adoption across residential energy systems.

On-grid dominates connectivity type at 73.3% in 2025, supported by self-consumption economics and virtual power plant (VPP) enrollment. Customer-owned leads the ownership type segment at 60.0%, fueled by greater control over energy usage, long-term cost savings, and increasing consumer preference for energy independence in the global residential energy storage system market. Europe commands 42.2%, led by Germany and Italy, driven by supportive policies, high electricity prices, and strong rooftop solar integration. In March 2026, baseload electricity prices climbed to approximately EUR150-160/MWh in Germany and Italy, depicting a surge of about 45% compared to February 2026.

Key Market Insights

|

Insight |

Data |

|

Leading Connectivity Type |

On-Grid - 73.3% revenue share (2025) |

|

Second Connectivity Type |

Off-Grid - 26.7% revenue share (2025) |

|

Leading Ownership Type |

Customer-owned - 60.0% revenue share (2025) |

|

Second Ownership Type |

Third-Party Owned - 24.1% revenue share (2025) |

|

Leading Region |

Europe - 42.2% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific - 28.6% revenue (2025) |

|

Top Companies |

Tesla Inc., LG Energy Solution, BYD Company Ltd., Generac Power Systems, Inc., Huawei Technologies Co. Ltd. |

Key Analytical Observations Expanding on the Data Above:

- On-grid dominance at 73.3% is driven by strong self-consumption economics, where households pair storage with rooftop solar to reduce reliance on grid electricity. Changes in net-metering policies further enhance the value of energy storage.

- Off-grid share at 26.7% is sustained by remote residential use, vacation properties, and rural electrification needs across developing regions. Declining solar-plus-storage costs are making standalone energy systems increasingly viable for households.

- Customer-owned leadership at 60.0% reflects homeowner preference for direct ownership and tax credit capture, allowing greater control over energy usage and access to financial incentives, such as tax benefits and subsidies.

- Third-party owned at 24.1% is growing through battery-as-a-service and VPP aggregator models from key players, which install home batteries at zero upfront cost in exchange for grid-service revenue-sharing agreements.

- Utility-owned at 15.9% represents direct utility deployment of behind-the-meter batteries for demand response and frequency regulation. Utility-owned systems also help firms manage peak load and improve overall grid stability.

- Europe at 42.2% dominates owing to German and Italian home battery subsidies, high residential tariffs, and mature residential solar penetration in Germany and the Netherlands. As of 2023, solar and home batteries with a capacity below 30KWh enjoyed 0% VAT in Germany.

Global Residential Energy Storage System Market Overview

Residential energy storage systems are behind-the-meter battery units, typically 3-20 kWh in capacity, that store electricity from rooftop solar or the grid for household use during outages, peak-tariff hours, or low-generation periods.

The global ecosystem integrates lithium-ion cell manufacturers, battery pack assemblers, hybrid inverter suppliers, rooftop solar installers, utility interconnection authorities, VPP aggregators, and home-energy-management software providers, together enabling seamless integration with solar PV and smart home systems.

