Naphthalene Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition

Naphthalene Price Trend, Index and Forecast

Track real-time and historical naphthalene prices across global regions. Updated monthly with market insights, drivers, and forecasts.

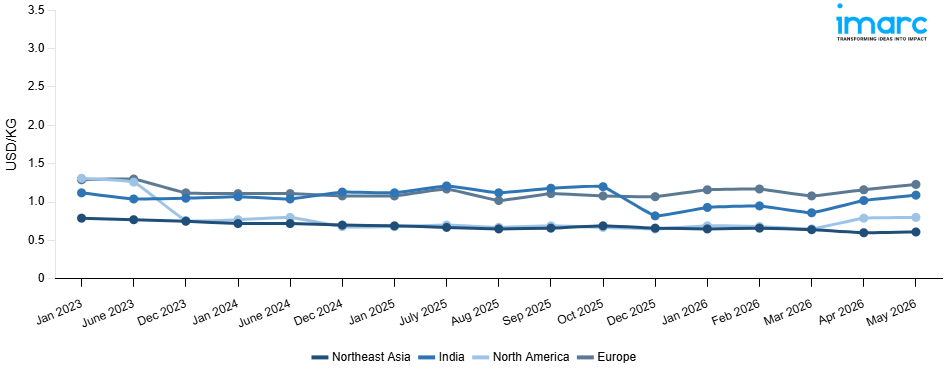

Naphthalene Prices May 2026

| Region | Price (USD/Kg) | Latest Movement |

|---|---|---|

| Northeast Asia | 0.61 | 1.7% ↑ Up |

| Europe | 1.23 | 6.0% ↑ Up |

| India | 1.09 | 6.9% ↑ Up |

| North America | 0.8 | 1.3% ↑ Up |

Naphthalene Price Index (USD/KG):

The chart below highlights monthly naphthalene prices across different regions.

Get Access to Monthly/Quarterly/Yearly Prices, Request Sample

Market Overview Q1 Ending March 2026

Northeast Asia: The naphthalene prices in Northeast Asia reached 0.64 USD/KG in March 2026. The downward pricing movement registered between December and March 2026 was 3.0%. Reduced procurement activity due to weak demand for phthalic anhydride, superplasticizer, and specialty chemicals led to slightly bearish market conditions for naphthalene in Northeast Asia during the review period. High domestic naphthalene production in China, driven by the output of coal tar products from coal tar plants, increased competition among suppliers in the region, negatively affecting prices. Reductions in feedstock costs at major producing plants lowered production costs and, consequently, weakened the cost floor of prevailing regional prices.

Europe: The naphthalene prices in Europe reached 1.08 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 0.9%. Marginally firming demand from the phthalic anhydride, construction chemical, and specialty dye manufacturing sectors provided modest procurement support and contributed to mildly bullish conditions across European markets during the review period. Slightly elevated upstream coal tar processing and refining costs at regional production facilities exerted incremental upward pressure on naphthalene manufacturing expenses and supported the prevailing marginal price increase throughout the quarter. Steady import cargo availability from key supplying regions maintained adequate supply conditions and limited the extent of upward price movement during the period.

India: The naphthalene prices in India reached 0.86 USD/KG in March 2026. The upward pricing movement registered between December and March 2026 was 4.9%. Firm demand from the construction chemical, phthalic anhydride, and specialty dye manufacturing sectors drove active naphthalene procurement and reinforced bullish pricing conditions across Indian markets throughout the review period. Rising upstream coal tar feedstock and processing costs at domestic and import production facilities elevated manufacturing expenses and provided consistent upward support to prevailing Indian market rates during the quarter. Constrained import cargo availability from key Asian supplying regions tightened domestic supply conditions and intensified competition among downstream construction chemical and dye intermediate buyers for available volumes.

North America: The naphthalene prices in North America reached 0.65 USD/KG in March 2026. The pricing movement between December and March 2026 remained unchanged. The constant demand for phthalic anhydride, construction chemicals, and specialty coatings from the manufacturing industries ensured a steady flow of naphthalene purchases across North America throughout the review period. The steady processing and refining costs of upstream coal tar in domestic manufacturing plants ensured that manufacturing costs remained at current levels and supported current regional market prices. Domestic manufacturing plants generated adequate output, ensuring stable supply conditions and, in turn, preventing directional price movement in naphthalene in North America during the quarter under review. The disciplined purchasing practices of downstream consumers, with no major market catalysts, ensured stable price conditions during the review period.

