Radar System Market Report by Type (Pulse Radar, Continuous Wave (CW) Radar), Component (Antenna, Transmitter, Receiver, and Others), Range (Short Range Radars, Medium Range Radars, Long Range Radars), Application (Air Traffic Control, Remote Sensing, Ground Traffic Control, Space Navigation and Control, and Others), Frequency Band (X Band, S Band, C Band, and Others), and Region 2026-2034

Radar System Market Overview:

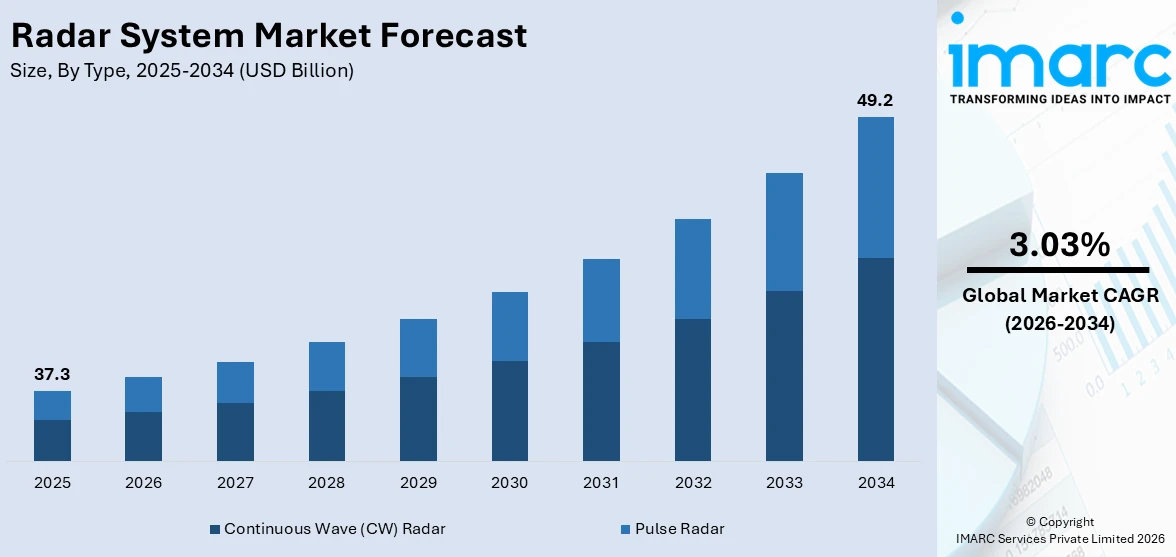

The global radar system market size reached USD 37.3 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 49.2 Billion by 2034, exhibiting a growth rate (CAGR) of 3.03% during 2026-2034. The growing need for effective navigation and safety systems, rising demand for precise weather monitoring and forecasting, and continuous technological advancements and innovations that enhance performance and expand capabilities are some of the factors impelling the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 37.3 Billion |

|

Market Forecast in 2034

|

USD 49.2 Billion |

| Market Growth Rate 2026-2034 | 3.03% |

Radar System Market Analysis:

- Major Market Drivers: The market is experiencing stable growth because of the increasing demand for surveillance systems in the defense and aerospace sectors, rising need for air traffic control systems, and advancements in autonomous vehicle technologies that rely on radar for navigation and safety.

- Key Market Trends: The development of next-generation radar systems, such as phased-array radars and synthetic aperture radars, which offer enhanced precision and range, is propelling the market growth. Additionally, the growing use of artificial intelligence (AI) and machine learning (ML) for improving radar capabilities is positively influencing the market.

- Geographical Trends: North America leads the market because of the growing investment in defense and aerospace technologies and the presence of major radar system manufacturers. In addition, the rising demand for radar technology in the automotive sector for advanced driver-assistance systems (ADAS) and autonomous vehicles is supporting the market growth in this region.

- Competitive Landscape: Some of the major market players in the industry include BAE Systems Plc, Dassault Aviation, General Dynamics Corporation, Honeywell International Inc., L3harris Technologies, Inc., Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Company, Rockwell Collins Inc., SAAB AB, and Thales Group.

- Challenges and Opportunities: Challenges consist of high development expenses and regulatory limitations, especially in developing economies. However, there are opportunities in the adoption of radar systems in commercial sectors, such as automotive and maritime, and the ongoing modernization of military equipment worldwide.

