Pine Chemicals Market Size, Share, Trends and Forecast by Product Type, Source, Application, and Region, 2026-2034

Pine Chemicals Market Size and Share:

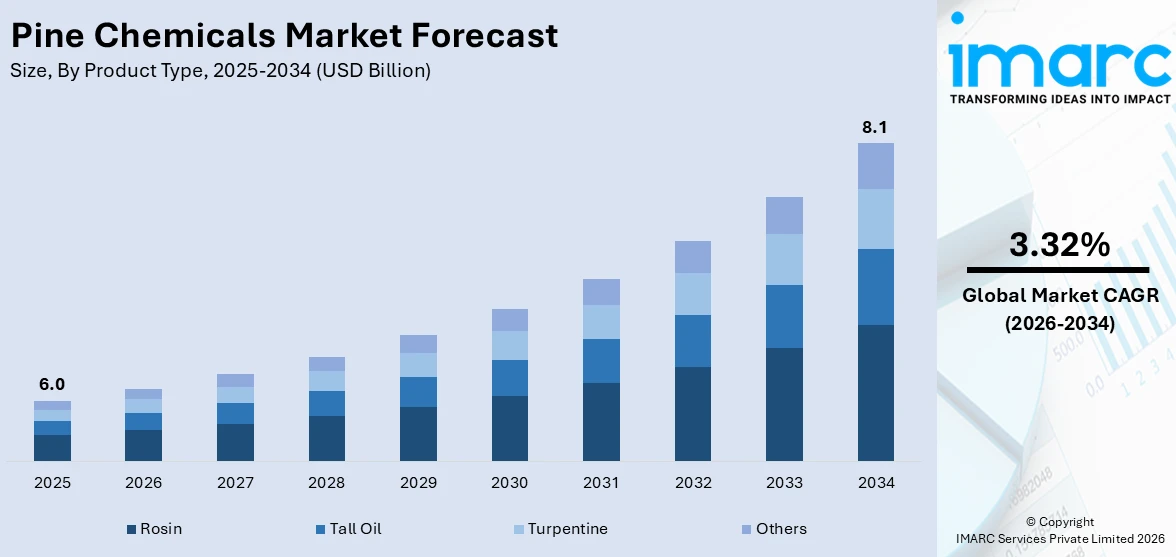

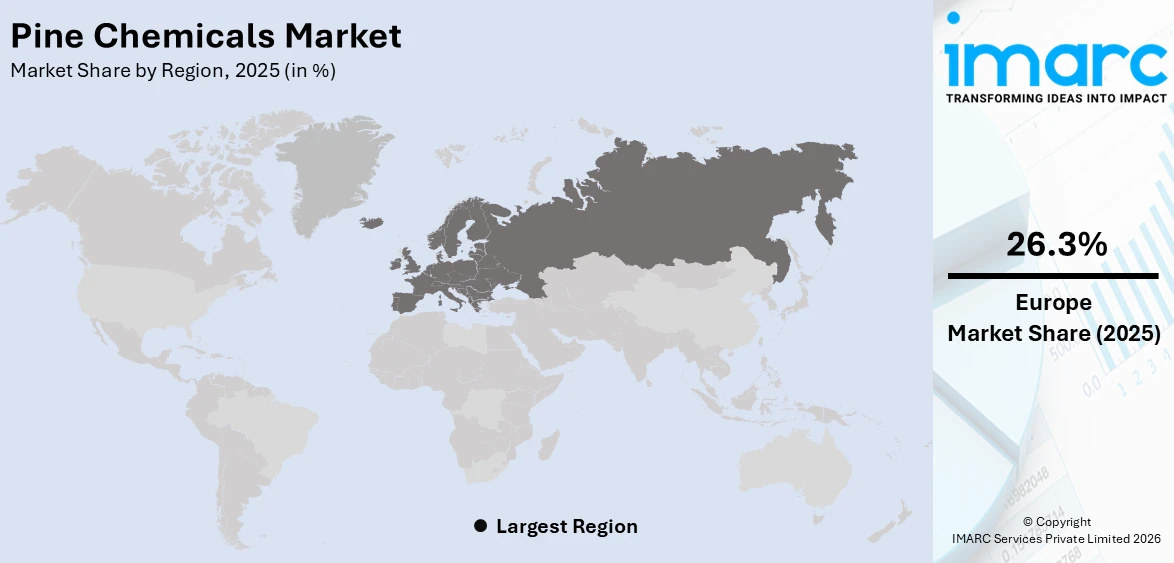

The pine chemicals market size was valued at USD 6.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 8.1 Billion by 2034, exhibiting a CAGR of 3.32% from 2026-2034. Europe currently dominates the market, holding a market share of over 26.3% in 2025.The market is growing as demand for bio-based chemicals rises, driven by advancements in extraction technologies and increased adoption across adhesives, coatings, personal care, and sustainable industrial applications, supported by a shift towards eco-friendly and renewable alternatives to petrochemical-based products.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 6.0 Billion |

