North America Specialty Paper Market Size, Share, Trends and Forecast by Type, Raw Material, Application, and Country, 2026-2034

North America Specialty Paper Market Summary:

The North America specialty paper market size reached 9,959.17 Million Tons in 2025 and is projected to reach 13,021.75 Million Tons by 2034, growing at a compound annual growth rate of 3.02% from 2026-2034.

The market is propelled by escalating demand for sustainable packaging solutions driven by regulatory initiatives promoting recyclable materials. Rising e-commerce activities across the region are amplifying the need for durable and lightweight specialty papers. Furthermore, expanding food service applications and technological advancements in paper manufacturing are creating new growth avenues, collectively strengthening the North America Specialty Paper market share.

Key Takeaways and Insights:

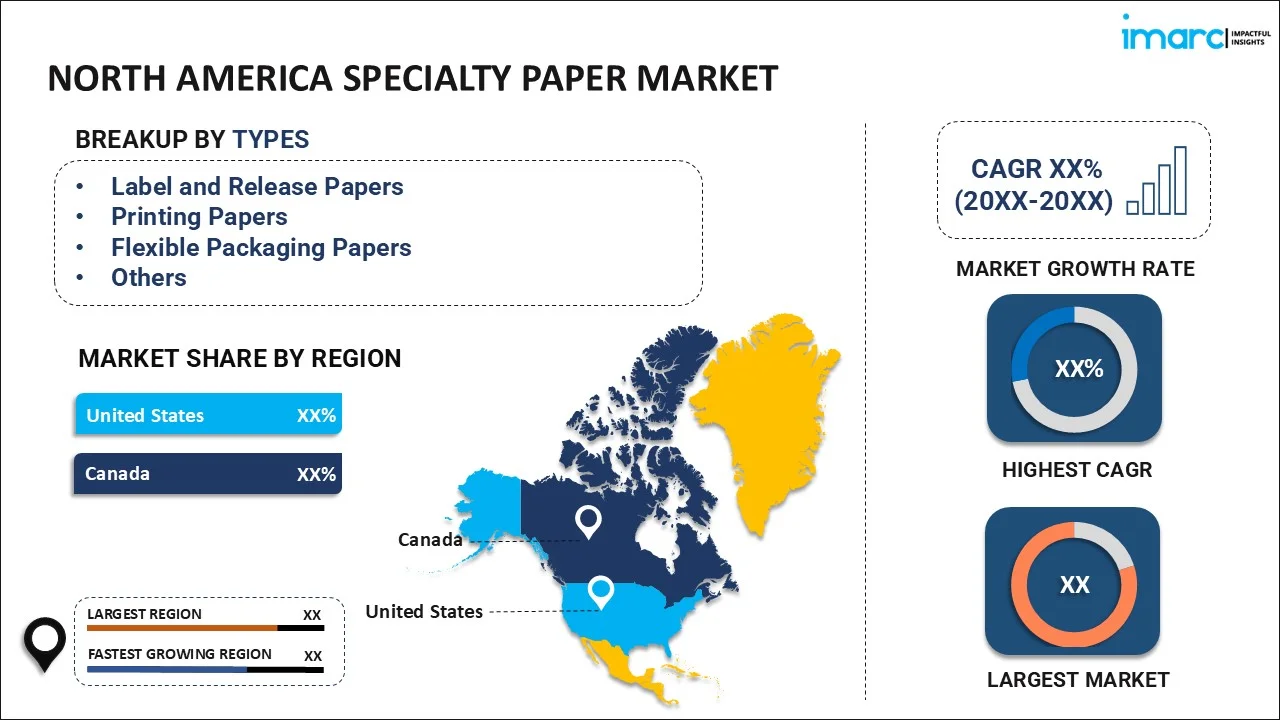

- By Type: Label and release papers dominate the market with a share of 28% in 2025, due to rising e-commerce packaging demands, brand differentiation needs, and increasing product labeling requirements across retail sectors.

