Pin and Sleeve Devices Market Size, Share, Trends and Forecast by Product, Material, End Use, and Region, 2026-2034

Pin and Sleeve Devices Market Size and Share:

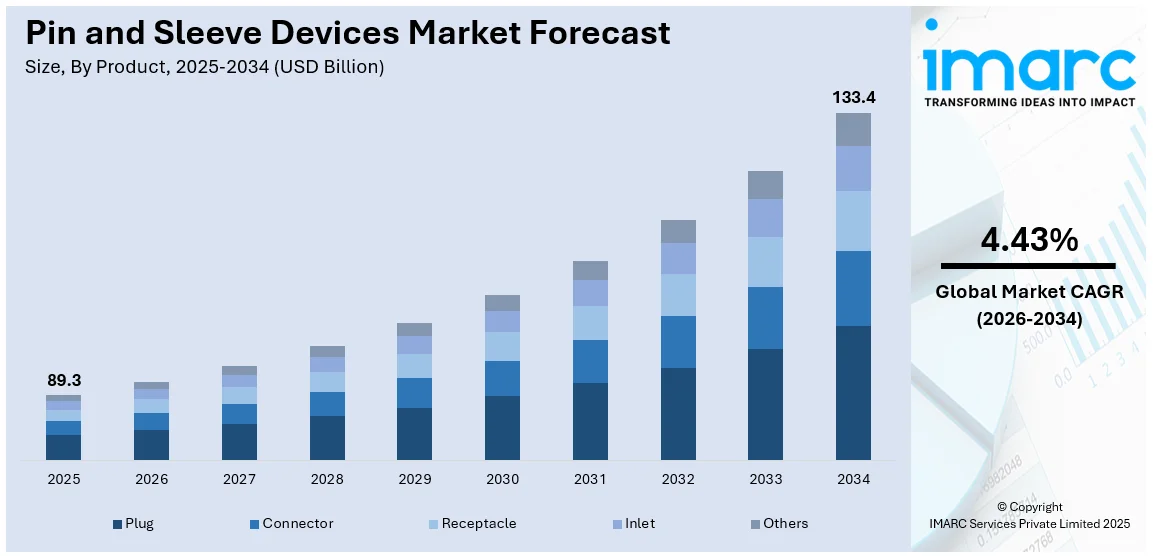

The global pin and sleeve devices market size was valued at USD 89.3 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 133.4 Billion by 2034, exhibiting a CAGR of 4.43% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of over 36.7% in 2025. The market is expanding due to increasing demand for secure, high-performance electrical connections across industrial, commercial, and residential sectors. Advancements in material technology and safety standards further support market expansion, strengthening pin and sleeve devices market share globally.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 89.3 Billion |

|

Market Forecast in 2034

|

USD 133.4 Billion |

| Market Growth Rate 2026-2034 | 4.43% |

The pin and sleeve devices market is driven by increasing industrial automation, stringent safety regulations and rising demand for secure power connections in hazardous environments. Growth in manufacturing, construction, and data centers fuels adoption, while the need for high-performance, moisture-resistant connectors supports market expansion. According to the report published by the US Census Bureau, in January 2025, total construction spending reached a seasonally adjusted annual rate of $2,192.5 billion, up 3.3% from January 2024. Private construction was $1,686.0 billion, residential at $932.7 billion, and public construction at $506.6 billion, up 0.1% from December. Advancements in durable, corrosion-resistant materials enhance product longevity, further boosting pin and sleeve devices market demand. Additionally, the rise of electric vehicles and renewable energy infrastructure requires robust power distribution solutions, contributing to the steady growth of the market.

To get more information on this market Request Sample

The United States pin and sleeve devices market is driven by strict workplace safety regulations, increasing industrial automation, and rising demand for reliable power distribution in manufacturing and construction. Growth in data centers, renewable energy projects, and electric vehicle infrastructure further boosts adoption. In January 2025, the Biden-Harris Administration announced $635 million in grants to expand EV charging and alternative fueling infrastructure. The funding, from the Bipartisan Infrastructure Law, will create over 11,500 charging ports across 49 projects in 27 states and the District of Columbia, supporting the goal of 500,000 EV chargers by 2030. The need for durable, waterproof, and corrosion-resistant connectors in harsh environments supports market expansion. Additionally, investments in advanced electrical systems, coupled with technological advancements in high-performance connectors, drive demand across industrial, commercial, and energy sectors.