|

Market Forecast in 2034

|

USD 8.1 Billion |

| Market Growth Rate (2026-2034) | 3.32% |

The growing need for bio-based and sustainable chemicals across a range of industries is propelling the worldwide pine chemicals market's notable expansion. Pine chemicals, derived from renewable sources like pine trees, serve as key raw materials in adhesives, coatings, flavors, and fragrances. The rising environmental concerns and stringent regulations restricting petrochemical usage have accelerated the adoption of bio-based alternatives, thereby boosting demand for pine chemicals. For example, In April 2024, Linxingpinechem launched innovative pine chemical products, including gum rosin, turpentine, and fragrance compounds, leading the industry with its commitment to quality and customer-centric solutions in various sectors. Additionally, advances in extraction technologies with improved efficiency in the production of chemicals from pine has enhanced cost-effectiveness and competitiveness of these products to use industrially. Rising demand by various sector, such as construction, automotive, and personal care, along with an ever-growing concern for environmental friendly solutions, further accelerated the market. Strong supply chain, especially in the regions with an abundant reserve of pine trees like North America and Europe, would assure growth in this market.

To get more information on this market Request Sample

The United States pine chemicals market is driven by amplified demand with 90.9% market share for sustainable and bio-based products across industries, such as adhesives, coatings, personal care, and food additives, as companies prioritize reducing their environmental footprint. Accelerating growth in regulatory pressure to limit the use of petrochemical-based alternatives has propelled the adoption of pine-derived products, such as rosin, tall oil, and turpentine, that offer eco-friendly, renewable, and biodegradable solutions. Advances in extraction and refining technologies have enhanced production efficiency, product quality, and cost-effectiveness, making pine chemicals more accessible for industrial applications. Furthermore, the U.S. is emerging with extensive pine tree availability, with an ample and constant supply of raw materials in the southeast. Bolstering demand from the construction, packaging, and automotive sectors that use high-performance adhesives and coatings fuels growth further as companies turn towards sustainable alternatives. For instance, Kraton’s Revolution™ Rosin Ester technology, launched in January 2024, provides a sustainable, biobased alternative for adhesives, enabling up to a 30% reduction in greenhouse gas emissions while maintaining performance, color, and stability, supporting the bioeconomy and circularity.

Pine Chemicals Market Trends:

Rising Demand for Bio-Based and Renewable Chemicals

This trend for the need of bio-based chemicals is seen growing in the global market. Pine chemicals, based on renewable raw materials like tall oil and gum rosin, are intensely displacing petrochemical-based equivalents in industrial applications. Such government regulations to minimize the environment impact and promote ecofriendly alternatives support this trend further. Bio-based ingredients are gaining popularity, especially in the adhesives, coatings, and personal care industries, in response to amplifying consumer demand for more eco-friendly solutions. In addition, pine chemicals provide exclusive performance benefits; these include biodegradable characteristics, high adhesive strength, and compatibility with different formulations, creating an excellent opportunity for production of sustainable products. These are now gaining momentum based on the ecological advantages of this product line, which place the industry on a stronger growth trajectory for the coming years.

Technological Advancements in Pine Chemical Extraction

The application of technological innovation in extraction processes is substantially escalating the production efficiency of pine chemicals and therefore supporting market growth. Current technologies include fractional distillation, solvent extraction, and molecular distillation. Modern recovery techniques improve the availability of the valuable products obtained from pine trees, including rosin, tall oil fatty acids, and turpentine. As production costs decline, and purity levels increase while minimizing the formation of waste products, the cost advantage that synthetic alternatives may enjoy diminishes with regard to pine chemicals. Moreover, companies are investing in research and development to improve yields from renewable raw materials, ensuring better resource utilization. Enhanced extraction technologies also allow to produce tailored pine chemical derivatives, catering to specific industrial requirements in adhesives, coatings, and specialty chemicals, thereby amplifying adoption across end-use markets.

