Radiation-Hardened Electronics Market Report by Product Type (Custom Made, Commercial-Off-the-Shelf), Material Type (Silicon, Silicon Carbide, Gallium Nitride, and Others), Technique (Radiation Hardening by Design (RHBD), Radiation Hardening by Process (RHBP), Radiation Hardening by Software (RHBS)), Component Type (Power Management, Application Specific Integrated Circuit, Logic, Memory, Field-Programmable Gate Array, and Others), Application (Space Satellites, Commercial Satellites, Military, Aerospace and Defense, Nuclear Power Plants, and Others), and Region 2026-2034

Radiation-Hardened Electronics Market Size:

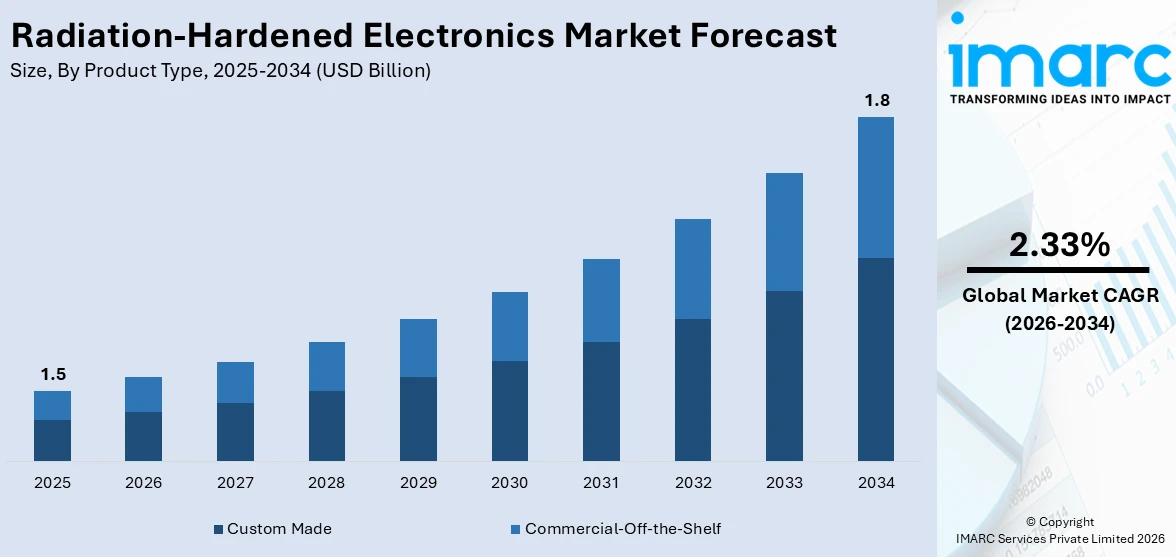

The global radiation-hardened electronics market size reached USD 1.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 1.8 Billion by 2034, exhibiting a growth rate (CAGR) of 2.33% during 2026-2034. The market is expanding primarily due to escalating product demand in space exploration, aerospace, and defense sectors. Furthermore, technological innovations and strategic collaborations foster advancements, while key challenges like elevated production costs present opportunities for companies to develop superior-performance and cost-efficient solutions.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2034 | USD 1.8 Billion |

| Market Growth Rate 2026-2034 | 2.33% |

Radiation-Hardened Electronics Market Analysis:

- Major Market Drivers: Some of the major drivers include heightening demand for resilient, radiation-resistant components across various sectors, such as space exploration, defense, and aerospace, where these components are requisite. The increasing focus on national security and the ongoing development of superior military technologies are further bolstering market growth. In addition, the surge in space missions and satellite deployments necessitates enhanced electronics deployment that are capable of enduring extreme cosmic conditions. Furthermore, rapid innovations in semiconductor technology and the accelerated adoption of radiation-hardened components in nuclear power and medical sector are also aiding in market expansion. Consequently, the radiation-hardened electronics market revenue is expected to surge due to expansion of these sectors.

- Key Market Trends: Key trends that steer the market growth include rapid inclination towards miniaturization of components, which is propelled by the demand for efficient and compact systems in defense and space applications. The incorporation of advanced technologies and materials, such as gallium nitride and silicon carbide, is improving the durability and performance of radiation-hardened devices. In addition, the market is experiencing amplified partnerships between private companies and government agencies to develop next-generation radiation-resistant components, particularly for space missions. The growing emphasis on reducing electronic waste and promoting sustainability is also influencing production processes and design formulation, further propelling radiation-hardened electronics demand.

