North America Analgesics Market Size, Share, Trends and Forecast by Type, Drug Class, Route of Administration, Pain Type, Application, and Country, 2025-2033

North America Analgesics Market Size and Share:

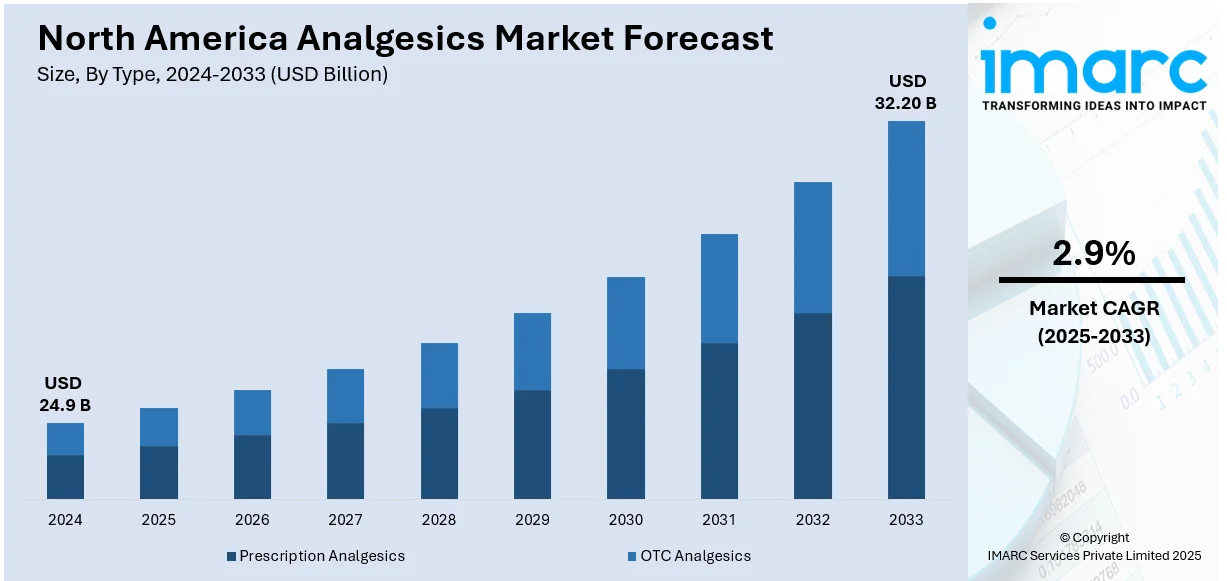

The North America analgesics market size was valued at USD 24.9 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 32.20 Billion by 2033, exhibiting a CAGR of 2.9% from 2025-2033. The growing incidences of chronic pain, an increase in the number of aging populations, and rising consumer demand in OTC and prescription pain management have driven the growth of the market. Additionally, improvements in non-opioid options and regulatory actions to combat opioid misuse are influencing market trends, promoting innovation in safer, effective pain management options.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 24.9 Billion |

|

Market Forecast in 2033

|

USD 32.20 Billion |

| Market Growth Rate 2025-2033 | 2.9% |

The market is expanding due to rising healthcare needs, an aging population, and increasing consumer preference for over-the-counter (OTC) pain relief. The prevalence of chronic pain conditions, migraines, and musculoskeletal disorders is driving demand for acetaminophen, ibuprofen, and topical analgesics. For instance, as per industry reports, in 2023, chronic pain affected approximately 24.3% of U.S. adults, while 8.5% experienced high-impact chronic pain that severely restricted their daily activities. Additionally, concerns over opioid dependency have led to a shift toward safer, non-opioid pain management solutions, including herbal and CBD-based analgesics. Regulatory policies promoting opioid alternatives and consumer awareness of self-care and pain relief options are further influencing purchasing decisions, encouraging pharmaceutical companies to develop innovative, fast-acting formulations.

Additionally, technological advancements and digital retail expansion are shaping market growth. The rise of e-commerce and direct-to-consumer sales is improving accessibility to OTC pain relievers, while telemedicine and digital pharmacies enhance convenience. Manufacturers are investing in extended-release formulas, transdermal patches, and oral disintegrating tablets to improve efficacy and patient compliance. For instance, in January 2025, Vertex Pharmaceuticals obtained FDA approval for Journavx (suzetrigine) 50 mg oral tablets, a pioneering non-opioid analgesic intended for treating moderate to severe acute pain in adults. This drug works by targeting pain-signaling pathways in the peripheral nervous system, providing a non-opioid alternative to traditional pain treatments.