Market Overview Q4 Ending December 2025

Northeast Asia: The naphthalene prices in Northeast Asia reached 0.66 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 0.1%. The minor price drop indicated a largely steady market, marked by a balance between supply and demand across the area. Steady usage in the phthalic anhydride, construction superplasticizer, and mothball production industries sustained regular purchasing levels, while sufficient manufacturing results from coal tar distillation plants- guaranteed ample supply availability. The decreased cost of upstream coal tar feedstock slightly reduced production economics, while stable inventory levels among major distributors prevented significant price fluctuations. Consistent demand from the dye intermediates and tanning agent sectors maintained baseline consumption dynamics, resulting in nearly stable market conditions over the quarter.

Europe: The naphthalene prices in Europe reached 1.07 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 3.4%. The moderate price decline was primarily attributed to weakened demand from the concrete superplasticizer and phthalic anhydride manufacturing sectors amid broader contraction in regional construction activity and industrial output. Softening upstream coal tar distillation feedstock costs reduced production cost benchmarks for domestic producers, diminishing baseline pricing support across the supply chain. Adequate supply availability from established coal tar processing facilities maintained comfortable inventory levels, while increased import competition from competitively priced cargoes exerted additional downward pressure on prevailing market rates. Cautious procurement strategies adopted by downstream consumers anticipating further market weakening restricted restocking activity, maintaining mildly bearish conditions throughout the quarterly period.

India: The naphthalene prices in India reached 0.82 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 30.7%. During a noticeable seasonal slowdown in building and downstream processing activity across the domestic market, the much weaker demand in the concrete admixture, phthalic anhydride, and dye intermediate manufacturing sectors was the reason for the price correction. For local manufacturers, softening upstream coal tar feedstock significantly reduced manufacturing costs, allowing for aggressive price reductions. Supply side pressure was increased by increased rivalry among dispersed domestic producers, and pricing support was further tempered by surplus production capacity from new distillation facilities. Increased warehouse supplies among major distributors led to quicker liquidation plans, which put ongoing negative pressure on market prices during the quarter.

North America: The naphthalene prices in North America reached 0.65 USD/KG in December 2025. The downward pricing movement registered between September and December 2025 was 5.3%. The notable price decline was driven by weakened demand from the concrete superplasticizer, phthalic anhydride, and insect repellent manufacturing sectors amid softening construction activity and cautious consumer spending patterns across the region. Easing upstream coal tar distillation feedstock costs reduced production costs for domestic manufacturers, facilitating downward pricing adjustments. Adequate domestic production capacity maintained comfortable supply availability, while steady import flows further limited upward pricing momentum.

Market Overview Q3 Ending September 2025

Northeast Asia: In Northeast Asia, naphthalene prices rose modestly, with the keyword price index reflecting stable demand growth across downstream industries. Consumption from the textile and construction chemical sectors provided steady support, while feedstock availability from coal tar distillation remained balanced. Export activity improved slightly, enhancing regional market sentiment. Despite competitive imports, strong local procurement prevented significant downward pressure. Buyers maintained steady interest, and producers reported stable operations, allowing prices to track upward in line with sustained demand.

Europe: Europe registered a sharper increase in naphthalene prices, with the keyword price index recording strong gains supported by robust demand. The construction and plasticizer industries contributed to higher procurement volumes, while reduced feedstock availability tightened market conditions. Imports were less competitive during the quarter, strengthening domestic producers’ positions. Improved margins supported steady output levels, yet supply lagged behind rising demand, fueling bullish sentiment. The region benefitted from consistent industrial activity, sustaining price momentum across both primary and derivative applications.

India: In India, naphthalene prices advanced steadily, supported by firm downstream demand from the textile finishing and dye intermediates industries. The keyword price index reflected improving procurement activity, as local manufacturers expanded production schedules. Adequate coal tar availability ensured supply stability, while stronger construction activity added an extra layer of demand support. Export markets also remained active, with regional suppliers benefiting from higher international inquiries. These factors collectively reinforced a stable upward trajectory in domestic prices through the quarter.