Market Dynamics

To evaluate market opportunities, Request Sample

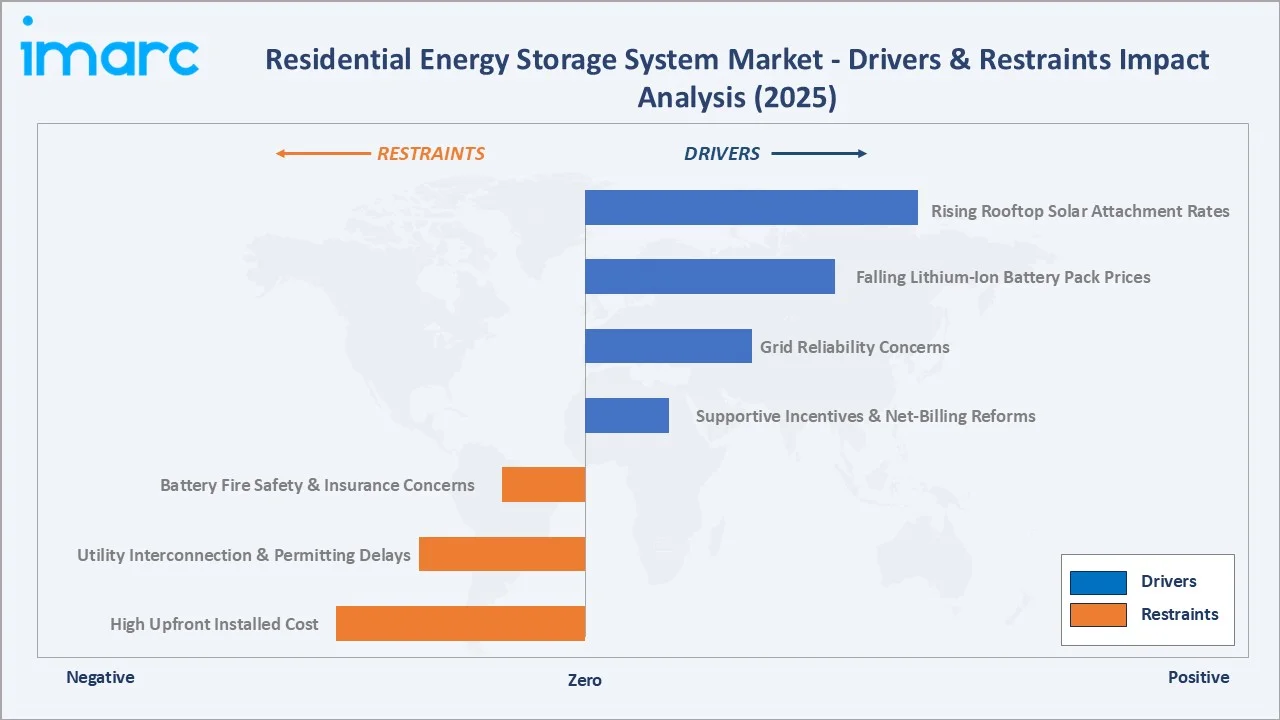

Market Drivers

- Rising Rooftop Solar Attachment Rates: Residential solar installations are increasingly paired with battery systems, reflecting a shift toward integrated home energy solutions and supporting steady growth in residential energy storage adoption.

- Falling Lithium-Ion Battery Pack Prices: Declining battery costs are improving affordability and payback periods, making residential energy storage accessible to a broader base of households across global markets.

- Grid Reliability Concerns and Extreme Weather: Increasing power outages and grid stress from extreme weather events are driving demand for backup power solutions, making energy resilience a key factor in household purchasing decisions.

- Supportive Incentives and Net-Billing Reforms: The US federal 30% Investment Tax Credit on standalone storage and net-billing transitions in Australia, Spain, and California materially improve residential battery investment economics.

Market Restraints

- High Upfront Installed Cost: Fully installed residential battery systems still represent a significant upfront expense for households, creating affordability challenges for middle-income segments. Even as hardware prices decline, adoption remains constrained in markets lacking supportive incentives or subsidy frameworks.

- Utility Interconnection and Permitting Delays: Complex interconnection processes and varying local permitting standards delay project completion and compress installer margins across the industry. As of 2025, in the United States, the backlog in the interconnection queue increased by 30% since 2023, with solar initiatives accounting for more than 1,080 GW awaiting approval.

Market Opportunities

- VPP Monetization: Aggregating residential batteries into VPPs is opening new revenue streams, with energy platforms enabling households to earn additional income by supplying stored power back to the grid.

- Emerging Market Entry with Affordable Kits: Expanding middle-class populations across countries like India, Brazil, Mexico, and South Africa, alongside unreliable grid supply and growing rooftop solar adoption, are creating strong opportunities for cost-effective home battery solutions.

Market Challenges

- Lithium and Critical Mineral Supply Volatility: Fluctuations in lithium pricing and the concentrated supply of key materials such as nickel, cobalt, and graphite continue to create uncertainty and sourcing risks for battery manufacturers.

