Reinforcement Materials Market Report by Material Type (Glass Fiber, Carbon Fiber, Aramid Fiber, Natural Fiber, and Others), Application (Composite, Concrete, and Others), End Use Industry (Aerospace and Defense, Construction, Transportation, Wind Energy, Industrial and Consumer Goods, and Others), and Region 2026-2034

Reinforcement Materials Market Size:

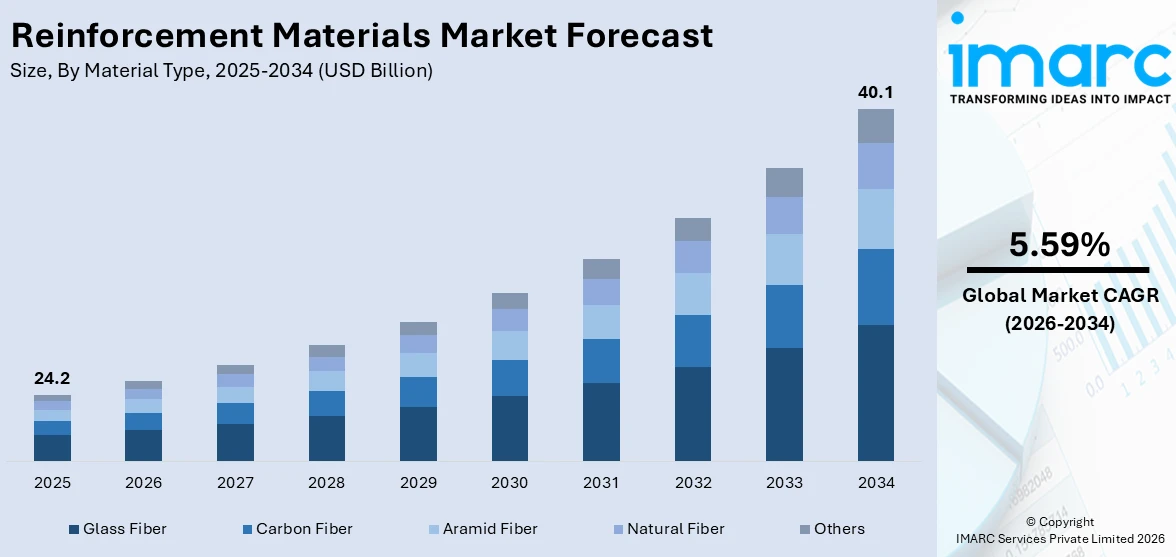

The global reinforcement materials market size reached USD 24.2 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 40.1 Billion by 2034, exhibiting a growth rate (CAGR) of 5.59% during 2026-2034. Asia Pacific dominated the market, holding a significant market share in 2025. The growing product demand in the automotive, aerospace, construction, and renewable energy sectors, increasing focus on lightweight and sustainable materials, and rapid technological innovations that enhance structural integrity, efficiency, and durability of these materials across various applications are some of the factors propelling the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 24.2 Billion |

|

Market Forecast in 2034

|

USD 40.1 Billion |

| Market Growth Rate 2026-2034 | 5.59% |

Reinforcement Materials Market Analysis:

- Major Market Drivers: The increasing need for these materials in the automotive, construction, aerospace, and renewable energy industries is driving this market. Moreover, the rising demand for high-strength and lightweight materials to improve structural performance and fuel economy, as well as the move toward environmentally friendly and sustainable building methods, are other contributing factors.

- Key Market Trends: Important developments in this industry include technological breakthroughs and improvements in composite materials, such as high-performance fibers and nanocomposites. Furthermore, there has been a rise in the usage of sustainable and bio-based reinforcing materials, which is in line with the global emphasis on minimizing environmental effect and using green construction techniques.

- Geographical Trends: The Asia Pacific region is the largest in this market, driven by fast industrialization, urbanization, and significant infrastructure development in countries like China, India, Japan, and South Korea. Other regions are also seeing development as a result of the expanding automobile sector and increased spending on aerospace and defense.

