Shrimp Market Size, Share, Trends and Forecast by Environment, Species, Shrimp Size, Distribution Channel, and Region, 2026-2034

Global Shrimp Market Size, Share, Trends & Forecast (2026-2034)

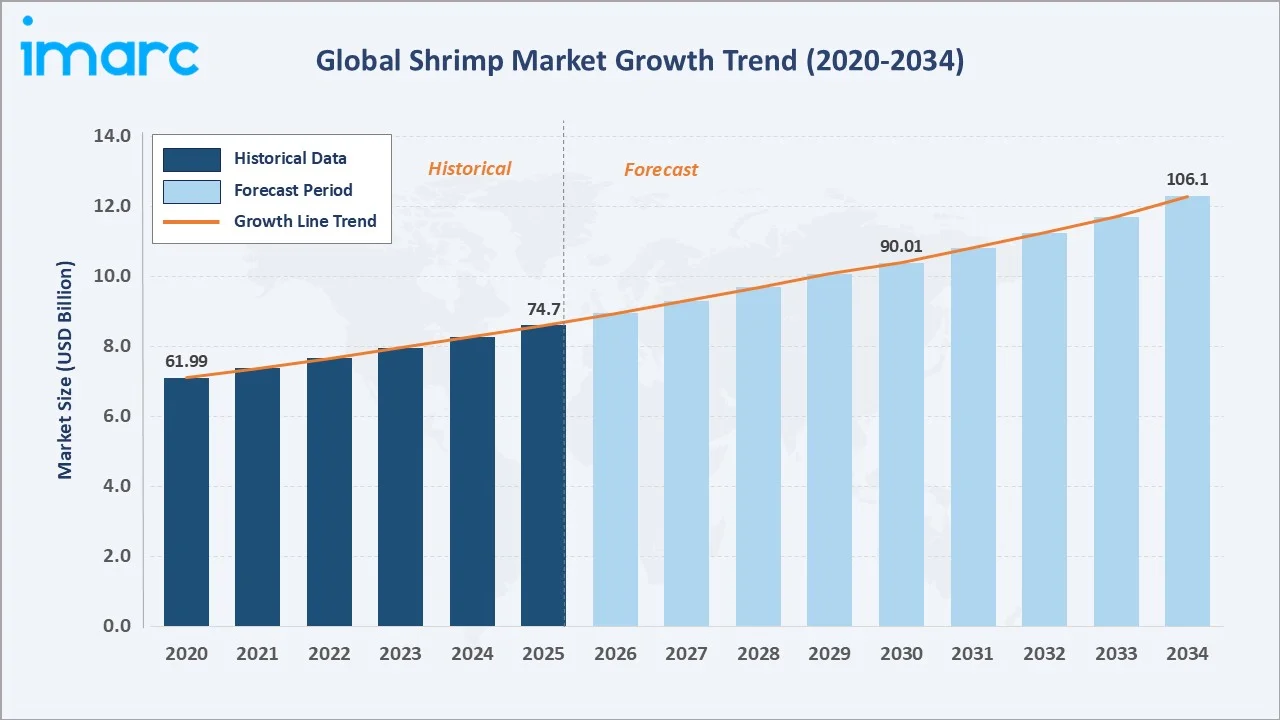

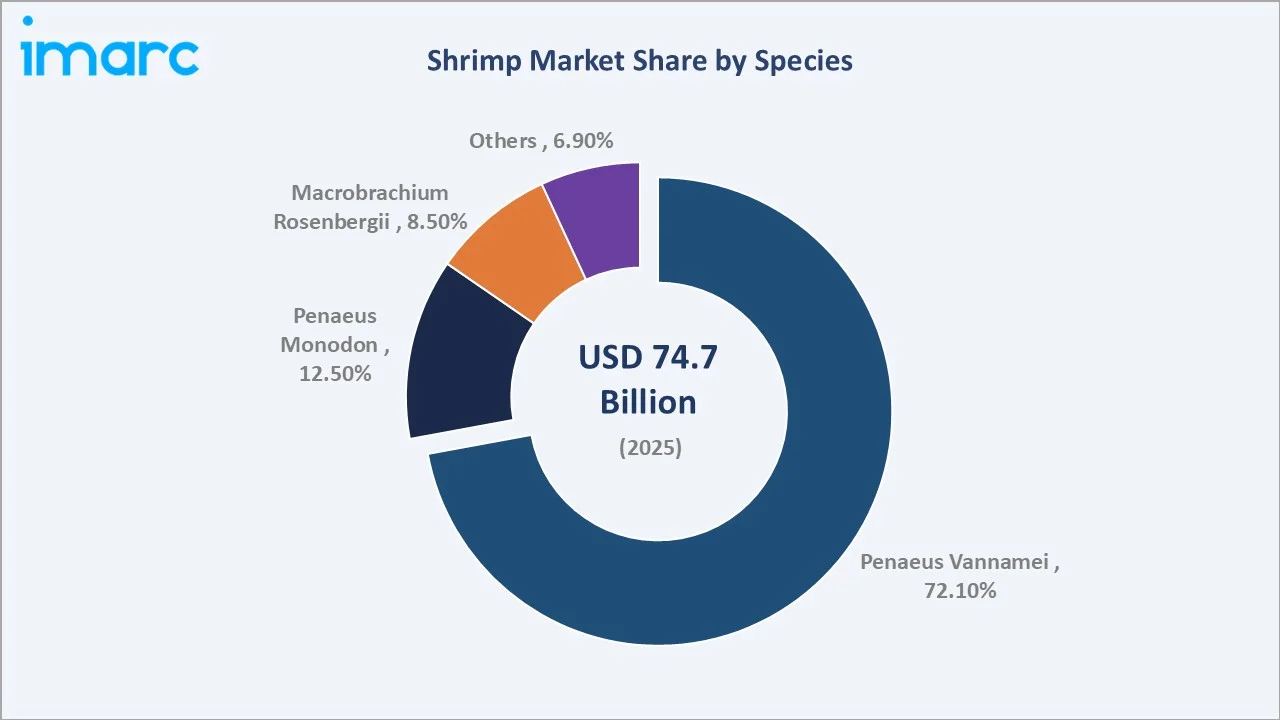

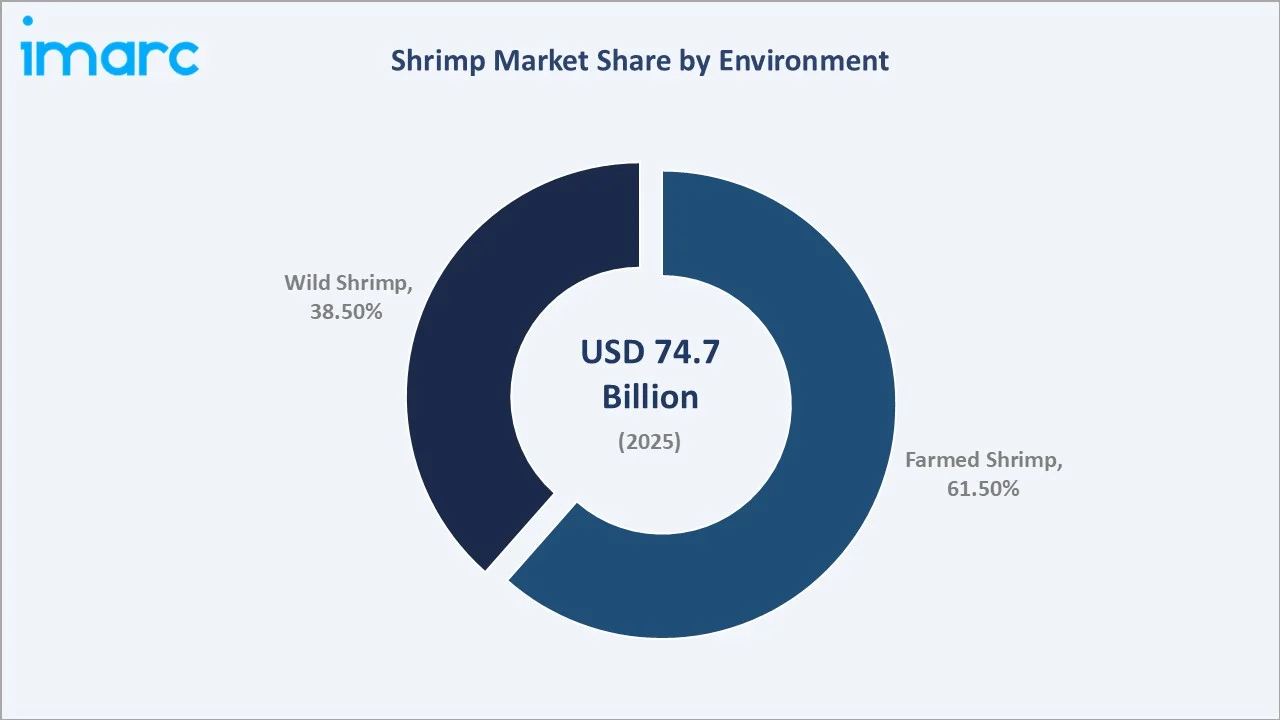

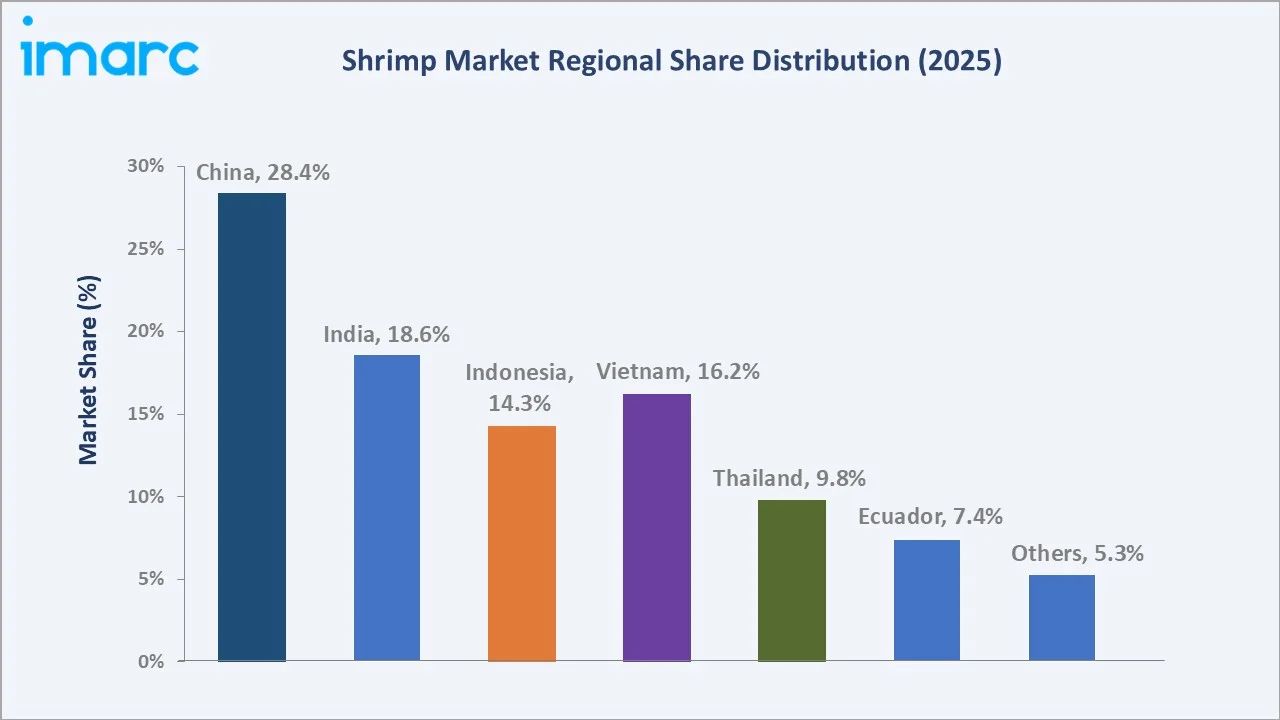

The global shrimp market reached a value of USD 74.7 Billion in 2025 and is projected to reach USD 106.1 Billion by 2034, exhibiting a CAGR of 3.80% during the forecast period (2026-2034). The market is supported by rising global seafood consumption, rapid advancements in aquaculture technology, growing health awareness around shrimp's high-protein and low-fat nutritional profile, and expanding food service and retail distribution networks. China dominates production with a 28.4% share of the global shrimp producing market in 2025, followed by India (18.6%), Vietnam (16.2%), and Indonesia (14.3%). Penaeus vannamei (whiteleg shrimp) leads by species at 72.1% (2025), favored for its high yield, farming adaptability, and strong global export demand. The market is expected to reach USD 90.01 Billion by 2030. Key industry players include Thai Union Group PCL, Charoen Pokphand Foods, Avanti Feeds Limited, High Liner Foods, and Clearwater Seafoods.

Market Snapshot

|

Metric |

Value |

|

Market Size (2020) |

USD 61.99 Billion |

|

Market Size (2025) |

USD 74.7 Billion |

|

Market Size (2030) |

USD 90.01 Billion |

|

Forecast Market Size (2034) |

USD 106.1 Billion |

|

CAGR (2026-2034) |

3.80% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Producing Region |

China (28.4%, 2025) |

|

Dominant Species |

Penaeus Vannamei (72.1%, 2025) |

|

Leading Environment |

Farmed Shrimp (61.5%, 2025) |

From USD 61.99 Billion in 2020 to USD 74.7 Billion in 2025, the shrimp market demonstrated consistent resilience despite COVID-19-related supply chain disruptions. The forecast addition of USD 31.4 Billion through 2034 reflects structural demand momentum anchored by population growth, rising middle-class seafood adoption, and ongoing aquaculture productivity gains.

