Non-Ferrous Metals Market Report by Type (Aluminum, Copper, Lead, Tin, Nickel, Titanium, Zinc, and Others), Application (Automobile Industry, Electronic Power Industry, Construction Industry, and Others), and Region 2025-2033

Non-Ferrous Metals Market Size:

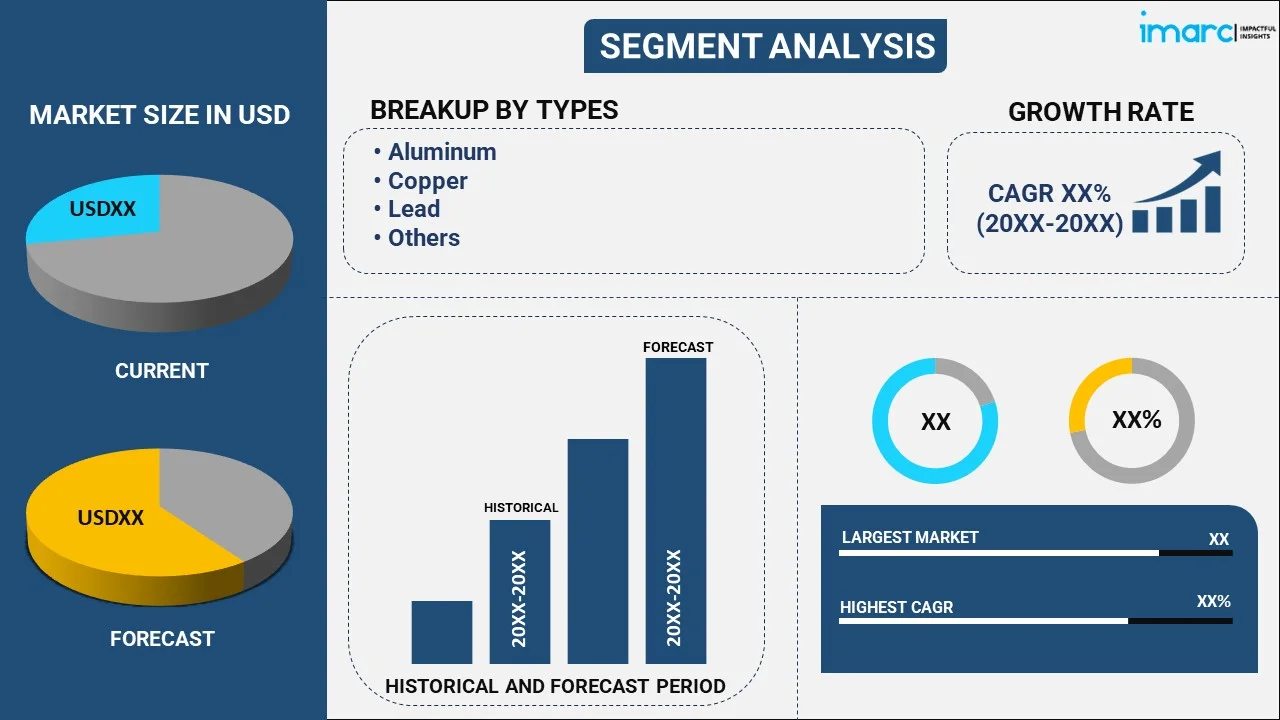

The global non-ferrous metals market size reached USD 1,183.9 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 1,746.9 Billion by 2033, exhibiting a growth rate (CAGR) of 4.2% during 2025-2033. The rising product utilization in the automotive industry, growing demand in the construction sector, recent advancements in coatings and treatments, and the adoption of sustainable production and recycling techniques are key factors driving market demand.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

|

Market Size in 2024

|

USD 1,183.9 Billion |

|

Market Forecast in 2033

|

USD 1,746.9 Billion |

| Market Growth Rate 2025-2033 | 4.2% |

Non-ferrous metals refer to metallic substances that do not contain iron (Fe) as their principal component. It includes copper, zinc, lead, aluminum, tin, nickel, titanium, chromium, magnesium, silver, platinum, and gold. They are widely used in electronic devices, automobile parts, jewelry, home appliances, decorative items, aircraft, satellites, defense equipment, medical instruments, batteries, building materials, packaging, and industrial machinery. Non-ferrous metals are non-magnetic substances and offer several characteristic properties, such as high corrosion resistance, lower melting point, excellent thermal and electrical conductivities, ductility, and malleability. They are cost-effective, lightweight, readily available, and easy to recycle substances, which aids in reducing energy consumption, and minimizing adverse environmental impact. As a result, non-ferrous metals find extensive applications across the automotive, aerospace, healthcare, defense, consumer electronics, construction, and manufacturing industries.