North America: In North America, naphthalene prices moved higher, with the keyword price index showing moderate gains. The market benefitted from stable consumption in the construction chemicals sector, while demand for dye intermediates provided additional support. Domestic supply was adequate, with balanced coal tar feedstock availability keeping production consistent. Import flows were steady, ensuring no major disruptions to supply chains. Buyers accepted slightly higher pricing as improved downstream pull and firm procurement trends outweighed supply-side stability, resulting in moderate upward pressure.

Naphthalene Price Trend, Market Analysis, and News

IMARC's latest publication, “Naphthalene Prices, Trend, Chart, Demand, Market Analysis, News, Historical and Forecast Data Report 2026 Edition,” presents a detailed examination of the naphthalene market, providing insights into both global and regional trends that are shaping prices. This report delves into the spot price of naphthalene at major ports and analyzes the composition of prices, including FOB and CIF terms. It also presents detailed naphthalene prices trend analysis by region, covering North America, Europe, Asia Pacific, Latin America, and Middle East and Africa. The factors affecting naphthalene pricing, such as the dynamics of supply and demand, geopolitical influences, and sector-specific developments, are thoroughly explored. This comprehensive report helps stakeholders stay informed with the latest market news, regulatory updates, and technological progress, facilitating informed strategic decision-making and forecasting.

Naphthalene Industry Analysis

The global naphthalene industry size reached USD 1.2 Billion in 2025. By 2034, IMARC Group expects the market to reach USD 1.7 Billion, at a projected CAGR of 3.60% during 2026-2034. Growth is primarily driven by expanding applications in construction chemicals, dyes, and phthalic anhydride production, supported by rising demand from infrastructure development and industrial manufacturing sectors.

Latest developments in the Naphthalene Industry:

- January 2025: The Odisha government approved investment proposals amounting to INR 4,222.24 crore (about USD 4.92 Billion) across 25 industrial projects. Among these, Utkal Hydrocarbon Pvt. Ltd. in Jharsuguda has been allocated INR 63.02 crore (about USD 7.35 Million) for the establishment of a manufacturing unit specializing in coal tar pitch, dehydrated coal tar, and naphthalene. These projects encompass a diverse range of sectors, including green energy equipment, chemicals, pharmaceuticals, textiles, plastics, food processing, and downstream aluminum. The initiatives will be implemented across 11 districts, including Angul, Ganjam, Khordha, and Sambalpur.

- January 2025: A USD 1.67 billion loan from the U.S. Department of Energy’s Loan Programs Office was granted to Montana Renewables, LLC, enabling expansion of its Great Falls facility. This will boost annual output of renewable naphtha, sustainable aviation fuel (SAF), and renewable diesel from 140 million to 315 million gallons.

- July 2024: Mitsubishi and Neste deepened their partnership in Japan to promote sales of Neste’s biomass-based naphtha, with plans to shift from petroleum naphtha toward bio-naphtha feedstocks.

- April 2024: BASF expanded its EcoBalanced product suite, reinforcing its commitment to greener solutions for detergent manufacturers, industrial formulators, and cleaning sectors. In doing so, the company intends to accelerate the shift from fossil-based inputs to renewable raw materials via its Care Chemicals division’s “Care 360° – Solutions for Sustainable Life.”

- April 2024: Evonik launched Ancamine® 2880, a fast-curing, UV-resistant epoxy curing agent with excellent mechanical strength and abrasion resistance, suited for flooring applications due to its low coloration and high gloss. This agent supports ambient and low-temperature curing, rapid hardness development, and early walk-on times.

- March 2024: Merck committed €14 million to expand its M Lab™ Collaboration Center in Shanghai, adding a biology application lab, process development training center, and upstream application facility to make it the largest in its global network. The expansion aims to support China’s biopharmaceutical industry in accelerating development and manufacturing of novel therapies.

Product Description

Naphthalene is an aromatic hydrocarbon with the chemical formula C₁₀H₈, typically derived from coal tar distillation or petroleum processing. It appears as white crystalline flakes with a distinct odor and is highly volatile and combustible. Naphthalene serves as a crucial intermediate in the production of phthalic anhydride, which is widely used in resins, plasticizers, and dyes. Additionally, it is employed in moth repellents, construction chemicals such as naphthalene sulfonates for concrete admixtures, and in the synthesis of various agrochemicals. Its strong chemical reactivity, low solubility in water, and ability to form derivatives make it valuable across multiple industries, from textiles to plastics, enhancing its role as a versatile industrial chemical.