To get more information on this market, Request Sample

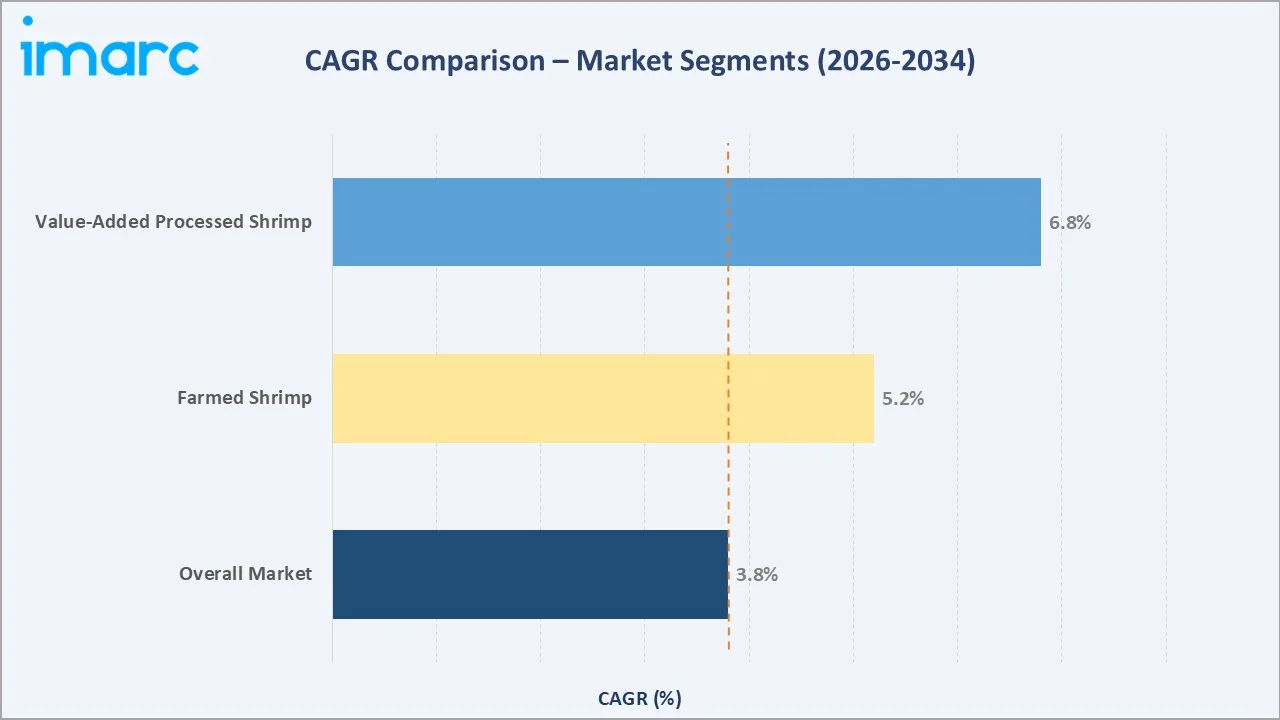

The 3.80% CAGR over 2026–2034 reflects a steady, resilience-backed expansion. Farmed shrimp, commanding a 61.5% share in 2025, is the primary volume driver, enabled by improvements in biosecurity, genetics, and feed technology that have materially reduced production costs per kilogram since 2018.

Executive Summary

The global shrimp market stood at USD 74.7 Billion in 2025, driven by the convergence of rising global seafood demand, technological advances in aquaculture farming systems, and expanding middle-class protein consumption in Asia, North America, and Europe. The market is forecast to reach USD 106.1 Billion by 2034 at a CAGR of 3.80%, passing USD 90.01 Billion by 2030. Penaeus vannamei dominates the species landscape at 72.1% (2025), followed by Penaeus monodon (12.5%) and Macrobrachium rosenbergii (8.5%). Farmed shrimp account for 61.5% of the total market in 2025, underscoring the structural shift away from wild capture toward sustainable aquaculture.

From a producing-region perspective, China leads at 28.4% (2025), followed by India (18.6%), Vietnam (16.2%), Indonesia (14.3%), Thailand (9.8%), and Ecuador (7.4%). These six nations collectively control over 74% of global shrimp supply, with significant production cost competitiveness, government support programs, and improving biosecurity standards driving continued export growth. Key market trends include the rise of value-added processed shrimp products, blockchain-enabled traceability, e-commerce seafood distribution, and aquaculture certification programs including ASC and BAP.

Leading companies including Thai Union Group PCL, Charoen Pokphand Foods, Avanti Feeds, and High Liner Foods are investing in sustainable aquaculture, cold chain expansion, and direct-to-consumer digital channels to capture the next phase of growth. In November 2024, Prime Shrimp expanded into over 200 Whole Foods Market locations across the U.S., exemplifying the accelerating premiumization trend in branded, convenient shrimp product formats.

Key Market Insights

|

Insight |

Data |

|

Largest Species |

Penaeus Vannamei – 72.1% (2025) |

|

Leading Environment |

Farmed Shrimp – 61.5% (2025) |

|

Largest Producing Region |

China – 28.4% (2025) |

|

Fastest Growing Producer |

India (~6.5% CAGR, 2026–2034) |

|

Top Companies |

Thai Union, Charoen Pokphand, Avanti Feeds, High Liner, Clearwater |

Key Analytical Observations Supporting the Above Data:

- Penaeus vannamei’s 72.1% species dominance (2025) reflects its superior adaptability to intensive farming, high survival rates, faster growth cycles versus other species, and broad consumer acceptance across Asian, European, and North American markets.

- Farmed shrimp’s 61.5% share (2025) underlines the structural shift away from wild-catch, driven by aquaculture productivity gains, lower per-unit costs via RAS and biofloc systems, and growing sustainability certification adoption.

- China's 28.4% producing share (2025) reflects deep integration of shrimp farming with industrial-scale processing and export infrastructure, supported by government-funded aquaculture development programs and proximity to key consumption markets in Asia.

- India's shrimp export sector is growing at approximately 6.5% CAGR, with the country emerging as the preferred low-cost, high-quality alternative sourcing market for U.S. and EU buyers seeking China supply chain diversification.

- Ecuador's 7.4% share (2025) is growing rapidly, with the country becoming the top shrimp supplier to China and Europe, leveraging cost-competitive vannamei farming and expanding certified-sustainable production capacity.

- Value-added processed shrimp, including frozen peeled, breaded, cooked, and marinated formats are growing at above-market rates, driven by food service demand and consumer preference for convenient, ready-to-cook seafood products.

Global Shrimp Market Overview

Shrimp is the world's most traded seafood commodity by value, representing a critical component of the global aquaculture and seafood processing ecosystem. The market encompasses the farming, processing, and distribution of multiple shrimp species across farmed and wild-capture environments, serving retail consumers, food service operators, and institutional buyers across 150+ countries. As of 2025, the market is valued at USD 74.7 Billion and supports livelihoods for an estimated 20+ million people across the aquaculture, processing, and trade value chain globally. Macroeconomic tailwinds including rising disposable incomes in emerging markets, global protein demand growth, and health-driven seafood consumption trends are sustaining long-term demand expansion, while aquaculture technology innovation is enabling producers to meet this demand with improved quality, consistency, and environmental compliance. Despite the high tariffs in the United States and low imports in China,exports of global shrimp were valued at 2.93 million tonnes in quantity and USD 21.62 billion in value during January to September 2025; these are up by 4.5% in quantity and 12% in value over the previous year.

