Polyols Market Size, Share, Trends and Forecast by Type, Application, Industry, and Region, 2025-2033

Polyols Market Size and Share:

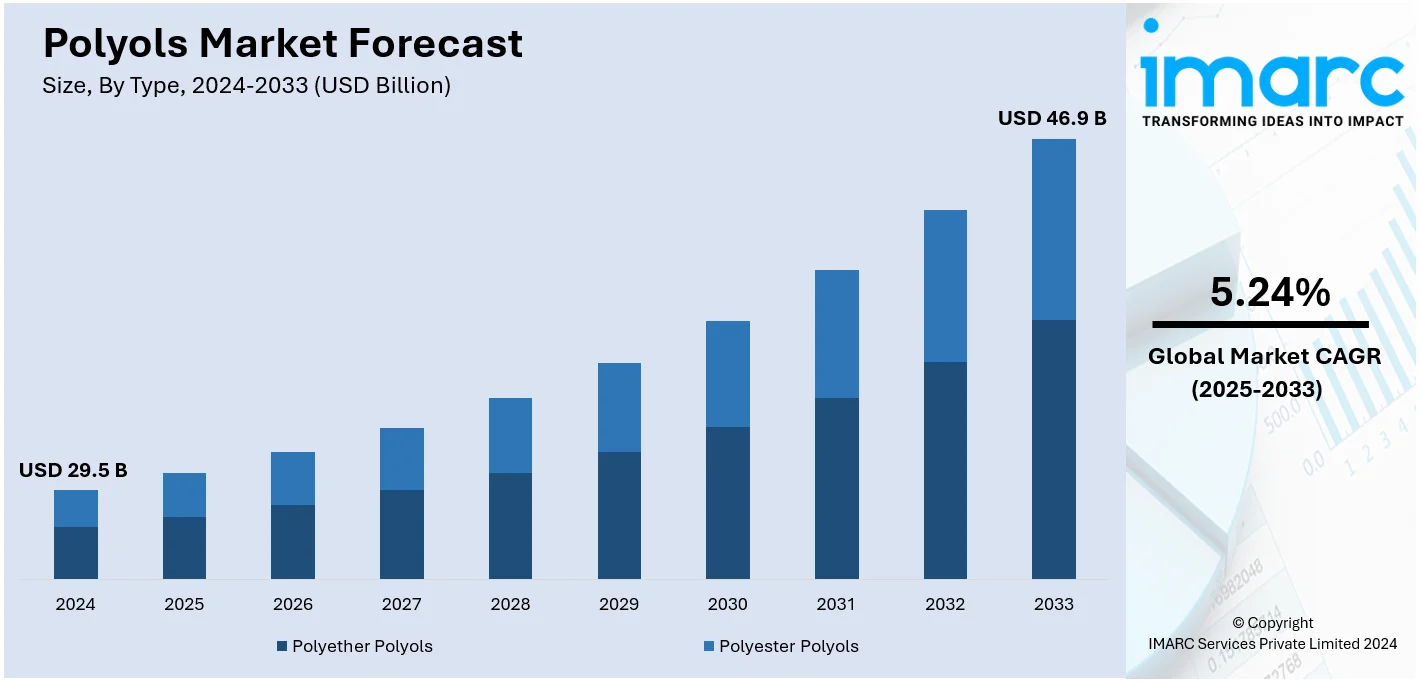

The global polyols market size was valued at USD 29.5 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 46.9 Billion by 2033, exhibiting a CAGR of 5.24% during 2025-2033. Asia-Pacific currently dominates the market, holding a significant market share of over 44.3% in 2024. A key factor driving the regional market is the growing demand for energy-efficient building materials, especially within the construction sector.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 29.5 Billion |

|

Market Forecast in 2033

|

USD 46.9 Billion |

| Market Growth Rate (2025-2033) | 5.24% |

One of the major drivers of the polyols market is the rising demand for energy-efficient building materials, particularly in the construction sector. Polyols, as key components in polyurethane insulation foams, play a crucial role in enhancing thermal insulation, reducing energy consumption, and supporting sustainable construction practices. The increasing focus on green building certifications and energy-saving standards enhances the uptake of polyols-based solutions. Additionally, the growing trend toward urbanization and infrastructural development worldwide creates significant demand for advanced insulating materials, solidifying polyols as indispensable in meeting modern construction and environmental efficiency requirements. For instance, in 2024, Dow, a leading polyols supplier, sold its flexible packaging laminating adhesives business, including five manufacturing sites, to Arkema for $150 million, encompassing solvent-based, solventless adhesives, and heat seal coatings.