Pin and Sleeve Devices Market Trends:

Expansion of Data Centers

Government investments in digital infrastructure are further accelerating the demand for reliable power distribution solutions. For instance, in January 2025, President-elect Donald Trump announced a $20 billion investment plan for new data centers across eight states, including Arizona and Texas, aiming to support AI and cloud technologies. Pin and sleeve devices ensure secure, high-capacity electrical connections essential for uninterrupted operations. Their durability, moisture resistance, and compliance with safety standards make them ideal for mission-critical IT environments. As hyperscale and edge data centers expand, the need for robust, high-performance electrical connectors continues to rise, supporting market growth.

Increasing Adoption in EV Charging and Renewable Energy

The rapid expansion of electric vehicle (EV) charging infrastructure and renewable energy projects is driving demand for durable electrical connectors. For instance, in September 2024, the Government of India issued revised EV charging station guidelines, introducing a revenue-sharing model to enhance financial viability. Under the PM E-DRIVE scheme, 74,300 chargers will be installed, including 22,100 fast chargers, with a Rs 2,000 crore budget. By 2030, one station will be required every 1 km in urban areas. Pin and sleeve devices provide reliable, weather-resistant power connections essential for EV charging stations, solar farms, and wind energy installations. Their ability to withstand harsh conditions, including moisture and temperature fluctuations, ensures long-term performance. As governments and industries invest in clean energy and transportation electrification, the need for high-performance electrical connectors continues to grow, supporting market expansion.

Advancements in Material Technology

The development of corrosion-resistant, waterproof, and high-durability materials is improving the performance and longevity of pin and sleeve devices. Manufacturers are focusing on high-grade thermoplastics and stainless steel to enhance resistance against extreme temperatures, moisture, and chemicals. These advancements ensure reliable power connections in industrial, marine, and outdoor applications, reducing maintenance costs and downtime. With growing demand for robust electrical solutions across sectors, material innovations are shaping the future of the industry thereby creating a positive pin and sleeve devices market outlook.

Pin and Sleeve Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global pin and sleeve devices market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, material, and end use.

Analysis by Product:

- Plug

- Connector

- Receptacle

- Inlet

- Others

Connector stands as the largest product in 2025, holding around 35.9% of the market. Connectors dominate the pin and sleeve devices market due to their critical role in ensuring secure, high-performance electrical connections across industries. Their widespread adoption in manufacturing, data centers, construction, and EV charging infrastructure drives market growth. Advanced designs with corrosion resistance, waterproofing, and enhanced safety features make them essential for harsh environments. As industries prioritize reliable power distribution and regulatory compliance, demand for durable, high-quality connectors continues to rise, reinforcing their position as the largest product segment.

Analysis by Material:

Access the comprehensive market breakdown Request Sample

- Metallic

- Non-Metallic

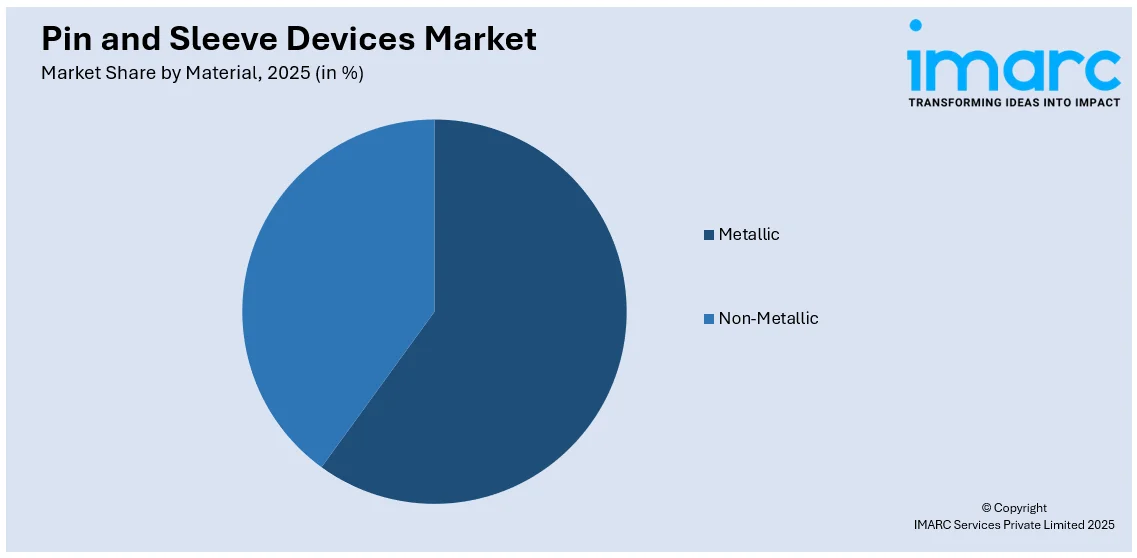

Metallic pin and sleeve devices offer superior durability, corrosion resistance, and high load-bearing capacity, making them ideal for heavy-duty industrial applications. Commonly made from stainless steel or aluminum, these connectors withstand extreme temperatures, chemicals, and mechanical stress. Their reliability in demanding environments, such as manufacturing plants and marine operations, drives significant market adoption.

Non-metallic pin and sleeve devices, typically made from high-grade thermoplastics, provide lightweight, cost-effective, and corrosion-resistant solutions. These devices offer excellent electrical insulation, moisture resistance, and impact protection, making them suitable for food processing, healthcare, and outdoor applications. Their increasing use in industries requiring non-conductive, easy-to-install connectors supports market growth, particularly in safety-sensitive and regulated sectors.

Analysis by End Use:

- Residential

- Commercial

- Industrial

- Automotive

- Manufacturing

- Oil and Gas

- Energy and Power

Residential leads the market with around 65.0% of market share in 2025. The residential sector dominates the pin and sleeve devices market due to increasing demand for safe and reliable electrical connections in smart homes, EV charging stations, and modern housing infrastructure. Rising adoption of home automation, renewable energy systems, and high-performance electrical appliances further boosts demand. Non-metallic, weather-resistant connectors ensure safety and durability in residential applications. As urbanization and electrification projects expand, the need for advanced pin and sleeve devices in homes continues to grow, driving market leadership.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, Asia-Pacific accounted for the largest market share of over 36.7%. Asia-Pacific holds the largest share in the pin and sleeve devices market due to rapid industrialization, urban expansion, and growing infrastructure projects. Increasing manufacturing activities in China, India, and Southeast Asia drive demand for durable electrical connectors. Government investments in renewable energy, EV charging stations, and smart city initiatives further boost market growth. Expanding data centers and automation in industries require high-performance power distribution solutions, reinforcing Asia-Pacific’s dominance in the global Pin and Sleeve Devices market.

Key Regional Takeaways:

North America Pin and Sleeve Devices Market Analysis

The pin and sleeve devices market in North America is expanding due to increasing industrial automation, stringent safety regulations, and modernization of electrical infrastructure. The demand for high-performance, weather-resistant connectors is growing across industries such as manufacturing, construction, and data centers. Rising adoption of electric vehicles and renewable energy projects is further driving the need for secure power distribution solutions. The region’s stringent electrical safety standards encourage innovation in interlock features, explosion-proof designs, and high-durability materials. Additionally, investments in smart grid development and advanced power management systems are creating opportunities for technologically enhanced pin and sleeve devices. The food and beverage sector, along with pharmaceuticals, requires connectors that comply with hygiene and washdown-resistant standards. Market players are focusing on ergonomic designs, heat-resistant materials, and smart features to enhance safety, efficiency, and ease of use in various industrial and commercial applications.