Market Dynamics

To evaluate market opportunities, Request Sample

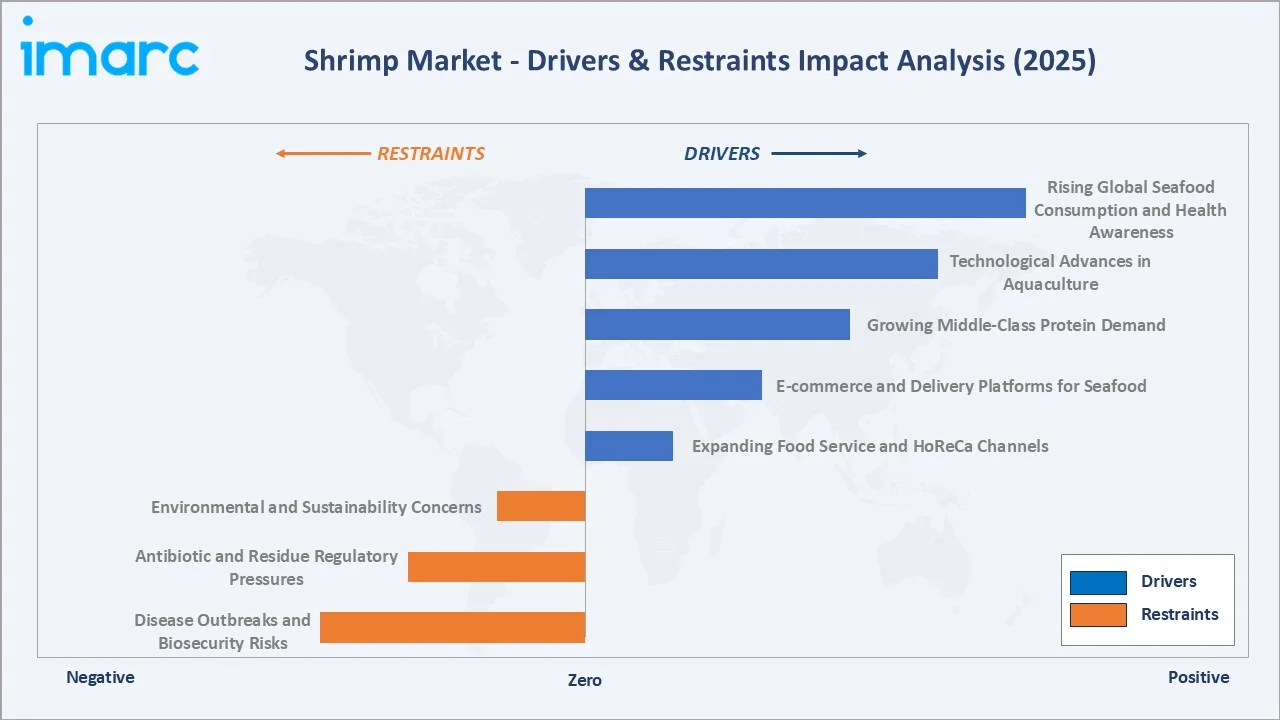

Market Drivers

- Rising Global Seafood Consumption and Health Awareness: Shrimp is increasingly favored by health-conscious consumers for its high protein (20g/100g), low fat, and rich omega-3 and selenium content. In Europe, shrimp retail prices ranged from USD 33–67/kg in H1 2023, reflecting robust premium demand. Rising incomes and urbanization in Asia and Latin America are broadening the consumer base rapidly.

- Technological Advances in Aquaculture: Innovations including biofloc systems, recirculating aquaculture systems (RAS), specific pathogen-free (SPF) broodstock genetics, and AI-powered pond monitoring are reducing disease losses, improving feed conversion ratios, and enabling year-round production in previously unsuitable geographies.

- Growing Middle-Class Protein Demand: The expanding middle class in China, India, Southeast Asia, and Latin America is shifting dietary patterns toward higher-value animal proteins including seafood. China’s total shrimp production over the last 20 years, with a growth rate of 120%, representing an average annual growth rate of 4.3%, creating demand absorption that complements export market growth.

- E-commerce and Delivery Platforms for Seafood: Online seafood retail is growing rapidly, with platforms including Amazon Fresh, Instacart, and specialized seafood subscription services expanding consumer access to premium shrimp products. In November 2024, Prime Shrimp expanded into 200+ Whole Foods locations across the U.S., exemplifying the trend toward branded, convenient, ready-to-cook shrimp retail formats.

- Expanding Food Service and HoReCa Channels: Shrimp is among the most widely consumed seafood in restaurant settings globally. The recovery and expansion of the food service sector post-2021 has significantly boosted shrimp procurement volumes, with QSR chains, casual dining groups, and catering businesses increasing shrimp-featuring menu items. These drivers create compounding demand, urbanization and income growth expand the consumer base; technology innovation enables cost-competitive supply; e-commerce and food service distribution broaden market access.

Market Restraints

- Disease Outbreaks and Biosecurity Risks: Shrimp disease, particularly Early Mortality Syndrome (EMS), White Spot Syndrome Virus (WSSV), and Vibrio bacteria, continues to cause significant annual production losses. EMS devastated production in China, Thailand, and Vietnam in the early 2010s and remains a latent risk to global supply stability.

- Antibiotic and Residue Regulatory Pressures: Importing markets including the EU, U.S., and Japan maintain strict residue limits for antibiotics including nitrofurans, chloramphenicol, and oxytetracycline. Non-compliance results in import bans and significant trade losses. India and Ecuador face periodic scrutiny, requiring sustained compliance investment from exporters.

- Environmental and Sustainability Concerns: Shrimp farming's historical association with mangrove destruction, water pollution, and high-density stocking practices continues to attract regulatory and NGO scrutiny. Meeting ASC, BAP, and EU Organic certification requirements adds cost and operational complexity, particularly for small-scale farmers.

Market Opportunities

- Value-Added Processed Shrimp Products: Consumer demand for frozen peeled, cooked, breaded, marinated, and ready-to-cook shrimp formats is growing at above-market rates. In February 2022, SeaPak introduced its Southern Style Jumbo Shrimp nationwide in the U.S., while Beaver Street Fisheries launched its Sea Best Seafood Festival boil kit in November 2023, both reflecting the expanding value-added product opportunity.

- Sustainable Aquaculture Certification: Certified shrimp products command significant price premiums in European and North American retail markets. Growing retailer and food service commitments to sourcing certified sustainable seafood are creating sustained certification-driven demand differentiation for producers achieving ASC, BAP, or Global G.A.P. standards.

- Emerging Market Demand Expansion: Sub-Saharan Africa, the Middle East, and Eastern Europe represent underserved import markets with growing seafood demand. India, Vietnam, and Ecuador are well-positioned to supply these emerging markets, with competitive cost structures and expanding cold chain export infrastructure.

