Oxidized Polyethylene Wax Market Report by Product (High-density, Low-density), Application (Plastic Processing, Paints and Coatings, Textiles, Rubber Processing, Metal Processing, Adhesives, and Others), and Region 2026-2034

Oxidized Polyethylene Wax Market Size:

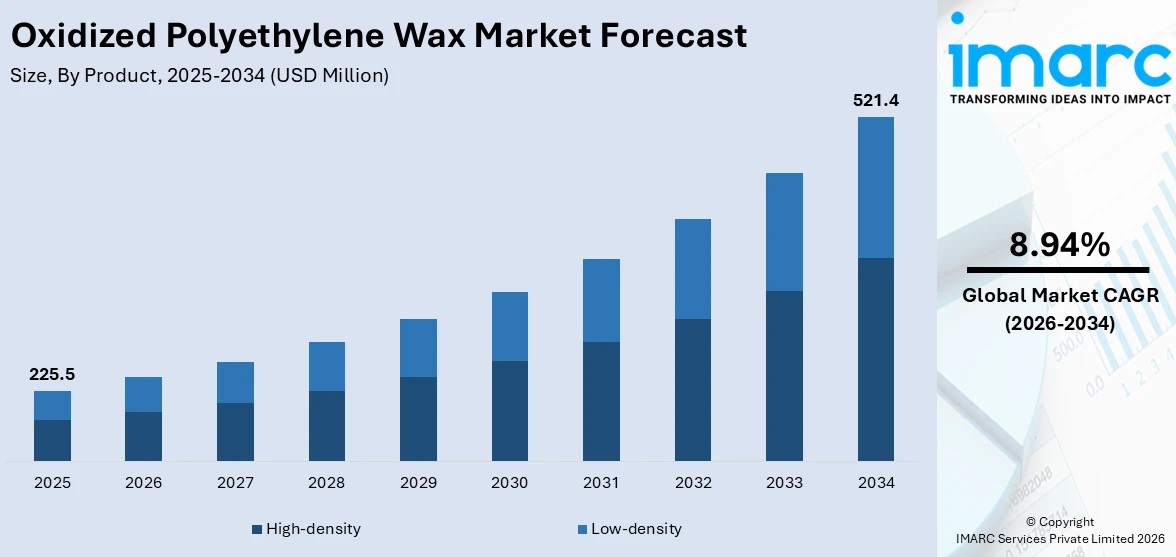

The global oxidized polyethylene wax market size reached USD 225.5 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 521.4 Million by 2034, exhibiting a growth rate (CAGR) of 8.94% during 2026-2034. The market is experiencing significant growth mainly due to the rising product demand in coatings, adhesives, and inks. The market is expanding gradually as industries nowadays seek enhanced performance in polymer processing and surface applications across diverse sectors.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 225.5 Million |

| Market Forecast in 2034 | USD 521.4 Million |

| Market Growth Rate (2026-2034) | 8.94% |

Oxidized Polyethylene Wax Market Analysis:

- Major Market Drivers: Key market drivers include the growing application of oxidized polyethylene wax in various industries, such as plastics, coatings and adhesives. The wax's excellent lubrication and dispersing properties makes it ideal for use in plastic processing thereby, enhancing the overall product's performance and durability. The rising demand for high-quality coatings and paints in automotive and construction sectors is also propelling the market growth. In line with this, the increasing focus on environmentally friendly materials is driving its adoption due to its non-toxic nature and biodegradability, further contributing to the oxidized polyethylene wax market growth.

- Key Market Trends: Key market trends include the growing shift toward eco-friendly and sustainable products mainly driven by increased environmental concerns and regulatory constraints. Manufacturers nowadays are focusing on producing bio-based waxes to meet demand for green alternatives. The rise in the demand for high-performance coatings, adhesives, and plastics is also pushing innovation in product development further leading to improved formulations with enhanced properties. In addition to this, advancements in polymer technology are expanding the use of oxidized polyethylene wax in niche applications including packaging and cosmetics where its emulsifying and stabilizing qualities are gaining attention contributing to market expansion.

