Orthodontics Market Size, Share, Trends and Forecast by Age Group, Type, End User, and Region, 2025-2033

Orthodontics Market Size and Share:

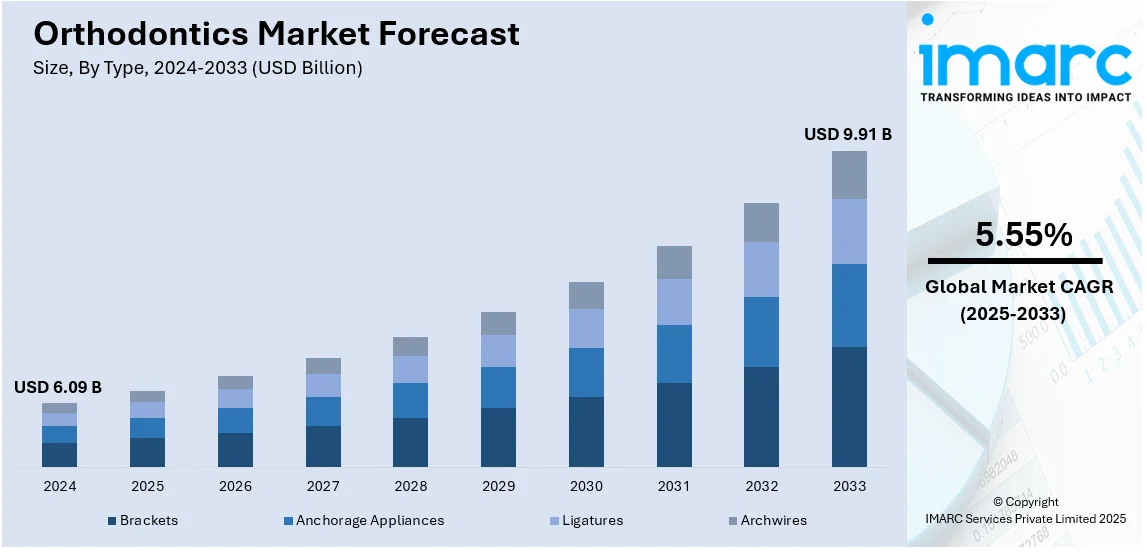

The global orthodontics market size was valued at USD 6.09 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 9.91 Billion by 2033, exhibiting a CAGR of 5.55% during 2025-2033. North America currently dominates the market, holding a significant market share of over 38.7% in 2024. The rising demand for aesthetic dental solutions, advancements in AI-driven treatment planning, increasing adoption of 3D printing in aligner production, growing geriatric population seeking corrective procedures, expanding teledentistry integration, regulatory approvals for innovative biomaterials, and the emergence of direct-to-consumer orthodontic solutions are some of the major factors augmenting orthodontics market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 6.09 Billion |

|

Market Forecast in 2033

|

USD 9.91 Billion |

| Market Growth Rate 2025-2033 | 5.55% |

The market is expanding due to increasing awareness regarding oral aesthetics and rising demand for minimally invasive treatments. Additionally, continual advancements in treatment planning are improving procedural efficiency and customization. According to industry reports, malocclusion ranks as the third most common oral disease globally, with approximately 30% of the population requiring significant orthodontic treatment. The rising prevalence of malocclusion and temporomandibular disorders is fueling demand for corrective treatments. Moreover, the development of transparent aligners with enhanced material properties is driving patient preference over conventional braces, which is providing a boost to market expansion. The emergence of direct-to-consumer orthodontic solutions is further transforming accessibility, which is positively impacting the orthodontics market outlook. Moreover, the integration of orthodontics with teledentistry is streamlining consultations and treatment monitoring, fostering market expansion.