Non-Ferrous Metals Market Trends:

Rising Demand for Lightweight Materials in Aerospace and Automotive

The global non-ferrous metals market is witnessing escalated requirement from the aerospace and automotive industries primarily due to the rapid inclination towards lightweight materials. Non-ferrous metals, including titanium and aluminum, are rapidly being preferred for their exceptional strength-to-weight ratio, significantly enhancing performance as well as fuel efficiency. Moreover, this trend is majorly driven by the requirement to adhere to the strict emission standards and lower overall vehicle weight. In addition, the increasing demand for electric vehicles (EVs) and the production of their components, particularly batteries, is playing a key role in driving non-ferrous metals market growth. As per industry reports, in 2023, around 88% of global EVs sales were recorded in the four dominant light-duty vehicles market, with China emerging as a leading market with 33% share.

Amplified Expansion of Renewable Energy Infrastructure

The proliferation of renewable energy infrastructure is substantially propelling the demand for non-ferrous metals. Wind and solar energy ventures require significant quantities of metals, such as zinc, aluminum, and copper, for manufacturing several components, storage systems, and wiring. Moreover, the increase in global inclination towards clean energy, incentivized by heavy government investments and beneficial incentives, is boosting the development of large-scale renewable energy projects, spurring the consumption of non-ferrous metals. In addition, as the world continues to focus on sustainability and shift toward green energy, this trend is anticipated to be a pivotal factor impacting the non-ferrous metals demand. According to the International Energy Agency, in 2023, the global annual renewable capacity additions elevated by approximately 50%, i.e., around 510 GW.

Increasing Adoption of Sustainable Production Practices and Recycling

According to the non-ferrous metals market report, sustainability is rapidly emerging as a chief focus in the global market, with a heightening preference for environmentally friendly manufacturing processes as well as recycling. Non-ferrous metals, being exceptionally recyclable in nature, are witnessing elevating demand from key sectors actively seeking solutions to lower their environmental impact. Moreover, several companies are increasingly adopting closed-loop recycling methods, facilitating the reuse of metals such as copper and aluminum in new applications. As per industry reports, globally, more than 30 million tons of aluminum scrap is recycled, positioning it as one of the most recycled non-ferrous metals. Additionally, one-third of global aluminum supply constitutes of recycled aluminum, with 1.5 billion tons of aluminum actively in circulation. Consequently, this recycling not only minimizes the demand for virgin material but also reduces energy consumption and costs of production. Furthermore, with global tightening of environmental policies, sustainable manufacturing practices are likely to steer the future of the non-ferrous metals industry.

Non-Ferrous Metals Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2025-2033. Our report has categorized the market based on type and application.

Type Insights:

- Aluminum

- Copper

- Lead

- Tin

- Nickel

- Titanium

- Zinc

- Others

The report has provided a detailed breakup and analysis of the market based on the type. This includes aluminum, copper, lead, tin, nickel, titanium, zinc, and others. According to the report, aluminum represented the largest segment.

Application Insights:

- Automobile Industry

- Electronic Power Industry

- Construction Industry

- Others

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes automobile industry, electronic power industry, construction industry, and others. According to the report, automobile industry accounted for the largest market share.

