North America Vascular Stents Market Size, Share, Trends and Forecast by Product Type, Material, Mode of Delivery, End-User, and Country, 2025-2033

North America Vascular Stents Market Size and Share:

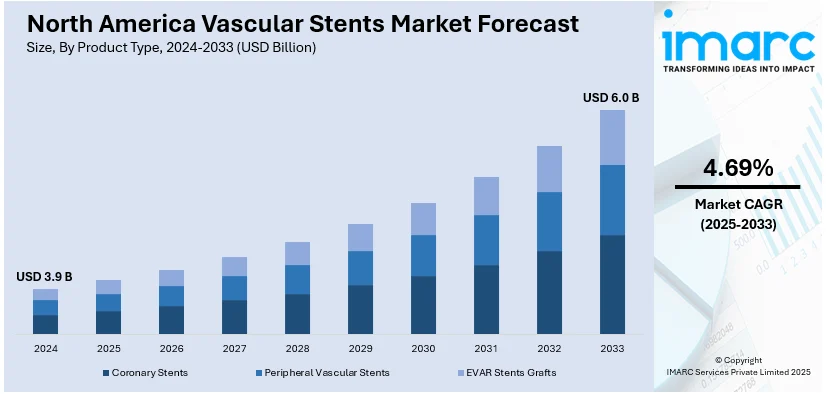

The North America vascular stents market size was valued at USD 3.9 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 6.0 Billion by 2033, exhibiting a CAGR of 4.69% from 2025-2033. The United States leads the vascular stents market, driven by an increasing aging population, rising cardiovascular diseases, ongoing technological advancements, increased healthcare investments, and a strong healthcare infrastructure.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 3.9 Billion |

|

Market Forecast in 2033

|

USD 6.0 Billion |

| Market Growth Rate (2025-2033) | 4.69% |

The North America vascular stents market demand is primarily fueled by the increasing prevalence of cardiovascular diseases, such as coronary artery disease (CAD), which affects approximately 1 in 20 adults aged 20 and older (around 5%). This increase in CAD cases is due to factors such as an aging population, sedentary lifestyles, and poor dietary habits. Additionally, the growing preference for minimally invasive procedures and ongoing advancements in stent technology, such as drug-eluting and bioresorbable stents, are driving market expansion. Furthermore, improvements in healthcare infrastructure, increased awareness of the benefits of stent placement, and the rising adoption of these procedures in both hospitals and outpatient settings are further contributing to market growth.

At the same time, government initiatives and increased healthcare investments are playing a key role in driving the North America vascular stents market growth. The United States, in particular, has experienced a surge in the demand for vascular stents due to improved reimbursement policies and rising consumer awareness regarding preventive healthcare. For instance, heart attacks remain undetected in 1 out of 5 patients since the damage occurs without any awareness from the victim, highlighting the importance of early detection. The shift toward patient-centric care and the integration of digital technologies, such as telemedicine and artificial intelligence (AI)-driven diagnostics, is driving the adoption of innovative stent technologies, providing an impetus to the market. Moreover, the presence of top medical device manufacturers and research institutions in the region promotes ongoing innovation and guarantees a consistent supply of advanced vascular stents, further propelling market growth.

North America Vascular Stents Market Trends:

Rising Adoption of Drug-Eluting Stents (DES)

The growing market demand for drug-eluting stents (DES) in the region is influencing the North America vascular stents market trends, as they demonstrate superior performance in minimizing restenosis compared to bare-metal stents. The medical coating on these stents blocks blood vessel re-narrowing which provides extended benefits to coronary artery disease patients. Moreover, the rising preference for DES emerges from better materials development safer profiles, and enhanced clinical results. For instance, research study between EES stents (everolimus-eluting stents) and BES stents (biolimus-eluting stents) showed similar results for device-oriented composite events (DOCE) and patient-oriented composite events (POCE) throughout the 10-year period with equal long-term effectiveness. Furthermore, healthcare providers are increasingly adopting DES as cardiovascular disease rates increase because this interventional therapy gives better treatment outcomes, thus catalyzing the market growth.

Growth of Bioresorbable Stents (BRS)

The growth of bioresorbable stents (BRS) in the region is expanding the North America vascular stents market share, as these devices have the ability to dissolve gradually. These stents provide the benefit of eliminating long-term metal implants so they might reduce the complications that traditional stents present. For example, in 2024, the Food and Drug Administration (FDA) gave its approval to Abbott Medical for the Esprit™ BTK Everolimus Eluting Resorbable Scaffold System. The device provides bioresorbable treatment for infrapopliteal arterial disease to peripheral artery disease patients while strengthening BRS technology adoption within this region. The latest technological progress has enabled BRS to effectively treat coronary artery disease while offering medical professionals an interim solution for vessel natural healing. Apart from this, patients choose natural and reversible procedures and clinical proof demonstrates their safety and effectiveness, which is significantly enhancing the North America vascular stents market outlook.