Market Challenges

- Feed Cost Volatility: Shrimp feed accounts for at least 40 of total farming costs. Volatility in fishmeal and soy-based ingredient prices, driven by climate impacts, El Niño, and commodity market disruptions – creates margin pressure particularly for small-scale and independent shrimp farmers.

- Cold Chain Infrastructure Gaps: Maintaining shrimp quality from harvest to consumer requires continuous refrigerated storage and logistics. Cold chain gaps in inland distribution markets of Asia, Africa, and Latin America limit market penetration and contribute to post-harvest losses estimated at 10–20% in some developing markets.

- Trade Policy and Import Tariff Risks: Anti-dumping duties, country-specific import bans, and trade policy shifts in the U.S. and EU can materially impact export economics for major producing nations. India and Ecuador have both faced U.S. anti-dumping investigations that created market uncertainty for exporters.

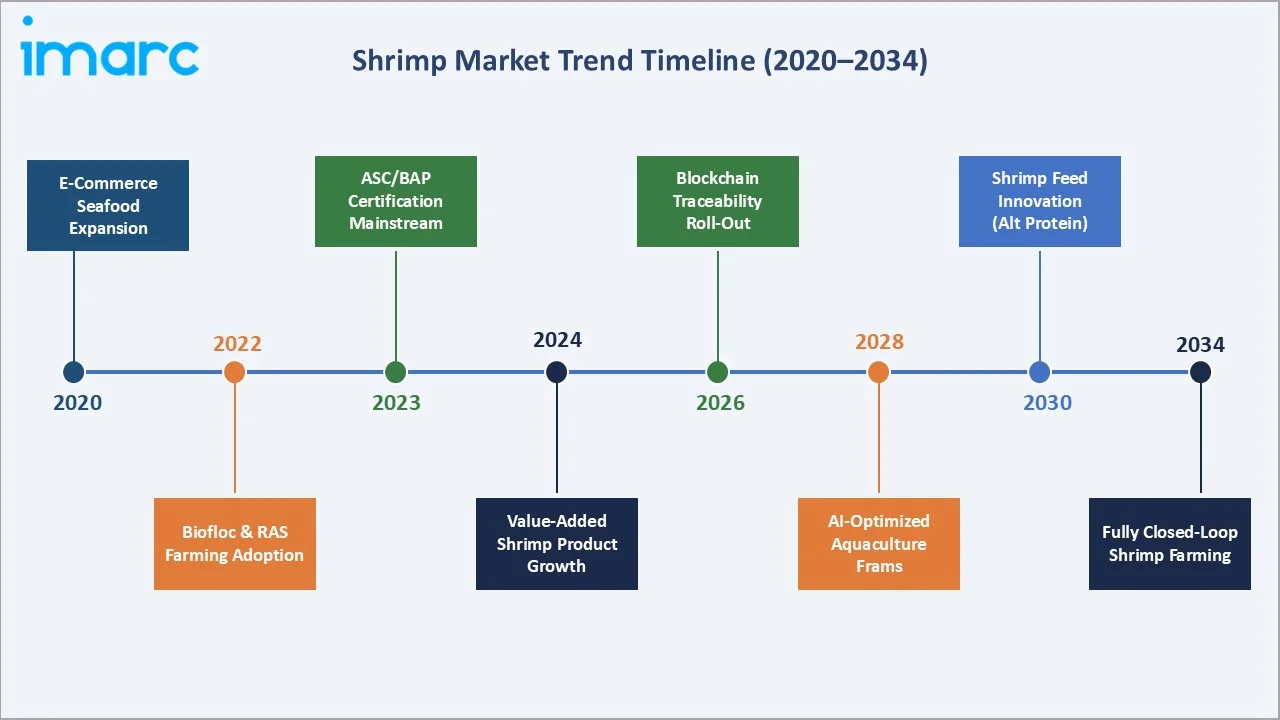

Emerging Market Trends

The global shrimp market is being reshaped by five converging trends that are redefining production methods, trade flows, product innovation, and competitive dynamics through 2034.

1. Sustainable Aquaculture Certification and Traceability

Retailer and food service procurement policies in Europe and North America are increasingly requiring ASC, BAP, GlobalG.A.P., or equivalent certification for shrimp sourcing. The Seafood Certifications and Ratings Collaboration measured that 15.7% of all farmed shrimp production is ASC, BAP, or Fair Trade certified in 2024. Blockchain-enabled traceability platforms are being deployed by Thai Union, Charoen Pokphand, and Walmart to provide end-to-end supply chain transparency from farm to fork.

2. Value-Added and Processed Shrimp Product Growth

The market for processed, frozen, breaded, cooked, and ready-to-cook shrimp products is growing faster than the commodity segment. Branded product launches, including marinated, seasoned, and cuisine-specific formats, are targeting premium retail consumers seeking convenient meal solutions. This trend is driving investment in processing facility capacity across India, Vietnam, and Ecuador to meet food service and retail specification requirements.

3. Biofloc and RAS Technology Adoption

Biofloc technology (BFT) and recirculating aquaculture systems (RAS) are enabling biosecure, high-density, and year-round shrimp production with significantly lower water usage and antibiotic application. RAS adoption is growing particularly in Europe and North America for domestic shrimp production, reducing import dependency and carbon footprint. BFT is gaining traction in India, Indonesia, and Vietnam as an intensive farming upgrade from traditional pond systems.

4. Ecuador's Rise as a Global Shrimp Supplier

Ecuador has emerged as one of the world's fastest-growing shrimp exporters with Ecuadorean shrimp exports rose 20% year-on-year in 2025 to $8.4 billion. Cost-competitive vannamei production, favorable climate conditions, and improving cold chain and processing infrastructure position Ecuador as the preferred supply source for China and Europe. Ecuador's shrimp exports grew significantly, establishing it as a dominant force in global shrimp trade.

5. Digital and E-commerce Seafood Distribution

Online seafood retail platforms, subscription-based delivery services, and direct-to-consumer seafood brands are growing at approximately 12–15% annually in developed markets. The pandemic-accelerated normalization of online grocery shopping has permanently expanded the digital seafood market. Premium branded shrimp products including wild-caught, sustainable-certified, and locally sourced varieties are capturing premium price points through DTC e-commerce channels across the U.S., EU, and China.