To get more information on this market, Request Sample

The U.S. orthodontics market is experiencing growth due to inflating disposable incomes and strong consumer willingness to invest in advanced dental treatments. In addition to this, expanding insurance coverage for orthodontic procedures, including Medicaid provisions for pediatric care, is increasing accessibility. According to industry reports, it is anticipated that the number of Americans aged 65 and over would increase by 47%, from 58 million in 2022 to 82 million by 2050, and that their proportion of the total population will increase from 17% to 23%. The growing geriatric population seeking orthodontic correction for age-related dental issues is also contributing to market growth. Furthermore, orthodontic practices are benefiting from growing collaborations with dental service organizations (DSOs), which enhance operational efficiency. Also, the introduction of AI-based diagnostic tools is improving treatment accuracy and patient outcomes. Additionally, the emphasis on personalized orthodontic solutions, including custom aligners and smart braces with real-time monitoring, is further driving adoption.

Orthodontics Market Trends:

Increasing Prevalence of Musculoskeletal Disorders and Abnormalities

The rising incidence of musculoskeletal disorders, particularly those affecting the craniofacial region, is significantly propelling the orthodontics market growth. According to reports, there have been 1.68 Billion MSD cases globally, a 95% increase since 1990. While disability-adjusted life years (DALYs) and total cases have risen, global mortality declines by 0.265% annually. By 2035, MSD cases may reach 2.161 Billion, with further increases in DALYs and deaths projected. Conditions such as temporomandibular joint (TMJ) disorders, malocclusions, cleft palate, and facial asymmetry are increasing due to genetic factors, poor oral habits, and lifestyle changes. In addition to this, misaligned teeth and jaw discrepancies often require orthodontic intervention to prevent complications like speech difficulties, chewing inefficiencies, and chronic pain. Furthermore, digital diagnostics and 3D imaging improve the early detection of musculoskeletal abnormalities, prompting orthodontists to recommend corrective measures at a younger age. The expansion of insurance coverage and government initiatives for congenital deformity treatments, such as cleft lip and palate surgeries, further boost demand for orthodontic solutions.

Growing Geriatric Population

The aging population is fueling orthodontic market demand as elderly individuals increasingly seek solutions for age-related dental issues. According to industry reports, the global population aged 65 and older is expected to double in the next 30 years. Currently, there are approximately 830 Million people in this age group, and UN projections estimate it will reach 1.7 Billion by 2054. Therefore, there is an increased requirement for orthodontics treatments. Tooth loss, gum recession, and bite misalignment are prevalent concerns among older adults, often leading to functional and aesthetic challenges. As life expectancy rises, more seniors are prioritizing oral health, contributing to the expansion of adult orthodontics. Traditional orthodontic treatments were once associated primarily with adolescents, but modern advancements, such as discreet aligners and lingual braces, have made them more appealing to older patients. Additionally, the demand for minimally invasive and shorter-duration treatments is prompting innovations in clear aligners and accelerated orthodontic techniques. Furthermore, improved awareness about oral-systemic health links is driving older individuals to seek orthodontic care.

Adoption of Digital Orthodontics and AI Integration

The integration of digital orthodontics is a merging orthodontics market trend, and it is revolutionizing treatment planning, diagnosis, and patient monitoring. Artificial intelligence (AI) and 3D printing technologies are playing a crucial role in improving efficiency, accuracy, and patient outcomes. AI-powered software can analyze orthodontic scans and predict treatment progress, allowing for precise customization of braces and aligners. Remote monitoring solutions, such as AI-based mobile applications, are enhancing patient compliance by allowing orthodontists to track progress without frequent in-office visits. These technologies enable early intervention in case of treatment deviations, reducing the risk of prolonged therapy. The continuous advancement in AI and digital tools is streamlining workflows and improving patient satisfaction. On February 24, 2025, Dror Ortho-Design, Inc. orthodontic platform company based on AI, declared the successful conclusion of its ZSmile platform's user experience trials, which evaluated the platform's usability among patients, orthodontists, and dental professionals in authentic operational environments. The company has integrated feedback from these trials and is finalizing regulatory processes to commence manufacturing and distribution in Israel in the first half of 2025.

Orthodontics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global orthodontics market, along with forecasts at the global, regional, and country levels from 2025-2033. The market has been categorized based on age group, type, and end user.