Integration of Advanced Imaging Technologies

The incorporation of advanced imaging technologies, like intravascular ultrasound (IVUS) and optical coherence tomography (OCT), into stent implantation procedures is greatly enhancing the accuracy and success rates of vascular stent placements. These technologies allow clinicians to better assess the vessel and accurately position the stent, reducing complications and improving patient recovery. Reports indicate that OCT-guided percutaneous coronary intervention (PCI) is linked to lower rates of cardiac death and stent thrombosis compared to traditional angiography-guided PCI. Besides this, the increasing use of these imaging modalities is enhancing procedural efficiency, supporting more personalized treatment approaches, and leading to better long-term results. Additionally, the rising adoption of more sophisticated tools in healthcare systems is thereby strengthening the market share.

North America Vascular Stents Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the North America vascular stents market, along with forecasts at the regional and country levels from 2025-2033. The market has been categorized based on product type, material, mode of delivery, and end-user.

Analysis by Product Type:

- Coronary Stents

- Peripheral Vascular Stents

- EVAR Stents Grafts

Coronary stents lead the North America vascular stents market because of their essential role in treating coronary artery disease (CAD), a major cause of death in the region. The elevated frequency of CAD among patients results from population aging along with deteriorating lifestyle patterns and expanding obesity statistics and this drives the need for coronary stents. Medical technologies especially DES have advanced treatment results through their ability to minimize restenosis risks and enhance sustained patient health. Concurrently, the rising demand for minimally invasive procedures that offer shortened recovery periods and fewer complications has driven the increase in coronary stent procedures. Also, better healthcare infrastructure and positive reimbursement policies in the United States market have enhanced the accessibility of coronary stents for patients. As a result, the combination of these factors with a greater public understanding of heart health makes coronary stents maintain their market leadership position in North America.

Analysis by Material:

- Metallic Stents

- Cobalt Chromium

- Platinum Chromium

- Nickel Titanium

- Stainless Steel

- Others

The North America vascular stents market is primarily driven by metallic stents made from materials such as cobalt chromium, platinum chromium, nickel titanium, and stainless steel, owing to their strength, flexibility, and durability. Medical procedures benefit from cobalt chromium and platinum chromium stents because these materials possess enhanced visibility due to their high radiopacity and stronger mechanical properties that minimize the risk of fracture. Moreover, nickel titanium maintains its shape memory abilities which produce flexible and adaptable properties suitable for treating complicated vascular structures. Furthermore, medical professionals continue to choose stainless steel for its economic value and dependable operation characteristics. Apart from this, the success of metallic stents persists because healthcare providers widely accept them due to their clinical effectiveness and low cost and their proven performance throughout history. The market expansion also stems from recent technological improvements in metallic stent material composition which improves both patient outcome results and decreases procedural complications. The market maintains metallic stents as its dominant player through these factors.

Analysis by Mode of Delivery:

- Balloon-Expandable Stents

- Self-Expanding Stents

Balloon-expandable stents hold the largest share of the North America vascular stents market due to their proven efficacy in treating coronary artery disease and their widespread use in clinical practice. The balloon-expandable stents allow medical professionals to perform precise placement and achieve optimal expansion within the artery for better vessel patency by using balloon catheters. The combination of simple operation and proven restenosis prevention together with universal patient compatibility makes balloon-expandable stents the standard selection among medical practitioners. The market dominance of balloon-expandable stents is further supported by doctors because these devices enable minimally invasive procedures through their ability to enter the body using small incisions. This combination of improved stent design technology and material advances alongside the development of drug-eluting balloon-expandable stents provides better patient results which promotes their market adoption. Apart from this, strong healthcare infrastructure and reimbursement policies in the United States together with the factors mentioned ensure balloon-expandable stents will maintain their market leadership position while continuing to grow.

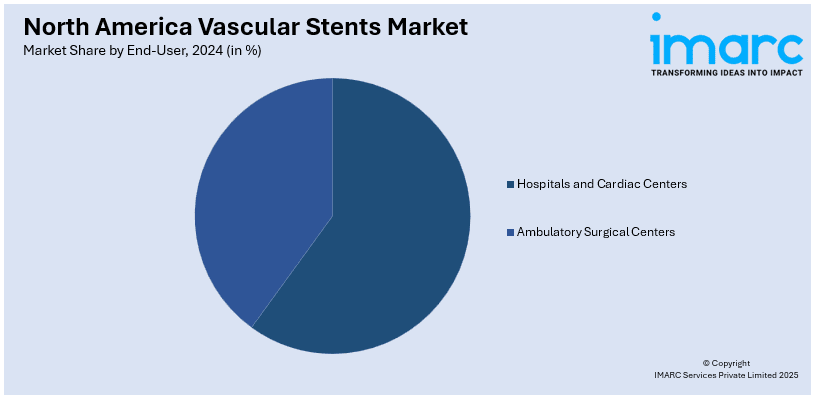

Analysis by End-User:

- Hospitals and Cardiac Centers

- Ambulatory Surgical Centers

Hospitals and cardiac centers represent the largest end-user segment in the North America vascular stents market, driven by their central role in the diagnosis, treatment, and management of cardiovascular diseases. The growing number of heart-related procedures together with increasing coronary artery disease prevalence has strongly increased vascular stent demand across health care facilities. Besides this, hospital departments that specialize in cardiac care lead the North America vascular stents market as they maintain cutting-edge technologies together with experienced medical personnel who conduct stent implantation treatments. The hospital approach to minimally invasive surgeries and improved patient success rates together with shorter recovery periods drives hospitals to adopt vascular stents. Also, the use of stents for heart condition treatment continues to increase within cardiac centers because they possess specialized expertise together with cutting-edge diagnostic tools. As a result, the combination of a strong medical infrastructure structure with favorable payment systems in the United States enables hospitals along with cardiac centers to serve as essential market growth factors.

Country Analysis:

- United States

- Canada

- Mexico

The United States commands the largest share of the North America vascular stents market, driven by a high prevalence of cardiovascular diseases, an aging population, and ongoing advancements in medical technology. The demand for vascular stents is further fueled by the country’s strong healthcare infrastructure, extensive healthcare insurance coverage, and favorable reimbursement policies. The Health System operates through 11 independent joint-venture centers with a network of 9000 primary and specialty care physicians who provide services throughout the entire New York City boroughs, as well as the regions of Westchester, Long Island, and Florida, to provide vascular stent procedures throughout the area. Concurrent with this, continuous technological innovations such as drug-eluting stents and bioresorbable stents are widely adopted, improving patient outcomes. For example, the Esprit BTK Everolimus Eluting Resorbable Scaffold System received FDA approval, highlighting the acceptance of innovative medical devices that offer superior treatment options. The regional market demand increases because major medical device producers and research centers operate in this area.

Competitive Landscape:

The competitive landscape of the North America vascular stents market is highly dynamic, with numerous key players focusing on innovation and product differentiation to maintain market share. The market sees companies actively invest in developing next-generation stents through research that produces drug-eluting and bioresorbable stent technologies with improved security and performance. Furthermore, companies regularly form strategic alliances including mergers and acquisitions because they aim to enhance their product range alongside global market expansion. Additionally, strong distribution networks, regulatory compliance, and continuous improvements in stent materials and delivery systems, intensify competition and driving the market growth and innovation.

The report provides a comprehensive analysis of the competitive landscape in the North America vascular stents market with detailed profiles of all major companies.

Latest News and Developments:

- In January 2025, Boston Scientific acquired Bolt Medical, a company specializing in advanced stent technologies. This acquisition strengthens Boston Scientific's position in the vascular stent market by integrating innovative stent designs and expanding its product offerings. The integration is expected to drive growth by providing a broader range of solutions to healthcare providers.

- In May 2024, Abbott launched an enhanced version of its Xience drug-eluting stent, featuring a new polymer coating designed to improve biocompatibility and reduce the risk of restenosis. This enhancement aims to provide better long-term outcomes for patients and strengthen Abbott's competitive position in the coronary stent market.

- In May 2024, Medtronic’s PulseSelect pulsed field ablation system received approval in Japan, expanding its global reach. This milestone enhances Medtronic's presence in North America, driving the adoption of innovative AFib treatments for improved patient outcomes.

- In January 2024, The FDA granted Boston Scientific approval to introduce its Farapulse pulsed field ablation system for treating atrial fibrillation patients. This approval allows Boston Scientific to enter the electrophysiology market, diversifying its portfolio and tapping into a new revenue stream.

- In December 2023, Biotronik launched the Orsiro Mission drug-eluting stent, featuring a biodegradable polymer coating designed to reduce inflammation and improve vessel healing. This development positions Biotronik as a leader in innovative stent technologies.

North America Vascular Stents Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Coronary Stents, Peripheral Vascular Stents, EVAR Stent Grafts |

| Materials Covered |

|

| Mode of Deliveries Covered | Balloon-Expandable Stents, Self-Expanding Stents |

| End-Users Covered | Hospitals and Cardiac Centers, Ambulatory Surgical Centers |

| Countries Covered | United States, Canada, Mexico |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the North America vascular stents market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the North America vascular stents market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the North America vascular stents industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The vascular stents market was valued at USD 3.9 Billion in 2024.

The growth of the North America vascular stents market is driven by factors such as the increasing prevalence of cardiovascular diseases, advancements in stent technology (e.g., drug-eluting stents), the aging population, rising awareness of early diagnosis and treatment, and improvements in healthcare infrastructure and access.

IMARC estimates the vascular stents market to exhibit a CAGR of 4.69% during 2025-2033, reaching a value of USD 6.0 Billion by 2033.

Coronary stents account for the largest share of the North America vascular stents product type market, driven by the high incidence of coronary artery diseases, advancements in stent technology (such as drug-eluting stents), and an increasing number of percutaneous coronary interventions (PCIs) performed to treat heart conditions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)