United States Pin and Sleeve Devices Market Analysis

In 2025, the United States accounted for over 87.60% of the pin and sleeve devices market in North America. The pin and sleeve devices market in the United States is significantly driven by strict safety regulations, industrial automation, and increasing demand for high-power electrical solutions. Similarly, industries such as manufacturing, construction, and data centers require rugged, moisture-resistant, and corrosion-proof connectors to maintain uninterrupted power supply. The growth of EV charging infrastructure and smart grid modernization further drives market demand. The Biden-Harris Administration recently allocated USD 521 Million in grants to support EV charging infrastructure across 29 states, 8 Tribes, and Washington, D.C., leading to the deployment of 9,200+ charging ports. Since 2021, the number of public EV chargers has doubled to 192,000, with 1,000 new chargers added weekly. Supported by the Bipartisan Infrastructure Law, programs like CFI and NEVI are encouraging private investments and job creation, enhancing national EV accessibility. The National Electrical Code (NEC) mandates safety interlock features in industrial plug-and-socket systems, driving innovation in IP-rated and explosion-proof devices. Furthermore, the ongoing shift to renewable energy also increases demand, as wind and solar farms require high-durability connectors for efficient energy distribution. Besides this, manufacturers prioritize ergonomic designs, heat-resistant materials, and advanced locking for safety and efficiency.

Europe Pin and Sleeve Devices Market Analysis

The pin and sleeve devices market in Europe is expanding due to strict EU safety regulations, industrial automation, and modernization of electrical infrastructure. Leading economies like Germany, France, and the UK drive adoption, propelled by high energy efficiency standards and workplace safety policies. The IEC 60309 standard plays a key role in market trends, prompting manufacturers to develop standardized, durable connectors that meet rigorous compliance requirements. The growing emphasis on electric mobility and railway electrification has fueled demand for high-amperage, weatherproof pin and sleeve devices. According to an industry report, EV sales in Western Europe are projected to increase 40% to 2.7 Million in 2025, with BEVs capturing 22% of the market. By 2026, 3 Million EVs are expected to be sold. Despite subsidy changes, Europe's EV market is expanding, increasing demand for heavy-duty connectors in charging infrastructure. The region’s renewable energy push, especially in offshore wind and solar, further drives high-durability electrical connections. Additionally, the food and beverage sector, especially in Italy and Spain, requires washdown-resistant and antimicrobial plug systems to maintain compliance with strict hygiene regulations, strengthening the market for specialized devices in industrial applications.

Latin America Pin and Sleeve Devices Market Analysis

In Latin America, the pin and sleeve devices market are propelled by industrial growth, infrastructure investments, and rising energy demands. By 2030, Latin America and the Caribbean (LAC) must invest over USD 2.22 Trillion in water, sanitation, energy, transportation, and telecommunications to meet Sustainable Development Goals (SDGs). 59% is needed for new infrastructure, while 41% will go to maintenance and asset replacement. This requires annual investment of 3.12% of GDP, according to the infrastructure integration and connectivity index. Moreover, Brazil, Mexico, and Argentina drive demand for rugged connectors through energy projects and private investments. Chile and Peru's mining sector relies on high-amperage devices for harsh conditions. Besides this, construction, industrial automation, oil and gas, and smart grid adoption further support demand for heat-resistant, explosion-proof, and smart connectors.

Middle East and Africa Pin and Sleeve Devices Market Analysis

The market in the Middle East and Africa is experiencing growth propelled by large-scale infrastructure projects, extreme climatic conditions, and industrial expansion. In early 2024, Saudi factories attracted SR38.6 Billion (USD 10.2 Billion) in investments, surpassing 2023’s pace by two months, per an industry report. The Saudi Authority for Industrial Cities expanded developed industrial land to 209 Million sq. meters, supporting 6,443 factories and 7,946 industrial, logistical, and investment establishments. Furthermore, Saudi Arabia, the UAE, and South Africa demand industrial-grade connectors for oil refineries, construction, and renewable energy. The GCC oil and gas sector needs explosion-proof connectors, while Africa’s mining industry drives demand for durable solutions. Apart from this, Middle East data centers fuel growth in high-current, surge-protected connectors.

Competitive Landscape:

The pin and sleeve devices market is highly competitive, driven by continuous innovation in product design, material technology, and safety standards. Manufacturers focus on developing durable, waterproof, and corrosion-resistant connectors to meet industry demands. Market players are investing in research and development to enhance product efficiency, withstand harsh environments, and comply with regulatory requirements. Collaborations, mergers, and acquisitions are frequently utilized strategies to enhance market presence and technological competencies. With increasing demand from industrial, commercial, and residential sectors, companies are strengthening their distribution networks and after-sales services to maintain a competitive edge in this evolving market.