- Battery Fire Safety and Insurance Concerns: Incidents related to thermal runaway in residential lithium-ion batteries have led to stricter safety testing standards, increased insurance scrutiny, and tighter local regulations on installation, raising compliance requirements for installers.

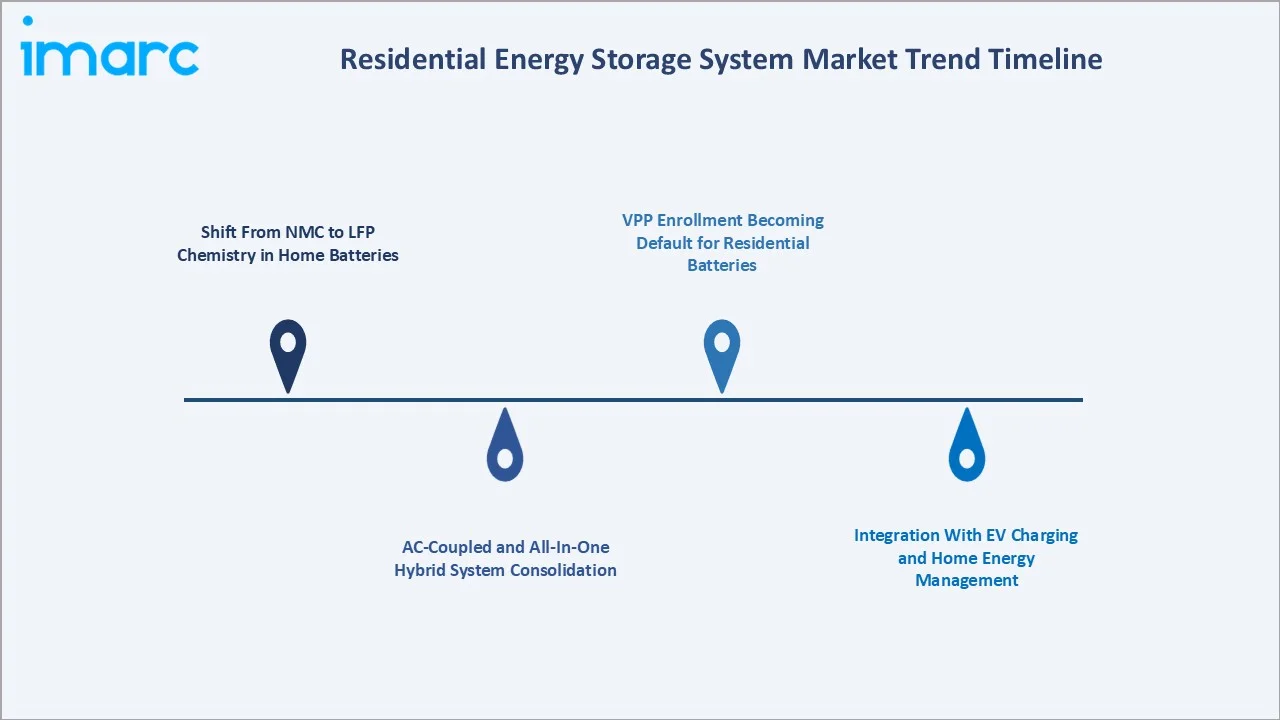

Emerging Market Trends

1. Shift From NMC to Lithium iron phosphate (LFP) Chemistry in Home Batteries

LFP has overtaken NMC as the dominant residential battery chemistry, driven by superior thermal stability, cycle life beyond 6,000 cycles, and absence of cobalt supply risk. This transition is also simplifying regulatory approvals and improving consumer confidence in home energy storage systems.

2. AC-Coupled and All-In-One Hybrid System Consolidation

All-in-one units integrating the battery, hybrid inverter, and energy management system in a single wall-mounted enclosure are replacing multi-component installations. This shift is reducing installation complexity, lowering labor requirements, and enabling faster deployment across residential markets.