Analysis by Age Group:

- Adults

- Children

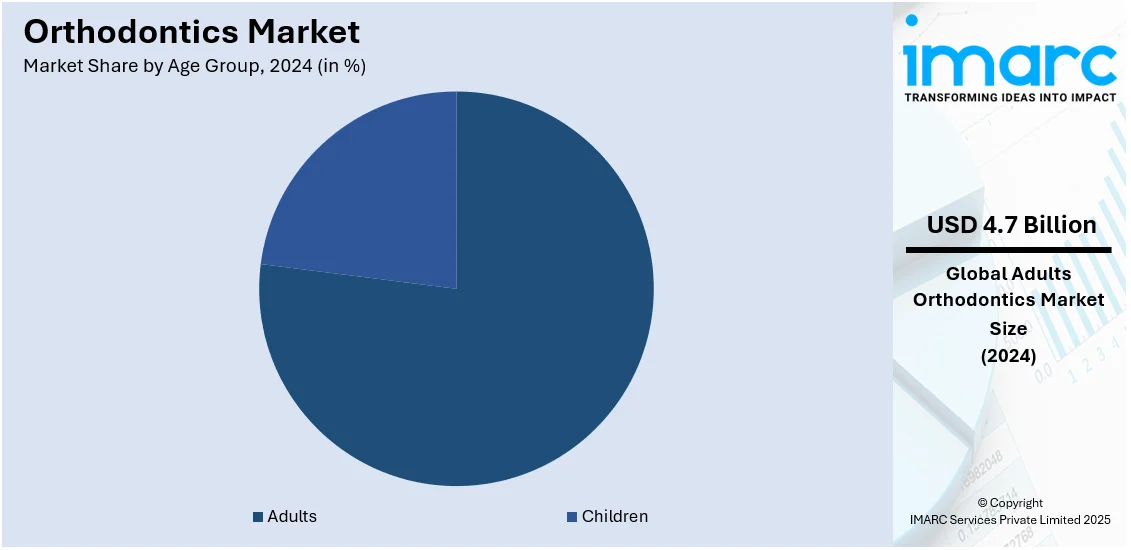

Adults lead the market with around 76.9% of market share in 2024 fueled by growing awareness of dental appearance, innovations in inconspicuous orthodontic treatment, and improved affordability of treatment. Clear aligners, lingual braces, and ceramic braces are in high demand as adults look for solutions that complement their professional and social lives. Continual advances in technology, including AI-based treatment planning and 3D-printed aligners, further increase accessibility and effectiveness. In addition to this, extended dental cover, flexible dental financing, and increased emphasis on oral health augment market growth. The prevalence of malocclusion, bite aberrations, and age-related dental shifts also result in significant requirements, which is especially predominant among middle-aged adults who have corrective procedures necessitated. As orthodontic treatments become more customized to adults, this age group is likely to remain driving market trends, shaping product offerings, and increasing the patient population beyond teenage group.

Analysis by Type:

- Brackets

- Fixed Brackets

- Removable Brackets

- Anchorage Appliances

- Bands and Buccal Tubes

- Miniscrews

- Ligatures

- Elastomeric Ligatures

- Wire Ligatures

- Archwires

Brackets lead the market with around 36.9% of market share in 2024. Brackets are a core element of fixed braces utilized in the treatment of misalignments, malocclusions, and bite problems. Orthodontic metal brackets continue to be used broadly due to their long life, cost, and efficacy in solving difficult cases. The demand for ceramic, lingual, and self-ligating brackets increased due to esthetic considerations, though they provide more invisible and less bothersome treatment options. The emergence of digital orthodontics, such as 3D printing and artificial intelligence based on treatment planning, increased the accuracy and specificity of the treatments involving orthodontic metal brackets, raising patient satisfaction levels. Technologies like heat-activated archwires and friction-lowering bracket shapes further maximize efficiency by lowering the time of treatment and discomfort. Brackets are essential in extreme orthodontic treatments, which guarantee their ongoing position in the marketplace. Their flexibility among patient demographics and changing technical innovations cement their place in orthodontic treatments.