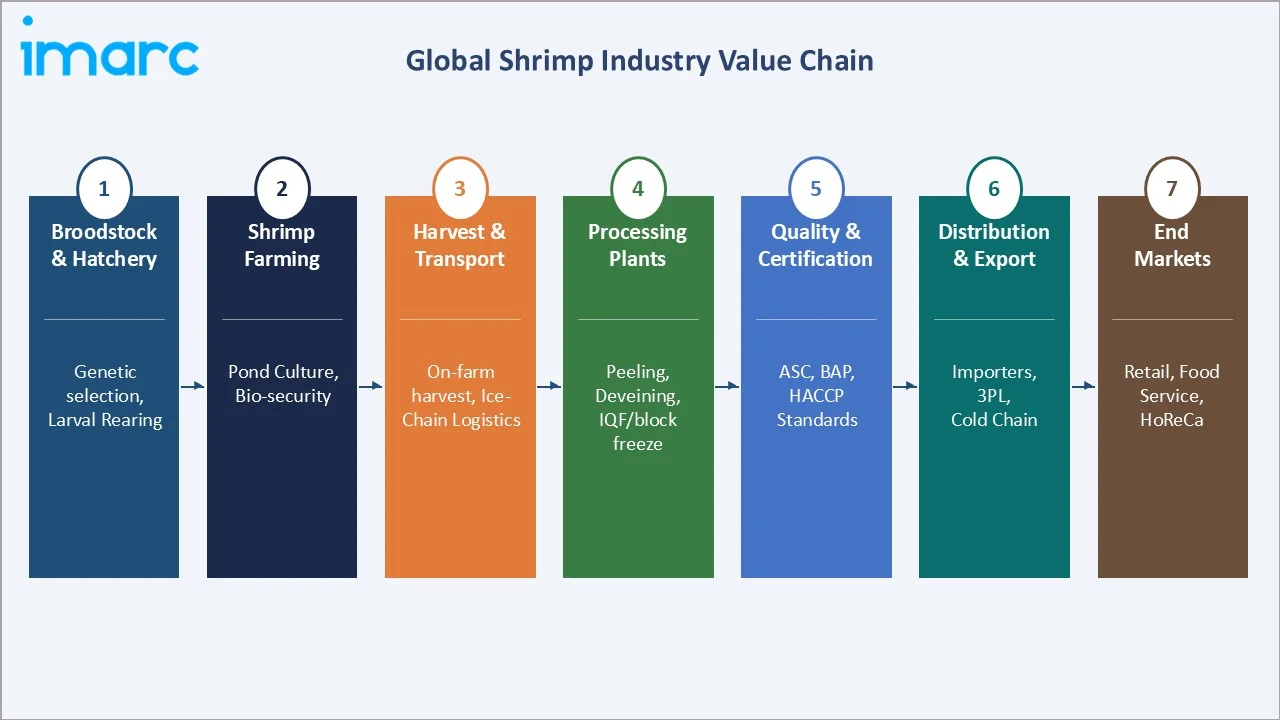

Industry Value Chain Analysis

The shrimp industry value chain spans seven interconnected stages from genetic broodstock selection to end-market consumption. Each stage requires specialized expertise, infrastructure investment, and quality management systems to ensure product safety, traceability, and commercial value retention.

|

Stage |

Key Activities |

Representative Players |

|

Broodstock & Hatchery |

Genetic selection, SPF broodstock maintenance, larval rearing to PL |

Shrimp Improvement Systems, Benchmark Genetics, INVE Aquaculture |

|

Shrimp Farming |

Pond preparation, stocking, feeding, biosecurity management, harvest |

CP Foods, Avanti Feeds, Waterbase Ltd., independent smallholders |

|

Harvest & Transport |

On-farm harvest, icing, transport to processing facilities |

Local collection agents, 3PL cold chain operators |

|

Processing Plants |

Peeling, deveining, head-off, IQF freezing, block freezing, value-added |

Thai Union, Surapon Foods, Devi Sea Foods, Integrated Aqua Farms |

|

Quality & Certification |

Residue testing, HACCP, ASC/BAP certification, traceability documentation |

SGS, Bureau Veritas, Control Union, Intertek |

|

Distribution & Export |

International shipping, cold storage, import clearance, domestic distribution |

Maersk, CMA CGM, domestic 3PL operators, seafood importers |

|

End Markets |

Retail supermarkets, food service/HoReCa, specialty seafood stores, e-commerce |

Walmart, Sysco, Carrefour, Amazon Fresh, restaurant chains |

The processing stage is a critical value creation point, where commodity shrimp is transformed into differentiated, specification-compliant, and branded products that command retail price premiums of 30–80% over farm-gate value. Cold chain integrity across the distribution stage is equally critical, shrimp quality deteriorates rapidly without continuous temperature control, making investment in refrigerated logistics infrastructure a key competitiveness determinant for producing nations.

Technology Landscape in the Shrimp Industry

Advanced Aquaculture Production Systems

Biofloc technology (BFT) has reduced shrimp farming's dependence on water exchange and external probiotics, enabling intensification while reducing disease risk. RAS technology is enabling indoor, climate-controlled shrimp farming in non-traditional geographies including the Netherlands, Germany, and the U.S., reducing supply chain carbon footprint and import dependency for key consumption markets.

Genetic Improvement and SPF Broodstock

Selective breeding programs for Penaeus vannamei focusing on growth rate, disease resistance, and feed conversion efficiency have dramatically improved farm economics over the past decade. SPF broodstock lines from suppliers including Shrimp Improvement Systems and Benchmark Genetics are now standard practice in intensive farming operations globally, reducing early mortality rates and improving harvest consistency.

Digital Farm Management and AI Monitoring

IoT-based pond monitoring systems tracking dissolved oxygen, pH, temperature, and feeding patterns are enabling real-time farm management optimization. AI-powered growth prediction models and automated feeding systems, deployed by companies including Eruvaka Technologies and XpertSea, are improving feed conversion ratios and reducing input costs. Blockchain platforms are providing immutable supply chain traceability from hatchery to retail shelf.

Processing Technology Innovation

High-speed automated peeling and deveining machines, IQF (Individual Quick Freezing) tunnel systems, and glazing technologies have dramatically improved processing throughput, quality consistency, and yield recovery. Value-added processing capabilities, including marinating, breading, cooking, and portion control, are enabling processors in India, Vietnam, and Ecuador to move up the value chain from commodity to branded product supply.

Market Segmentation Analysis

By Species

Penaeus Vannamei dominates the global shrimp market at 72.1% of total revenues in 2025, owing to its rapid growth rate (reaching harvest size in 90–120 days), high stocking density tolerance, and adaptability to a wide range of salinity and temperature conditions. Penaeus monodon (black tiger shrimp) at 12.5% commands premium pricing in Asian and European gourmet markets due to its larger size and distinctive flavor profile.

To access detailed market analysis, Request Sample

Penaeus Vannamei’s dominance reflects decades of selective breeding investment, feed technology development, and processing standardization that have made it the most economically efficient shrimp species for large-scale commercial production. The species accounts for over 80% of traded shrimp volumes in the U.S. retail market.

By Environment

Farmed shrimp dominates the global shrimp market, accounting for 61.5% of total production, driven by its scalability, consistent supply, and cost efficiency compared to wild catch. Aquaculture-led growth is supported by technological advancements, controlled farming practices, and increasing demand from large-scale retail and food service buyers who prioritize volume reliability and standardized quality. In contrast, wild shrimp, with a 38.5% share, occupies a more premium niche, valued for its natural sourcing and perceived superior taste, particularly in high-end food service and specialty retail segments.

The farmed shrimp segment continues to expand as sustainability initiatives, traceability standards, and certifications such as ASC and BAP gain traction, improving consumer confidence. Meanwhile, wild shrimp faces supply constraints due to regulatory limits and environmental pressures, reinforcing the structural shift toward aquaculture as the primary driver of global shrimp market growth.