Growing Applications in Personal Care and Fragrance Industries

The rising consumer preference for natural and bio-based ingredients in personal care and fragrance products is propelling the demand for pine chemicals. Pine-derived components such as turpentine and rosin serve as key raw materials in the production of fragrances, deodorants, soaps, and cosmetics due to their natural antibacterial and biodegradable properties. This trend is fueled by growing awareness of harmful effects associated with synthetic chemicals, driving consumers and manufacturers toward sustainable alternatives. According to reports, the fragrances segment grew by 12% in January-September 2024, nearly double the 6% growth in personal care, as demand surged, and companies raised prices. Pine chemicals are increasingly used in fragrance formulations, supporting this growth. Additionally, the global expansion of the personal care industry, coupled with changing lifestyles and demand for premium, eco-friendly products, has amplified the adoption of pine chemicals. Companies are focusing on producing high-quality, pine-based derivatives that meet stringent safety and environmental standards, further reinforcing the market’s growth potential in the personal care segment.

Pine Chemicals Market Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global pine chemicals market, along with forecasts at the global, regional and country levels from 2026-2034. The market has been categorized based on product type, source, and application.

Analysis by Product Type:

- Tall Oil

- Rosin

- Turpentine

- Others

Rosin stands the largest segment in the pine chemicals market in 2025 with 46.8% share, due to its versatile applications across multiple industries. Rosin is widely used in adhesives, coatings, inks, and sealants, mainly because of its excellent tackiness, binding, and film-forming properties. The construction, packaging, and automotive industries' demand for high-performance adhesives contributes to the dominance of this segment. Furthermore, rosin is a critical component in soldering flux, personal care products, and food-grade additives which is boosting its market base. Various innovations with respect to derivative of rosin, have modified rosins and emulsions among others improve its utility. However, considering sustainability concerns rose nowadays with natural and renewable aspects, making it a promising substitute in favor of petrochemical-based products within global markets.

Analysis by Source:

- Pine Trunks

- Aged Pine Stumps

- Kraft Pulp

In 2025, pine trunks are accounted as largest segment with 52.5% share in the pine chemicals market, serving as a major raw material source for rosin, turpentine, and tall oil production. Pine trunks, sourced by tapping and wood pulping processes, ensure a reliable and constant supply of bio-based chemicals for adhesives, coatings, and personal care applications. Large-scale availability, primarily in resource-rich areas of North America and Europe, propels this segment further ahead steadily. Technological breakthroughs in extraction methodology maximize efficiency, improving yield, while reducing waste. With bolstering global emphasis on sustainability, pine trunk utilization ensures the development of renewable and eco-friendly chemicals, further strengthening its position as the primary feedstock for pine chemical production across industrial and commercial markets.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