The United States is a key market for polyols, and the market is influenced by the strong chemical manufacturing base in the country, innovation, and the increasing desire for sustainability. U.S.-based companies are major players in the development of conventional and bio-based polyols to meet the fast-growing demand for sustainable products across various industries. Its strong R&D capabilities ensure high-performance polyols for diverse applications in the construction, automotive, and furniture sectors. In addition, a strong focus on environmental compliance has positioned the U.S. as an eco-friendly hub for producing polyols. For instance, in 2024, JLR, Dow MobilityScience, and Adient achieved a breakthrough by recycling polyurethane seat foam into new car seats, reducing CO2 emissions by 44kg per seat, and cutting emissions by half. Strategic exportation and a well-established domestic supply chain add much to the contribution of U.S. to the polyols market in the globe.

Polyols Market Trends:

Rising demand for bio-based polyols

At present, there is a focus on the production of bio-based polyols to reduce the carbon footprint and occurrence of pollution. According to the 2024 global carbon budget, CO2 emissions from fossil fuel use are expected to increase by 0.8% in 2024, reaching a record 37.4GtCO2. This marks an increase of 0.4GtCO2 over the previous record set last year. Bio-based polyols are sourced from plant oils, such as rapeseed oil. They are also manufactured by following a special process where a reduction of all carboxyl groups creates primary and particularly high-quality polyols. They are often manufactured using renewable resource technologies, helping to eliminate unwanted odors and address the demands of various industries by providing excellent performance and high levels of renewable content. In addition, governing agencies of various countries are enacting stringent regulations to help promote the adoption of renewable resources and reduce the environmental impact of industrial processes. They are also giving incentives in the form of tax credits, grants, and subsidies to the business houses using bio-based polyols. Besides, it is a highly sustainable and environmental-friendly product, which is boosting demand for bio-based polyols. Bio-based polyols possess similar or even superior performance properties than their petroleum-based counterparts. They can be formulated to meet specific requirements, providing a wide range of functionalities suitable for various applications such as polyurethane foams, coatings, adhesives, and elastomers.

Increasing utilization in the packaging industry

The growing concern for environment and regulatory pressure is a driving factor for polyols growth as demand is increasing day by day. As per McKinsey, 60% to 70% of consumers expressed a readiness to pay more for sustainable packaging. Polyols find a wide usage in polyurethane foam and coating, which can be extremely flexible, long-lasting and moisture-resistant. In addition, polyols-based packaging materials improve the shelf life of many perishable products by providing better protection in storage and transportation. Polyurethane foams and coatings allow for good cushioning shock absorption properties preventing damaged items during handling and shipping. It is also possible for materials based on polyols to provide insulation against temperature shifts, helping ensure the freshness and quality of food and pharmaceutical products. The increasing demand for convenient and sustainable packaging solutions is driving the interest of the packaging industry toward polyols-based materials to fulfill these requirements while ensuring the integrity and safety of products.

Development of advanced polyurethanes

Advanced polyurethanes are manufactured to offer superior performance properties. They comprise innovative formulations and can be tailored according to the requirements of industries. They have a high load capacity in both compression and tension. Advanced polyurethanes may undergo a change in shape under a heavy weight but can immediately return to their original shape after the load is removed with minimum compression set in the material. They can also function effectively when used in high-flex applications and possess high tear resistance along with efficient tensile properties. Additionally, advancements in manufacturing processes enable the production of polyurethanes with reduced emissions, lower energy consumption, and improved resource efficiency. For instance, in 2024, BASF has partnered with STOCKMEIER Urethanes USA, Inc. to produce Stobielast S polyurethane binders for playground surfacing, utilizing 100% domestically produced Biomass Balance (BMB) Lupranate MDI. These eco-friendly attributes make advanced polyurethanes attractive to industries and people seeking sustainable solutions. Advanced polyurethanes are increasingly getting incorporated with functionalities, such as self-healing, shape memory, antimicrobial activity, and sensing capabilities, to expand their application potential using diverse fields, including healthcare electronics and textiles.

