Osteogenesis Imperfecta Market Size, Epidemiology, In-Market Drugs Sales, Pipeline Therapies, and Regional Outlook 2025-2035

Market Overview:

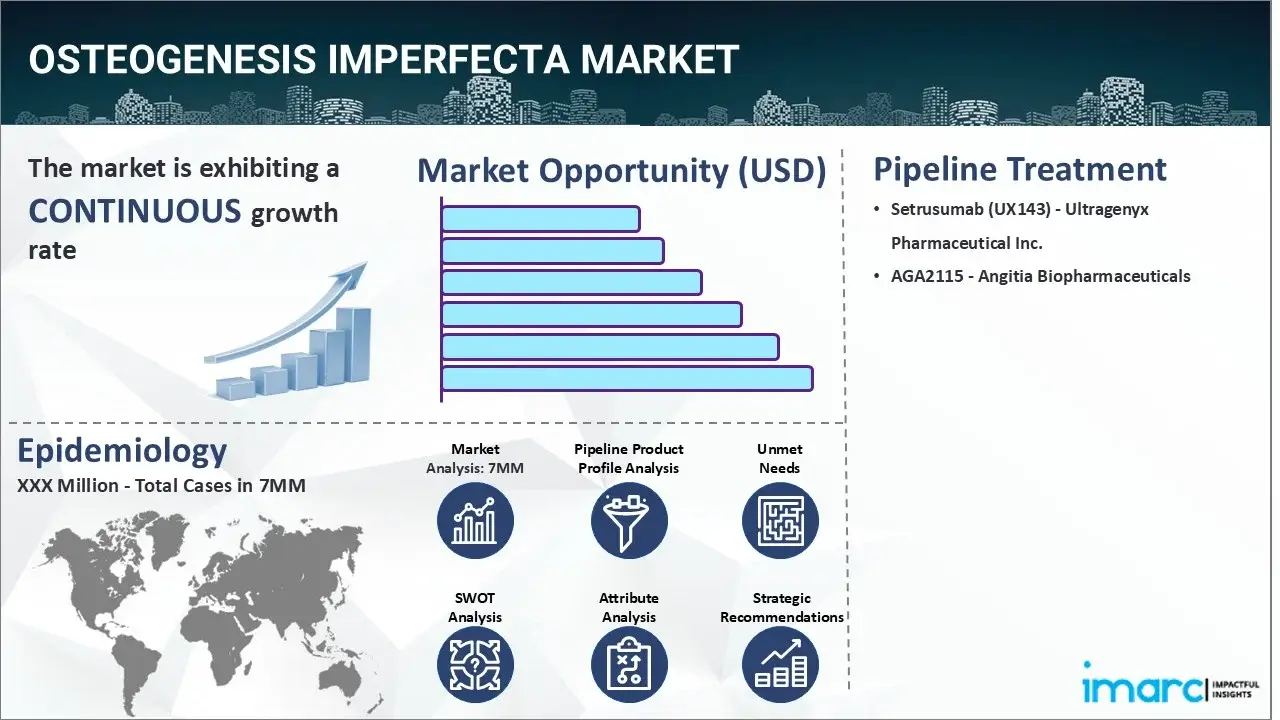

The osteogenesis imperfecta market reached a value of USD 515.3 Million across the top 7 markets (US, EU4, UK, and Japan) in 2024. Looking forward, IMARC Group expects the top 7 major markets to reach USD 625.8 Million by 2035, exhibiting a growth rate (CAGR) of 1.78% during 2025-2035.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Base Year |

2024

|

| Forecast Years | 2025-2035 |

| Historical Years |

2019-2024

|

|

Market Size in 2024

|

USD 515.3 Million |

|

Market Forecast in 2035

|

USD 625.8 Million |

| Market Growth Rate 2025-2035 | 1.78% |

The osteogenesis imperfecta market has been comprehensively analyzed in IMARC's new report titled "Osteogenesis Imperfecta Market Size, Epidemiology, In-Market Drugs Sales, Pipeline Therapies, and Regional Outlook 2025-2035". Osteogenesis imperfecta refers to a rare genetic disorder characterized by a defect in collagen production, which leads to fragile and easily breakable bones. This disease affects the connective tissues in the body, making bones more susceptible to fractures even with minimal force. The illness exhibits a wide spectrum of severity, with some patients experiencing frequent fractures, while others may have milder symptoms. Common indications of osteogenesis imperfecta include frequent bone fractures, bone deformities, short stature, joint laxity, and hearing loss. In severe cases, people suffering from the ailment might also experience breathing and mobility difficulties due to skeletal abnormalities. The diagnosis of the condition is typically based on a comprehensive evaluation of the patient's medical history, physical investigation, and imaging studies, such as X-rays or bone density tests. The healthcare professional may also perform genetic testing to confirm the prognosis and determine the specific gene mutation responsible for the disease.