- Geographical Trends: North America is the dominant region in the global market, principally due to the presence of major companies and significant government investments in defense and aerospace sectors. The U.S., in particular, boosts regional growth through its exceptional space programs, heavy military expenditure, and robust demand for radiation-hardened devices in crucial infrastructure. The region’s superior research and development (R&D) landscape further fosters innovation in radiation-resistant technologies. In addition, North America’s emphasis on maintaining technological leadership in space exploration and defense operations ensures its dominance, with rapid advancements in radiation-hardened devices.

- Competitive Landscape: Some of the major market players in the radiation-hardened electronics industry include Advanced Micro Devices, Inc., BAE Systems plc, Data Device Corporation (Transdigm Group Incorporated), Honeywell International Inc., Microchip Technology Inc, Renesas Electronics Corporation, STMicroelectronics, Teledyne Technologies Incorporated, Texas Instruments Incorporated, TTM Technologies Inc., VORAGO Technologies, among many others.

- Challenges and Opportunities: Some radiation-hardened electronics market recent opportunities include the potential for companies to develop high-performance, cost-effective solutions. Moreover, the increasing demand for radiation-hardened electronics in emerging industries, such as advanced medical equipment and commercial space travel, presents prominent growth potential. Companies that are currently investing in sustainable practices and research are anticipated to lead the market by capitalizing on these opportunities. However, the global market experiences some notable challenges, such as elevated development costs, complexity of incorporating advanced technologies, constrained availability of radiation-resistant materials, and elevated costs of development. In addition, the requirement for extensive validation and testing in harsh environments can delay product release, limiting market expansion.

To get more information on this market Request Sample

Radiation-Hardened Electronics Market Trends:

Increasing Product Demand in Satellites and Space Exploration Programs

The heightening emphasis on satellite deployments and space exploration is propelling the demand for radiation-hardened electronics. With more private enterprises and countries embarking on space missions, the requirement for dependable electronics that can endure cosmic radiation is increasing rapidly. Such components are crucial for ensuring the functionality and longevity of spacecrafts and satellites, which must in function in rigorous environments for prolonged periods. This trend is further bolstered by innovations in space technology, resulting in continuous inclination towards the adoption of radiation-hardened electronics in aerospace missions. For instance, in April 2024, U.S. Defense Advanced Research Projects Agency (DARPA) announced that it has entered into a USD 18.1 million contract with Northrop Grumman and RadiaBeam Technologies LLC to develop radiation-hardened 3D electronic components and circuits for space applications.

Rapid Advancements in Defense and Military Sectors

The radiation-hardened electronics market growth is significantly influenced by military and defense sectors due to the amplifying intricacies of modern warfare and the requirement for dependable systems in high-radiation and nuclear environments. Such electronics are requisite to ensure the robustness of navigation, weapons systems, and communication exposed to electronic warfare or nuclear operations. Additionally, the development of superior military technologies, including self-operating missile defense and systems, further bolsters the utilization of radiation-hardened devices, establishing them as indispensable components in improving nation defense and security capabilities. For instance, in June 2024, HEICO launched a radiation-hardened power supply DC-DC converter SLNP17-100, which offers low noise outputs and leverages multi-stage technique to cancel noise for conducted susceptibility and emissions. It is particularly designed for military space applications.

Rapid Shift Towards Smaller and More Efficient Electronics

The radiation-hardened electronics market report highlights a significant shift towards miniaturization, which is heavily influencing the market due to the amplifying need for compact and lightweight devices for defense as well as aerospace industries. As a result, manufacturers are currently emphasizing on the development of smaller components without compromising on radiation tolerance and performance. For instance, in September 2023, Efficient Power Conversion Corp unveiled two radiation-hardened field-effect transistors (FETs), particularly for space applications. These are 40 volt rated gallium nitride transistors which are cost-efficient, significantly small-sized, and offer excellent electrical performance. These can be used in DC-DC power converters, motor drivers, lidar, etc. This trend is critical for applications where weight and space constraints are crucial, such as in portable military devices or small satellites.

Radiation-Hardened Electronics Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product type, material type, technique, component type, and application.

Breakup by Product Type:

- Custom Made

- Commercial-Off-the-Shelf

Custom made accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product type. This includes custom made and commercial-off-the-shelf. According to the report, custom made represented the largest segment.