- Competitive Landscape: Some of the major market players in the reinforcement materials industry include BASF SE, Bekaert, Century Enka Limited, Cordenka GmbH & Co. KG, DuPont de Nemours, Inc., Formosa Taffeta Co. Ltd., Hs Hyosung Advanced Materials, Kolon Industries, Inc., Owens Corning, Teijin Limited, Toray Industries Inc. and Toyobo Co. Ltd, among many others.

- Challenges and Opportunities: The high expense of cutting-edge reinforcing materials like carbon fiber and the requirement for technological know-how in their application are two of the market's biggest obstacles. Opportunities are presenting themselves as a result of the expanding emphasis on renewable energy initiatives, higher infrastructure spending, and the creation of creative and economical production techniques for reinforcing materials.

To get more information on this market Request Sample

Reinforcement Materials Market Trends:

Advanced Material Evolution

The reinforcement materials sector is experiencing a significant shift towards ultra-lightweight, high-strength composite solutions. Innovations are focusing on developing fabrics and fibers that enable superior mechanical properties while drastically reducing weight. This advancement is particularly crucial for industries like aerospace, automotive, and sporting goods, where performance and fuel efficiency are paramount. The introduction of advanced carbon fiber woven fabrics, characterized by their minimal mass and exceptional durability, underscores this drive. Such materials facilitate the creation of components that are not only robust but also contribute to overall system efficiency, marking a crucial progression in composite material capabilities. For example, Hexcel Corporation, a top producer of advanced composite reinforcement materials, has introduced its latest product, i.e., HexForce 1K woven reinforcement fabric. This new fabric is lightweight and made with Hexcel's special HexTow AS4C 1K carbon fiber. This allows for the creation of composite materials that are both high-strength and low-weight, further driving the adoption of fiber reinforced composite material.

Growing Product Demand in the Automotive Industry

The expanding automotive industry is one of the major factors that is driving the reinforcement materials market growth. As the automotive sector continues to evolve, the need for materials that give better performance, safety, and fuel efficiency also surges. The automotive industry is expanding at a rapid pace, particularly in emerging economies, which is creating the demand for these materials. For instance, China exported 2.1 million vehicles between January and September 2022, which is a hike of 55% in comparison to the year 2021. Also, a total of 85.4 million motor vehicles were produced around the world in the same year, which is an increase of 5.7% compared to its previous year. Reinforcement materials like carbon fiber, glass fiber, and aramid fiber play an important role in these vehicles, contributing to the development of fiber reinforced plastic components. They are used to better the mechanical properties of many automotive components, like body panels, chassis, and interior parts.

Rising Construction and Infrastructure Development

The expansion of the construction and infrastructure sector is a main driver that is expanding the reinforcement materials market revenue. For instance, in the budget of 2023 and 2024, India's capital investment for infrastructure was hiked by 33% to Rs.10 lakh crore. Along with India, China's investment in fixed assets grew by 4.9% in 2021, which is 2.9% growth from 2020. Its industrial investment also reached 11.4%, registering a drastic acceleration from 0.1% growth in 2020. Rapid urbanization and industrialization are leading to a continuous demand for durable and high-performance construction materials. Reinforcement materials like steel rebar, fiber-reinforced polymers (FRPs), and composite materials are majorly being used to better the structural integrity and lifespan of buildings, bridges, and other infrastructures, including applications of fiberglass reinforced plastic.

Increasing Use in Aerospace and Defense Applications

Reinforcement materials are increasingly being embraced in the aerospace and defense sectors. The requirement for strict performance and the need for lightweight and high-strength materials in these industries are creating a demand for these advanced materials. Carbon fiber composites play an important role in improving the performance and efficiency of aerospace and defense applications, acting as a crucial reinforced plastic material. Growth and expenditure in these industries are fueling the need for reinforcement materials. For example, in 2023-24, the Indian defense sector added capital of Rs 5.94 lakh crore, a jump of 13% over the previous year. Along with India, China also raised its allocation of budget in the defense sector by 7.2% for 2024, which sums up to 1.67 trillion yuan in Chinese currency. The reliance of this sector on these materials for various applications, including military aircraft, vehicles, and protective gear, is boosting its market expansion.