North America Analgesics Market Trends:

Rising Demand for Non-Opioid and Safer Pain Relief Alternatives

The North America analgesics market is witnessing a significant shift toward non-opioid pain relief options due to growing concerns over opioid addiction and regulatory restrictions. For instance, as per industry reports, in 2023, Illegally manufactured fentanyls (IMFs) were involved in an estimated 70% of U.S. overdose deaths, highlighting their significant role in the ongoing opioid crisis. Consumers increasingly prefer acetaminophen, ibuprofen, topical analgesics, and natural pain relief solutions, which offer effective pain management with fewer risks. Government policies and healthcare initiatives encourage the development of opioid-free medications, leading pharmaceutical companies to invest in innovative pain relief formulations, including CBD-based products, topical patches, and extended-release tablets. This trend is driving product diversification and fueling competition among leading brands and emerging healthcare startups focusing on safer pain management solutions.

Expansion of E-Commerce and Direct-to-Consumer Sales Channels

The growing shift toward online shopping is transforming the North America analgesics market, with e-commerce platforms and direct-to-consumer sales channels gaining traction. For instance, as per industry reports, IMARC Group stated that the U.S. e-commerce market is expected to reach USD 2,083.97 Billion by 2033. Moreover, consumers seek convenience, competitive pricing, and doorstep delivery, leading pharmaceutical companies and retailers to strengthen their digital presence. Online pharmacies, subscription-based medication services, and brand-owned websites provide easy access to over-the-counter (OTC) and prescription analgesics, supported by telemedicine consultations. Additionally, digital marketing strategies, including personalized promotions and AI-driven recommendations, enhance customer engagement. This digital transformation is expanding market reach, increasing competition, and improving accessibility to pain relief solutions across various consumer demographics.

Innovation in Drug Formulations and Advanced Delivery Systems

Pharmaceutical companies in North America are investing in advanced drug formulations and innovative delivery systems to enhance analgesic effectiveness and patient convenience. New developments include sustained-release tablets, transdermal patches, and nano-formulated pain relievers that provide longer-lasting relief with reduced side effects. The demand for fast-acting, non-invasive options is driving research into orally disintegrating tablets, sublingual sprays, and topical gels. Additionally, biodegradable drug implants are emerging as long-term pain management solutions for chronic conditions. For instance, in November 2024, Bioretec collaborated with Tri-State Biologics to advance RemeOs commercialization in the U.S., ensuring seamless implant distribution to hospitals across key Northeast regions. These advancements cater to consumer preferences for safer, more efficient pain relief options, strengthening competition among leading pharmaceutical brands and innovative healthcare startups.

North America Analgesics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the North America analgesics market, along with forecasts at the regional and country levels from 2025-2033. The market has been categorized based on type, drug class, route of administration, pain type, and application.

Analysis by Type:

- Prescription Analgesics

- OTC Analgesics

Prescription painkillers lead the market, driven by increasing incidence of chronic pain, postoperative recovery requirements, and management of severe trauma. These drugs, such as opioids, NSAIDs, and corticosteroids, are needed to manage moderate to severe pain conditions under medical guidance. Despite concerns over opioid misuse, regulatory policies encourage safer prescribing, driving demand for non-opioid prescription options such as gabapentinoids and muscle relaxants. Additionally, technological improvements in long-acting release forms and drug delivery systems targeting specific sites maximize efficacy while reducing side effects. As growing healthcare accessibility and physician-recommended pain management options present prescription analgesics with a strong North America analgesics market share.

Analysis by Drug Class:

- Opioids

- NSAID

- Others

Opioids are the dominant drug class segment because of their potent efficacy in treating pain that is moderately to severe. They are most commonly prescribed for postoperative convalescence, pain associated with cancer, and chronic diseases. Opioids, such as morphine, oxycodone, and fentanyl, despite growing regulatory controls and public health anxiety regarding their abuse, are still a core part of pain management. Moreover, pharmaceutical firms are concentrating on abuse-deterrent products and controlled-release technology to improve safety. With continued demand in surgical, palliative, and trauma medicine, opioids continue to hold a large market share of analgesics, even with changing regulatory environments.