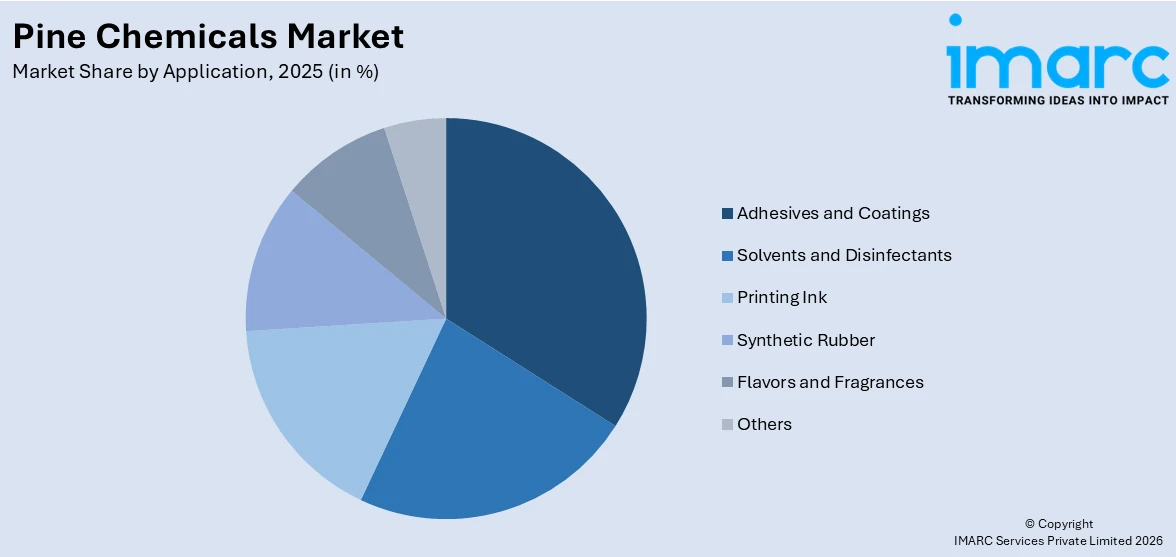

- Adhesives and Coatings

- Solvents and Disinfectants

- Printing Ink

- Synthetic Rubber

- Flavors and Fragrances

- Others

The adhesives and coatings segment dominates the pine chemicals market in 2025, with 33.2% share due to its widespread industrial applications and growing demand for eco-friendly solutions. The key usage of pine-based products in adhesives and coatings is rosin and tall oil fatty acids, showing excellent durability, tackiness, and binding properties. In the construction, automotive, and packaging industries, there is a growing interest in using bio-based adhesives and coatings for sustainability purposes and reducing dependence on synthetic chemicals. Also, the compatibility of pine chemical derivatives with modern industrial processes enhances demand. The shift towards ecofriendly solutions in infrastructure and manufacturing sectors, along with amplifying regulatory support for bio-based chemicals, ensures adhesives and coatings remain a leading segment in the market.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, Europe is accounted as the largest regional market for pine chemicals with 26.3% share, driven by strong environmental regulations and a focus on sustainability. The demand for bio-based alternatives to petrochemical products in the region has hastened the growth of pine chemicals in adhesives, coatings, personal care, and fragrances. Germany, France, and Sweden are the leading contributors, with their advanced industrial base and availability of raw material from managed pine forests. Technological advancements in extraction and production processes further enhance the growth of the region's market. Moreover, the growing demand for pine-based products in the construction and automotive industries, coupled with government support for sustainable solutions, further strengthens Europe's leadership position. The region's focus on circular economies and eco-friendly innovations remains a strong driver for the expansion of the pine chemical market.

Key Regional Takeaways:

North America Pine Chemicals Market Analysis

The North America pine chemicals market is experiencing steady growth, driven by the region's abundant pine tree resources, particularly in the southeastern United States, which serves as a key raw material hub for rosin, tall oil, and turpentine production. The growing demand for sustainable and bio-based alternatives across industries such as adhesives, coatings, personal care, and fragrances is a major factor propelling market expansion. Stringent environmental regulations and increasing corporate commitments to sustainability are encouraging the shift away from petrochemical-based products toward renewable solutions. Additionally, technological advancements in extraction and refining processes are enhancing production efficiency and product quality, boosting the adoption of pine chemicals in construction, automotive, and packaging applications. The presence of established market players and their focus on innovation and capacity expansion further support the region's leadership in the global market.

United States Pine Chemicals Market Analysis

Pine chemicals are widely used in adhesives, coatings, and automotive applications due to their superior bonding properties. The country’s strong chemical industry infrastructure, along with significant investments in green chemistry, fosters innovation. Furthermore, pine-based products are gaining popularity in bio-based materials, such as surfactants, resins, and plastics, especially with growing interest in eco-friendly alternatives to petroleum-based chemicals. Additionally, stringent environmental regulations have pushed industries to adopt renewable raw materials, offering a competitive advantage for pine chemicals. The availability of pine forests in the southeastern U.S. provides a consistent raw material supply, further enhancing production capabilities. The automotive and construction industries’ shift toward environmentally friendly coatings and adhesives contributes to the rising use of pine-based products in America. According to reports, the U.S. auto industry contributes 3% of GDP and employs 1.7 Million people directly. As automobile manufacturing grows, the demand for pine chemicals, used in various automotive applications has raised, boosting their market potential. As global demand for sustainable products increases, the U.S. remains at the forefront of adopting innovative pine chemical applications across various sectors, positioning itself as a leader in developing eco-conscious solutions.

Asia Pacific Pine Chemicals Market Analysis

Asia-Pacific stands as a pivotal region for the growth of pine chemical applications, largely fuelled by the growing industrial base and rising environmental concerns. Countries like China and India have seen rapid urbanization, driving demand for chemicals in construction materials, adhesives, and paints. According to World Bank, India's rapid urbanization, with its urban population expected to reach 600 Million by 2036, requires USD 840 Billion in infrastructure investments by 2036 (approximately USD 11 Billion annually), which will boost demand for pine chemicals used in sustainable urban development and infrastructure projects. As the region focuses on sustainable industrial practices, pine-derived resins and solvents are gaining traction as alternatives to petroleum-based products. The rise in demand for eco-friendly coatings in industries like automotive and electronics, as well as in household products, has led to the increased adoption of bio-based pine chemicals. In addition, the region's significant forest resources, particularly in Southeast Asia, ensure a steady supply of raw materials. Governments in countries like China and Japan are also incentivizing green manufacturing processes, further promoting the use of renewable chemicals. As industries prioritize sustainability, the region’s shift towards clean technologies and renewable resources positions it as a key hub for the pine chemicals sector. With robust infrastructure, the Asia-Pacific market is poised to continue expanding as businesses transition to greener alternatives across various sectors.