Polyols Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global polyols market, along with forecasts at the global and regional levels from 2025-2033. The market has been categorized based on type, application, and industry.

Analysis by Type:

- Polyether Polyols

- Polyester Polyols

Polyether polyols stand as the largest type in 2024, holding around 27.9% of the market. Polyether polyols hold the biggest polyols market share. They are a kind of synthetic oil and are made from ethylene oxide, epoxy propane, epoxy butane, and various other raw materials. They are manufactured by the process of open ring homopolymerisation or copolymerization under the function of a catalyst. They are widely used for the preparation of synthetic detergents with low foaming features. They also have low toxicity and are often employed as drug excipients and emulsifiers, which are often used in oral and nasal sprays and shampoos. They can be used as demulsifiers for crude oil to prevent the formation of hard scales in oil pipelines. Moreover, polyether polyols are utilized as a papermaking additive and bleaching agent to improve the quality of various coated papers. Polyester polyols are the derivatives of dicarboxylic acids and polyols. They are primarily synthesized from petroleum but can also be manufactured from various types of plant-based oils. Their viscosity generally increases with their molecular weights, and they can impart various properties, including water resistance, abrasion resistance, and cut resistance.

Analysis by Application:

- Flexible Polyurethane Foams

- Rigid Polyurethane Foams

- CASE (Coatings, Adhesives, Sealants & Elastomers)