Report Coverage

| Key Attributes | Details |

|---|---|

| Product Name | Naphthalene |

| Report Features | Exploration of Historical Trends and Market Outlook, Industry Demand, Industry Supply, Gap Analysis, Challenges, Naphthalene Price Analysis, and Segment-Wise Assessment. |

| Currency/Units | US$ (Data can also be provided in local currency) or Metric Tons |

| Region/Countries Covered | The current coverage includes analysis at the global and regional levels only. Based on your requirements, we can also customize the report and provide specific information for the following countries: Asia Pacific: China, India, Indonesia, Pakistan, Bangladesh, Japan, Philippines, Vietnam, Thailand, South Korea, Malaysia, Nepal, Taiwan, Sri Lanka, Hongkong, Singapore, Australia, and New Zealand Europe: Germany, France, United Kingdom, Italy, Spain, Russia, Turkey, Netherlands, Poland, Sweden, Belgium, Austria, Ireland, Switzerland, Norway, Denmark, Romania, Finland, Czech Republic, Portugal and Greece North America: United States and Canada Latin America: Brazil, Mexico, Argentina, Columbia, Chile, Ecuador, and Peru Middle East & Africa: Saudi Arabia, UAE, Israel, Iran, South Africa, Nigeria, Oman, Kuwait, Qatar, Iraq, Egypt, Algeria, and Morocco The list of countries presented is not exhaustive. Information on additional countries can be provided if required by the client. |

| Information Covered for Key Suppliers |

|

| Customization Scope | The report can be customized as per the requirements of the customer |

| Report Price and Purchase Option |

Plan A: Monthly Updates - Annual Subscription

Plan B: Quarterly Updates - Annual Subscription

Plan C: Biannually Updates - Annual Subscription

|

| Post-Sale Analyst Support | 360-degree analyst support after report delivery |

| Delivery Format | PDF and Excel through email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report presents a detailed analysis of naphthalene pricing, covering global and regional trends, spot prices at key ports, and a breakdown of FOB and CIF prices.

- The study examines factors affecting naphthalene price trend, including input costs, supply-demand shifts, and geopolitical impacts, offering insights for informed decision-making.

- The competitive landscape review equips stakeholders with crucial insights into the latest market news, regulatory changes, and technological advancements, ensuring a well-rounded, strategic overview for forecasting and planning.

- IMARC offers various subscription options, including monthly, quarterly, and biannual updates, allowing clients to stay informed with the latest market trends, ongoing developments, and comprehensive market insights. The naphthalene price charts ensure our clients remain at the forefront of the industry.

Frequently Asked Questions About the Naphthalene Price Trend Report

The naphthalene prices in May 2026 were 0.61 USD/KG in Northeast Asia, 1.23 USD/KG in Europe, 1.09 USD/KG in India, and 0.8 USD/KG in North America.

The naphthalene pricing data is updated on a monthly basis.

We provide the pricing data primarily in the form of an Excel sheet and a PDF.

Yes, our report includes a forecast for naphthalene prices.

The regions covered include North America, Europe, Asia Pacific, Middle East, and Latin America. Countries can be customized based on the request (additional charges may be applicable).

Yes, we provide both FOB and CIF prices in our report.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Inquire Before Buying

Inquire Before Buying

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Why Choose Us

IMARC offers trustworthy, data-centric insights into commodity pricing and evolving market trends, enabling businesses to make well-informed decisions in areas such as procurement, strategic planning, and investments. With in-depth knowledge spanning more than 1000 commodities and a vast global presence in over 150 countries, we provide tailored, actionable intelligence designed to meet the specific needs of diverse industries and markets.

1000

+Commodities

150

+Countries Covered

3000

+Clients

20

+Industry

Robust Methodologies & Extensive Resources

IMARC delivers precise commodity pricing insights using proven methodologies and a wealth of data to support strategic decision-making.

Subscription-Based Databases

Our extensive databases provide detailed commodity pricing, import-export trade statistics, and shipment-level tracking for comprehensive market analysis.

Primary Research-Driven Insights

Through direct supplier surveys and expert interviews, we gather real-time market data to enhance pricing accuracy and trend forecasting.

Extensive Secondary Research

We analyze industry reports, trade publications, and market studies to offer tailored intelligence and actionable commodity market insights.

Trusted by 3000+ industry leaders worldwide to drive data-backed decisions. From global manufacturers to government agencies, our clients rely on us for accurate pricing, deep market intelligence, and forward-looking insights.