Reinforcement Materials Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on material type, application, and end use industry.

Breakup by Material Type:

- Glass Fiber

- Carbon Fiber

- Aramid Fiber

- Natural Fiber

- Others

Glass fiber accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the material type. This includes glass fiber, carbon fiber, aramid fiber, natural fiber, and others. According to the report, glass fiber represented the largest segment.

According to the reinforcement materials market trends and analysis, glass fiber accounted the largest share as it is extensively used across various industries due to its excellent properties, including high tensile strength, lightweight, corrosion resistance, and cost-effectiveness. Moreover, it is favored in the automotive, construction, aerospace, and wind energy sectors for applications such as automotive body panels, structural components, insulation, and wind turbine blades. Besides this, the versatility and relatively lower cost of glass fiber compared to other reinforcement materials, like carbon fiber, is positively influencing the reinforcement materials market share.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

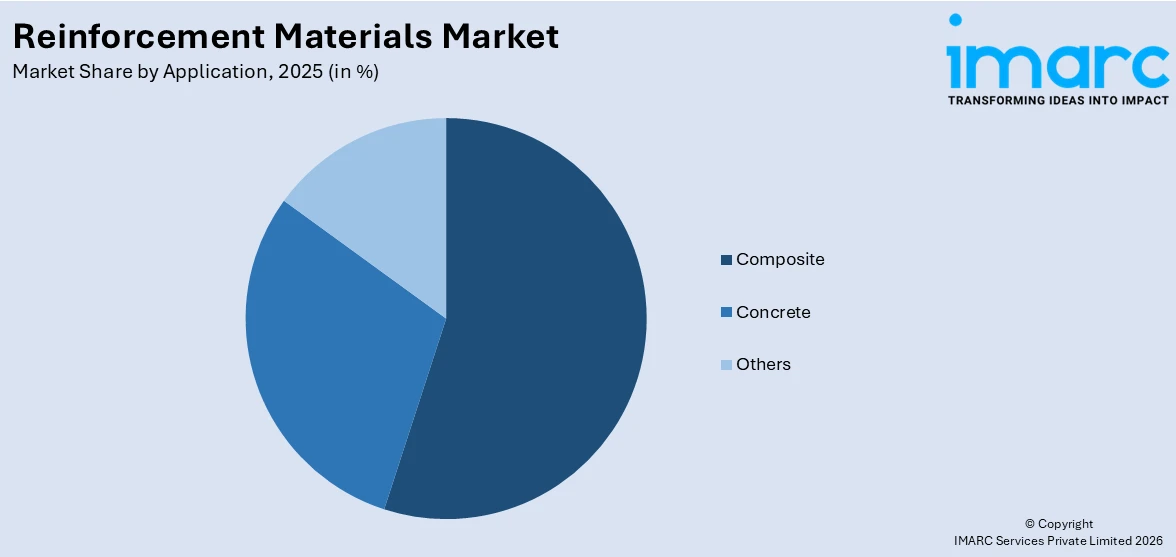

- Composite

- Concrete

- Others

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes composite, concrete, and others.

Composite materials are extensively use in industries such as aerospace, automotive, construction, and marine. They combine reinforcement fibers like glass, carbon, and aramid with a matrix material and offer superior mechanical properties, including high strength-to-weight ratio, corrosion resistance, and durability. Moreover, they are utilized in the manufacturing of lightweight and high-performance components, such as aircraft structures, automotive body panels, wind turbine blades, and sports equipment.

As per the reinforcement materials market forecast and outlook, concrete materials are used in the construction industry. Steel rebar, glass fiber, and synthetic fibers are used to enhance the structural integrity, durability, and longevity of concrete structures. Moreover, reinforced concrete is essential for building bridges, highways, commercial buildings, and residential structures, to provide the necessary strength to withstand heavy loads and environmental stresses.

Breakup by End Use Industry:

- Aerospace and Defense

- Construction

- Transportation

- Wind Energy

- Industrial and Consumer Goods

- Others

Construction represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the end use industry. This includes aerospace and defense, construction, transportation, wind energy, industrial and consumer goods, and others. According to the report, construction represented the largest segment.