Analysis by End User:

- Hospitals

- Dental Clinics

- Others

Hospitals play a significant part in the market for orthodontics by delivering specialized dental care, especially to complex orthodontic cases necessitating multidisciplinary treatment. With sophisticated diagnostic equipment, hospitals treat severe malocclusions, jaw misalignment, and surgical orthodontics. Hospitals also treat patients with underlying medical issues that need coordinated dental care. The availability of orthodontic departments in large hospitals increases the accessibility of quality treatment, especially in urban areas. Secondly, hospitals promote research and development (R&D) activities on orthodontic technology that lead to innovation in treatment approaches. As the focus increases on overall dental care, hospitals remain important end users for the orthodontics industry, providing updated solutions for functional as well as cosmetic orthodontic requirements.

Dental clinics are the key end users within the orthodontics industry, serving a vast majority of patients requiring corrective dental procedures. These clinics provide an array of orthodontic treatments, from traditional braces to clear aligners and lingual braces, customized to individual requirements. Convenient, affordable, and individualized care by dental clinics over hospital care is preferred by patients. Technological incorporation in the form of 3D imaging and AI-driven planning of treatment further enhances efficiency and precision in orthodontic treatment in clinics. Moreover, the growing number of orthodontic specialist clinics has increased market accessibility and made treatments more available. As demand for beauty and minimally invasive orthodontics continues to grow, dental clinics remain top suppliers, informing market trends and driving innovation in patient management.

Regional Analysis:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024, North America accounted for the largest market share of over 38.7%, driven by the strong presence of market players, highly advanced healthcare facilities, and superior awareness among customers. The access to orthodontic treatments is common across North America, based on widespread availability and complete insurance covers from dental health plans along with greater embracement of easy payment schedules. The growth in orthodontic procedures is propelled by both functional and aesthetic reasons, with the increasing popularity of clear aligners, self-ligating brackets, and lingual braces. Continual advances in technology, including AI-based treatment planning, 3D-printed orthodontic appliances, and teledentistry software, also drive patient convenience and treatment accuracy. The availability of top orthodontic companies and ongoing product advancements support market growth. Also, the expanding adult orthodontic market, coupled with a growing emphasis on pediatric orthodontics, provides an impetus to the market. North America is likely to dominate the global market, accelerating industry trends, shaping product innovation and treatment practices.

Key Regional Takeaways:

United States Orthodontics Market Analysis

The United States holds a substantial share of the North America orthodontics market with 90.50% in 2024.The market in the U.S is expanding due to increasing demand for dental aesthetics, technological advancements, and improved access to treatment. As per the American Association of Orthodontists, around four Million people in the U.S. are currently undergoing orthodontic treatment. Similarly, the rising popularity of clear aligners, driven by patient preference for discreet treatment options, is fueling market growth. Companies and competitors are developing AI-powered treatment planning tools, enhancing treatment accuracy and efficiency. Traditional braces remain widely used, especially for complex cases, with self-ligating brackets and lingual braces improving patient comfort. Furthermore, the expansion of orthodontic insurance coverage, making treatment more affordable, is propelling the market growth. The rise of direct-to-consumer (DTC) orthodontic solutions introducing cost-effective alternatives and raising regulatory concerns due to limited professional oversight is impelling the market. Besides this, increasing investment in digital dentistry, including 3D printing for custom appliances, is further transforming treatment delivery. For instance, in September 2024, Carestream Dental secured USD 525 Million in investment, led by GA Credit’s Atlantic Park Fund, to reduce debt and accelerate innovation. The company launched the Oral Healthcare Innovation Hub (OHIH) and plans to unveil Oral Healthcare Practice 2040 at IDS 2025 in Cologne, Germany.