To get more information on this market Request Sample

Radar System Market Trends:

Growing Demand for Traffic Control and Management

With the rise of international trade and the increase in maritime activities, there is a heightened need for effective navigation and safety systems. Radar systems play a vital role in ensuring safe navigation by providing accurate information on the locations and movements of ships, especially in busy sea routes and adverse weather conditions. They aid in avoiding accidents, enhancing the understanding about a situation, and improving the effectiveness of port activities. Moreover, geopolitical tensions and the need to maintain a strategic military presence are resulting in higher defense budgets, which support the procurement of modern radar systems. Saab Inc. was given a $47.5 million contract by the US Navy in 2024 to produce three AN/SPN-50(V) 1 shipboard air traffic control radar systems for aircraft carriers and amphibious assault ships. The AN/SPN-50(V) 1, equipped with Saab's Sea Giraffe flexible multi-beam radar technology, helps to improve the current AN/SPN-43C systems by enhancing air traffic control capabilities within a 50-nautical-mile radius.

Advancements in Weather Monitoring Systems

The growing demand for detailed data on precipitation, storm patterns, wind speed, and atmospheric conditions is offering a favorable market outlook. Weather radar technology is vital in identifying and monitoring weather events like storms, precipitation, and wind movements, essential for aviation safety, agriculture, disaster response, and public safety. Recent developments in radar technology, including dual-polarization radar and phased array systems, are enhancing the precision and dependability of weather forecasts. These improvements allow for improved identification of extreme weather occurrences, aiding in early alerts and readiness. In 2024, Taiwan's Central Weather Administration (CWA) revealed plans to implement a new dual-polarization radar system for improved weather predictions and monitoring of bird movements. This radar can distinguish rain, snow, and hail, as well as pick up signals from migrating birds like Chinese sparrowhawks and gray-faced buzzards in Taiwan heading to Southeast Asia.

Technological Innovations in Radar Systems

Manufacturers are creating advanced radar technologies to meet the changing requirements of contemporary security and defense applications. Modern radar systems incorporate elements such as gallium nitride (GaN) amplifiers, which enhance long-range detection and target precision while also conserving energy. These developments are especially crucial in dealing with novel risks where accurate detection and fast response are essential. In addition, the advent of adaptable radar designs that can be seamlessly integrated into different platforms is allowing them to be used for various purposes like military defense and environmental monitoring. Moreover, Toshiba Infrastructure Systems & Solutions Corporation confirmed it will present its newest radar technologies at Eurosatory 2024 in Paris, France, between June 17 and 21. The showcase will present Toshiba's counter-unmanned aircraft system (C-UAS), a 3D radar for coastal surveillance with GaN amplifiers for long-distance detection and radar modules for flexible integration into different systems. These advancements showcase Toshiba's dedication to offering dependable, eco-friendly solutions for improved security and defense.

Radar System Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on type, component, range, application, and frequency band.

Breakup by Type:

- Pulse Radar

- Continuous Wave (CW) Radar

Continuous wave (CW) radar accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the type. This includes pulse radar and continuous wave (CW) radar. According to the report, continuous wave (CW) radar represented the largest segment.

Continuous wave (CW) radars account for the majority of the market share, driven by its superior capabilities in target detection and velocity measurement. They perform by constantly emitting a signal, which makes it effective for applications requiring precise speed and distance calculations like automotive radar for adaptive cruise control and collision avoidance systems. The growing adoption of advanced driver-assistance systems (ADAS) and autonomous vehicles is driving the demand for CW radar technology. In 2025, the University of Cape Town (UCT) UCT introduced a novel method using CW radar to evaluate Antarctic Sea ice levels. The main objective of this project is to utilize stepped frequency continuous wave (SFCW) radar on the SAS Agulhas II, a South African icebreaker, to collect accurate information on sea ice thickness and characteristics in Antarctica. This data is crucial for understanding the unique attributes of Antarctic Sea ice in comparison to Arctic ice.

Breakup by Component:

- Antenna

- Transmitter

- Receiver

- Others

Antenna holds the largest share of the industry

A detailed breakup and analysis of the market based on the component have also been provided in the report. This includes antenna, transmitter, receiver, and others. According to the report, antenna accounted for the largest market share.

Antenna holds the biggest market share as it plays a crucial role in defining the range, precision, and overall capabilities of the radar. It is vital in transmitting and receiving electromagnetic waves, which is necessary for radar systems to operate effectively in a variety of sectors, including military, aerospace, automotive, and maritime. Advances in antenna technology like phased array and electronically scanned antennas, are improving radar capabilities and increasing adoption. The rising need for advanced radar systems in defense for surveillance, navigation, and threat detection, as well as the rise of autonomous vehicles and intelligent transportation systems, are propelling the market growth. In 2025, Hanwha Systems revealed an agreement with Leonardo SpA to provide AESA antenna units for light combat aircraft, with deliveries commencing in September 2025. The cooperation entails working together to develop AESA radars for improving performance in contemporary air combat and promoting exports worldwide.