Analysis by Route of Administration:

- Oral

- Parenteral

- Topical

- Transdermal

- Rectal

The oral route of administration dominates the market, propelled by high patient preference, ease of use, and widespread availability of pain relief medications. Over-the-counter (OTC) and prescription analgesics, including acetaminophen, NSAIDs, and extended-release formulations, are commonly used for managing acute and chronic pain. The segment benefits from fast absorption, consistent dosing, and cost-effectiveness, making it the preferred choice among consumers and healthcare providers. With advancements in orally disintegrating tablets, liquid formulations, and sustained-release capsules, oral analgesics continue to lead the market, addressing the growing demand for effective, convenient, and accessible pain management solutions.

Analysis by Pain Type:

- Musculoskeletal Pain

- Surgical and Trauma Pain

- Cancer Pain

- Neuropathic Pain

- Migraine

- Obstetrical Pain

- Fibromyalgia

- Pain due to Burns

- Dental/Facial Pain

- Pediatric Pain

- Others

Surgical and trauma pain is the market's largest pain type segment, driven by increasing surgical procedures, sports injuries, and trauma cases resulting from accidents. The growing number of orthopedic, cardiovascular, and cosmetic surgeries requires effective pain management measures. Healthcare professionals are moving toward non-opioid analgesics such as NSAIDs, acetaminophen, and multimodal pain management approaches to minimize opioid addiction. Improved postoperative pain relief strategies, including extended-release drugs and targeted drug delivery systems, accelerate recovery. Increasing age, more elective procedures, and growing healthcare accessibility mean continued demand for trauma and surgical pain management.

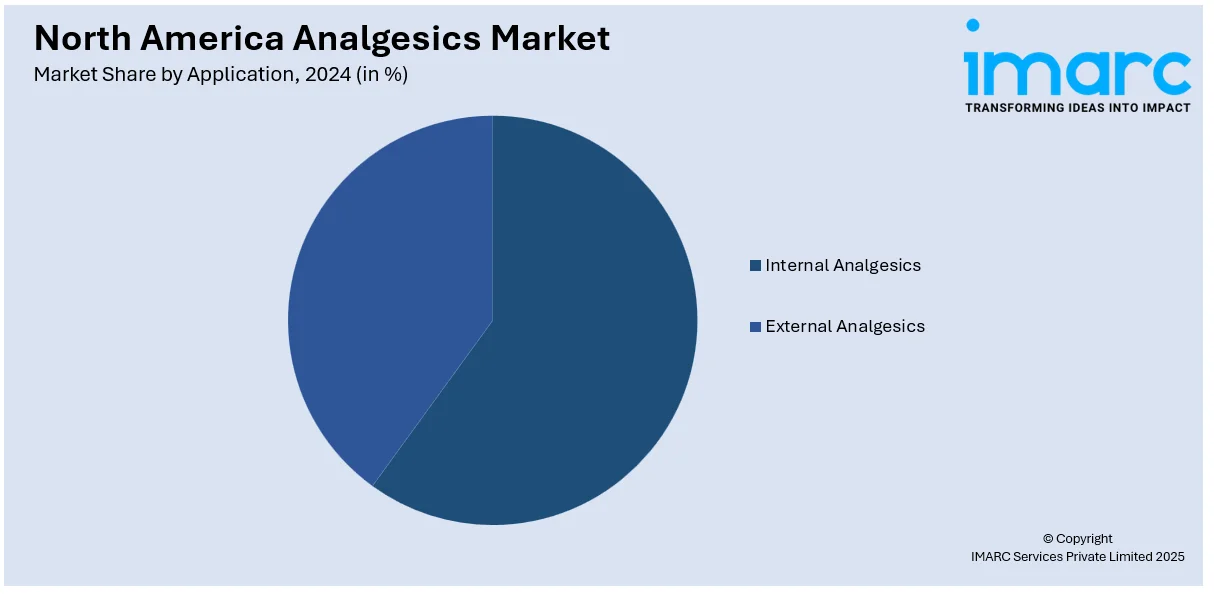

Analysis by Application:

