North America Wheat Flour Market Size, Share, Trends and Forecast by Type, End-Use, Distribution Channel, and Country, 2026-2034

North America Wheat Flour Market Size and Share:

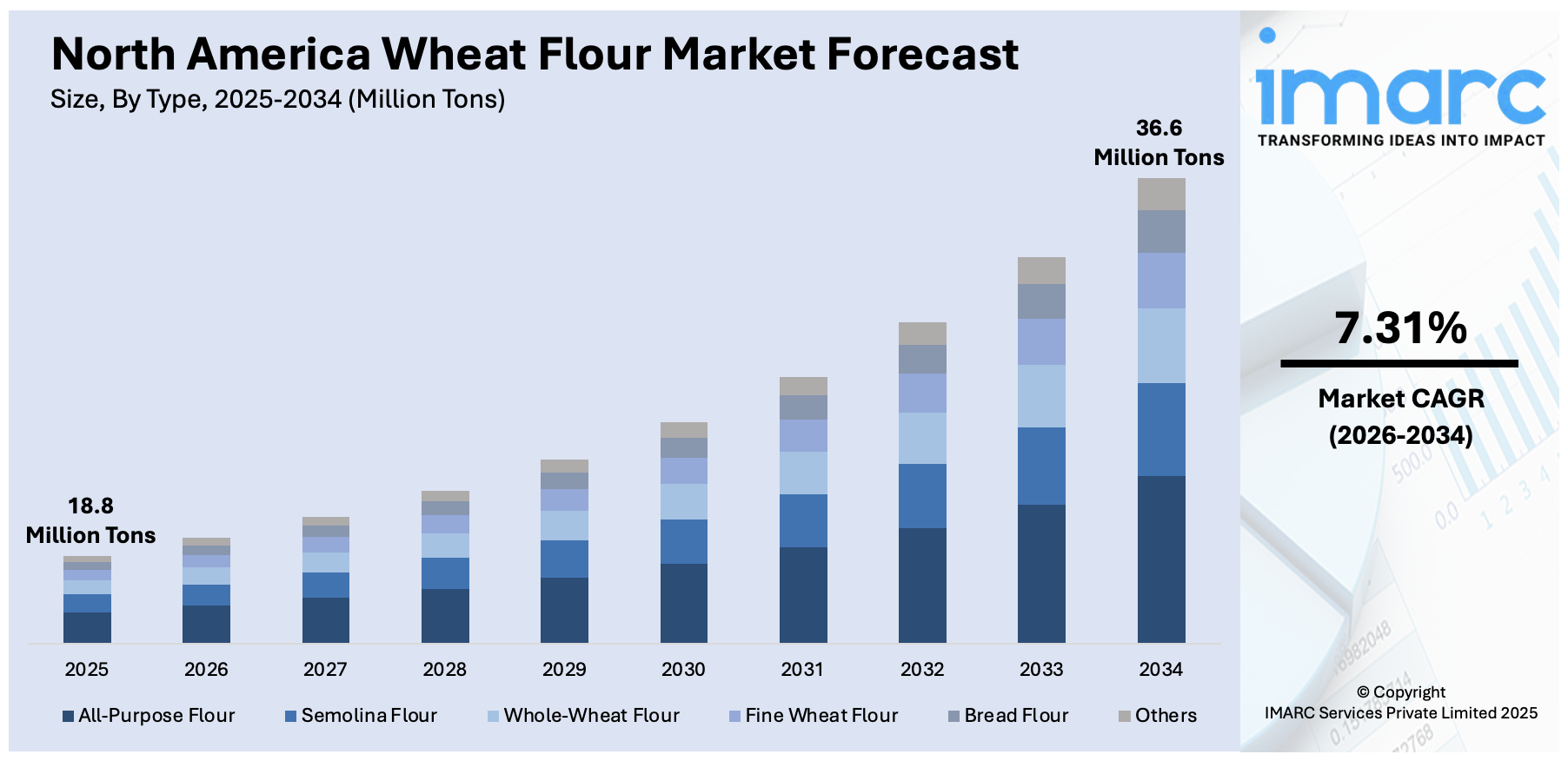

The North America wheat flour market size reached 18.8 Million Tons in 2025. Looking forward, IMARC Group estimates the market to reach 36.6 Million Tons by 2034, exhibiting a CAGR of 7.31% from 2026-2034. The market is driven by the growth in health-conscious consumer preferences for whole wheat and fortified flours, heightened demand for sustainable milling practices like regenerative agriculture, and the rise in e-commerce, offering convenience, niche products, and personalized experiences for specialty flours.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