- Others

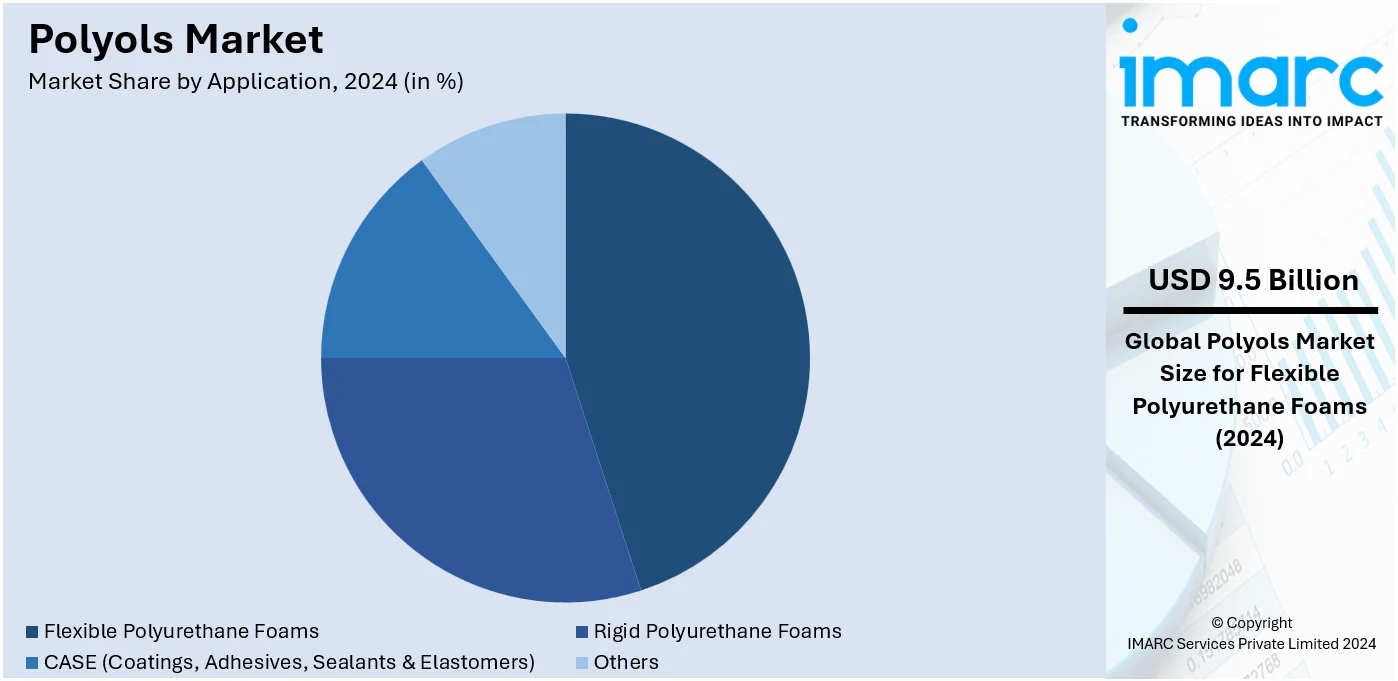

Flexible polyurethane foams lead the market with around 32.2% of the market share in 2024. Flexible polyurethane foams are the most prominent segment due to their versatility in mattress, pillow, furniture cushion, and car seat manufacturing. These foams are soft and resilient and can be molded to conform to the shape of the body to distribute weight and ease pressure points. Flexible polyurethane foams also show endurance and resilience to repeated compression, thereby ensuring long-term performance. Due to their excellent comfort, support, and durability properties, flexible polyurethane foams remain a number one favorite for manufacturers and consumers across diverse industries.

Analysis by Industry:

- Carpet Backing

- Packaging

- Furniture

- Automotive

- Building & Construction

- Electronics

- Footwear

- Others

Packaging leads the market in 2024. Packaging represents the biggest market share owing to the rising utilization of polyols for making flexible packaging solutions. Polyols improve the adhesion properties in packaging materials, making them less prone to cracking or breaking during transportation and handling. They are also compatible with various materials like plastic, silicone, paper, and metals. This versatility allows them to be incorporated into different types of packaging solutions. Polyols have hygroscopic properties, meaning they can absorb and retain moisture. This property is valuable in packaging applications where moisture control is crucial, such as pharmaceuticals, food, and electronic components. By keeping products dry, polyols help maintain their quality and shelf life.

Regional Analysis:

- North America

- Asia Pacific

- Europe

- Latin America

- Middle East and Africa

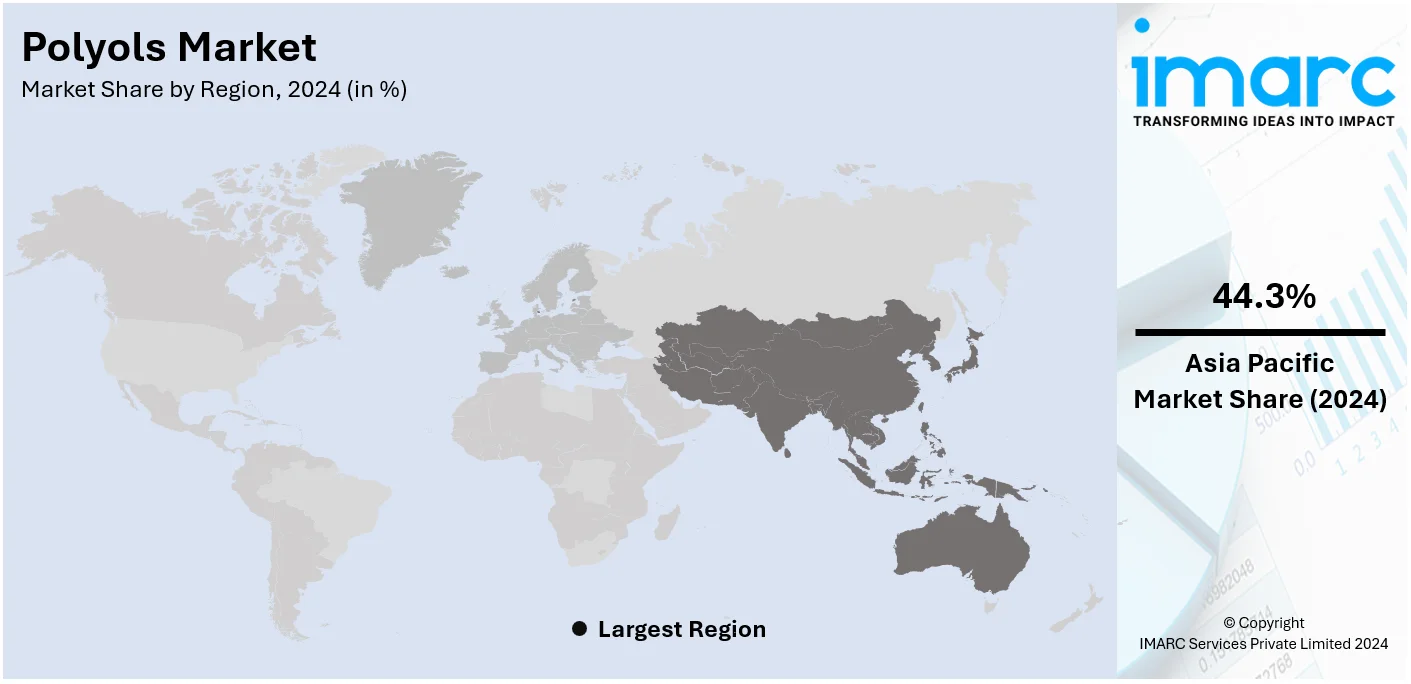

In 2024, Asia-Pacific accounted for the largest market share of over 44.3%. The Asia Pacific polyols market is being driven by the growing adoption of flexible packaging solutions across various industry sectors. The region is witnessing a rise in partnerships and collaborations between automakers and polyol and polyurethane foam manufacturers, fostering innovation and local production of customized and ergonomic car seats. Stringent emissions regulations in China and other countries are encouraging the production of bio-based polyols. Moreover, the construction industry in Asia Pacific is a major consumer of polyols, utilizing them in the production of insulation materials and adhesives. The growing population and urbanization in countries like India and China are driving the demand for sustainable construction materials, thereby propelling the growth of the polyols market in the region. Additionally, the rising disposable income levels in emerging economies are fueling the demand for consumer goods, such as furniture and electronics, further boosting the market for polyols. With favorable government policies and increasing investments in research and development, the Asia Pacific polyols market is expected to continue its growth trajectory in the coming years. In conclusion, the region's diverse industrial landscape and focus on sustainable solutions make it a key player in the global polyols market.

Key Regional Takeaways:

United States Polyols Market Analysis

US accounts for 83.8% of the market share in North America. The increasing demand for polyols, particularly sorbitol, xylitol, and erythritol, is being driven by health-conscious consumers residing across the United States who are seeking lower-calorie alternatives in the food and beverage industry. These polyols are gaining popularity as they are helping in weight management and blood sugar control. According to the International Diabetes Federation (IDF), in 2021, 237,306,100 adults were affected with diabetes across the region. Moreover, the prevalence rate of diabetes among adults were 13.6%. In line with this, polyols, particularly glycerin, act as humectants, helping to bind water within the skin, thereby promoting hydration. Therefore, this is used in several types of skin care products across the United States. Additionally, polyols are essential in the production of polyurethanes across the region, which are used in the automotive industry. According to the International Trade Administration (ITA), in 2020, the United States recorded light vehicle sales totaling 14.5 Million units.

North America Polyols Market Analysis

The steady growth of the North America polyols market is observed in such growing demands by the construction, automobile, and furniture industries. Polyols are important parts in polyurethane manufacturing, used in a vast array of applications that range from flexible and rigid foams to coatings, adhesives, and sealants. The construction industry growth has supported rigid polyurethane foam due to its insulating properties. On the other hand, flexible foam is used more by the automotive industry to develop light, energy-efficient vehicles. For example, as per industry reports, the U.S. biomass technology roadmap outlines a goal to replace 25% of petroleum-based organic compounds with biobased alternatives by 2030, which will include renewable and degradable vegetable oil-based polyols for polyurethane foam production. The increasing interest in sustainable solutions is driving the adoption of bio-based polyols, which aligns with regulatory and consumer preferences for eco-friendly materials. Major players focus on innovation and capacity expansion. With robust industrial activity and advancements in polyurethane technologies, the North America polyols market is positioned for sustained expansion.