Europe Pine Chemicals Market Analysis

Europe’s market for pine chemicals is driven by a strong commitment to sustainability and environmental stewardship. The European Union's emphasis on reducing carbon footprints and promoting renewable energy solutions has boosted the demand for bio-based chemicals. For instance, according to European Environment Agency, in 2023, renewable energy sources accounted for an estimated 24.1% of the European Union's final energy use and to meet the EU's 42.5% target for 2030. Pine chemicals are highly used in applications, such as paints, adhesives, and personal care products, where their natural properties and minimal environmental impact make them attractive to manufacturers. The EU’s extensive regulatory framework, including REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals), has led to the substitution of harmful synthetic chemicals with more sustainable pine-based alternatives. Moreover, the region’s well-established forestry sector in countries like Finland and Sweden offers abundant access to raw materials, ensuring the continuous supply of pine-derived chemicals. The motivation for ecofriendly products in the automotive, packaging, and consumer goods industries has accelerated the adoption of pine chemicals as a sustainable alternative. The European market benefits from advanced research and innovation in the field of green chemistry, with companies constantly developing new applications for pine-derived products. This, combined with consumer preference for eco-friendly solutions, ensures that the region remains a significant player in driving the global demand for sustainable chemical products.

Latin America Pine Chemicals Market Analysis

Latin America benefits from the availability of vast pine forests, making it an ideal region to produce pine chemicals. The demand for these chemicals is primarily driven by the increasing use of sustainable materials in construction and packaging. For instance, the Brazilian Chamber of Construction Industry (CBIC) forecasts a 3.5% growth in the sector's GDP, up from 3%, driven by affordable housing. Pine resins are frequently used in adhesives, especially in the wood and furniture industries. Additionally, the growing focus on green building practices has led to an uptick in the use of eco-friendly construction materials derived from pine chemicals. The region’s favourable climate for pine cultivation further supports the industry’s growth, providing a steady raw material supply.

Middle East and Africa Pine Chemicals Market Analysis

In the Middle East and Africa, the growing demand for natural ingredients in the flavours and fragrances industry is a key driving factor for the pine chemicals sector. As consumers in the region lean toward organic and sustainable products, pine-derived chemicals, particularly those used in fragrances and perfumes, experience heightened demand. The flourishing fragrance market, coupled with a growing interest in plant-based and eco-friendly products, has led to an increased need for natural sources of chemical ingredients. According to research in the UAE, Saudi Arabia, and Kuwait shows that 76% of consumers prioritize sustainability in their purchasing decisions, with nearly 75% willing to pay a premium for eco-friendly products, highlighting a growing demand for sustainable practices in the GCC region. With a rising middle class and changing consumer preferences, this region is witnessing a steady rise in the consumption of pine chemicals in personal care and food industries.

Competitive Landscape:

The competitive scenario of the pine chemicals market is dominated by global leading players, with an approach towards innovation, sustainability, and strategic expansions. The leading companies focus on achieving high-quality product efficiency with the aid of advanced extraction technologies. These players are highly focusing on research and development (R&D) in producing eco-friendly and bio-based pine chemical derivatives that can fulfill the increasingly industrialized demand for environmentally friendly solutions. Strategic merger and acquisition, as well as collaborations, are seen to enhance geographic reach, strengthen supply chains, and further expand production facilities within regions of rich pine resources like North America and Europe, thus cementing market positions. Growth in this area is driven by competitive differentiation in terms of product customization, improved performance, and the fulfillment of environmental regulations.

The report provides a comprehensive analysis of the competitive landscape in the pine chemicals market with detailed profiles of all major companies, including:

- Arakawa Chemical Industries, Ltd.

- Arboris

- DRT (DSM-Firmenich)

- Florachem Corporation

- Forchem Oyj

- Harima Chemicals Group, Inc.