18.8 Million Tons |

|

Market Forecast in 2034

|

36.6 Million Tons |

| Market Growth Rate (2026-2034) | 7.31% |

The market in North America is seeing notable expansion attributed to the heightened demand for processed and convenience foods. In line with this, fast-paced lifestyles are driving consumers to prefer to ready-to-cook and easy-to-prepare meals, which rely heavily on wheat flour, particularly in bakery products, snacks, and pasta. Arya International's June 2024 launch of Whole Wheat Rotis at Whole Foods Market exemplifies this trend, offering a plant-based, clean-label alternative made with whole wheat flour and avocado oil. Furthermore, the rise of online grocery shopping, improving access to artisanal and health-focused wheat flour products, such as organic and whole wheat options is expanding the North America wheat flour market share. Moreover, the growing foodservice sector, including restaurants and fast-food chains, contributes to the market's expansion, with wheat flour being a major ingredient in a broad range of menu offerings.

To get more information on this market Request Sample

In addition to this, the increasing awareness of wheat flour's nutritional benefits is a key factor driving market growth. Customers are becoming more health-conscious, resulting in growth in demand for whole wheat flour, known for its higher fiber content and lower glycemic index compared to refined flour. Alongside this, the heightened popularity of gluten-free and alternative flours is strengthening the North America wheat flour market demand, with manufacturers offering wheat flour variants enriched with vitamins, minerals, and proteins to meet diverse dietary preferences. Notably, on October 21, 2024, Nature's Path, a Canadian brand, launched its organic flour line in the U.S. The line includes products like Organic All-Purpose Flour, Whole Wheat Flour, and Gluten-Free All-Purpose Flour, all made with non-GMO, responsibly sourced ingredients. These products are available in U.S. stores and online, aligning with consumer demands for healthier, functional food options.

North America Wheat Flour Market Trends:

Rise of Health-Conscious Consumer Preferences

One of the notable North America weat flour market rends is the ongoing shift toward health-conscious consumer preferences. With a heightened focus on balanced diets, consumers are increasingly opting for whole wheat, organic, and enriched flours, which offer superior nutritional benefits compared to refined flour. The growing demand for whole wheat flour, known for its higher fiber content and lower glycemic index, is on the rise as it is perceived as a healthier alternative. According to the USDA's National Agricultural Statistics Service (NASS), U.S. whole wheat flour production grew by 4.1% in the first quarter of 2024, reaching 4,686,000 cwts, with its share of total flour production rising to 4.4%. Additionally, fortified flours rich in vitamins, minerals, and proteins are gaining popularity, prompting manufacturers to emphasize clean, nutritious ingredients to cater to health-conscious consumers.

Innovation in Sustainable and Eco-Friendly Milling Practices

Sustainability is an emerging priority contributing to the North America wheat flour market growth as consumers become more conscious of food production’s environmental impact. In response, manufacturers are adopting eco-friendly practices, including sustainable milling methods and energy-efficient processes. For instance, on June 18, 2024, Ahold Delhaize USA, Kellanova, and Bartlett launched a regenerative agriculture pilot in North Carolina to reduce Scope 3 emissions from wheat farming, supporting the production of Cheez-It® and Club® crackers. This initiative highlights a shift toward sourcing organic, non-GMO grains and utilizing low-temperature, stone milling techniques to preserve nutritional quality. Additionally, eco-friendly packaging and carbon footprint reduction are integral to many companies' sustainability strategies. As these efforts align with growing consumer demand, new wheat flour products are emerging that meet higher environmental standards.

Growth of E-Commerce and Direct-to-Consumer Sales

Another significant trend in the industry is the rise in e-commerce and direct-to-consumer sales channels. According to the FMI and NielsenIQ Digital Engagement Transforms Grocery Shopping report published on February 3, 2025, over 90% of shoppers now shop both online and in-store, with U.S. online grocery sales projected to hit USD 388 Billion by 2027. This growth is driving the demand for specialty wheat flours such as organic, gluten-free, and high-protein varieties, which are increasingly purchased through digital platforms. As per the North America wheat flour market forecast report, e-commerce offers consumers convenience, greater product variety, and access to niche products not always available in physical stores. Flour brands are responding by enhancing their online presence, offering subscription models, and providing detailed product information, thus transforming the distribution landscape and offering a more personalized shopping experience.

North America Wheat Flour Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the North America wheat flour market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on type, end-use, and distribution channel.

Analysis by Type:

- All-Purpose Flour

- Semolina Flour

- Whole-Wheat Flour

- Fine Wheat Flour

- Bread Flour

- Others

Bread flour is dominating the market in 2025 due to its essential role in producing high-quality, consistent bread products. Bread flour, that has a greater amount of proteins, is extremely in demand attributed to its higher dough elasticity along with the resultant improvement in texture. The present-day consumer, with a keen sense of a penchant for handmade, homemade bread and health consciousness, is influencing the North America wheat flour market outlook. Additionally, its versatility in various bread types makes it a staple in both commercial and home kitchens.