Asia Pacific Polyols Market Analysis

The rising middle class and health-conscious consumers are significantly driving the demand for sugar-free and low-calorie products across the region, increasing the use of polyols like sorbitol and xylitol in the food and beverage industry. According to the India Brand Equity Foundation (IBEF), wealthy households of India are earning over ₹2 crore (around USD 242,709) per year. This increased from USD 1.06 Million in 2016 to 1.8 Million in 2021.In line with this, the increasing use of polyols as excipients in drug formulations is addressing the growing healthcare needs of the large and expanding population in the Asia-Pacific region. According to the India Brand Equity Foundation (IBEF), the Indian pharmaceutical industry is currently experiencing a compound annual growth rate (CAGR) of 6-8% from FY18 to FY23, driven by an ongoing 8% increase in exports and a 6% rise in the domestic market.

Europe Polyols Market Analysis

The increasing use of polyols in the manufacturing of polyurethane foams across the European region is driving their application in the automotive sector for seating, insulation, and soundproofing materials. According to the Office for National Statistics, in 2018, motor vehicle manufacturing firms in the United Kingdom directly employed over 169,000 individuals, accounting for 0.5% of the total workforce. In addition to this, the construction industry is increasingly using polyurethane-based insulation materials, derived from polyols, for thermal insulation. According to the European Commission, the construction sector generates approximately 18 Million direct jobs and accounts for around 9% of the European Union's GDP. Furthermore, the rising demand for diabetic-friendly and low-sugar food options are stimulating the increasing use of polyols as sugar alcohols in sugar-free and low-calorie products. In line with this, polyols are being incorporated into drug formulations, especially as excipients, stabilizers, and sweeteners in products like syrups and chewable tablets.

Latin America Polyols Market Analysis

Polyols, particularly glycerin, are being used in cosmetics, especially in moisturizers, shampoos, and conditioners, due to their moisturizing properties. In addition to this, consumer awareness of health and wellness is increasing, stimulating the rising demand for low-calorie sweeteners and sugar substitutes, particularly sorbitol and mannitol, across the Latin American region. According to the International Diabetes Federation (IDF), in 2021, 149,916,800 adults were affected with diabetes across Brazil. In line with this, the prevalence rate of diabetes among adults were 10.5%.

Middle East and Africa Polyols Market Analysis

The demand for low-calorie and low-sugar foods is driving the use of polyols like sorbitol and mannitol in sugar-free and diabetic-friendly food products, particularly in the Middle East. According to the International Diabetes Federation (IDF), in 2021, 8,057,100 adults were affected with diabetes across the United Arab Emirates. In line with this, the prevalence rate of diabetes among adults were 12.3%. Additionally, according to the International Diabetes Federation (IDF), in 2021, 24,194,300 adults were affected with diabetes across Saudi Arabia.

Competitive Landscape:

The polyols market has shown a competitive landscape with huge international giants and emerging regional manufacturing firms. Industry leaders tend to upgrade their production volumes, move towards bio-based polyol production, and widen the variety of products according to developing sustainability demands. Strategic collaborations, mergers, and acquisitions take place in frequent sequences which help to acquire improved and stronger market positions and enhance global reach in terms of market. Technological change in producing processes and innovative product intensifies competition. Key players are also prioritizing investments in R&D to create high-performance polyols tailored for specific applications. This competitive environment fosters continual innovation and positions the market for sustainable growth in a wide array of industries. For instance, in 2024, BASF partnered with Carlisle Construction Materials to produce MDI-based polyiso boards and polyurethane foam using Lupranate ZERO, the first zero-carbon-footprint isocyanate, revolutionizing sustainable building insulation.

The report provides a comprehensive analysis of the competitive landscape in the polyols market with detailed profiles of all major companies, including:

- BASF SE

- Royal Dutch Shell Plc

- Mitsui Chemicals

- Covestro AG

- The Dow Chemical Company

- Wanhua Chemical Group

- Huntsman Corporation

- LANXESS AG

- Stepan Company

- Repsol SA

Latest News and Developments:

- December 2024: Dow announced the production of VORANOL™ WK5750, an advanced polyether polyol, at its Freeport polyol plant, further demonstrating its continued dedication to providing high-performance applications.

- August 2024: MA Silva launched the Neo Select stopper, an eco-friendly cork made using plant-based polyol. This innovative stopper combines ecological benefits with the feel of natural cork, ensuring quality wine preservation.