- By Raw Material: Pulp leads the market with a share of 45% in 2025, owing to its essential role as the primary fiber source for specialty paper manufacturing. The abundance of forestry resources in North America ensures reliable supply chains and cost-effective production processes.

- By Application: Packaging and labeling holds the largest segment with a share of 33% in 2025. This dominance is driven by the exponential growth in e-commerce activities and increasing consumer preference for sustainable packaging alternatives, positioning specialty papers as preferred solutions across retail sectors.

- By Country: United States represents the leading region with 78% share in 2025, driven by robust manufacturing infrastructure, strong regulatory support for sustainable materials, and high consumer awareness regarding environmental concerns across multiple end-use industries.

- Key Players: Key players drive the North America specialty paper market by expanding production capacities, investing in sustainable manufacturing technologies, and strengthening distribution networks. Their focus on innovation, research partnerships, and product diversification ensures consistent market growth and enhanced consumer satisfaction.

The North America specialty paper market continues demonstrating robust momentum fueled by converging sustainability trends and evolving consumer preferences. Regional manufacturers are increasingly adopting advanced pulp processing technologies and eco-friendly coating solutions to meet stringent environmental regulations while maintaining product quality standards. The expanding food service sector is generating heightened demand for microwave-safe and oven-safe specialty papers, particularly in convenience food applications. Furthermore, pharmaceutical industry growth is spurring requirements for specialized drug packaging solutions that ensure product integrity and regulatory compliance. Construction sector expansion continues driving masking tape demand, while the flourishing cosmetics industry seeks premium packaging materials. E-commerce proliferation across North America is simultaneously creating unprecedented demand for protective packaging papers and label solutions, with major retailers prioritizing fiber-based alternatives to conventional plastic packaging materials.

North America Specialty Paper Market Trends:

Growing Adoption of Sustainable Packaging Solutions

The regional market is witnessing accelerated transition toward sustainable packaging materials as brands prioritize environmental responsibility. Consumer awareness regarding plastic pollution is driving retailers and manufacturers to adopt specialty paper alternatives for product packaging, wrapping, and cushioning applications. Regulatory frameworks, including state-level plastic reduction mandates, are further encouraging enterprises to integrate recyclable paper-based solutions into their packaging strategies, thereby strengthening market expansion prospects. According to the American Forest & Paper Association (AF&PA), 46 million tons of paper was recycled in the United States in 2024, with US mills consuming 1.29 million more tons of recycled paper compared to 2023. The recycled paper share of all fiber used at US mills increased from 36.6% in 2005 to 44.4% in 2024, demonstrating strong industry commitment to sustainable packaging solutions.

Technological Advancements in Digital Printing and Smart Labeling

Specialty paper uses in the branding and product identification sectors are changing due to advancements in digital printing technologies. The region's supply chain traceability and logistical efficiency are being improved by the incorporation of RFID-based paper labels. Manufacturers are able to create high-performance label sheets with exceptional moisture resistance and durability thanks to advanced coating methods, satisfying changing needs for personalization in the food, beverage, and pharmaceutical industries.

Expansion of Food Service and Convenience Applications

The proliferating quick-service restaurant sector and home cooking popularity are escalating demand for specialty food-grade papers. Manufacturers are developing microwave-safe, oven-safe, and grease-resistant specialty papers tailored for convenience food applications. Rising consumer preference for ready-to-eat meals and baking products is stimulating innovation in parchment and baking papers, creating substantial growth opportunities across the food service value chain within North America. According to the National Restaurant Association's 2025 State of the Restaurant Industry report, the foodservice industry is projected to reach USD 1.5 Trillion in sales in 2025, with employment expected to grow to 15.9 million.