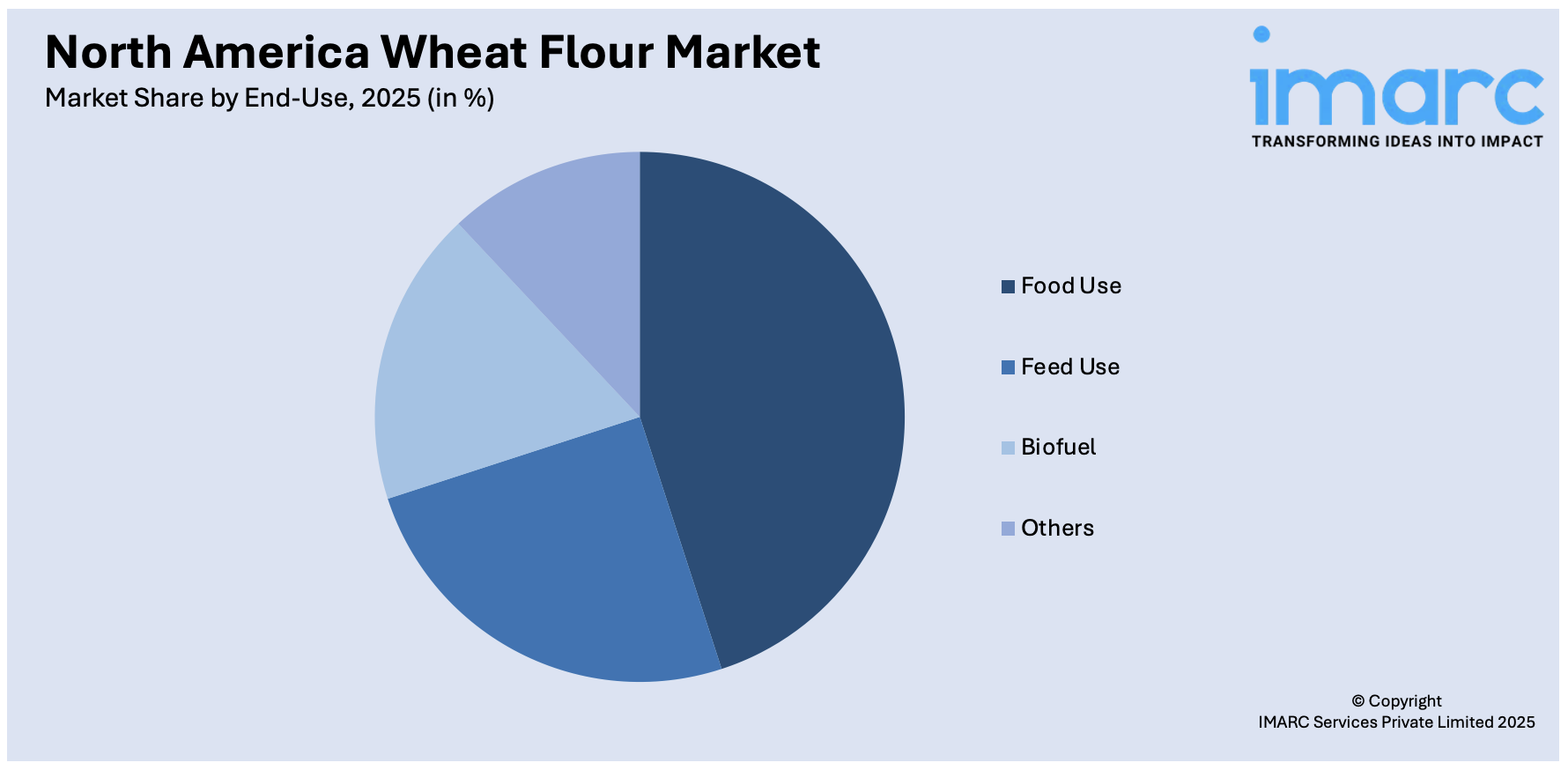

Analysis by End-Use:

Access the comprehensive market breakdown Request Sample

- Food Use

- Feed Use

- Biofuel

- Others

Food use leads the market share in 2025 attributed to its essential role in the production of a wide variety of food products. Wheat flour is a key ingredient in bread, pastries, snacks, and baked goods, which remain consumer staples. As demand for convenience foods and healthier alternatives grows, wheat flour’s versatility in recipes, especially in whole wheat, organic, and high-protein variants, further bolsters its market share. Moreover, increasing consumer awareness of nutrition and the shift toward cleaner labels is fueling innovation in flour products, keeping wheat flour at the forefront of food manufacturing and home baking.

