North America Polypropylene Copolymer Market Size, Share, Trends and Forecast by End-Use and Country, 2026-2034

North America Polypropylene Copolymer Market Summary:

The North America polypropylene copolymer market size was valued at USD 16.6 Billion in 2025 and is projected to reach USD 21.81 Billion by 2034, growing at a compound annual growth rate of 3.10% from 2026-2034.

North America market continues expanding as manufacturers across packaging, automotive, and consumer goods sectors increasingly adopt this versatile thermoplastic for its superior impact resistance and processability. The polymer's balanced combination of stiffness and flexibility makes it indispensable in applications ranging from food-safe containers to technical automotive components, while ongoing material innovations enhance performance characteristics and sustainability credentials, thereby expanding the North America polypropylene copolymer market share.

Key Takeaways and Insights:

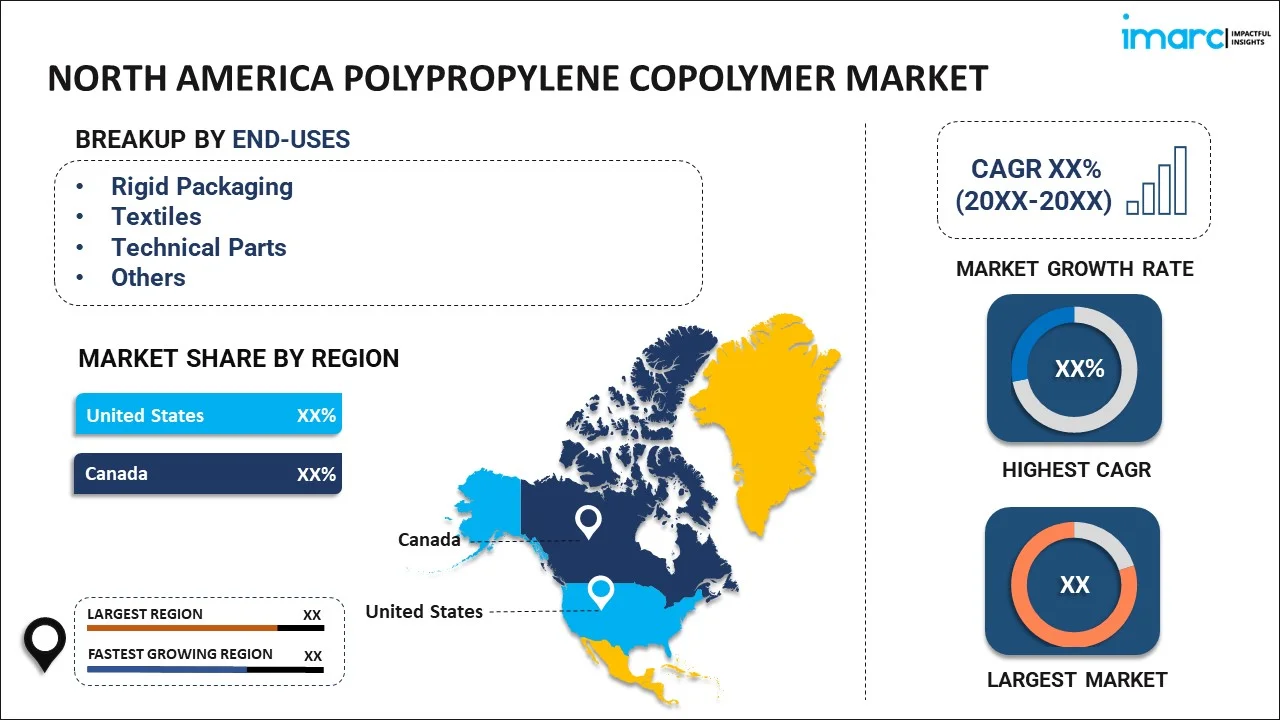

- By End-Use: Rigid packaging dominates the market with a share of 42% in 2025, driven by food and beverage container manufacturers seeking durable, lightweight, and chemically resistant materials that meet stringent FDA regulations.

- By Country: United States leads the market with a share of 78% in 2025, reflecting the concentration of packaging manufacturing facilities, automotive production plants, and consumer goods companies throughout the industrialized regions.

- Key Players: The North America polypropylene copolymer market exhibits moderate consolidation with established petrochemical corporations competing alongside specialized resin producers across diverse application segments and geographic territories.