- Geographical Trends: Geographical trends in the market show strong growth in Asia-Pacific, driven by rapid industrialization, expanding automotive and construction sectors, and the rising demand for plastic processing and coatings. China and India are key markets due to their growing manufacturing industries. In North America and Europe, the demand is fueled by advancements in polymer processing, as well as the shift toward eco-friendly materials in coatings and adhesives. These regions are also witnessing increased investment in research and development (R&D) to produce sustainable wax solutions. Meanwhile, Latin America and the Middle East are emerging markets, benefiting from infrastructure development and expanding industrial bases.

- Competitive Landscape: Some of the major market players in the oxidized polyethylene wax industry include BASF SE, Clariant AG, Deurex Ag, Honeywell International Inc, Industrial Raw Material LLC, Innospec Inc., Mitsui Chemicals Inc, Palmer Holland, The Lubrizol Corporation (Berkshire Hathaway Inc.), Trecora Resources, Westlake Chemical Corporation and Zellag, among many others.

- Challenges and Opportunities: The market faces various challenges including fluctuation in raw material prices and stringent environmental regulations, which can impact production costs and limit market growth. In addition to this, the availability of alternatives like Fischer-Tropsch waxes poses competitive pressure. However, opportunities abound with the rising demand for eco-friendly products pushing manufacturers to develop bio-based and sustainable wax solutions. Increasing applications in emerging sectors such as packaging, textiles and cosmetics offer significant growth potential. The continued expansion of industrial activities in developing regions further opens doors for market growth, with a focus on innovative, high-performance formulations to meet diverse industry needs.

To get more information on this market Request Sample

Oxidized Polyethylene Wax Market Trends:

Rising Demand in Plastics and Polymer Processing

According to oxidized polyethylene wax market insights, the growing demand for OPE wax in plastics and polymer processing is primarily driven by its ability to enhance thermal stability and processability, leading to optimized production cycles and lower energy consumption. OPE wax plays a crucial role in the plastics and polymer processing industry as a lubricant and processing aid. It is particularly effective in PVC and polyethylene compounds, improving melt flow and reducing friction during processing. According to an article published by Economic Times, Indian PVC industry seeks to quadruple capacity to support $10 trillion economy by 2030. Domestic demand surge met by 60% imports, primarily from China and the USA, poses a threat to the $8 billion investments lined up for capacity expansion. Recent reduction in PVC import duty to 7.5% led to a surge in imports, endangering domestic industry survival and potential investments. This enhances the overall efficiency of plastic production, reducing wear on machinery and improving the surface finish of end products. In sectors like automotive, construction, and packaging, where high-quality plastic materials are in the demand, OPE wax helps manufacturers achieve better product consistency, dimensional stability, and surface smoothness. Its ability to improve dispersion of pigments and fillers further boosts its utility in these industries.

Rising Demand from Coatings and Adhesives Industry

The rising demand for OPE wax in coatings and adhesives is fueled by its ability to significantly enhance surface properties, such as gloss, smoothness, and abrasion resistance. In coatings, OPE wax improves water repellency, hardness, and overall durability, making it ideal for use in industrial, automotive, and decorative applications. In adhesives, it enhances performance by improving tack and bond strength while also reducing friction during application. The product's compatibility with a wide range of formulations and its ability to improve texture and durability make it a valuable additive in both sectors, driving its increasing market demand. For instance, in February 2024, BASF and INEOS Automotive partnered to develop a global automotive refinish body and paint program, aiming to exceed industry standards and provide sustainable solutions. BASF will support INEOS body shop networks in Europe, North America, and Asia Pacific with expertise in sustainable and efficient refinish practices. This partnership extends their existing collaboration for the INEOS Grenadier and includes the newly launched Quartermaster vehicle.

Expanding Use in Emerging Market

The expanding use of OPE wax in emerging markets is driven by growing demand from industries such as automotive, packaging, and construction. These sectors are experiencing rapid growth due to increasing industrialization and urbanization in regions like Asia-Pacific, Latin America, and Africa. According to industry reports, Asia-Pacific’s Light Vehicle (LV) production surged by almost 10% YoY to a record 51.8 million units in 2023, driven by robust production in China and Japan. Companies are capitalizing on the rising need for high-performance materials, using OPE wax to enhance product quality, durability, and processing efficiency. As these markets continue to develop, the demand for OPE wax in applications like coatings, adhesives, and plastic processing is expected to grow, offering significant growth opportunities for manufacturers.

Oxidized Polyethylene Wax Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product and application.