3. VPP Enrollment Becoming Default

Utilities and energy service providers are increasingly integrating VPP participation into standard residential battery offerings, enabling automated grid interaction, demand response participation, and seamless monetization of stored energy without active user intervention. As per IMARC Group, the global virtual power plant market size reached USD 2.5 Billion in 2025.

4. Integration With Electric Vehicle (EV) Charging and Home Energy Management

Residential battery systems are increasingly integrated with EV chargers and smart home energy platforms, enabling coordinated load balancing, optimized solar utilization, and unified control of household energy consumption through centralized digital interfaces.

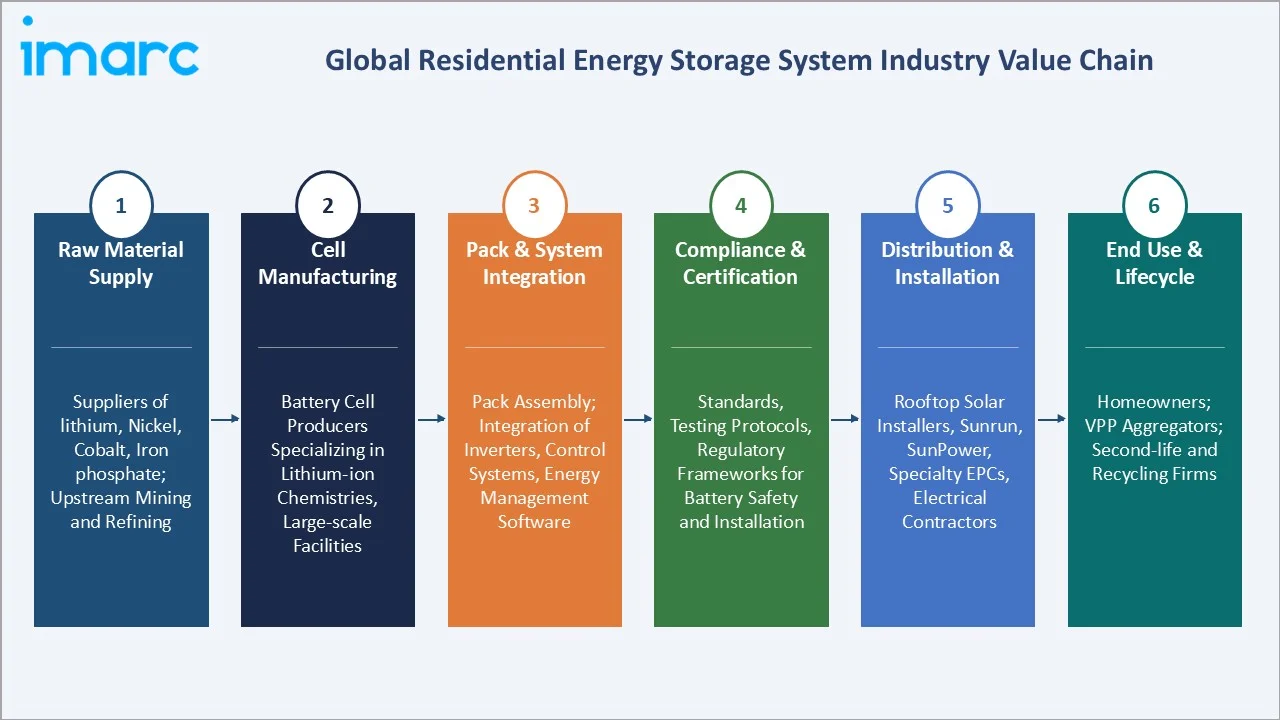

Industry Value Chain Analysis

The residential energy storage system value chain spans six stages from critical mineral mining through end-of-life recycling. Cell manufacturing and system integration capture the highest value-add, while installer relationships and utility program enrollment generate downstream competitive advantages in this regulated category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of lithium, nickel, cobalt, and iron phosphate, along with upstream mining and refining entities supporting battery-grade material production |

|

Cell Manufacturing |

Battery cell producers specializing in lithium-ion chemistries, including large-scale facilities focused on performance optimization and cost efficiency |