Market Outlook 2026-2034:

The outlook for the North American specialty paper market is still positive as technology advancements and sustainability requirements continue to change the dynamics of the sector. To meet changing end-user needs, manufacturers are directing investments into product development and capacity expansion. Innovation in barrier papers and recyclable packaging formats is being accelerated by strategic partnerships between manufacturers and brand owners. Over the course of the projected period, e-commerce growth is anticipated to maintain good growth momentum in conjunction with regulatory support for sustainable materials. The market size was estimated at 9,959.17 Million Tons in 2025 and is projected to reach 13,021.75 Million Tons by 2034, reflecting a compound annual growth rate of 3.02% from 2026-2034.

To get detailed segment analysis of this market Request Sample

North America Specialty Paper Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Type | Label and Release Papers | 28% |

| Raw Material | Pulp | 45% |

| Application | Packaging and Labeling | 33% |

| Country | United States | 78% |

Type Insights:

- Label and Release Papers

- Printing Papers

- Flexible Packaging Papers

- Rolling Papers

- Others

Labels and release papers represent the leading segment with a market share of 28% of the total North America specialty paper market in 2025.

Label and release papers serve essential functions in packaging, branding, and product identification applications across diverse industry verticals. These papers offer exceptional versatility in design, texture, and printability, enabling brands to create customized and visually appealing packaging solutions that enhance consumer engagement across retail environments. The expanding e-commerce sector is driving substantial demand for shipping labels and barcode applications, while pharmaceutical and food industries increasingly rely on specialized label papers for regulatory compliance and product traceability requirements.

The growth trajectory of label and release papers is further supported by technological advancements in pressure-sensitive adhesives and release liner technologies that improve application efficiency and performance consistency. Rising consumer preference for sustainable packaging solutions is encouraging manufacturers to develop recyclable and compostable label papers that align with environmental regulations. Additionally, the proliferation of smart labeling technologies incorporating RFID and NFC capabilities is creating new application opportunities that strengthen market positioning throughout North America.

Raw Material Insights:

- Pulp

- Fillers and Binders

- Additives and Coatings

- Others

Pulp dominates with a market share of 45% of the total North America specialty paper market in 2025.

Pulp serves as the fundamental raw material backbone for specialty paper manufacturing throughout North America, ensuring superior strength, brightness, and consistency in finished products. The region benefits from abundant forestry resources, particularly in Canada, where the forest sector contributes significantly to the national economy and supports substantial employment across rural communities. This robust supply infrastructure enables manufacturers to maintain cost-effective production processes while meeting rising demand for sustainable, FSC-certified virgin pulp grades across packaging and food-contact applications.

The dominance of pulp-based specialty papers reflects market preference for products offering exceptional physical, optical, and chemical properties essential for diverse industrial applications. Vertically integrated producers leverage plantation forestry ownership to shield margins against raw material price volatility while ensuring supply chain resilience. Manufacturing innovations in pulp processing technologies continue enhancing fiber quality and production efficiency, enabling development of higher-margin specialty grades that command premium positioning across food service, pharmaceutical packaging, and medical sterilization applications throughout the regional marketplace.

Application Insights:

- Packaging and Labeling

- Printing and Writing

- Industrial Use

- Building and Construction

- Others

Packaging and labeling leads with a share of 33% of the total North America specialty paper market in 2025.

The packaging and labeling segment maintains leadership driven by exponential e-commerce growth and sustainability mandates accelerating paper-based packaging adoption across North America. This surge has created parallel demand for durable, lightweight, and customizable specialty papers suitable for diverse shipping and retail applications. Kraft paper and containerboard are gaining prominence as preferred materials among major retailers prioritizing sustainable packaging alternatives, while stringent environmental regulations continue encouraging enterprises to transition from plastic-based solutions toward recyclable paper-based packaging options.