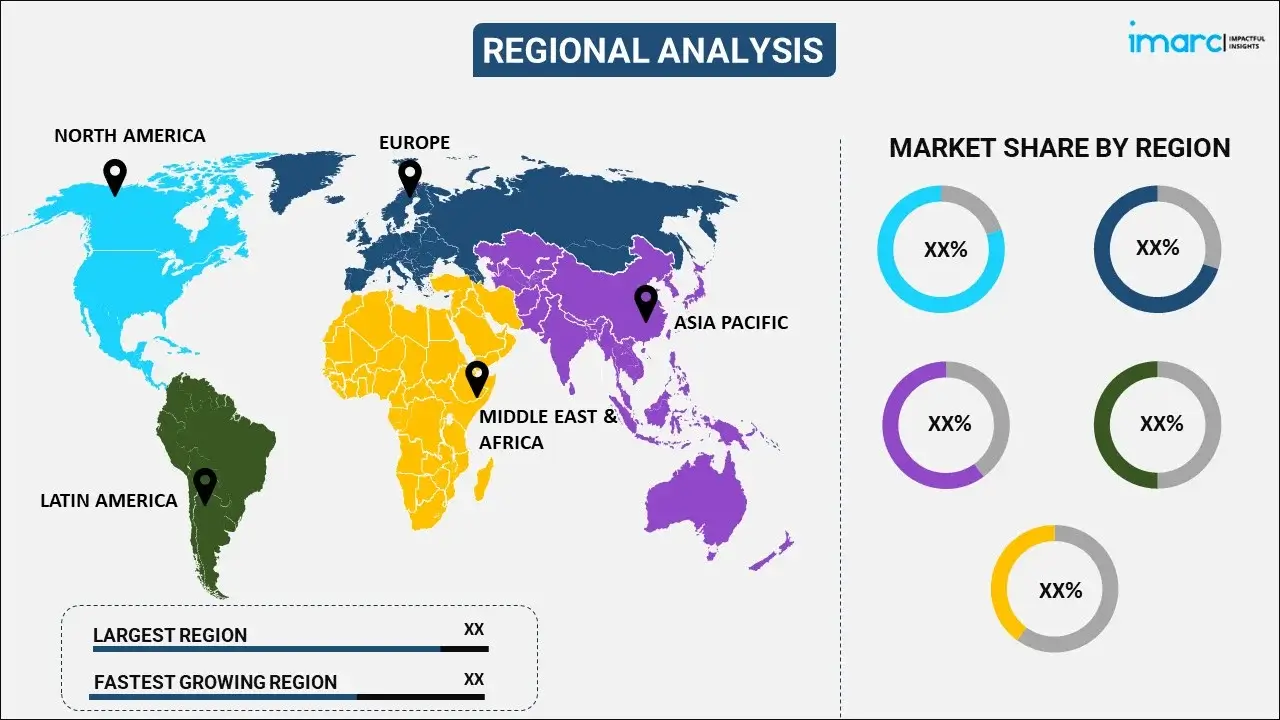

Regional Insights:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for non-ferrous metals. Some of the key factors driving the non-ferrous metals market share in Asia Pacific includes rapid industrialization, increasing infrastructural development activities, and significant technological advancements.

Competitive Landscape:

The report has also provided a comprehensive analysis of the competitive landscape in the global non-ferrous metals market. Detailed profiles of all major companies have also been provided. Some of the companies covered include:

- Aditya Birla Group

- Alcoa Corporation

- Aluminum Corporation of China Limited

- Anglo American plc

- BHP

- RUSAL (En+ Group MKPAO)

- Glencore Plc

- Norilsk Nickel

- Rio Tinto Group

- Sumitomo Metal Mining Co. Ltd.

- Vale S.A

Kindly note that this only represents a partial list of companies, and the complete list has been provided in the report.

Non-Ferrous Metals Market News:

- In October 2024, MineHub expanded its commercial agreement with Sumitomo Corporation with an aim to incorporate Sumitomo's non-ferrous metals business. This strategic move is anticipated to pave new growth prospects for MineHub beyond copper markets.

- In July 2024, Alucop, a non-ferrous and ferrous trade company, unveiled its new non-ferrous recycling plant in Morocco that will manufacture 4000 tons of copper wire, 5000 tons of aluminum billet, 5000 tons of copper anodes, 20,000 tons of aluminum ingots, etc., annually.

- In July 2024, Heraeus Group, a Germany-based metals company, announced strategic acquisition of McCol Metals, a Canada-based prominent producer of iridium, a non-ferrous metal. This acquisition is projected to expand Heraeus's efficacy in recycling precious metals.

Non-Ferrous Metals Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Aluminum, Copper, Lead, Tin, Nickel, Titanium, Zinc, Others |

| Applications Covered | Automobile Industry, Electronic Power Industry, Construction Industry, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Aditya Birla Group, Alcoa Corporation, Aluminum Corporation of China Limited, Anglo American plc, BHP, RUSAL (En+ Group MKPAO), Glencore Plc, Norilsk Nickel, Rio Tinto Group, Sumitomo Metal Mining Co. Ltd., Vale S.A, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the non-ferrous metals market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global non-ferrous metals market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the non-ferrous metals industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

The global non-ferrous metals market was valued at USD 1,183.9 Billion in 2024.

We expect the global non-ferrous metals market to exhibit a CAGR of 4.2% during 2025-2033.

The rising demand for non-ferrous metals across various industries, such as automotive, aerospace, healthcare, etc., as they offer high corrosion resistance, lower melting point, excellent thermal and electrical conductivities, ductility, and malleability, is primarily driving the global non-ferrous metals market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary closure of numerous end-use industries for non-ferrous metals.

Based on the type, the global non-ferrous metals market has been segregated into aluminum, copper, lead, tin, nickel, titanium, zinc, and others. Among these, aluminum currently holds the largest market share.

Based on the application, the global non-ferrous metals market can be bifurcated into automobile industry, electronic power industry, construction industry, and others. Currently, the automobile industry exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, where Asia Pacific currently dominates the global market.

Some of the major players in the global non-ferrous metals market include Aditya Birla Group, Alcoa Corporation, Aluminum Corporation of China Limited, Anglo American plc, BHP, RUSAL (En+ Group MKPAO), Glencore Plc, Norilsk Nickel, Rio Tinto Group, Sumitomo Metal Mining Co. Ltd., Vale S.A, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)