Analysis by Distribution Channel:

- Supermarkets and Hypermarkets

- Independent Retailers

- Convenience Stores

- Specialty Stores

- Online Stores

- Others

Supermarkets and hypermarkets represent the highest market share in 2025 driven by their extensive reach and ability to provide a wide range of flour products under one roof. These retail formats meet different consumer requirements by providing bulk and specialty flours, organic, gluten-free, and high-protein types. The advantage of supermarkets and hypermarkets lies in their convenience, competitive pricing, and frequent promotions, which makes them the preferred choice for consumers. Apart from this, the established supply chain and strategic location of these retailers ensure consistent availability of wheat flour to cater to the growing demand from both consumers and commercial bakeries across the region.

Country Analysis:

- United States

- Canada

- Mexico

In 2025, the United States accounted for the majority share in the market propelled by the region’s large-scale wheat production and advanced milling infrastructure. The U.S. has a highly developed agricultural sector, with extensive wheat cultivation across key states like Kansas, North Dakota, and Montana. The country's well-established supply chain, modern milling technology, and high production capacity contribute to a steady and efficient flour output. Additionally, the growing demand for wheat flour in both food processing and export markets, along with strong consumer preferences for convenience and variety, supports the U.S.'s dominance in the region’s flour market.

Competitive Landscape:

The competitive nature of the North America wheat flour market is given by industry players focusing on innovations, sustainability, and strategic investment. For instance, Ardent Mills, which is one of the key leaders, announced, on August 27, 2024, an expansion in its Commerce City, Colorado, mill to further increase its capacity for wheat flour production. Expansion is to renew equipment and better efficiency, growing demand. Companies are also making healthy flour varieties investments such as gluten-free and high protein versions which meet consumer needs for clean and healthy ingredients. Furthermore, consumers' need for sustainability, the companies adopt renewable sources in energy efficient milling as well as using environment friendly package designs. E-commerce continues to unlock small scale markets; as such the companies have stepped up the level of competition within this sector.

The report provides a comprehensive analysis of the competitive landscape in the North America wheat flour market with detailed profiles of all major companies.

Latest News and Developments:

- July 11, 2024: Protein Industries Canada launched a USD 4.5 Million partnership with Ground Truth Agriculture, Parametrics.Ag, Cas-Grain Farms, and C-Merak Innovations to develop AI technology for in-field grain quality prediction. This project aims to improve wheat and protein crop consistency, benefiting farmers, wheat flour manufacturers, and food processors by enhancing crop quality and streamlining supply chains.

- May 20, 2024: Sunrise Flour Mill partnered with Cead Farms to ensure a sustainable supply of premium organic heritage wheat. This collaboration supports Sunrise's commitment to organic, regenerative farming practices and provides nutrient-rich, digestible wheat products. The partnership guarantees a reliable wheat source to meet growing demand, benefiting consumers seeking healthy, sustainable baking ingredients.

- April 23, 2024: King Arthur Baking Co. launched its Regeneratively-Grown Climate Blend Flour, a higher-fiber wheat flour developed in collaboration with Washington State University’s Breadlab. The flour, using perennial wheat, supports regenerative farming practices by reducing tilling, improving soil health, and offering 4 grams of fiber per ¼-cup serving, surpassing the original whole-wheat flour.

- April 10, 2024: King Milling Co. built a new "D" mill, designed to grind hard wheat into hard wheat flour. The combined flour capacity now rises to 24,500 cwts per day. King Milling operates different types of mills that process soft red, soft white, hard red winter, and hard red spring wheat to produce white flour, whole wheat flour, and wheat bran.

North America Wheat Flour Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | All-Purpose Flour, Semolina Flour, Whole-Wheat Flour, Fine Wheat Flour, Bread Flour, Others |

| End Uses Covered | Food Use, Feed Use, Biofuel, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Independent Retailers, Convenience Stores, Specialty Stores, Online Stores, Others |

| Countries Covered | United States, Canada, Mexico |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the North America wheat flour market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the North America wheat flour market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the North America wheat flour industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The North America wheat flour market size reached 18.8 Million Tons in 2025.

The growth of the market is majorly driven by increased consumer demand for health-conscious, whole wheat, and fortified flours, sustainable milling practices, the rise of e-commerce, and the growing foodservice sector. Additionally, innovations in gluten-free and high-protein flours are augmenting market expansion.

The North America wheat flour market is expected to reach 36.6 Million Tons by 2034, growing at a CAGR of 7.31% from 2026-2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)