Brand owners increasingly recognize packaging as a critical differentiator, driving innovation in high-quality label papers offering superior printability and barrier properties. Regulatory frameworks promoting recyclable materials, including California's Plastic Pollution Prevention Act, have incentivized enterprises to transition toward paper-based packaging solutions. Manufacturers are responding by developing enhanced moisture-resistant, grease-proof, and food-safe specialty papers that meet stringent compliance requirements while delivering premium shelf appeal and product protection across retail and food service channels.

Country Insights:

- United States

- Canada

The United States exhibits a clear dominance with a 78% share of the total North America specialty paper market in 2025.

Because of its sophisticated supply chain networks, substantial industrial infrastructure, and strong governmental backing for sustainable packaging materials, the United States continues to have a commanding market leadership position. Recyclable specialty papers are preferred in the retail, food service, and pharmaceutical industries due to high customer awareness of environmental issues. In order to improve product performance and sustainability credentials, major industry companies with their headquarters in the nation continue to invest in technological advancements and increases in manufacturing capacity. The demand for protective packaging solutions is further increased by the consolidation of e-commerce giants.

Specialty packaging papers used in shipping and product protection applications are in high demand due to the country's booming e-commerce industry. The shift away from paper-based packaging is being accelerated by corporate sustainability initiatives from large retailers and government legislation that promote the use of recyclable materials. The United States is the main growth engine for the market for specialty paper in North America owing to its leadership in innovation and manufacturing excellence.

Market Dynamics:

Growth Drivers:

Why is the North America Specialty Paper Market Growing?

Rising E-Commerce Growth and Sustainable Packaging Demand

The exponential expansion of e-commerce activities across North America is generating unprecedented demand for specialty papers used in packaging, wrapping, and cushioning applications. Online retail proliferation requires substantial quantities of durable, lightweight, and protective packaging materials that maintain product integrity during transit while meeting consumer expectations for sustainable alternatives. Major retailers are prioritizing fiber-based packaging solutions to align with corporate sustainability commitments and evolving consumer preferences. The surge in direct-to-consumer shipping has particularly amplified requirements for kraft paper mailers, corrugated cushioning, and protective paper packaging. Manufacturers are responding by developing innovative specialty paper grades offering enhanced barrier properties, moisture resistance, and structural strength without compromising recyclability. Brand differentiation through premium packaging presentation further stimulates adoption of high-quality specialty papers that enhance unboxing experiences. According to the US Census Bureau's Quarterly Retail E-Commerce Sales report, e-commerce sales in 2024 accounted for 16.1% of total retail sales, up from 15.3% in 2023. In the fourth quarter of 2024, U.S. retail e-commerce sales reached an estimated USD 352.9 billion, representing a 9.3% increase compared to Q4 2023, significantly outpacing overall retail sales growth of 4.5% during the same period.

Regulatory Support for Sustainable Materials

Government regulations promoting recyclable and biodegradable materials are significantly accelerating specialty paper market expansion throughout the region. State-level plastic reduction mandates, including California's Plastic Pollution Prevention Act, have incentivized enterprises to transition toward paper-based packaging alternatives that meet stringent environmental compliance requirements. Federal agencies continue strengthening frameworks that encourage sustainable material adoption across industries. These regulatory initiatives are compelling brand owners and manufacturers to reformulate packaging strategies, replacing conventional plastic materials with specialty paper solutions. Extended producer responsibility programs are further driving accountability for packaging end-of-life management, favoring recyclable paper grades. The alignment between regulatory requirements and consumer sustainability preferences creates favorable market conditions for specialty paper products meeting environmental certifications and recyclability standards. According to industry report, more than 2.9 million tons of plastic went into producing single-use plastic packaging and plastic food service ware in California in 2023, which must be reduced by approximately 725,000 tons by 2032.