According to the reinforcement materials market report and overview, the construction industry accounted for the largest segment, driven by the continuous demand for durable and high-performance building materials. The rapid urbanization and industrialization, particularly in emerging economies, are fueling construction activities, thereby increasing the need for reinforced concrete and other construction materials. Additionally, the growing focus on sustainable building practices, seismic resilience, and advanced construction techniques such as prefabrication and modular construction is driving the demand for reinforcement materials. Besides this, the rising emphasis on infrastructure development and modernization projects is boosting the role of these materials in the construction industry.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest reinforcement materials market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for reinforcement materials.

The Asia Pacific region represented the largest segment in the reinforcement materials industry, driven by rapid industrialization, urbanization, and infrastructure development. Moreover, the significant growth in construction, automotive, aerospace, and renewable energy sectors, boosting the need for high-performance materials, is catalyzing the market growth. Along with this, the booming construction industry and building materials market in the region, which require large quantities of reinforced concrete and other building materials to support the development of residential, commercial, and industrial projects, are favoring the market growth. Additionally, the ongoing shift in the automotive industry towards lightweight and fuel-efficient vehicles, coupled with the increasing adoption of electric vehicles (EVs), is boosting the reinforcement materials market growth.

Key Regional Takeaways:

United States Reinforcement Materials Market Analysis

In the US, a prominent trend in advanced materials involves the expansion of high-performance composite portfolios, particularly those featuring continuous fiber-reinforced thermoplastics. This movement is driven by a growing need for lightweight yet robust solutions across diverse industries. These advanced materials offer superior strength-to-weight ratios, enhanced durability, and often, recyclability, which aligns with increasing sustainability mandates. The strategic focus is on boosting capabilities for creating specialized tapes that can withstand extreme temperatures, thereby broadening their application scope. This development addresses the burgeoning demand from sectors such as high-performance sports equipment, energy exploration (e.g., oil and gas), and various industrial applications where conventional materials fall short. The emphasis is on industrializing these advanced composites, making them more accessible and cost-effective for large-scale integration and fostering innovation in material science and manufacturing processes. For example, in November 2024, Toray Advanced Composites expanded its continuous fiber-reinforced thermoplastic composite materials portfolio by acquiring Gordon Plastics' assets. This strategic move enhances Toray's development, testing, and production capacity for unidirectional tapes, crucial for high-temperature polymer systems. The acquisition signifies Toray's commitment to industrializing thermoplastic composites, particularly for burgeoning demand in sports, oil and gas, and industrial sectors, bolstering the reinforcement materials market.

Asia Pacific Reinforcement Materials Market Analysis

The aerospace industry in Asia Pacific is witnessing a significant shift toward advanced, lightweight materials to enhance efficiency and performance. A key trend is the increasing adoption of continuous fiber-reinforced composites, particularly carbon fiber-based materials, in both commercial and military aircraft structures. This is driven by the imperative to reduce weight, improve fuel efficiency, and extend the lifespan of aerospace components. Furthermore, there's a strong push for automated production processes and out-of-autoclave (OOA) technologies. These innovations streamline manufacturing, reduce costs, and increase output, making high-performance composites more accessible for high-rate applications. The development of specialized carbon fibers and compatible resin systems is crucial to meet the demanding requirements for strength, stiffness, and high-temperature performance in next-generation aerospace designs. This strategic material evolution underpins the future of more sustainable and advanced air and space travel. At Aero India 2025 (February 10-14, Bengaluru), Hexcel Corporation showcased innovations in lightweight, high-performance aerospace materials. A long-term partner to India's aerospace industry, Hexcel supplies composites for civil, military, and space programs, including the new Airbus C295 and H125. Highlights include HexTow carbon fibers for advanced applications and out-of-autoclave technologies like HexPly M51 and HexPly M56, enabling cost-effective, high-rate automated production of aerospace structures.