Breakup by Product:

- High-density

- Low-density

High-Density accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product. This includes high-density and low-density. According to the report, high-density represented the largest segment.

High-density oxidized polyethylene (HDPE) wax holds a dominant share of the Oxidized Polyethylene Wax (OPE) market due to its superior performance characteristics. HDPE wax is favored for its high molecular weight and hardness, making it ideal for applications requiring enhanced durability and chemical resistance, such as in plastics, coatings, and adhesives. Its ability to improve flow properties, surface smoothness, and stability under extreme conditions makes it a preferred choice across industries. Moreover, HDPE wax's role as a processing aid in PVC and rubber compounding further cements its market leadership, driven by high demand in manufacturing and automotive sectors. For instance, in May 2023, Texplore, a subsidiary of SCG Chemicals, partnered with Lummus Technology to license EXCENE™, HDPE process technology, aiming to expand its reach in the global market. The agreement includes licensing of EXCENE™ technology, engineering design for plant construction, EL-CAT™ Catalyst supply and services, and operational lifecycle services. Lummus Technology is set to benefit from broadening its product portfolio and production technology services as a result of the collaboration. These developments are creating a positive oxidized polyethylene wax market outlook by expanding global production capacities and driving innovation in high-performance materials for key industries like manufacturing and automotive.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Plastic Processing

- Paints and Coatings

- Textiles

- Rubber Processing

- Metal Processing

- Adhesives

- Others

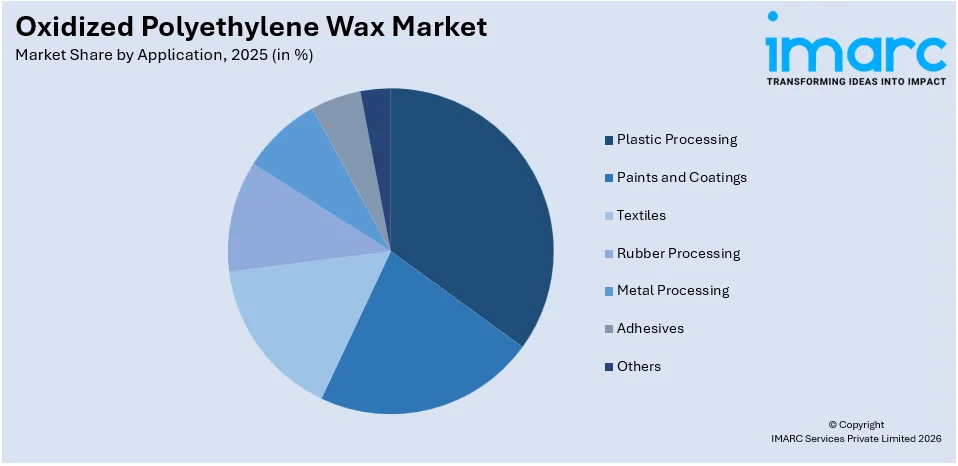

Plastic Processing holds the largest share of the industry

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes plastic processing, paints and coatings, textiles, rubber processing, metal processing, adhesives and others. According to the report, plastic processing accounted for the largest market share.

According to oxidized polyethylene wax market research report, plastic processing holds the largest share of the Oxidized Polyethylene Wax (OPE Wax) industry due to its extensive application as a lubricant and processing aid. In plastic production, OPE wax improves mold release, reduces friction, and enhances surface properties, making it essential for efficient manufacturing processes. Its use in PVC compounding, film production, and injection molding highlights its versatility and critical role in improving the performance of plastic products. This broad application across various plastic segments drives its dominant market share, further fueled by the increasing demand for high-performance materials in industries like packaging, automotive, and construction. Technological advancements and a growing emphasis on sustainable, bio-based wax alternatives are also shaping oxidized polyethylene wax market dynamics. The rise in environmental regulations, particularly in developed regions, is further encouraging the shift toward greener formulations. With these developments, the OPE wax market is expected to see sustained growth and innovation in the coming years.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest oxidized polyethylene wax market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represents the largest regional market for oxidized polyethylene wax.