Europe Orthodontics Market Analysis

Europe’s market is witnessing growth, attributed to a strong focus on preventive care, government-backed initiatives, and advancements in orthodontic technologies. Countries like Germany, France, and the UK have well-developed orthodontic systems, with national health programs partially covering children’s treatments. Similarly, the demand for aesthetic orthodontic solutions, such as clear aligners and ceramic braces, is rising among adults and teenagers. The integration of AI and digital scanning is streamlining treatment planning, reducing chair time and improving precision. Orthodontic startups focusing on remote monitoring and digital treatment solutions are reshaping the market. To illustrate, in November 2024, Barcelona-based startup Impress secured EUR 110 Million to expand its digital orthodontic services across Europe. The funding, led by Trinity Capital Inc., CareCapital, LBO France, and TA Ventures, will support new clinic openings and market expansion. Following its DrSmile acquisition, Impress plans to open 20+ flagship clinics by 2025, reinforcing its D2C aligner model and health tech leadership. Rising orthodontic costs drive dental tourism to Eastern Europe for affordable, quality care. Moreover, rising biodegradable aligners and eco-friendly packaging as regulations promote greener practices, are impelling the market. The growing emphasis on digital dentistry and sustainability is shaping the market landscape.

Asia Pacific Orthodontics Market Analysis

The Asia Pacific orthodontics market is growing rapidly due to rising disposable incomes, increasing awareness of dental aesthetics, and access to advanced treatments. China’s per capita disposable income reached 11,539 yuan (USD 1,624.57) in Q1 2024, up 6.2% year-on-year, with urban income at 15,150 yuan (+5.3%) and rural income at 6,596 yuan (+7.6%), as per National Bureau of Statistics. Additionally, the region leads in traditional and modern orthodontic solutions, with clear aligners gaining popularity, especially among younger populations seeking aesthetic, non-invasive treatments. Furthermore, supportive government-led initiatives in India and Indonesia are expanding orthodontic access through public health programs. Social media and cosmetic trends are also driving demand, particularly among millennials and Gen Z. Moreover, continual technological advancements, such as intraoral scanners and AI-driven treatment planning are improving treatment efficiency. Teleorthodontics is increasing accessibility in rural areas, while local manufacturers offer affordable alternatives, intensifying competition with premium global brands.

Latin America Orthodontics Market Analysis

The Latin America market is bolstering as demand for dental misalignment treatments increases, driven by greater awareness and economic improvements. Brazil and Mexico lead in orthodontic adoption, particularly among younger populations. Furthermore, financing options and payment plans render treatments more accessible, augmenting clear aligner and braces adoption. Dental tourism is also a key driver, with Colombia and Costa Rica offering high-quality, affordable care. As per an industry report, in Colombia, dental implants cost USD 1,000–USD 2,500 per implant, compared to USD 3,000–USD 6,000 in the U.S. Moreover, digital orthodontics advancements, including 3D printing for custom aligners and brackets, are augmenting market demand. Public health initiatives promote early orthodontic screening, supporting market growth. However, economic instability and healthcare disparities limit expansion in rural and underserved areas.

Middle East and Africa Orthodontics Market Analysis

The Middle East and Africa orthodontics market is expanding given the rising disposable income, growing medical tourism, and increasing demand for cosmetic dentistry. Furthermore, gulf countries, including the UAE and Saudi Arabia, are investing in advanced orthodontic technologies, making clear aligners and lingual braces more accessible. King Faisal Specialist Hospital & Research Centre (KFSHRC) showcased its AI-powered diagnostics, robotic surgeries, and telemedicine at Arab Health 2025, attracting 46,476 new patients in 2024, with medical tourism rising 47.39%. The 2,443-bed hospital has performed 5K+ bone marrow, 4K+ organ transplants, and 3K+ robotic procedures. Additionally, high-income consumers are increasingly opting for digital orthodontics and AI-driven treatment planning, thereby positively influencing the market outlook. Apart from this, orthodontic care in Africa is urban-centered, but teleorthodontics and social media drive rural access and demand.

Competitive Landscape:

The orthodontic market is marked by intense competition, propelled by advancements in technology, heightened demand for cosmetic dental procedures, and the amplified incidence of malocclusion cases. Businesses are investing in digital orthodontics, 3D printing, and AI-based treatment planning to increase accuracy and productivity. Clear aligners are gaining popularity quickly, pitted against conventional braces because of their convenience and stealthy appearance. Market participants are diversifying their portfolios with new products, such as self-ligating brackets and lingual braces, to meet the varied needs of patients. Strategic alliances with dental clinics and direct-to-consumer models are transforming distribution channels. Regulatory clearances and reimbursement policies also determine market entry and expansion strategies. The increasing adoption of teledentistry is also further escalating competition, enabling remote consultations and monitoring of treatment. Also, some of the major factors impacting market dynamics include price competition, brand positioning, and clinician preference.