The radiation-hardened electronics market outlook points to the prominent domination of custom made product type globally, principally due to their crucial applications in defense, space exploration, and aerospace missions. As a result, with an increasing number of nations venturing into space missions and space launches, the dominance of this segment further strengthens. According to the Our World in Data, annually 2664 objects, including satellites probes, landers, spacecrafts, etc., were launched into space globally in 2023. These customized solutions provide improved performance and reliability, addressing the rigorous environmental demands with elevated radiation exposure. The amplifying complexity of technologies and missions further necessitates the adoption of these components, ultimately spurring the demand for custom made options. Their capability of addressing challenging operations makes them the excellent choice, fortifying their dominant stance in the global market.

Breakup by Material Type:

- Silicon

- Silicon Carbide

- Gallium Nitride

- Others

Silicon and silicon carbide holds the largest share of the industry

A detailed breakup and analysis of the market based on the material type have also been provided in the report. This includes silicon, silicon carbide, gallium nitride, and others. According to the report, silicon and silicon carbide accounted for the largest market share.

Silicon represents the largest market share due to its excellent radiation resistance, extensive availability, and cost-effectiveness. According to the radiation-hardened electronics market overview, the ability of silicon to sustain its functionality in high-radiation conditions makes it an ideal choice for crucial applications in defense, space exploration, and aerospace. In addition, advancements in silicon-based technology have improved reliability and performance, further spurring its adoption in manufacturing radiation-hardened electronics sector. Moreover, the segment’s domination is fortified by key manufacturers focusing on strategic partnerships to expand their production capacities. For instance, in April 2024, Infineon, a well-known manufacturer of silicon-based radiation-hardened semiconductors for space and military applications, announced partnership with Amkor Technology, Inc., to strengthen its manufacturing footprint in Europe.

Silicon carbide is another significant material type that dominates the global radiation-hardened electronics market due to its excellent performance in harsh environments. Its superior attributes like high resistance to radiation, exceptional thermal conductivity, and ability to function at high temperatures and voltages make it an integral component for electronics used in space, aerospace, and defense applications. Additionally, the growing demand for dependable and durable electronics in these sectors strengthens silicon carbide's leading position, driving its adoption in critical, high-reliability applications. For instance, in June 2023, UK Space Agency granted IceMOS Technology £300,000 for the development of radiation-tolerant, high-voltage silicon carbide power transistors for more effective high power distribution electrical systems on spacecrafts for deep space, middle earth orbit, and low earth orbit exploration.

Breakup by Technique:

- Radiation Hardening by Design (RHBD)

- Radiation Hardening by Process (RHBP)

- Radiation Hardening by Software (RHBS)

Radiation hardening by design (RHBD) represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the technique. This includes radiation hardening by design (RHBD), radiation hardening by process (RHBP), and radiation hardening by software (RHBS). According to the report, radiation hardening by design (RHBD) represented the largest segment.

According to the radiation-hardened electronics market forecast, radiation hardening by design (RHBD) segment is anticipated to sustain its prevailing position in the global market majorly due to its excellent reliability and cost-effectiveness. By designing the components to naturally resist radiation effects rather than leveraging radiation-hardened materials, it lowers the demand for additional protective measures as well as reduces the overall cost of production. According to a research article published in November 2023 in ScienceDirect, RHBD-based memory cells in transistor chips are more reliable and efficient, exhibiting enhanced stability under stress and reduced power consumption. By leveraging source isolation technology, RHBD cells minimize the number of radiation-sensitive parts, thereby significantly amplifying the robustness and radiation-hardening of electronic components.

Breakup by Component Type:

- Power Management

- Application Specific Integrated Circuit

- Logic

- Memory

- Field-Programmable Gate Array

- Others

Power management exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the component type have also been provided in the report. This includes power management, application specific integrated circuit, logic, memory, field-programmable gate array, and others. According to the report, power management accounted for the largest market share.