Breakup by Range:

- Short Range Radars

- Medium Range Radars

- Long Range Radars

Short range radars represent the leading market segment

The report has provided a detailed breakup and analysis of the market based on the range. This includes short range radars, medium range radars, and long range radars. According to the report, short range radars represented the largest segment.

Short range radars exhibit a clear dominance in the market segment because of their widespread use in automotive safety applications and various industrial settings. These radars are created for detecting objects in close range, which makes them ideal for tasks including parking aid, blind-spot warning, collision alert, and other ADAS in vehicles. The growing focus on improving vehicle safety standards and the increasing usage of autonomous vehicles are driving the need for short-range radars. Additionally, their affordability and capacity to deliver accurate, immediate information in crowded settings make them the preferred choice for both automotive manufacturers and industrial users.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Air Traffic Control

- Remote Sensing

- Ground Traffic Control

- Space Navigation and Control

- Others

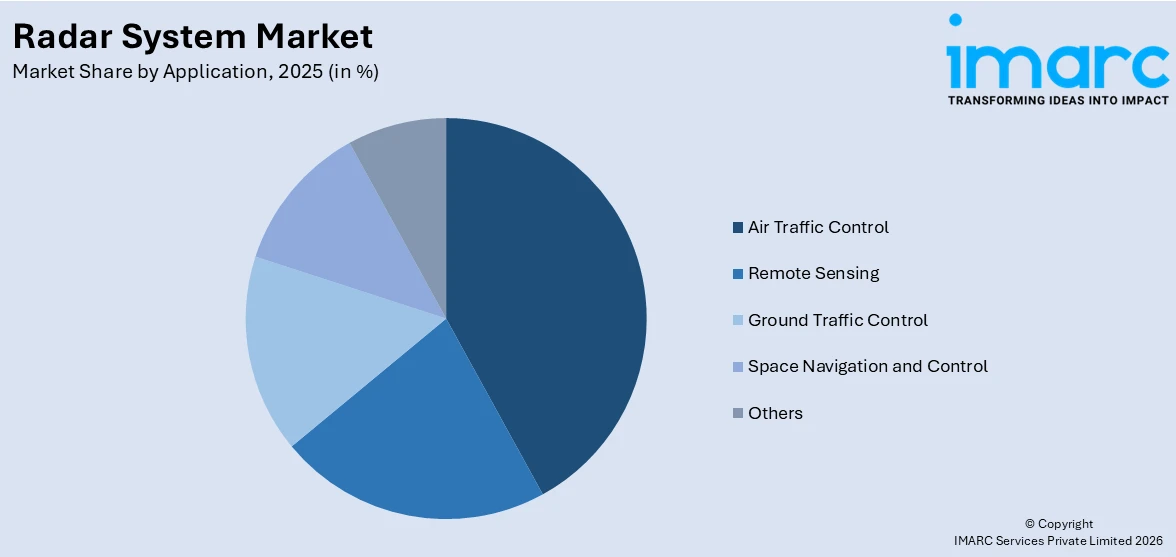

Air traffic control exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes air traffic control, remote sensing, ground traffic control, space navigation and control and others. According to the report, air traffic control accounted for the largest market share.

Air traffic control represents the largest segment, driven by the critical need for reliable and accurate radar systems to ensure the safety and efficiency of air travel. Radar systems play a crucial role in air traffic control by monitoring aircraft positions, managing flight paths, and preventing collisions, making them vital for both civil and military aviation. The increasing worldwide air travel, along with the modernization of airport infrastructure and the implementation of stricter safety regulations, are driving the demand for advanced radar systems in this segment. Moreover, enhancements in radar technology, such as automated tracking integration and improved surveillance abilities, are bolstering the market growth. In 2025, Hensoldt Australia revealed the first operational capability (IOC) of a new Air Traffic Control (ATC) radar sensor for the Royal Australian Air Force (RAAF) under the AIR5431 Phase 2 initiative. The goal of the program is to improve surveillance capabilities at Australian Defence Force bases by upgrading old air traffic systems and sensors.

Breakup by Frequency Band:

- X Band

- S Band

- C Band

- Others

X band dominates the market

The report has provided a detailed breakup and analysis of the market based on the frequency band. This includes X band, S band, C band and others. According to the report, X band represented the largest segment.

X band holds the biggest market share due to its versatility and effectiveness in a wide range of applications, including military, aviation, marine, and weather monitoring. X band radars work within a higher frequency range of 8 to 12 GHz, resulting in improved target discrimination and finer resolution. This specific frequency range is highly preferred for tasks that require precision and accuracy, such as military surveillance, airborne radars, and maritime vessel traffic control. Furthermore, the ability of the X band to perform well in different weather conditions and its compatibility with high-resolution imaging are leading to its widespread usage across various industries. In 2025, HENSOLDT UK revealed the approval of its Manta NEO X band radar system, which targets the commercial shipping industry. The Manta NEO X band radar provides excellent target separation, precise long-range resolution, and reliable performance.