- May 2024: MOL launched a polyol facility in Tiszaújváros, Hungary, worth €1.3 billion, with a yearly output of 200,000 tonnes. The facility, representing MOL's biggest organic investment, will manufacture polyol, an essential raw material for plastics, using advanced, environment-friendly techniques. This facility is projected to produce €150 million each year and offer stable jobs for approximately 300 individuals.

- April 2024: Chimcomplex SA Borzesti completed a project to produce eco-friendly polyols at its Rm. Valcea plant. The EUR 2.4 million investment, partially funded by Innovation Norway, substitutes petrochemical elements with natural oils such as castor and soybean oil.

- April 2024: Sanyo Chemical and Econic Technologies have entered into an MOU to investigate CO2-derived polyols for eco-friendly polyurethane manufacturing. This collaboration aims to reduce carbon footprints by integrating CO2 into polyol structures, advancing carbon neutrality. The technology could lower production costs while enhancing sustainability in various industries.

- January 2024: Aether Industries, H.B. Fuller, and Saudi Aramco Technologies announced the commercialization of Converge polyols, a sustainable technology using up to 40% CO2. This innovation aims to reduce carbon emissions and cater to the CASE industry, with a market potential of 850,000 MT annually. The collaboration highlights advancements in eco-friendly polyol applications.

- March 2023: BASF started manufacturing its first biobased polyol, Sovermol®, at its plant in Mangalore, India. Additionally, this product is designed to address the growing need for environmentally friendly options in multiple applications, such as New Energy Vehicles (NEV), wind turbines, flooring, and industrial protective coatings in the Asia Pacific area.

- April 2023: Aether Industries has joined forces with Saudi Aramco Technologies to bring their Converge polyols technology to market, emphasizing the creation of sustainable polyols that contain as much as 40% carbon dioxide by weight. This advancement is anticipated to greatly lessen the carbon footprint in relation to conventional polyols utilized in the CASE (Coatings, Adhesives, Sealants, and Elastomers) sector.

- September 2022: Covestro has launched eco-friendly polyether polyols made from bio-circular resources, along with renewable isocyanates, greatly decreasing the carbon footprint relative to fossil fuels.

Polyols Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Polyether Polyols, Polyester Polyols |

| Applications Covered | Flexible Polyurethane Foams, Rigid Polyurethane Foams, CASE (Coatings, Adhesives, Sealants & Elastomers), Others |

| Industries Covered | Carpet Backing, Packaging, Furniture, Automotive, Building & Construction, Electronics, Footwear, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | BASF SE, Royal Dutch Shell Plc, Mitsui Chemicals, Covestro AG, The Dow Chemical Company, Wanhua Chemical Group, Huntsman Corporation, LANXESS AG, Stepan Company, Repsol SA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the polyols market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global polyols market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the polyols industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

Polyols are sugar alcohols that are commonly used as sugar substitutes in a variety of foods and beverages. They have fewer calories than traditional sugars and do not raise blood sugar levels as much, making them popular among those with diabetes or those looking to reduce their sugar intake.

The polyols market was valued at USD 31.0 Billion in 2025.

IMARC estimates the global polyols market to exhibit a CAGR of 5.24% during 2025-2033.

The key factors driving the global polyols market include increasing demand for polyurethane-based products in the construction and automotive industries, rising consumer preferences for eco-friendly and energy-efficient products, and growing awareness about the benefits of using polyols in various applications. Additionally, technological advancements in manufacturing processes are also contributing to market growth.

According to the report, polyether polyols represented the largest segment by type, driven by their wide range of applications in industries such as automotive, construction, and furniture manufacturing.

Flexible polyurethane leads the market by application as it is a versatile material that can be used in a wide range of industries and applications, including automotive, furniture, construction, and insulation.

Packaging leads the market by industry as it is essential for preserving the quality and shelf life of polyol products.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein Asia Pacific currently dominates the global market.

Some of the major players in the global polyols market include BASF SE, Royal Dutch Shell Plc, Mitsui Chemicals, Covestro AG, The Dow Chemical Company, Wanhua Chemical Group, Huntsman Corporation, LANXESS AG, Stepan Company, Repsol SA, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)