Europe Reinforcement Materials Market Analysis

The field of soft-tissue reconstruction, particularly for hernia repair, is experiencing a significant trend toward more biological and patient-friendly solutions in Europe. There's a notable shift away from purely synthetic meshes towards reinforced tissue matrices that encourage natural tissue healing and minimize long-term foreign body presence. This trend is amplified by advancements in minimally invasive surgical techniques, such as laparoscopic and robotic-assisted procedures, which demand materials compatible with precise and intricate delivery. The focus is on developing customizable, anatomically shaped implants that integrate seamlessly with the body, aiming for improved patient outcomes, reduced complications, and a more natural repair process. For example, in June 2025, TELA Bio introduced its OviTex Inguinal Reinforced Tissue Matrix in Europe, designed for laparoscopic and robotic inguinal hernia repair. This reinforced tissue matrix offers surgeons a natural alternative to synthetic mesh. Available in multiple configurations for patient-specific needs, OviTex Inguinal aims to revolutionize soft-tissue reconstruction by leveraging natural healing and minimizing permanent synthetic material exposure.

Latin America Reinforcement Materials Market Analysis

A prominent trend across industrial sectors, particularly in Latin America's oil and gas industry, is the accelerated adoption of additive manufacturing, or 3D printing. This strategic embrace of advanced production technologies, specializing in materials like polymers, is driven by a critical need for enhanced logistical independence and optimized operational processes. By leveraging 3D printing for critical components, companies can achieve faster, more efficient production, reduce reliance on traditional, often complex, external supply chains, and enable on-demand manufacturing, fundamentally transforming regional industrial capabilities. For instance, in December 2024, Petrobras inaugurated LABi3D at its Rio de Janeiro research center, partnering with 3DCRIAR to create one of Latin America's most advanced additive manufacturing laboratories. Specializing in polymeric additive manufacturing, LABi3D enhances Petrobras' logistical independence and process optimization for the oil and gas industry. This strategic move reinforces the growing trend of leveraging 3D printing for critical parts in Latin America, enabling faster, more efficient production and reducing reliance on external supply chains.

Middle East and Africa Reinforcement Materials Market Analysis

The Middle East and Africa, particularly Saudi Arabia, is undergoing a profound economic diversification, moving beyond its traditional reliance on oil and gas. A significant aspect of this transformation is the accelerated adoption and promotion of advanced materials, especially fiber-reinforced composites and other nonmetallic solutions. Driven by ambitious national visions like Saudi Vision 2030, there's a concerted effort to enhance local manufacturing capabilities, foster technological transfer, and attract international partnerships. This trend sees these high-performance, sustainable materials being increasingly integrated across critical sectors such as mobility, construction, renewable energy, and even within the evolving oil and gas infrastructure, addressing demands for lighter, more durable, and corrosion-resistant alternatives. For instance, JEC Group will launch a series of composites events in Saudi Arabia, starting with a JEC Talks in June 2025 and a JEC Forum Middle East in 2026. This 3-year agreement with OSP and IFC Promosalons aims to accelerate the adoption of sustainable and nonmetallic materials, aligning with Saudi Vision 2030's economic diversification.

Competitive Landscape:

The top reinforcement materials companies are focusing on strategic initiatives such as mergers and acquisitions, partnerships, and expansions to strengthen their market positions and broaden their product portfolios. They are investing in research and development (R&D) to innovate and improve their materials, thereby enhancing properties like strength, durability, and sustainability. For instance, rapid advancements in carbon fiber and glass fiber technologies are enabling the production of lighter and more efficient composite materials. Additionally, these companies are expanding their manufacturing capacities and establishing new facilities, particularly in high-growth regions, to meet the rising demand. They are also exploring eco-friendly and bio-based reinforcement materials to align with global sustainability trends, which is positive impacting the reinforcement materials market’s recent opportunities and developments. In addition to this, many players are forming collaborations with automotive, aerospace, and construction industries to help them tailor their products to specific applications, while ensuring higher performance and compliance with stringent regulations.

The report provides a comprehensive analysis of the competitive landscape in the global reinforcement materials market with detailed profiles of all major companies, including:

- BASF SE

- Bekaert

- Century Enka Limited

- Cordenka GmbH & Co. KG

- DuPont de Nemours, Inc.