The North American market has evolved into a critical component of the region's manufacturing ecosystem, supported by integrated petrochemical infrastructure and proximity to propylene feedstock sources. The material's thermoplastic properties enable efficient molding, extrusion, and film-forming processes that reduce production cycle times while maintaining dimensional stability across temperature fluctuations. Automotive lightweighting initiatives have particularly accelerated adoption, with polypropylene copolymers replacing heavier metals in interior trim panels, door components, and under-hood applications. Implementing lightweight components and high-efficiency engines, made possible by advanced materials, in a quarter of the U.S. fleet could result in over 5 billion gallons of fuel savings each year by 2030. For instance, major automotive manufacturers have integrated these polymers into dashboard assemblies and bumper systems, achieving weight reductions exceeding fifteen percent while maintaining crash performance standards and aesthetic requirements.

North America Polypropylene Copolymer Market Trends:

Advanced Recycling Technologies Transforming Material Circularity

Chemical recycling facilities across North America are implementing pyrolysis and solvolysis processes that convert post-consumer polypropylene copolymer waste back into virgin-quality monomers, enabling closed-loop material flows. These technologies address contamination challenges that traditionally limited mechanical recycling effectiveness, particularly for multi-layer packaging structures and pigmented products. Apart from this, a consortium of petrochemical producers announced plans to establish advanced recycling capacity capable of processing over two hundred thousand metric tons annually, with feedstock sourced from municipal collection programs and industrial scrap streams throughout the Great Lakes region. In 2025, OVA Chemicals launched its inaugural polyethylene (PE) film recycling plant, named SYNDIGO1, situated in Connersville, Indiana, USA. The facility is said to be one of the most sophisticated of its type in the world, covering 450,000ft2.

Bio-Based Propylene Integration Reducing Carbon Footprint

Renewable propylene derived from biomass gasification and bioethanol dehydration is entering commercial production streams, offering polypropylene copolymer grades with significantly lower lifecycle carbon emissions compared to conventional petroleum-based materials. These bio-attributed polymers maintain identical physical and chemical properties to fossil-derived counterparts, enabling drop-in replacement without reformulating existing product specifications or modifying processing equipment. Several consumer goods manufacturers have begun incorporating bio-based polypropylene copolymers into packaging applications, responding to corporate sustainability commitments and growing retailer demands for renewable content verification through third-party certification programs. In 2025, ABB formed a supply contract with Citroniq to deliver cutting-edge automation, electrification, and digitalization technologies for a fully biogenic polypropylene plant in Nebraska, US, seeking to become the world's initial fully commercial-scale facility of this type. Polypropylene is utilized in numerous common products that society depends on, such as packaging for food and beverages, components for vehicles, consumer products, and medical equipment.

Smart Packaging Integration Driving Functional Material Development

Polypropylene copolymer formulations are being engineered to incorporate conductive additives, antimicrobial agents, and oxygen-scavenging compounds that extend shelf life while enabling digital interaction capabilities. These functional enhancements transform traditional packaging into intelligent systems capable of monitoring product freshness, authenticating supply chain provenance, and communicating with consumer smartphones through embedded sensors. In early 2025, food packaging innovators demonstrated temperature-indicating polypropylene copolymer containers that change color when cold chain integrity is compromised, providing visual verification of proper refrigeration throughout distribution networks from production facilities to retail display cases. In 2025, Nextloop revealed that its unique recycling method for recycled polypropylene (rPP) complies with the direct food contact standards established by the Food and Drug Administration (FDA). The FDA LNO, recorded as Prenotification Consultation (PNC) No. 3291, permits NEXTLOOPP rPP to be used at levels reaching 100% for all food categories and under Conditions of Use A to H, covering the entire range of applications, from high-temperature heat sterilization to frozen storage.

Market Outlook 2026-2034:

North America's polypropylene copolymer sector is positioned for sustained expansion as manufacturers prioritize material efficiency, regulatory compliance, and performance optimization across diversified end-use applications. Automotive electrification trends continue driving demand for lightweight polymer solutions that maximize battery range, while pharmaceutical packaging requirements for moisture barrier properties and sterilization compatibility support growth in technical applications. The market generated a revenue of USD 16.6 Billion in 2025 and is projected to reach a revenue of USD 21.81 Billion by 2034, growing at a compound annual growth rate of 3.10% from 2026-2034. Infrastructure development across the region promises to strengthen supply chain resilience, with new propylene dehydrogenation units and polymer production facilities planned throughout Gulf Coast and Midwest locations to reduce import dependency and improve logistics efficiency.