Power management represents the largest market segment due to their crucial role in facilitating the reliable functioning of electronics systems in extreme radiation conditions. Radiation-hardening is requisite for power management components as they are integral for managing the longevity and stability of systems, especially in defense and space applications where power fluctuation can result in catastrophic failures. For instance, in January 2023, Microchip Technology Inc. launched a power management solution MIC69300RT, which is the company’s first commercial-off-the-shelf radiation-tolerant power device. It is particularly designed for low-earth orbit (LEO) space applications. Additionally, the heightening demand for energy-efficient and robust power solutions further strengthens its dominance in the market.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Space Satellites

- Commercial Satellites

- Military

- Aerospace and Defense

- Nuclear Power Plants

- Others

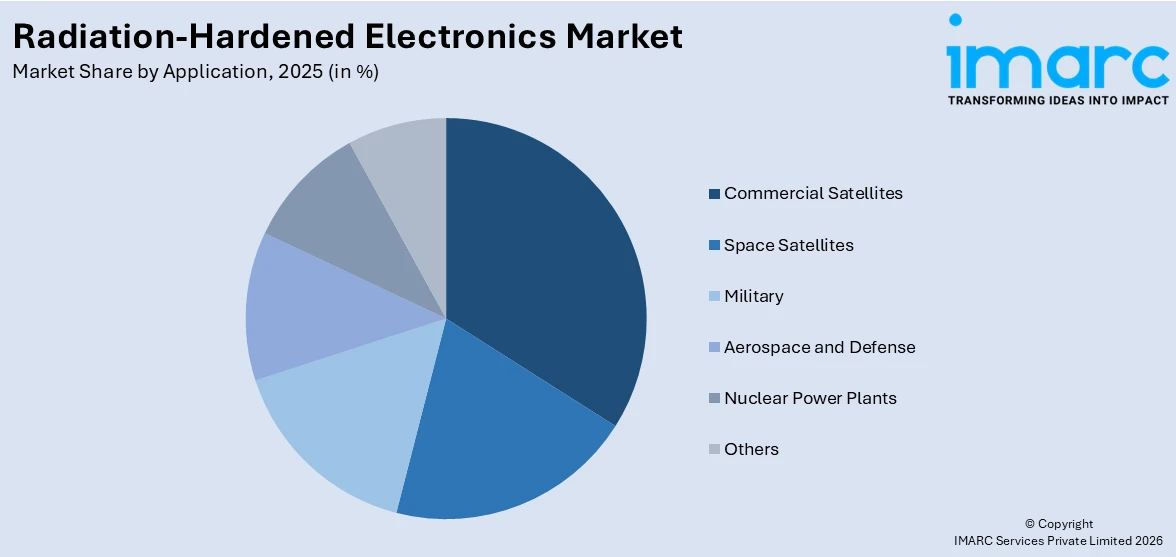

Commercial satellites dominate the market

The report has provided a detailed breakup and analysis of the market based on the application. This includes space satellites, commercial satellites, military, aerospace and defense, nuclear power plants, and others. According to the report, commercial satellites represented the largest segment.

The commercial satellite segment accounts for the largest market share due to the escalating demand for resilient components that can endure extreme space environments. With the expansion of commercial space industry, particularly due to propulsion of satellite-based navigation, earth observation, and communication services, the demand for high-performance electronics is boosting. According to Federal Aviation Administration, currently 31 navigation satellites are active in space. Additionally, according to recent data, 2024 has surpassed record number of commercial launches observed in 2023. This number is predicted to rise to 338 by 2028. Furthermore, commercial satellites heavily rely on radiation-hardened components to enhance their operational efficiency and longevity, spurring significant investments and adoption in the satellites sector.

Breakup by Region:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest radiation-hardened electronics market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represents the largest regional market for radiation-hardened electronics.

North America represents the largest regional market, primarily driven by heavy investments in space exploration, defense, and aerospace. For instance, in December 2023, Texas Legislature approved USD 350 million investment for Texas A&M research facility to maintain its leadership in the U.S. space exploration. In addition, USD 200 million of the total investment will be utilized for the construction of this facility next to NASA’S Johnson Space Center. Furthermore, the region’s magnified demand for advanced electronics in crucial applications, including satellite technologies and military systems, highlights its domination in the global market. Additionally, the radiation-hardened electronics market recent developments, such as advancements in R&D infrastructure and supportive government policies, further bolsters the expansion of the regional market, making North America a key player in the global market dynamics.