The report provides a comprehensive analysis of the competitive landscape in the pin and sleeve devices market with detailed profiles of all major companies, including:

- ABB Ltd

- Amphenol Corporation

- Eaton Corporation plc

- Emerson Electric Co.

- Hubbell Incorporated

- Legrand Group

- MELTRIC (Marechal Electric Group)

- MENNEKES Elektrotechnik GmbH & Co. KG

- Schneider Electric SE

- WALTHER-WERKE Ferdinand Walther GmbH

Latest News and Developments:

- February 2025: Sdiptech completed the acquisition of Phase 3 Connectors, a UK manufacturer specializing in high-current power connectors for industrial and event applications. With an annual EBIT of GBP 3 million, this acquisition strengthens Sdiptech’s Energy & Electrification unit, promoting growth in areas such as backup power, data centers, and live events.

- October 2024: Boomi introduced a new Veeva Vault connector designed to streamline integration with third-party applications in the life sciences sector. This low-code platform facilitates automated workflows, secure deployments, and easy data access, significantly reducing the need for manual coding. It aims to enhance operational efficiency and regulatory compliance throughout the drug development and commercialization processes.

- September 2024: Schneider Electric unveiled the UNICA X range of 6.5mm slimline stainless-steel switches and sockets in Hong Kong. This series includes various options such as 1-4G switches, BS sockets, universal sockets, 3-round pin sockets, USB chargers, dimmers, and hotel-specific configurations. Available in five colors and three textures, it combines innovative technology with high-end design.

- July 2024: Smiths Interconnect launched Press-Fit cPCI connectors that do away with the need for soldering, enabling more efficient installations for defense, space, and aerospace sectors. Leveraging Hyperboloid contact technology, these connectors support data rates of 3.125 Gbps while being resistant to shock and vibration. They comply with PICMG Compact PCI and IEC 1076-4-101 standards, ensuring dependable performance in demanding environments.

- July 2024: ABB Vietnam rolled out the ORIGEN, INORA, and ZENIT ranges of switches and sockets, focusing on safety, smart integration, and stylish design. The ZENIT model features an ultra-slim 4mm frame and includes options for universal sockets, British Standard sockets, and USB charging ports.

- May 2024: Molex launched the MX-DaSH portfolio of data-signal hybrid connectors, which combines power, signal, and high-speed data in a single compact system suitable for next-generation automotive designs. This innovation simplifies wiring complexity, minimizes size and costs, and reduces labor, enabling support for autonomous systems, LiDAR, infotainment, and sensors while improving reliability and efficiency in automated assembly.

Pin and Sleeve Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Plug, Connector, Receptacle, Inlet, Others |

| Materials Covered | Metallic, Non-Metallic |

| End Uses Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB Ltd, Amphenol Corporation, Eaton Corporation plc, Emerson Electric Co., Hubbell Incorporated, Legrand Group, MELTRIC (Marechal Electric Group), MENNEKES Elektrotechnik GmbH & Co. KG, Schneider Electric SE and WALTHER-WERKE Ferdinand Walther GmbH |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the pin and sleeve devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global pin and sleeve devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the pin and sleeve devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The pin and sleeve devices market was valued at USD 89.3 Billion in 2025.

IMARC estimates the pin and sleeve devices market to reach USD 133.4 Billion by 2034, exhibiting a CAGR of 4.43% from 2026-2034.

The pin and sleeve devices market is driven by increasing industrial automation, stringent safety regulations, rising demand for reliable power connections in hazardous environments, and expanding data centers. Growth in EV charging infrastructure, renewable energy projects, and advanced material innovations further fuel market expansion across industrial, commercial, and residential applications.

Asia-Pacific holds the largest pin and sleeve devices market share due to rapid industrialization, growing infrastructure projects, and increasing demand for reliable power distribution in manufacturing, data centers, and renewable energy sectors. Government investments in EV charging stations and smart grid projects further drive market expansion in the region.

Some of the major players in the pin and sleeve devices market include ABB Ltd, Amphenol Corporation, Eaton Corporation plc, Emerson Electric Co., Hubbell Incorporated, Legrand Group, MELTRIC (Marechal Electric Group), MENNEKES Elektrotechnik GmbH & Co. KG, Schneider Electric SE and WALTHER-WERKE Ferdinand Walther GmbH., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)