The report provides a comprehensive analysis of the competitive landscape in the orthodontics market with detailed profiles of all major companies, including:

- Align Technology Inc.

- American Orthodontics

- DB Orthodontics Limited

- DENTAURUM GmbH & Co. KG

- Dentsply Sirona

- G&H Orthodontics

- KLOwen

- Planmeca Oy

- Rocky Mountain Orthodontics

- TP Orthodontics Inc.

Latest News and Developments:

- November 2024: Align Technology received CE Mark approval for its Invisalign Palatal Expander System in Europe and MHRA registration in the UK. This 3D-printed, removable device offers a modern alternative to traditional expanders, supporting early orthodontic treatment for children, teens, and adults, with EMEA availability expected in Q1 2025.

- October 2024: Nasser Orthodontics will merge with Cosse & Silmon Orthodontics on expanding services across six Louisiana locations. The combined practice will offer braces, clear aligners, and advanced 3D scanning technology, including Aligners in an Hour, enhancing patient care, affordability, and treatment precision.

- August 2024: G&H Orthodontics updated its Tune Clear Aligner System with SmileStudio 1.1, enhancing tooth movement predictability, treatment visualization, and customization. The FDA-approved system ensures affordable, high-quality treatment, leveraging Zendura FLX for optimal aligner forces. Each case is doctor-reviewed, improving treatment efficiency and patient comfort.

- May 2024: DentalMonitoring received De Novo FDA approval for its AI-powered remote orthodontic monitoring software, the first AI/ML-enabled Software as a Medical Device in dentistry. It enhances treatment tracking, patient compliance, and clinician insights, introducing SmartSTL for remote STL file updates, and setting a new standard in orthodontic care.

- May 2024: Henry Schein Orthodontics is showcasing its latest aligner solutions, bite correction technology, and treatment planning software at the AAO Meeting in New Orleans. Booth #2719 features in-booth education, product demos, and expert-led sessions on Carriere Motion appliances, NemoStudio software, and advanced orthodontic treatment solutions.

Orthodontics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Age Groups Covered | Adults, Childres |

| Types Covered |

|

| End Users Covered | Hospitals, Dental Clinics, Others |

| Regions Covered | North America, Asia Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Align Technology Inc., American Orthodontics, DB Orthodontics Limited, DENTAURUM GmbH & Co. KG, Dentsply Sirona, G&H Orthodontics, KLOwen, Planmeca Oy, Rocky Mountain Orthodontics, TP Orthodontics Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the orthodontics market from 2019-2033.

- The orthodontics market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the orthodontics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The orthodontics market was valued at USD 6.09 Billion in 2024.

The orthodontics market is projected to exhibit a CAGR of 5.55% during 2025-2033, reaching a value of USD 9.91 Billion by 2033.

The market is driven by the increasing prevalence of malocclusion, rising demand for aesthetic dental treatments, technological advancements in clear aligners and 3D printing, and expanding dental insurance coverage. Growing awareness of oral health, rising disposable income, and the increasing adoption of digital orthodontics also contribute to market expansion.

North America currently dominates the orthodontics market, accounting for a share of 38.7% in 2024. The dominance is fueled by high orthodontic treatment adoption, strong healthcare infrastructure, widespread insurance coverage, and the presence of key industry players. Increasing demand for clear aligners and advanced digital orthodontic solutions further supports the market growth.

Some of the major players in the orthodontics market include Align Technology Inc., American Orthodontics, DB Orthodontics Limited, DENTAURUM GmbH & Co. KG, Dentsply Sirona, G&H Orthodontics, KLOwen, Planmeca Oy, Rocky Mountain Orthodontics and TP Orthodontics Inc., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)