North America leads the Oxidized Polyethylene Wax (OPE Wax) market, holding the largest share due to several key factors. The region's well-established manufacturing sectors, including automotive, construction, and packaging, drive significant demand for OPE wax as a lubricant and processing aid. According to industry reports, in December 2023, the United States produced 10,611,555.000 units of motor vehicles. The United States, in particular, plays a crucial role with its advanced plastic and polymer industries that rely on OPE wax for improving product durability, surface finish, and processing efficiency. Additionally, rising environmental regulations in North America have fueled the adoption of bio-based and eco-friendly wax alternatives, further strengthening the region's market position in sustainable manufacturing.

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the oxidized polyethylene wax industry include BASF SE, Clariant AG, Deurex Ag, Honeywell International Inc, Industrial Raw Material LLC, Innospec Inc., Mitsui Chemicals Inc, Palmer Holland, The Lubrizol Corporation (Berkshire Hathaway Inc.), Trecora Resources, Westlake Chemical Corporation and Zellag.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- The Oxidized Polyethylene Wax (OPE Wax) market is characterized by intense competition, driven by growing demand across industries such as plastics, coatings, and adhesives. Market players focus on product innovation, particularly in developing eco-friendly, bio-based formulations to comply with tightening environmental regulations. Advancements in production technologies are allowing manufacturers to improve wax performance in high-demand applications like PVC processing and rubber compounding. Pricing strategies also play a critical role as producers seek to balance cost efficiency with performance. Geographical expansion into emerging markets further intensifies competition, with companies aiming to tap into the rising demand from sectors like automotive and packaging. Differentiation through product quality and sustainability remains a key competitive edge. These factors are expected to increase the oxidized polyethylene wax market revenue in the coming future.

Oxidized Polyethylene Wax Market News:

- In May 2024, Shamrock Technologies' subsidiary, EDO Waxes, and South Carolina Polymer Group (SCPG) announced a joint venture to establish NeuWax, focusing on producing and distributing oxidized wax. Based in Cowpens, SC, the joint venture will specialize in manufacturing specialty high-density polyethylene waxes, with applications spanning various industries. Both Shamrock Technologies and NeuWax will be jointly exhibiting at the American Coatings Show in Indianapolis.

- In March 2024, AdPlus, a subsidiary of Haldia Petrochemicals Ltd, officially launched a cutting-edge LMW PE-PE Wax manufacturing plant in Haldia. The state-of-the-art facility, a collaboration with TCG Lifesciences, signifies a major step toward eco-friendly operations and technological advancement. The plant, with zero-waste discharge, is projected to revolutionize various industries such as plastics, adhesives, and cosmetics. This significant investment has also created job opportunities, marking a milestone for HPL's commitment to sustainability and innovation.

Oxidized Polyethylene Wax Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | High-Density, Low-Density |

| Applications Covered | Plastic Processing, Paints and Coatings, Textiles, Rubber Processing, Metal Processing, Adhesives, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BASF SE, Clariant AG, Deurex Ag, Honeywell International Inc, Industrial Raw Material LLC, Innospec Inc., Mitsui Chemicals Inc, Palmer Holland, The Lubrizol Corporation (Berkshire Hathaway Inc.), Trecora Resources, Westlake Chemical Corporation, Zellag, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the oxidized polyethylene wax market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global oxidized polyethylene wax market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the oxidized polyethylene wax industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Key Questions Answered in This Report

We expect the global oxidized polyethylene wax market to exhibit a CAGR of 8.94% during 2026-2034.

The rising demand for oxidized polyethylene wax in floor finishes to minimize black marks, provide stability, enhance friction, decrease slipping, etc., is primarily driving the global oxidized polyethylene wax market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary closure of numerous end-use industries for oxidized polyethylene wax.

Based on the product, the global oxidized polyethylene wax market has been segregated into high-density and low-density. Currently, high-density holds the largest market share.

Based on the application, the global oxidized polyethylene wax market can be bifurcated into plastic processing, paints and coatings, textiles, rubber processing, metal processing, adhesives, and others. Among these, plastic processing exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where North America currently dominates the global market.

Some of the major players in the global oxidized polyethylene wax market include BASF SE, Clariant AG, Deurex Ag, Honeywell International Inc, Industrial Raw Material LLC, Innospec Inc., Mitsui Chemicals Inc, Palmer Holland, The Lubrizol Corporation (Berkshire Hathaway Inc.), Trecora Resources, Westlake Chemical Corporation, and Zellag.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)