|

Pack & System Integration |

Companies assembling battery packs and integrating inverters, control systems, and energy management software into complete residential storage solutions |

|

Compliance & Certification |

Standards, testing protocols, and regulatory frameworks governing battery safety, transport, and installation across residential applications |

|

Distribution & Installation |

Rooftop solar installers, Sunrun, SunPower, specialty EPCs, electrical contractors |

|

End Use & Lifecycle |

Homeowners; VPP aggregators; second-life and recycling firms |

Vertically integrated players such as Tesla Inc., which manufactures battery packs, and BYD Company Ltd., which produces cells, packs, and inverters in-house, achieve superior cost control and supply security versus integrators relying on third-party cell sourcing.

Technology Landscape in the Global Residential Energy Storage System Industry

Battery Chemistry Innovation

LFP has become the preferred chemistry for residential battery installations, driven by strong safety performance, long operational life, and reduced reliance on constrained raw materials. Emerging alternatives such as sodium-ion and solid-state batteries are progressing toward early-stage commercial deployment, with pilot projects exploring their scalability and cost potential.

Hybrid Inverter and Power Electronics

Hybrid inverters integrating solar maximum power point tracking, bidirectional battery conversion, and grid-forming capabilities are becoming standard in new residential systems. These advancements are improving overall system efficiency, enabling seamless switching between grid and backup modes, and supporting more resilient home energy infrastructure.

Smart Connectivity and Home Energy Management

Connected battery systems with cloud-based monitoring, wireless communication, and integration with smart home ecosystems are enabling real-time energy tracking and automated optimization. These features allow households to manage consumption more effectively, participate in grid services, and coordinate energy use across multiple devices through unified digital platforms.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Technology Type | Lithium-ion Batteries | NA | 2025 |

| Power Rating | 6–10 kW | 🔒 | 2025 |

| Ownership Type | Customer-owned | 60.0% | 2025 |

| Connectivity Type | On-Grid | 73.3% | 2025 |

| Region | Europe | 42.2% | 2025 |

By Connectivity Type

On-grid commands a 73.3% majority share in 2025, driven by self-consumption economics, net-billing compensation, time-of-use arbitrage, and growing VPP participation. These systems remain grid-connected and use the public network as backup during shortfalls or maintenance periods.

To access detailed market analysis, Request Sample

Off-grid at 26.7% in 2025 serve remote homes, vacation properties, islands, and rural electrification programs across Sub-Saharan Africa, Southeast Asia, and parts of Latin America. Off-grid penetration is growing faster than on-grid in several emerging markets due to unreliable or unavailable grid infrastructure.

By Ownership Type

Customer-owned dominates with 60.0% share in 2025, reflecting homeowner preference for direct ownership and long-term bill-savings capture. This model provides greater control over energy usage, system operation, and participation in grid services without reliance on third-party agreements. It also aligns with increasing consumer interest in asset ownership and long-term value realization from residential energy investments.

Third-party owned prevail over the market, with 24.1% share, expanding rapidly through battery-as-a-service models, where the installer retains ownership and the homeowner pays a monthly fee. This zero-upfront-cost structure broadens affordability for middle-income households significantly.

Utility-owned at 15.9% involves utilities directly deploying behind-the-meter batteries under bill-credit or demand-response programs. These setups enable centralized control of distributed storage assets, supporting grid stability, peak load management, and more efficient energy distribution across networks.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

| Europe | 42.2% | Strong rooftop solar adoption, supportive regulatory frameworks, and growing consumer focus on energy independence |

| Asia-Pacific | 28.6% | Expanding distributed energy adoption, rapid urbanization, supportive government initiatives, and increasing integration of solar with storage systems |

| North America | 17.4% | Favorable policy support, rising demand for backup power, increasing grid reliability concerns, and growing residential solar penetration |

| Latin America | 6.3% | Unreliable grid infrastructure, rising electricity prices, expanding distributed generation adoption, and increasing interest in energy self-sufficiency |

| Middle East & Africa | 5.5% | Power supply instability, growing investment in decentralized energy systems, rising electrification efforts, and increasing adoption of solar solutions |

Europe at 42.2% in 2025 leads the global market, driven by elevated electricity prices, widespread rooftop solar deployment, enabling regulatory environments, and a strong shift toward energy self-sufficiency. Well-established installation networks and mature residential solar ecosystems are further supporting sustained adoption of home energy storage solutions.