Expanding Food and Beverage Industry Applications

The flourishing food and beverage sector is generating heightened demand for food-grade specialty papers across packaging, labeling, and food service applications. Growing consumption of convenience foods, ready-to-eat meals, and quick-service restaurant offerings stimulates requirements for microwave-safe, oven-safe, and grease-resistant specialty papers that ensure food safety and preservation. Rising home baking and cooking popularity further amplifies demand for parchment and baking papers. Manufacturers are developing innovative barrier coatings and antimicrobial treatments that enhance specialty paper functionality for food-contact applications. Stringent food safety regulations necessitate compliance with FDA requirements, driving adoption of certified food-grade specialty papers. The quick-service restaurant segment expansion, combined with increasing takeaway and delivery services, continues creating substantial growth opportunities for specialty food packaging papers throughout North America.

Market Restraints:

What Challenges the North America Specialty Paper Market is Facing?

Fluctuating Raw Material Costs and Supply Chain Pressures

Volatile raw material prices, especially those of wood pulp and specialized coatings, which have a substantial impact on production economics, are a continuous challenge for the specialty paper sector. Manufacturer profits are squeezed, and long-term planning is made more difficult by pricing pressures brought on by energy cost changes and supply chain interruptions. Smaller manufacturers who don't have long-term fiber contracts or vertical integration are still particularly susceptible to these price fluctuations.

Competition from Digital Alternatives

Accelerating digital transformation continues eroding demand for traditional printing and writing paper applications across commercial and office environments. The proliferation of electronic communication, digital marketing platforms, and paperless documentation systems reduces reliance on paper-based products. Publishing industry decline and transition toward digital media consumption particularly impact graphic paper segments, requiring manufacturers to diversify toward sustainable packaging applications.

Stringent Regulatory Compliance Requirements

Evolving environmental and food safety regulations impose significant compliance burdens on specialty paper manufacturers. Recent mandates eliminating PFAS chemicals from food-contact applications require substantial reformulation investments and process modifications. Food-contact certification requirements, recycled-content mandates, and safety testing protocols extend time-to-market while increasing production costs, particularly challenging smaller manufacturers lacking research and development resources.

Competitive Landscape:

The competitive dynamics of the North American specialty paper industry are somewhat concentrated, with both specialized regional firms and well-established global corporations. To improve their market positioning, top firms concentrate on investing in sustainable technologies, increasing capacity, and making smart acquisitions. With businesses investing in cutting-edge coating technologies, barrier paper development, and recyclable packaging solutions, innovation continues to be a crucial differentiator. To guarantee supply security and margin protection, major producers use vertical integration that spans forestry resources to completed product manufacturing. While mergers and acquisitions increase market share, strategic alliances between paper producers and brand owners expedite the development of sustainable packaging. Targeting particular end-user needs in food service, medicinal, and industrial applications, smaller specialist producers compete through niche product offerings, customization capabilities, and regional service excellence.

North America Specialty Paper Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Label and Release Papers, Printing Papers, Flexible Packaging Papers, Rolling Papers, Others |

| Raw Materials Covered | Pulp, Fillers and Binders, Additives and Coatings, Others |

| Applications Covered | Packaging and Labeling, Printing and Writing, Industrial Use, Building and Construction, Others |

| Countries Covered | United States, Canada |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The North America specialty paper market reached a volume of 9,959.17 Million Tons in 2025.

The North America specialty paper market is expected to grow at a compound annual growth rate of 3.02% from 2026-2034 to reach 13,021.75 Million Tons by 2034.

Pulp dominated the market with a share of 45%, owing to its fundamental role as the primary fiber source for specialty paper manufacturing and the region's abundant forestry resources ensuring reliable supply chains and cost-effective production processes.

Key factors driving the North America specialty paper market include rising e-commerce packaging demand, regulatory support for sustainable materials, expanding food and beverage applications, technological advancements in barrier papers, and growing consumer preference for recyclable packaging alternatives.

Major challenges include fluctuating raw material costs particularly wood pulp prices, competition from digital alternatives reducing traditional paper demand, stringent regulatory compliance requirements for PFAS-free formulations, supply chain pressures, and energy cost volatility impacting production economics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)