- Kraton Corporation

- OOO Torgoviy Dom Lesokhimik

- Pine Chemical Group

- Sunpine AB

Latest News and Developments:

- July 2024: Kraton Corporation and DL Chemicals have raised USD 1 Billion in global bonds, backed by KDB's credit guarantee. The funds will enhance Kraton's sustainable innovations, including biobased products from pine chemical co-products. The issuance attracted investors globally, highlighting market confidence. Key bookrunners included KDB, Citigroup, and JP Morgan.

- March 2024: Brazilian pine chemicals group Grupo Resinas Brasil (RB) is set to acquire Portugal’s Pinopine, a producer of gum rosin derivatives, sources reveal. This deal will enhance RB’s access to European markets, leveraging Pinopine’s strategic location in Aveiro. Pinopine employees have been informed, though financial details remain undisclosed. Portugal is a significant importer of Brazilian gum rosin, key in producing rosin esters.

- April 2024: Nordmann has extended its partnership with Kraton Corporation to distribute pine chemical and specialty resin products across several European countries. This collaboration enhances access to Kraton's pine-based resins for applications in paints, coatings, and adhesives. The expansion strengthens both companies’ presence in the European market. The partnership aims to cater to growing industry demands.

- February 2024: Kraton Corporation has introduced SYLVASOLV, an innovative biobased oils product line derived from pine chemicals. The first product, SYLVASOLV 1000, addresses agriculture needs, enhancing fertilizer coatings and crop protection. This launch reinforces Kraton's commitment to sustainable solutions across industries like agrochemicals and adhesives. SYLVASOLV offers superior performance with environmental benefits.

- August 2023: Pine Chemical Group has inaugurated a state-of-the-art production site in Kotka, Finland. The facility expands the company's portfolio with certified products, including Crude Tall Oil, Tall Oil Pitch, and Pitch Fuel, adhering to REACH standards. This initiative underscores their commitment to innovation and customer satisfaction. The site is expected to bolster sustainable production capabilities. Pine Chemical Group continues to meet evolving market demands with quality and compliance.

Pine Chemicals Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Tall Oil, Rosin, Turpentine, Others |

| Sources Covered | Pine Trunks, Aged Pine Stumps, Kraft Pulp |

| Applications Covered | Adhesives and Coatings, Solvents and Disinfectants, Printing Ink, Synthetic Rubber, Flavors and Fragrances, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Arakawa Chemical Industries, Ltd., Arboris, DRT (DSM-Firmenich), Florachem Corporation, Forchem Oyj, Harima Chemicals Group, Inc., Kraton Corporation, OOO Torgoviy Dom Lesokhimik, Pine Chemical Group, Sunpine AB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pine chemicals market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the pine chemicals market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pine chemicals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Pine Chemicals Market Report

Pine chemicals are bio-based products derived from pine trees, primarily obtained through the distillation of pine resin, tall oil, or wood pulping byproducts. Key components include rosin, turpentine, and tall oil fatty acids. They are widely used in adhesives, coatings, inks, fragrances, personal care, and food additives, they offer sustainable, biodegradable alternatives to petrochemical-based chemicals across multiple industries.

The pine chemicals market was valued at USD 6.0 Billion in 2025.

IMARC estimates the pine chemicals market to exhibit a CAGR of 3.32% during 2026-2034.

The pine chemicals market is driven by rising demand for bio-based and sustainable chemicals, advancements in extraction technologies, increasing applications in adhesives, coatings, personal care, and fragrances, and growing environmental regulations that encourage alternatives to petrochemicals. Expanding industrial sectors and consumer preference for eco-friendly products further fuel growth.

In 2025, rosin represented the largest segment by product type, driven by its extensive use in adhesives, coatings, inks, and personal care. Its superior binding properties, tackiness, and eco-friendly characteristics continue to support strong industrial demand.

Pine trunks leads the market by source offering abundant and renewable raw materials for producing rosin, turpentine, and tall oil. Their cost-effectiveness and consistent availability make them essential for large-scale pine chemical production.

The adhesives and coatings are the leading segment by application, fueled by rising demand in construction, automotive, and packaging industries. The shift toward durable, high-performance, and sustainable solutions accelerates the adoption of pine-based adhesives and coatings globally.

On a regional level, the market has been classified into Asia Pacific, Europe, North America, Latin America, Middle East and Africa, wherein Europe currently dominates the market.

Some of the major players in the pine chemicals market include Arakawa Chemical Industries, Ltd., Arboris, DRT (DSM-Firmenich), Florachem Corporation, Forchem Oyj, Harima Chemicals Group, Inc., Kraton Corporation, OOO Torgoviy Dom Lesokhimik, Pine Chemical Group, Sunpine AB, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)