Asia-Pacific at 28.6% is the highest-growth region through 2034. Strong policy support, urban energy demand growth, and rapid deployment of residential solar-plus-storage solutions are accelerating regional expansion.

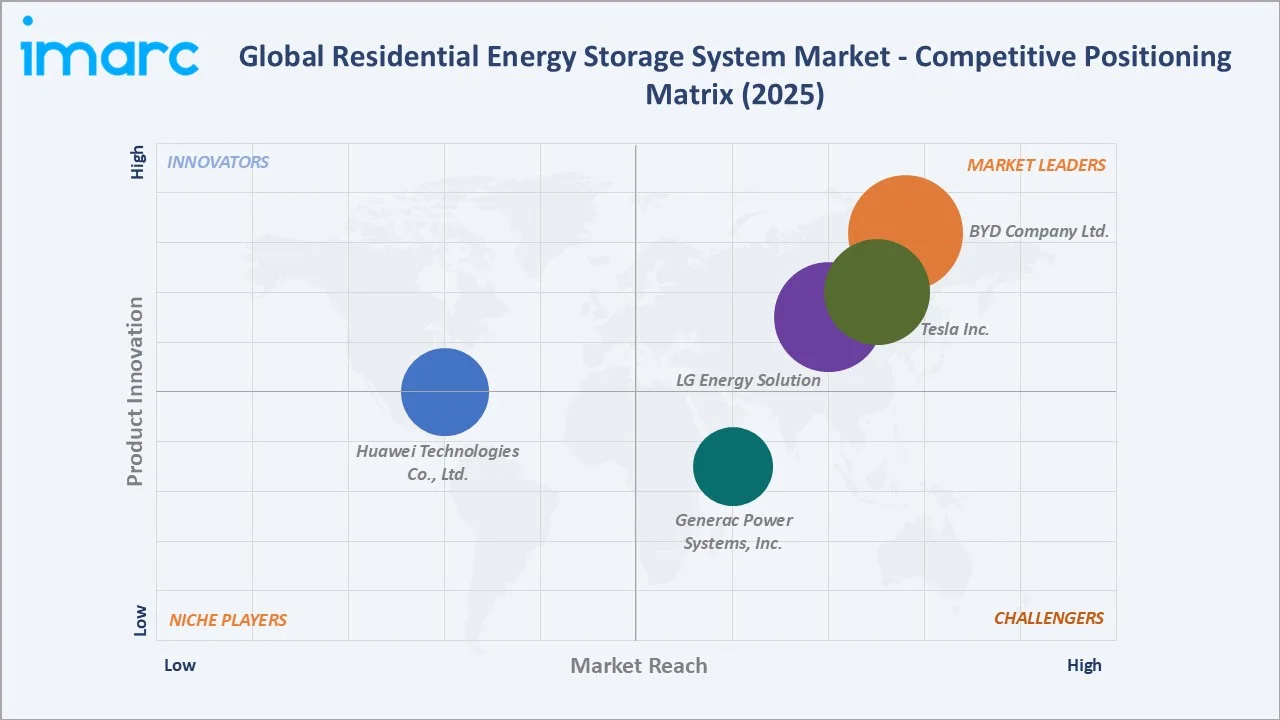

Competitive Landscape

The global residential energy storage system market is moderately fragmented, with global leaders dominating brand awareness and installer relationships while regional specialists serve niche chemistry, price-tier, or integration segments. Installer-channel depth and software capabilities form the key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

| Tesla Inc. | Powerwall 3 | Leader | Premium all-in-one system; VPP software leadership; direct-to-home channel |

| LG Energy Solution | enblock E and enblock S | Leader | Broad installer channel; modular capacity; strong US and Europe presence |

| BYD Company Ltd. | Battery-Box Premium HVS+ and HVM+ | Leader | Cost-competitive LFP modular design; strong Europe and Australia footprint |

| Generac Power Systems, Inc. | PWRcell2 | Challenger | Dealer-installer network; whole-home backup positioning; US focus |

| Huawei Technologies Co., Ltd. | LUNA2000-S1 Series | Emerging | Hybrid-inverter integration; strong EMEA and APAC reach |

Key players include Tesla Inc., LG Energy Solution, BYD Company Ltd., Generac Power Systems, Inc., and Huawei Technologies Co. Ltd., among others.