- Internal Analgesics

- External Analgesics

Internal analgesics predominate in the market due to heavy demand for prescription and over-the-counter (OTC) painkillers. Frequently used for headache, arthritis, muscle ache, and chronic disease, internal analgesics encompass acetaminophen, ibuprofen, aspirin, and naproxen. Widespread concern about opioid addiction has also escalated dependence on non-opioid oral pain medication, especially in the United States and Canada. Additionally, pharmaceutical technology in the form of extended-release dosage forms and combination products maximizes efficacy and compliance. With aging populations, increased healthcare awareness, and access to OTC products, internal analgesics continue to be the dominant segment, guaranteeing continued market growth in North America.

Country Analysis:

- United States

- Canada

- Mexico

According to the North America analgesics market forecast, the United States leads the market, driven by high healthcare expenditure, an aging population, and a rising number of chronic pain cases. The country has a well-established pharmaceutical industry with leading companies investing in innovative pain management solutions, including non-opioid alternatives, extended-release formulations, and topical analgesics. For instance, in May 2024, Medidata, a Dassault Systèmes brand, announced its collaboration with Lexicon Pharmaceuticals to advance the Phase 2b PROGRESS study of LX9211, a potential first non-opioid treatment for neuropathic pain in over 20 years. Moreover, rising concerns over opioid misuse have led to regulatory measures promoting safer analgesic options, further fueling market growth. Additionally, strong R&D investments, advanced healthcare infrastructure, and widespread accessibility to over-the-counter (OTC) and prescription pain relievers contribute to the United States' leadership in this segment, ensuring continued market expansion.

Competitive Landscape:

The North America analgesics market is highly competitive, fueled by increasing healthcare demands, self-medication practices, and a growing elderly population. Major pharma players compete on brand value, R&D expenditure, and varied product portfolios, such as OTC and prescription painkillers. For instance, in November 2024, Kenvue Canada announced the completion of its expanded Guelph manufacturing facility, increasing production capacity by 7.5%. This expansion enhances supply resilience, ensuring the availability of essential OTC medicines to consumers. Additionally, there is increasing demand for opioid substitutes, topical painkillers, and natural painkillers because of regulatory constraints and customer desire for safer alternatives. Pharmacies and e-commerce increase market accessibility, whereas intense FDA regulations and price pressures condition competition. Furthermore, firms emphasize innovation, promotional strategies, and alliances to hold their market share in a changing environment conditioned by healthcare policies and consumer awareness.

The report provides a comprehensive analysis of the competitive landscape in the North America analgesics market with detailed profiles of all major companies.

Latest News and Developments:

- In February 2024, Hyloris Pharmaceuticals announced the U.S. launch of Combogesic IV by Hikma Pharmaceuticals, offering an innovative non-opioid pain relief option.

- In October 2024, B. Braun Canada introduced Acetaminophen for Injection in Ready-to-Use Mini-Plasco and Ecoflac plus containers, providing a non-opioid alternative for treating mild to moderate pain, opioid adjunct therapy, and fever. The new containers are designed to enhance patient care while minimizing plastic waste.

North America Analgesics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Prescription Analgesics, OTC Analgesics |

| Drug Classes Covered | Opioids, NSAID, Others |

| Route of Administrations Covered | Oral, Parenteral, Topical, Transdermal, Rectal |

| Pain Types Covered | Musculoskeletal Pain, Surgical and Trauma Pain, Cancer Pain, Neuropathic Pain, Migraine, Obstetrical Pain, Fibromyalgia, Pain due to Burns, Dental/Facial Pain, Pediatric Pain, Others |

| Applications Covered | Internal Analgesics, External Analgesics |

| Countries Covered | United States, Canada, Mexico |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the North America analgesics market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the North America analgesics market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the North America analgesics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The North America analgesics market was valued at USD 24.9 Billion in 2024.

The North America analgesics market is driven by rising chronic pain cases, an aging population, and increased surgeries. Moreover, regulatory measures promoting non-opioid alternatives and advancements in drug formulations further boost demand, ensuring effective pain management and sustained market growth.

IMARC estimates the global North America analgesics market to reach USD 32.20 Billion in 2033, exhibiting a CAGR of 2.9% during 2025-2033.

Prescription analgesics segment accounted for the largest type market share.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)