Competitive Landscape:

The competitive landscape of the global market is represented by the presence of severel leading radiation-hardened electronics companies that are focusing on tactical acquisitions and technological advancements. For instance, in June 2024, Honeywell Inc. announced the strategic acquisition of CAES Systems Holdings LLC to boost its capabilities in radiation-hardened integrated circuits for defense technologies in crucial military systems, including aircrafts, radars, weapons, and uncrewed systems. Furthermore, these companies are heavily investing in R&D to improve product functionality and proliferate their portfolios. Strategic partnerships with defense, space, and aerospace agencies are key to secure market positioning and contracts. In addition, the market is witnessing intensified competition as emerging companies are launching cost-efficient solutions to challenge established players, thereby maintaining the competitive edge.

The report provides a comprehensive analysis of the competitive landscape in the global radiation-hardened electronics market with detailed profiles of all major companies, including:

- Advanced Micro Devices, Inc.

- BAE Systems plc

- Data Device Corporation (Transdigm Group Incorporated)

- Honeywell International Inc.

- Microchip Technology Inc

- Renesas Electronics Corporation

- STMicroelectronics

- Teledyne Technologies Incorporated

- Texas Instruments Incorporated

- TTM Technologies Inc.

- VORAGO Technologies

Radiation-Hardened Electronics Market News:

- In June 2024, Infineon Technologies AG announced the availability of its newly launched radiation-hardened 1 and 2 Mb parallel interface ferroelectric-RAM (F-RAM) nonvolatile memory devices. This new addition to Infineon's product portfolio exhibits excellent endurance and reliability, with up to 120 years of data retention at 85°C. It is ideally developed for space-based applications.

- In May 2024, Microchip Technology Inc. expanded its radiation-tolerant microcontroller portfolio by launching SAMD21RT MCU. This microcontroller is specifically designed for space-constrained applications to function efficiently in harsh environments.

Radiation-Hardened Electronics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Custom Made, Commercial-Off-the-Shelf |

| Material Types Covered | Silicon, Silicon Carbide, Gallium Nitride, Others |

| Techniques Covered | Radiation Hardening by Design (RHBD), Radiation Hardening by Process (RHBP), Radiation Hardening by Software (RHBS) |

| Component Types Covered | Power Management, Application Specific Integrated Circuit, Logic, Memory, Field-Programmable Gate Array, Others |

| Applications Covered | Space Satellites, Commercial Satellites, Military, Aerospace and Defense, Nuclear Power Plants, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Advanced Micro Devices, Inc., BAE Systems plc, Data Device Corporation (Transdigm Group Incorporated), Honeywell International Inc., Microchip Technology Inc, Renesas Electronics Corporation, STMicroelectronics, Teledyne Technologies Incorporated, Texas Instruments Incorporated, TTM Technologies Inc., VORAGO Technologies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the radiation-hardened electronics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global radiation-hardened electronics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the radiation-hardened electronics industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global radiation-hardened electronics market was valued at USD 1.5 Billion in 2025.

We expect the global radiation-hardened electronics market to exhibit a CAGR of 2.33% during 2026-2034.

The widespread adoption of radiation-hardened electronics for protecting equipment from physical damage and failure caused by harmful radiations in outer space is primarily driving the global radiation-hardened electronics market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary closure of numerous manufacturing units for radiation-hardened electronics.

Based on the product type, the global radiation-hardened electronics market can be segmented into custom made and commercial-off-the-shelf. Currently, custom made holds the majority of the total market share.

Based on the material type, the global radiation-hardened electronics market has been divided into silicon, silicon carbide, gallium nitride, and others. Among these, silicon and silicon carbide currently exhibits a clear dominance in the market.

Based on the technique, the global radiation-hardened electronics market can be categorized into Radiation Hardening by Design (RHBD), Radiation Hardening by Process (RHBP), and Radiation Hardening by Software (RHBS). Currently, Radiation Hardening by Design (RHBD) accounts for the majority of the global market share.

Based on the component type, the global radiation-hardened electronics market has been segregated into power management, application specific integrated circuit, logic, memory, field-programmable gate array, and others. Among these, power management currently holds the largest market share.

Based on the application, the global radiation-hardened electronics market can be bifurcated into space satellites, commercial satellites, military, aerospace and defense, nuclear power plants, and others. Currently, commercial satellites exhibit a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global radiation-hardened electronics market include Advanced Micro Devices, Inc., BAE Systems plc, Data Device Corporation (Transdigm Group Incorporated), Honeywell International Inc., Microchip Technology Inc, Renesas Electronics Corporation, STMicroelectronics, Teledyne Technologies Incorporated, Texas Instruments Incorporated, TTM Technologies Inc., VORAGO Technologies, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)