Key Company Profiles

Tesla Inc.

Tesla Inc. is the global residential storage leader through its Powerwall line, integrating LFP cells, built-in inverter, and Tesla Energy app control in a single wall-mount unit deployed across several countries.

- Product Portfolio: Powerwall 3 (13.5 kWh LFP, integrated hybrid inverter), Solar Roof and Solar Panels ecosystem, Tesla Energy App and VPP software platform.

- Recent Developments: In November 2023, Tesla Inc. revealed the initiation of a large-scale VPP initiative in Puerto Rico, enabling Powerwall owners to join the territory’s Battery Emergency Demand Response Program. The VPP offers significant advantages as it aids Puerto Rico’s power grid and rewards homeowners engaged in the program.

- Strategic Focus: Vertically integrated combining Gigafactory LFP cells, direct-to-home sales, and Tesla Inc.-certified installer network.

LG Energy Solution

LG Energy Solution is a leading global battery supplier serving the residential energy storage market through its LG ESS Home portfolio, combining proprietary NMC and LFP modules with a broad installer network across North America, Europe, and Australia.

- Product Portfolio: enblock E and enblock S, RESU FLEX stackable series spanning 8.6-17.2 kWh, and compatibility with SolarEdge, SMA, and Fronius hybrid inverter ecosystems.

- Recent Developments: In September 2025, the company unveiled the JF2S Home Battery Module at RE+ 2025 — a 15.9 kWh LFP-powered home battery produced in the US, with a slim 5.6-inch-thick wall-mountable design to support flexible residential installation.

- Strategic Focus: Leverages global cell manufacturing scale, modular designs that let homeowners expand capacity over time, and deep installer-channel relationships to maintain leadership as LFP chemistry becomes the residential standard.

BYD Company Ltd.

BYD Company Ltd. is a vertically integrated leader producing LFP cells, packs, and hybrid inverters in-house, delivering cost-competitive solutions through its Battery-Box Premium family across Europe, Asia, Africa, Australia, and the Americas.

- Product Portfolio: Battery-Box Premium HVS and HVM high-voltage modular units, Battery-Box Premium LVS/LVL low-voltage systems, fully LFP chemistry.

- Recent Developments: In May 2025, the firm introduced the new Battery‑Box HVB, an advanced high-voltage storage solution that brings the reliable Blade‑Battery technology to residential storage uses. The HVB stands out with its high energy density, adaptable modular design, and exceptionally strong safety framework — perfect for challenging self-consumption and backup applications

- Strategic Focus: Full vertical integration, aggressive LFP pricing, and scaling distribution through EFT Energy Solutions, Fronius, and local distributors in Europe and Australia to capture mid-market segments.

Market Concentration Analysis

The global residential energy storage system market is moderately concentrated, with the top five companies (Tesla Inc., LG Energy Solution, BYD Company Ltd., Generac Power Systems, Inc., and Huawei Technologies Co. Ltd.) estimated to hold approximately 55-65% of global installed-capacity share in 2025.

Barriers to entry include UL 9540 and IEC 62619 certification, multi-year installer-channel relationship building, and the software platform capabilities needed for VPP participation, favoring well-capitalized incumbents with deep battery cell supply and integrated manufacturing.

Consolidation is accelerating through LFP cell partnerships, VPP platform acquisitions, and hybrid inverter-and-battery bundling. Scale advantages in manufacturing, distribution, and after-sales service are further reinforcing the competitive position of established players.