North America Polypropylene Copolymer Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

End-Use |

Rigid Packaging |

42% |

|

Country |

United States |

78% |

End-Use Insights:

To get detailed segment analysis of this market, Request Sample

- Rigid Packaging

- Textiles

- Technical Parts

- Films

- Consumer Products

- Others

Rigid packaging dominates with a market share of 42% of the total North America polypropylene copolymer market in 2025.

Rigid packaging applications command the largest market share as food and beverage manufacturers leverage polypropylene copolymer's exceptional clarity, impact resistance, and chemical inertness for containers ranging from yogurt cups to pharmaceutical bottles. The material's ability to withstand microwave heating, refrigeration cycles, and hot-fill processing makes it particularly valuable for single-serve food packaging where product visibility and tamper-evidence are critical consumer requirements. Major dairy producers have transitioned to polypropylene copolymer containers that offer superior drop impact performance compared to traditional polystyrene alternatives, reducing breakage rates during distribution and improving shelf presentation.

The segment's dominance reflects polypropylene copolymer's regulatory approvals for direct food contact across North American jurisdictions, combined with processing advantages that enable high-speed thermoforming and injection molding operations. Thin-wall packaging technologies have advanced significantly, allowing manufacturers to reduce material usage while maintaining structural integrity and barrier properties essential for preserving product freshness. Consumer preference for transparent packaging that showcases product quality further reinforces polypropylene copolymer adoption, particularly in premium food categories where visual appeal influences purchasing decisions at retail points of sale throughout supermarket and convenience store channels.

Country Insights:

- United States

- Canada

United States leads with a share of 78% of the total North America polypropylene copolymer market in 2025.

The United States represents the predominant market for polypropylene copolymer consumption, supported by extensive petrochemical refining infrastructure along Gulf Coast regions that provides reliable propylene feedstock availability and competitive production economics. Concentrated automotive manufacturing in the Midwest, packaging operations throughout the Southeast, and consumer goods production across diverse geographic areas create sustained demand for polypropylene copolymer grades tailored to specific application requirements. The country's advanced logistics networks facilitate efficient polymer distribution from production facilities to end-user manufacturing sites, while research institutions and polymer science centers drive continuous material innovation and performance enhancement.

Regulatory frameworks governing food contact materials, automotive safety standards, and environmental compliance have shaped polypropylene copolymer formulation development throughout United States markets. Manufacturers have invested significantly in analytical capabilities and quality control systems that ensure batch-to-batch consistency and traceability requirements demanded by pharmaceutical, medical device, and food packaging customers. The concentration of technical expertise, processing equipment suppliers, and mold-making specialists within United States industrial clusters enables rapid product development cycles and customization capabilities that differentiate North American polypropylene copolymer markets from other global regions with less developed manufacturing ecosystems.

Market Dynamics:

Growth Drivers:

Why is the North America Polypropylene Copolymer Market Growing?

Automotive Lightweighting Mandates Accelerating Polymer Adoption

Regulatory pressures to improve fuel efficiency and reduce vehicular emissions are compelling automotive manufacturers to systematically replace metal components with high-performance polymer alternatives throughout vehicle architectures. Polypropylene copolymers offer density reductions approaching fifty percent compared to steel while maintaining mechanical properties suitable for non-structural applications including instrument panels, door trims, and center consoles. Engineering developments have expanded polypropylene copolymer applications into semi-structural components through reinforcement with glass fibers and mineral fillers, achieving stiffness levels that meet automotive industry specifications for dimensional stability and impact resistance. The transition toward electric vehicle platforms further intensifies lightweighting priorities, as battery weight penalties necessitate mass reductions in all ancillary vehicle systems to maximize driving range and competitive positioning against conventional powertrains. IMARC Group predicts that the United States electric vehicles market is projected to attain USD 1,895.8 Billion by 2033.

E-Commerce Expansion Driving Protective Packaging Demand

The continued growth of online retail channels has created unprecedented demand for protective packaging materials that prevent product damage during multi-touch distribution networks involving warehouse handling, parcel sorting, and last-mile delivery. The Commerce Department's Census Bureau reported that the estimated U.S. retail e-commerce sales for Q3 2025, seasonally adjusted but not accounting for price fluctuations, reached $310.3 billion, reflecting a rise of 1.9 percent (±0.4%) compared to Q2 2025. Moreover, polypropylene copolymer's toughness characteristics make it ideal for clamshell packaging, protective corner guards, and returnable transport containers that withstand repeated impacts without cracking or permanent deformation. The material's low density translates directly into reduced shipping costs for high-volume e-commerce operations, while recyclability addresses growing consumer expectations for sustainable packaging solutions. Distribution centers are increasingly standardizing on polypropylene copolymer containers for internal material handling systems, recognizing superior durability compared to alternative materials that require frequent replacement due to mechanical failure.