Regional Market Insights

By Shrimp Producing Region

Six nations, China, India, Vietnam, Indonesia, and Ecuador, collectively account for 74% of global farmed shrimp production in 2025. Each represents distinct cost structures, species mixes, export market orientations, and sustainability compliance profiles.

China's 28.4% leadership (2025) reflects both massive domestic farm infrastructure and sophisticated processing and export operations. India's 18.6%, growing at approximately 6.5% CAGR, positions it as the market's fastest-growing major supplier, with Andhra Pradesh and Gujarat states serving as key production hubs. Ecuador's 7.4% share masks its exceptional growth trajectory; the country became China's top shrimp supplier in 2023 and has maintained that position through aggressive farm expansion and competitive pricing.

Competitive Landscape

The global shrimp market is moderately fragmented at the production level, with millions of small and medium-scale farmers supplying a relatively concentrated processing and trading tier. At the branded and processed product level, Thai Union Group PCL, Charoen Pokphand Foods, and Avanti Feeds hold dominant positions through integrated farm-to-market supply chain control.

|

Company Name |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Thai Union Group PCL |

Thai Union, Chicken of the Sea |

Global Leader – Processing & Export |

Sustainable aquaculture investment, brand building, digital traceability |

|

Charoen Pokphand Foods (CP Foods) |

CP Shrimp |

Leader – Integrated Aquaculture |

Vertical integration, biosecurity R&D, Asia Pacific dominance |

|

Avanti Feeds Limited |

Avanti Shrimp Feed |

Leader – India |

India shrimp feed dominance, integrated farming, export processing |

|

High Liner Foods |

High Liner, Fisher Boy |

Leader – North America |

Value-added product innovation, retail channel leadership, DTC expansion |

|

Clearwater Seafoods |

Clearwater |

Leader – Wild-Catch Premium |

Sustainable wild shrimp, premium positioning, European export |

|

Surapon Foods |

Surapon |

Established – Thailand |

Thailand shrimp processing, EU/USA export, quality compliance |

|

Waterbase Limited |

Waterbase Shrimp Feed |

Challenger – India |

Shrimp feed innovation, aquaculture services, RAS farm development |

|

Mazzetta Company |

Mazzetta, Harbor Banks |

Established – USA Import/Distribution |

U.S. seafood import-distribution, retail/food service supply |

|

Aqua Star |

Aqua Star |

Established – USA |

Frozen seafood distribution, private-label retail supply |

|

Nordic Seafood A/S |

Nordic Seafood |

Challenger – Europe |

European distribution, sustainable certification leadership |

Vertical integration, from feed production and broodstock supply through farming, processing, and branded distribution is the primary competitive moat for leading companies. Thai Union and Charoen Pokphand have invested billions in biosecure intensive farming infrastructure, reducing disease vulnerability and achieving cost-per-kilogram advantages over less-integrated competitors.

Key Company Profiles

Thai Union Group PCL

Thai Union Group is the world's largest seafood company and a leading global shrimp processor. The company operates across the full seafood value chain with significant shrimp processing capacity in Thailand and internationally.

- Product Portfolio: Frozen shrimp (IQF, block), cooked shrimp, breaded shrimp, value-added shrimp products, Chicken of the Sea branded shrimp (USA), King Oscar (Europe).

- Recent Developments: Thai Union Group PCL, announced a strategic partnership with Wholechain, the supply chain traceability and transparency technology leader, to enable the global deployment of standardized digital traceability across Thai Union's global seafood operations.

- Strategic Focus: Sustainable aquaculture sourcing, value-added product premiumization, digital traceability, global distribution network expansion, and branded seafood growth.

Charoen Pokphand Foods (CP Foods)

CP Foods is one of Southeast Asia's largest integrated agri-food companies, with a comprehensive shrimp business spanning broodstock genetics, feed production, contract farming, processing, and branded distribution across 30+ countries.

- Product Portfolio: CP Shrimp, frozen raw shrimp, cooked shrimp, breaded shrimp formats, aquaculture inputs (feed, health products, genetics).

- Recent Developments: Invested in advanced biosecurity systems including WSSV-resistant shrimp genetics; expanded RAS demonstration facilities in Thailand.

- Strategic Focus: Vertical integration leadership, biosecurity and genetic innovation, international market expansion, and sustainable aquaculture certification.

Avanti Feeds Limited

Avanti Feeds is India's largest shrimp feed producer and a significant integrated shrimp processor and exporter, holding a dominant position in the Indian aquaculture industry with revenues exceeding USD 600 Million annually.

- Product Portfolio: Avanti shrimp feed (starter, grower, finisher), frozen shrimp (IQF, block), value-added shrimp, Svein brand export products.

- Recent Developments: The company has expanded and commenced commercial operation in March 2024, at its new state-of-the-art facility at Krishnapatnam, with a capacity of 7,000 MT.

- Strategic Focus: Shrimp feed technology leadership, India export growth, processing capacity expansion, and sustainable aquaculture input innovation.

High Liner Foods

High Liner Foods is a leading North American seafood company specializing in value-added frozen seafood products, with a strong shrimp portfolio sold through retail and food service channels across the U.S. and Canada.

- Product Portfolio: High Liner breaded shrimp, cooked frozen shrimp, raw frozen shrimp, shrimp appetizers, Fisher Boy branded value products, private-label supply.

- Recent Developments: Expanded sustainable seafood sourcing commitments in 2024; launched new premium shrimp SKUs targeting health-conscious retail consumers.

- Strategic Focus: Value-added product innovation, North American retail and food service channel leadership, sustainable sourcing certification, and e-commerce channel development.

Clearwater Seafoods

Clearwater Seafoods is one of North America's largest wild-capture seafood companies, with a premium shrimp portfolio focused on cold-water, sustainably harvested species for the North American and European gourmet markets.

- Product Portfolio: Wild-caught cold-water shrimp, Greenland shrimp, Argentine red shrimp, premium frozen shrimp formats for retail and specialty food service.

- Recent Developments: Expanded MSC-certified wild shrimp offerings; developed direct e-commerce channel for premium consumer segments in 2023–2024.

- Strategic Focus: Wild-catch sustainability leadership, premium market positioning, European export expansion, and direct-to-consumer branded seafood growth.

Market Concentration Analysis

The global shrimp market is structurally bifurcated: production is highly fragmented among millions of small-scale and independent farmers, while the processing, branding, and export tier is more concentrated. The top five processing and distribution companies, Thai Union, CP Foods, Avanti Feeds, High Liner, and Clearwater, collectively account for approximately 20–25% of global processed shrimp trade value in 2025.

At the producing-nation level, the top six countries (China, India, Vietnam, Indonesia, Ecuador) control 74% of global farmed shrimp supply, creating a geographically concentrated supply base with significant exposure to single-country biosecurity events, trade policy disruptions, and climate risks. This concentration has driven major importers in the U.S. and EU to actively pursue supply diversification strategies, benefiting India, Ecuador, and Indonesia as alternative sourcing markets.