Investment & Growth Opportunities

Fastest-Growing Segments

Off-grid connectivity expands faster than the overall 17.14% market CAGR through 2034, driven by remote residential, cabin, and rural electrification applications. Third-party owned at 24.1% is the fastest-growing ownership category as battery-as-a-service models scale globally.

Emerging Markets

Asia-Pacific at 28.6% is the highest-growth region, with Australia, Japan, and China leading installations. India, Brazil, and South Africa represent the largest untapped opportunities as rising affordability, grid reliability concerns, and falling LFP prices unlock mass-market adoption.

Venture & Investment Trends

Venture capital is concentrated in VPP software, LFP cell capacity in Europe and North America, bidirectional EV-to-home integration, and second-life battery reuse. Investment is also expanding into advanced energy management platforms and grid-interactive technologies that enable more flexible and scalable residential energy ecosystems.

Future Market Outlook (2026-2034)

The global residential energy storage system market is forecast to expand from USD 1,460.2 Million in 2025 to USD 6,314.3 Million by 2034 at a CAGR of 17.14%, adding roughly USD 4,854 Million in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: LFP cost declines; VPP revenue unlocking new customer economics; EV plus home battery integration; and bidirectional heat-pump and water-heater load coordination across household energy use.

By 2034, home batteries will be installed in most new rooftop solar households across leading markets and will serve as a core grid-flexibility asset. Utility-owned and third-party owned shares are expected to rise collectively to over 45% of global deployments.

Research Methodology

Primary Research

Primary research included interviews with senior product managers at leading battery manufacturers, solar-plus-storage EPC executives, utility program managers, VPP platform leaders, and household adopters, validating market sizing, regional demand, connectivity splits, and ownership-mix evolution.

Secondary Research

Secondary sources include IEA World Energy Outlook 2025, BloombergNEF Energy Storage Outlook, IRENA statistics, SEIA/Wood Mackenzie US Energy Storage Monitor, SolarPower Europe reports, CEA reviews, and annual reports, press releases, and investor presentations from listed manufacturers.

Forecasting Models

Market forecasts used top-down and bottom-up models combining rooftop solar attachment rates, average capacity per installation (kWh), installed price per kWh, incentive durations, and utility program pipelines. Scenario analysis addressed interest-rate and lithium-cell price variation.

Residential Energy Storage System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technology Types Covered | Lithium-ion Batteries, Lead-acid Batteries, Others |

| Power Ratings Covered | 3-6 Kw, 6-10 Kw, More Than 10 Kw |

| Ownership Types Covered | Customer-owned, Utility-owned, Third-Party Owned |

| Connectivity Types Covered | On-Grid, Off-Grid |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Tesla Inc., LG Energy Solution, BYD Company Ltd., Generac Power Systems, Inc., Huawei Technologies Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the residential energy storage system market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global residential energy storage system market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the residential energy storage system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Residential Energy Storage System Market Report

The global market was valued at USD 1,460.2 Million in 2025, driven by rooftop solar attachment, falling battery prices, and residential incentives.

The market is projected to grow at 17.14% CAGR from 2026 to 2034, reaching USD 6,314.3 Million, supported by LFP cost declines and VPP expansion.

On-grid leads at 73.3% in 2025, driven by self-consumption economics and net-billing. Off-grid at 26.7% expands faster via rural applications.

Customer-owned dominates at 60.0% in 2025. Third-party owned at 24.1% is fastest growing due to zero-upfront battery-as-a-service offerings.

Europe commands 42.2% in 2025, led by Germany and Italy. Asia-Pacific at 28.6% is the fastest-growing region through 2034.

Leading players include Tesla Inc., LG Energy Solution, BYD Company Ltd., Generac Power Systems, Inc., and Huawei Technologies Co. Ltd.

LFP adoption is driven by superior thermal safety, cycle life beyond 6,000 cycles, absence of cobalt risk, and sub-USD 100 per kWh cell prices.

VPP enrollment enables households to earn recurring income by aggregating batteries for services such as peak demand reduction and grid frequency support.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)