To get more information on this market, Request Sample

The escalating prevalence of genetic mutations that affect collagen production in bones, resulting in fragile and easily breakable bones, is primarily driving the osteogenesis imperfecta market. In addition to this, the inflating utilization of effective medications, such as bisphosphonates, which help to enhance bone density and minimize the risk of fractures, is also creating a positive outlook for the market. Moreover, the widespread adoption of calcitonin and teriparatide therapies, since they are aimed at managing pain and promoting bone formation in individuals suffering from the illness, is further bolstering the market growth. Apart from this, the rising application of physical and occupational therapies on account of their various advantages, like strengthening bones, improving motor skills, and enhancing overall physical function, is acting as another significant growth-inducing factor. Additionally, the emerging popularity of innovative orthopedic devices, including intramedullary and telescopic rods, which provide support and stability to weakened bones, is also propelling the market growth. These techniques mainly assist in improving the quality of life for patients and reducing the risk of further damage. Besides this, the increasing demand for bone grafting procedures to correct deformities by repairing and rebuilding diseased or damaged bones is expected to drive the osteogenesis imperfecta market during the forecast period.

IMARC Group's new report provides an exhaustive analysis of the osteogenesis imperfecta market in the United States, EU4 (Germany, Spain, Italy, and France), United Kingdom, and Japan. This includes treatment practices, in-market, and pipeline drugs, share of individual therapies, market performance across the seven major markets, market performance of key companies and their drugs, etc. The report also provides the current and future patient pool across the seven major markets. According to the report, the United States has the largest patient pool for osteogenesis imperfecta and also represents the largest market for its treatment. Furthermore, the current treatment practice/algorithm, market drivers, challenges, opportunities, reimbursement scenario, unmet medical needs, etc., have also been provided in the report. This report is a must-read for manufacturers, investors, business strategists, researchers, consultants, and all those who have any kind of stake or are planning to foray into the osteogenesis imperfecta market in any manner.

Time Period of the Study

- Base Year: 2024

- Historical Period: 2019-2024

- Market Forecast: 2025-2035

Countries Covered

- United States

- Germany

- France

- United Kingdom

- Italy

- Spain

- Japan

Analysis Covered Across Each Country

- Historical, current, and future epidemiology scenario

- Historical, current, and future performance of the osteogenesis imperfecta market

- Historical, current, and future performance of various therapeutic categories in the market

- Sales of various drugs across the osteogenesis imperfecta market

- Reimbursement scenario in the market

- In-market and pipeline drugs

Competitive Landscape:

This report also provides a detailed analysis of the current osteogenesis imperfecta marketed drugs and late-stage pipeline drugs.

In-Market Drugs

- Drug Overview

- Mechanism of Action

- Regulatory Status

- Clinical Trial Results

- Drug Uptake and Market Performance

Late-Stage Pipeline Drugs

- Drug Overview

- Mechanism of Action

- Regulatory Status

- Clinical Trial Results

- Drug Uptake and Market Performance

| Drugs | Company Name |

|---|---|

| Setrusumab (UX143) | Ultragenyx Pharmaceutical Inc. |

| AGA2115 | Angitia Biopharmaceuticals |

*Kindly note that the drugs in the above table only represent a partial list of marketed/pipeline drugs, and the complete list has been provided in the report.

Key Questions Answered in this Report:

Market Insights

- How has the osteogenesis imperfecta market performed so far and how will it perform in the coming years?

- What are the markets shares of various therapeutic segments in 2024 and how are they expected to perform till 2035?

- What was the country-wise size of the osteogenesis imperfecta across the seven major markets in 2024 and what will it look like in 2035?

- What is the growth rate of the osteogenesis imperfecta across the seven major markets and what will be the expected growth over the next ten years?

- What are the key unmet needs in the market?

Epidemiology Insights

- What is the number of prevalent cases (2019-2035) of osteogenesis imperfecta across the seven major markets?

- What is the number of prevalent cases (2019-2035) of osteogenesis imperfecta by age across the seven major markets?

- What is the number of prevalent cases (2019-2035) of osteogenesis imperfecta by gender across the seven major markets?

- What is the number of prevalent cases (2019-2035) of osteogenesis imperfecta by type across the seven major markets?

- How many patients are diagnosed (2019-2035) with osteogenesis imperfecta across the seven major markets?

- What is the size of the osteogenesis imperfecta patient pool (2019-2024) across the seven major markets?

- What would be the forecasted patient pool (2025-2035) across the seven major markets?

- What are the key factors driving the epidemiological trend osteogenesis imperfecta of?

- What will be the growth rate of patients across the seven major markets?

Osteogenesis Imperfecta: Current Treatment Scenario, Marketed Drugs and Emerging Therapies

- What are the current marketed drugs and what are their market performance?

- What are the key pipeline drugs and how are they expected to perform in the coming years?

- How safe are the current marketed drugs and what are their efficacies?

- How safe are the late-stage pipeline drugs and what are their efficacies?

- What are the current treatment guidelines for osteogenesis imperfecta drugs across the seven major markets?

- Who are the key companies in the market and what are their market shares?

- What are the key mergers and acquisitions, licensing activities, collaborations, etc. related to the osteogenesis imperfecta market?

- What are the key regulatory events related to the osteogenesis imperfecta market?

- What is the structure of clinical trial landscape by status related to the osteogenesis imperfecta market?

- What is the structure of clinical trial landscape by phase related to the osteogenesis imperfecta market?

- What is the structure of clinical trial landscape by route of administration related to the osteogenesis imperfecta market?

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Inquire Before Buying

Inquire Before Buying

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Request Customization

Request Customization

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)