Consolidation trends at the processing and branded product tier are accelerating, with private equity investment in aquaculture technology companies, vertical integration M&A among regional processors, and major retailer private-label seafood program expansions. The market is expected to see 8–12 significant M&A or strategic partnership transactions annually through 2034, as global seafood companies seek to combine sustainable sourcing credentials with processing efficiency and branded market access.

Investment & Growth Opportunities

Fastest Growing Segments

Value-added processed shrimp (CAGR approximately 6–7%), certified sustainable and organic shrimp (CAGR approximately 8%), and online/DTC seafood distribution (CAGR approximately 12–15%) represent the highest-growth investment vectors through 2034. These segments collectively address a total addressable market exceeding USD 25 Billion by 2034.

Emerging Producer Nation Opportunities

India's shrimp export sector is growing at approximately 6.5% CAGR, supported by government aquaculture expansion programs, improving processing infrastructure, and competitive labor costs. Ecuador presents significant investment opportunity in biofloc intensification, cold chain logistics, and value-added processing capability. Vietnam and Indonesia offer opportunities in RAS technology adoption, biosecurity improvement, and sustainability certification programs targeting EU and Japanese market requirements.

Technology and Innovation Investment Trends

- Aquaculture technology companies including Eruvaka Technologies (AI pond monitoring) and XpertSea (biosecurity AI) are attracting significant VC and corporate venture investment as biosecurity and feed efficiency become primary competitive differentiators.

- Alternative shrimp feed ingredients including insect meal (black soldier fly), single-cell proteins, and algae are receiving investment from major shrimp feed producers seeking to reduce fishmeal dependence and improve sustainability credentials.

- Blockchain and digital traceability platforms are being mandated by major retail and food service buyers, creating B2B software investment opportunities across the shrimp supply chain from farm to fork.

- Indoor RAS shrimp farming ventures in the EU and USA are attracting investment from impact funds, sovereign wealth vehicles, and agri-food corporations seeking to localize premium seafood supply and reduce carbon-intensive international cold-chain trade.

Future Market Outlook (2026-2034)

The global shrimp market is poised for steady, resilience-backed growth through 2034, anchored by demographic demand expansion, aquaculture productivity improvement, and geographic diversification of both supply and consumption.

Technological disruption will be the primary driver of competitive dynamics over the next decade. Producers achieving farm-level biosecurity through SPF genetics and RAS intensification, combined with processing-level automation and value-added product capabilities, will command the most durable competitive positions. The shift toward digital supply chain traceability, mandated by both regulatory frameworks and major buyer procurement policies, will create a two-tier market of compliant, premium-priced certified product versus undifferentiated commodity shrimp.

By 2034, the farmed shrimp segment is expected to represent approximately 80% of total market value, as aquaculture productivity gains continue to outpace wild-capture supply growth. The adult protein demand surge in Sub-Saharan Africa, the Middle East, and South Asia will create new import market opportunities for Asian and Latin American producers, while domestic consumption growth in China and India will absorb an increasing share of regional production. Companies that invest now in sustainable certification, value-added processing, and digital distribution infrastructure will be best positioned to capture the next decade of market value.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 160 industry participants in 2024–2025, comprising shrimp farm operators, processing plant managers, seafood import-export traders, retail buyers, food service procurement managers, aquaculture technology companies, and regulatory officials across China, India, Vietnam, Thailand, Ecuador, the U.S., and EU.

Secondary Research

Secondary research encompassed a comprehensive review of FAO Global Fisheries and Aquaculture data, company annual reports, trade publications (Seafood Source, Undercurrent News, IntraFish), government aquaculture ministry statistics, USDA ERS seafood trade data, and industry databases including Euromonitor and IHS Markit. Over 300 primary statistical sources were triangulated for market size validation.

Forecasting Models

Market size estimations and growth projections were derived using bottom-up aquaculture production volume modeling combined with top-down trade value analysis, incorporating species-specific production cost curves, exchange rate assumptions, aquaculture yield improvement trajectories, and consumer demand elasticity data. Scenario analysis across base, optimistic, and conservative cases was performed to account for biosecurity event risk and macroeconomic uncertainty.

Shrimp Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Environments Covered | Farmed Shrimp, Wild Shrimp |

| Species Covered | Penaeus Vannamei, Penaeus Monodon, Macrobrachium Rosenbergii, Others |

| Shrimp Sizes Covered | <21, 21-25, 26-30, 31-40, 41-50, 51-60, 61-70, >70 |

| Distribution Channels Covered | Hypermarkets and Supermarkets, Convenience Stores, Hotels and Restaurants, Online Sales, Others |

| Regions Covered |

|

| Companies Covered | Thai Union Group PCL, Charoen Pokphand Foods (CP Foods), Avanti Feeds Limited, High Liner Foods, Clearwater Seafoods, Surapon Foods, Waterbase Limited, Mazzetta Company, Aqua Star, Nordic Seafood A/S |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the shrimp market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global shrimp market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the shrimp industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Global Shrimp Market Report

The global shrimp market was valued at USD 74.7 Billion in 2025 and is projected to reach USD 106.1 Billion by 2034.

The market is forecast to grow at a CAGR of 3.80% during 2026-2034, driven by rising seafood consumption, aquaculture technology advances, and expanding emerging market demand.

Penaeus vannamei (whiteleg shrimp) dominates with a 72.1% share in 2025, owing to its high yield, rapid growth cycle, intensive farming adaptability, and broad global market acceptance.

Farmed shrimp accounts for 61.5% of global shrimp market revenues in 2025, reflecting the structural shift to aquaculture-based production driven by cost efficiency, supply consistency, and technology improvement.

China is the largest shrimp producing nation with a 28.4% share in 2025, followed by India (18.6%), Vietnam (16.2%), and Indonesia (14.3%).

Key drivers include rising global seafood and protein demand, aquaculture technology advances, expanding middle-class consumption in Asia and Latin America, e-commerce seafood distribution growth, and food service sector expansion.

Key trends include sustainable aquaculture certification, value-added processed shrimp product growth, biofloc and RAS technology adoption, Ecuador's emergence as a global supplier, and digital e-commerce seafood distribution expansion.

Leading companies include Thai Union Group PCL, Charoen Pokphand Foods (CP Foods), Avanti Feeds Limited, High Liner Foods, Clearwater Seafoods, Surapon Foods, Waterbase Limited, Mazzetta Company, Aqua Star, Nordic Seafood A/S, etc.

The global shrimp market is projected to reach USD 90.01 Billion by 2030, reflecting steady compound growth from the 2025base of USD 74.7 Billion.

Online retail is the fastest-growing distribution channel at approximately 12–15% CAGR, driven by subscription seafood services, DTC branded shrimp products, and expanded grocery e-commerce platforms in the U.S., EU, and China.

High-growth opportunities exist in value-added processing, sustainable certification programs, aquaculture technology (RAS, biofloc, AI monitoring), emerging market expansion (India, Ecuador, Africa), and digital traceability platforms.

Key challenges include shrimp disease outbreaks (EMS, WSSV), antibiotic residue regulatory compliance, environmental sustainability pressures, feed cost volatility, cold chain infrastructure gaps in developing markets, and trade policy/anti-dumping risks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)