Breakup by Regional:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest radar system market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represents the largest regional market for radar system.

North America dominates the market owing to the rising investment in defense and aerospace technologies and the presence of major radar system manufacturers. The growing demand for advanced radar systems, driven by its extensive military modernization programs, border security needs, and focus on enhancing air traffic control systems, is offering a favorable market outlook. Additionally, the adoption of radar technology in the automotive sector for ADAS and autonomous vehicles is supporting the market growth in this region. In 2025, Northrop Grumman Corporation announced it has been awarded a multi-year contract to begin production of the AN/APR-39E(V)2 radar warning receivers for the US Army. This advanced digital radar warning system features clutter reduction, threat geolocation capabilities, and a smart antenna to detect a wide range of radar threats, enhancing warfighter survivability.

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the industry include BAE Systems Plc, Dassault Aviation, General Dynamics Corporation, Honeywell International Inc., L3harris Technologies, Inc., Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Company, Rockwell Collins Inc., SAAB AB, Thales Group, etc.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- Key players in the market are focusing on innovation, strategic partnerships, and expansion to maintain competitive advantages and meet evolving user demands. Companies are investing heavily in research operations to enhance radar capabilities, such as improving accuracy, range, and target detection, while also reducing costs and system size. Additionally, there is a strong emphasis on integrating advanced technologies like AI and ML into radar systems to enable smarter, more adaptive solutions for defense, automotive, aviation, and other critical sectors. In 2024, the Indra-led consortium under the European Defense Agency (EDA) completed the development of an AESA radar prototype for the Future Combat Air System (FCAS) program involving France, Germany, and Spain. Funded by the European Commission, the €10 million project, named 'CROWN,' aims to enhance defense capabilities by integrating radar, communications, and electronic warfare functions into a single radio frequency (RF) system.

Radar System Market News:

- June 2024: SAAB announced the Giraffe 1X Compact Radar Module at Eurosatory 2024, designed as an all-in-one solution to enhance mobility and rapid deployment for operational needs. This radar system provides advanced air defense target data, drone detection, and continuous software upgrades to address emerging threats.

- January 2023: The Lithuanian Defence Material Agency signed an agreement with the Dutch procurement Agency COMMIT to acquire Thales Ground Master 200 Multi-Mission Compact (GM200 MM/C) radars. These radars enhanced Lithuania’s counter-battery operations by providing advanced situational awareness, fire support, and weapon location capabilities, while also supporting air defense against various threats, including drones.

Radar System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Pulse Radar, Continuous Wave (CW) Radar |

| Components Covered | Antenna, Transmitter, Receiver, Others |

| Ranges Covered | Short Range Radars, Medium Range Radars, Long Range Radars |

| Applications Covered | Air Traffic Control, Remote Sensing, Ground Traffic Control, Space Navigation and Control, Others |

| Frequency Bands Covered | X Band, S Band, C Band, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BAE Systems Plc, Dassault Aviation, General Dynamics Corporation, Honeywell International Inc., L3harris Technologies, Inc., Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Company, Rockwell Collins Inc., SAAB AB, Thales Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, radar system market forecasts, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the radar system industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

The radar system market was valued at USD 37.3 Billion in 2025.

We expect the global radar system market to exhibit a CAGR of 3.03% during 2026-2034.

The rising demand for radar systems as they offer enhanced safety and security, improved efficiency, and enhanced situational awareness, is primarily driving the global radar system market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the decline of various aviation activities, thereby negatively impacting the global market for radar systems.

Based on the type, the global radar system market can be bifurcated into pulse radar and Continuous Wave (CW) radar. Currently, Continuous Wave (CW) radar holds the majority of the total market share.

Based on the component, the global radar system market has been segmented into antenna, transmitter, receiver, and others, where antenna currently exhibits a clear dominance in the market.

Based on the range, the global radar system market can be divided into short range radars, medium range radars, and long range radars. Currently, short range radars account for the largest market share.

Based on the application, the global radar system market has been segregated into air traffic control, remote sensing, ground traffic control, space navigation and control, and others. Among these, air traffic control currently holds the majority of the global market share.

Based on the frequency band, the global radar system market can be categorized into X Band, S Band, C Band, and others. Currently, X band exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global radar system market include BAE Systems Plc, Dassault Aviation, General Dynamics Corporation, Honeywell International Inc., L3harris Technologies, Inc., Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Company, Rockwell Collins Inc., SAAB AB, Thales Group, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)