Manufacturing Capacity Expansion and Technology Advancement

Strategic investments in next-generation production facilities are enhancing North America's polypropylene copolymer manufacturing capabilities and supply chain reliability. Formosa Plastics USA inaugurated North America's largest horizontal polypropylene reactor at Point Comfort, Texas in September 2025, adding 550 million pounds of annual capacity with advanced process control systems enabling precise molecular weight distribution for specialized applications. These facility expansions incorporate advanced catalyst systems, energy-efficient processing technology, and real-time quality monitoring capabilities that improve product consistency while reducing manufacturing costs. Enhanced domestic production capacity reduces import dependence, strengthens supply chain resilience, and positions North American manufacturers to better serve evolving customer requirements for high-performance polymers with consistent quality specifications across automotive, packaging, and consumer goods applications.

Market Restraints:

What Challenges the North America Polypropylene Copolymer Market is Facing?

Volatile Propylene Feedstock Pricing Impacting Production Economics

Polypropylene copolymer manufacturers face persistent challenges managing propylene monomer price fluctuations driven by crude oil market dynamics, refinery operating rates, and seasonal demand variations across petrochemical derivatives. These feedstock cost uncertainties complicate long-term supply agreements with end-users who require stable pricing structures for budgeting and competitive bidding processes. Producers must balance inventory holding costs against supply security concerns, while downstream customers increasingly demand price protection mechanisms that transfer volatility risk upstream through formula-based pricing arrangements.

Regulatory Restrictions on Single-Use Plastics Constraining Applications

Legislative initiatives targeting disposable plastic products have introduced market uncertainty for polypropylene copolymer applications in food service packaging, beverage containers, and consumer convenience items. Municipal plastic bag bans, extended producer responsibility programs, and minimum recycled content mandates are reshaping packaging design priorities and material selection criteria. Compliance costs associated with evolving regulations create barriers for smaller manufacturers while advantaging vertically integrated producers with dedicated regulatory affairs capabilities and alternative material development programs.

Competition from Alternative Polymer Systems Eroding Market Share

Polypropylene copolymers face intensifying competition from polyethylene grades offering comparable performance at lower costs in select applications, while engineering thermoplastics capture high-value opportunities requiring superior thermal resistance or mechanical properties. Bio-based polymer alternatives are gaining traction in sustainability-focused market segments despite premium pricing, particularly where brand owners seek differentiation through renewable content claims. Material substitution pressures require continuous innovation in polypropylene copolymer formulations to maintain competitive positioning across diverse end-use applications.

Competitive Landscape:

The North America polypropylene copolymer market features established petrochemical corporations operating large-scale production facilities alongside regional compounders serving specialized application niches with customized formulations and technical service capabilities. Vertical integration strategies enable leading producers to secure propylene feedstock access while controlling polymer production, compounding operations, and select downstream fabrication processes. Competition centers on technical differentiation through proprietary catalyst technologies, processing stabilizers, and application-specific additive packages that enhance performance characteristics beyond commodity-grade offerings. Market participants maintain extensive laboratory capabilities for material characterization, application development support, and quality certification required by automotive, medical, and food contact end-users with stringent specification requirements.

North America Polypropylene Copolymer Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

End-Uses Covered |

Rigid Packaging, Textiles, Technical Parts, Films, Consumer Products, Others |

|

Countries Covered |

United States, Canada |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The North America polypropylene copolymer market size was valued at USD 16.6 Billion in 2025.

The North America polypropylene copolymer market is expected to grow at a compound annual growth rate of 3.10% from 2026-2034 to reach USD 21.81 Billion by 2034.

Rigid packaging dominated the North America polypropylene copolymer market with a 42% share in 2025, driven by food and beverage container manufacturers requiring durable, lightweight materials with excellent clarity and chemical resistance for applications ranging from yogurt cups to pharmaceutical bottles.

Key factors driving the North America polypropylene copolymer market include automotive lightweighting mandates that require polymer alternatives to reduce vehicle weight and improve fuel efficiency, e-commerce expansion creating demand for protective packaging materials, and medical device manufacturing requiring sterilizable polymers for healthcare applications.

Major challenges include volatile propylene feedstock pricing that impacts production economics and supply agreements, regulatory restrictions on single-use plastics constraining applications in food service and consumer packaging, and competition from alternative polymer systems including polyethylene grades and bio-based materials that erode market share across select applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)