- Formosa Taffeta Co. Ltd.

- Hs Hyosung Advanced Materials

- Kolon Industries, Inc.

- Owens Corning

- Teijin Limited

- Toray Industries Inc.

- Toyobo Co. Ltd

Reinforcement Materials Market News:

- In February 2025, India-based Praana Group signed a definitive agreement to acquire Owens Corning's glass reinforcements business for USD 755 Million. This strategic move allows Owens Corning to focus on residential and commercial building products in North America and Europe. Praana Group gains a significant footprint in the global reinforcement materials market, spanning wind energy, infrastructure, industrial, transportation, and consumer sectors.

- In June 2024, JOGANI Reinforcement, a leading Indian producer of crack control concrete fibers, secured a 20-year patent for its innovative blended concrete fibers. This significant development is set to enhance concrete's vital parameters, aligning with the global focus on sustainable and durable construction materials. The company's director, Mahesh Kumar Jogani, emphasizes innovation as crucial for value creation in the concrete, infrastructure, and construction industries, especially concerning environmental friendliness.

- In May 2024, BASF committed to a sustainable future and has set itself the ambitious goal of reducing its Scope 3.1 emissions by 15% across its entire portfolio by 2030 and achieving net zero by 2050. The company’s one of the first steps is the partial use of glass fibers from sustainable production in BASF’s Ultramid A & B compound portfolio. These glass fibers are produced by 3B Fibreglass, a leading company and supplier of glass fiber solutions for the reinforcement of thermoplastic and thermoset polymers. To reduce its carbon footprint, it uses green electricity in production.

- In March 2024, Century Enka Limited announced that the company has commissioned the SSP and polyester spinning capacity to be used in polyester tyre cord fabric (PTCF). This announcement is in reference to its earlier communication in May 2021 regarding the investment of INR 2,400 million to strengthen its competitive position in the tyre reinforcement market by modernization of the plant & augmenting capacity and increasing the capacity of drawing texturized and mother yarn.

Reinforcement Materials Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered | Glass Fiber, Carbon Fiber, Aramid Fiber, Natural Fiber, Others |

| Applications Covered | Composite, Concrete, Others |

| End Use Industries Covered | Aerospace and Defense, Construction, Transportation, Wind Energy, Industrial and Consumer Goods, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BASF SE, Bekaert, Century Enka Limited, Cordenka GmbH & Co. KG, DuPont de Nemours, Inc., Formosa Taffeta Co. Ltd., Hs Hyosung Advanced Materials, Kolon Industries, Inc., Owens Corning, Teijin Limited, Toray Industries Inc., Toyobo Co. Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the reinforcement materials market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global reinforcement materials market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the reinforcement materials industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Reinforcement Materials Market Report

The global reinforcement materials market was valued at USD 24.2 Billion in 2025.

We expect the global reinforcement materials market to exhibit a CAGR of 5.59% during 2026-2034.

The rising utilization of reinforcement materials in fishing rods, storage tanks, and aircraft parts, owing to their low cost and high corrosion resistance, is primarily driving the global reinforcement materials market.

The sudden outbreak of the COVID-19 pandemic has led to the growing demand for reinforcementmaterials across the healthcare sector, in manufacturing swabs, disposable masks, and Personal Protective Equipment (PPE) to combat the risk of coronavirus infection.

Based on the material type, the global reinforcement materials market has been segmented into glass fiber, carbon fiber, aramid fiber, natural fiber, and others. Currently, glass fiber holds the majority of the total market share.

Based on the end use industry, the global reinforcement materials market can be divided into aerospace and defense, construction, transportation, wind energy, industrial and consumer goods, and others. Among these, the construction industry exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global reinforcement materials market include BASF SE, Bekaert, Century Enka Limited, Cordenka GmbH & Co. KG, DuPont de Nemours, Inc., Formosa Taffeta Co. Ltd., Hs Hyosung Advanced Materials, Kolon Industries, Inc., Owens Corning, Teijin Limited, Toray Industries Inc., and Toyobo Co. Ltd.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)