Modular Data Center Market Size, Share, Trends and Forecast by Component, Data Center Size, Application, Industry Vertical, and Region, 2026-2034

Modular Data Center Market Size and Share:

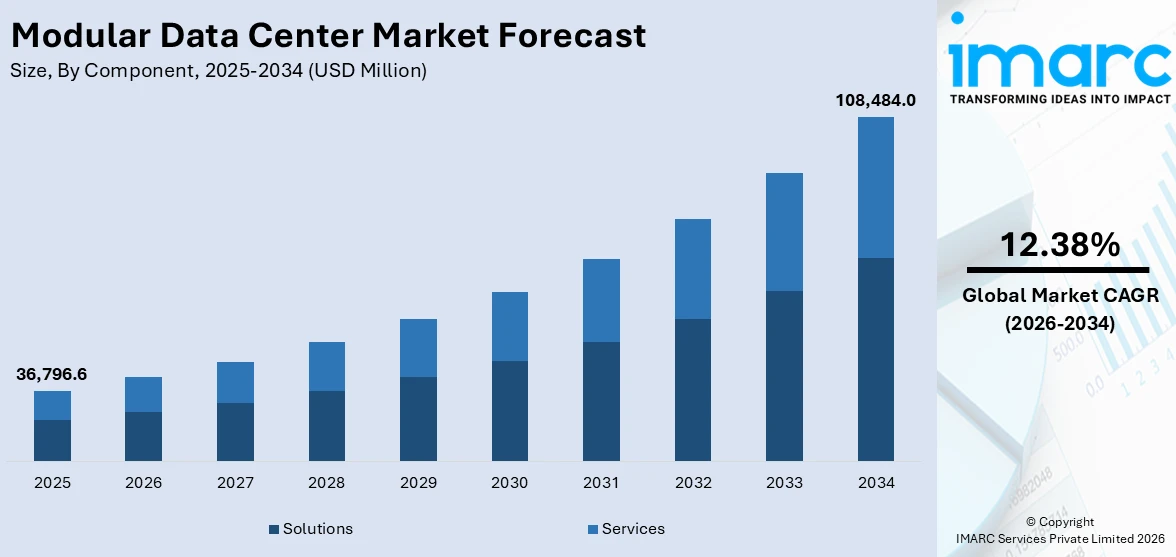

The global modular data center market size was valued at USD 36,796.6 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 108,484.0 Million by 2034, exhibiting a CAGR of 12.38% during 2026-2034. North America currently dominates the market, holding a significant market share of over 41.0% in 2025. The growing demand for scalable, energy-efficient, and rapidly deployable data center solutions, driven by cloud computing expansion, edge computing adoption, 5G rollout, artificial intelligence (AI) driven workloads, and increasing data traffic are some of the major factors augmenting the modular data center market share.

Modular Data Center Market Insights:

- The spread of AI applications is driving demand for modular data centers faster.

- Aggressive 5G rollouts and edge computing migrations fuel decentralized infrastructure demand.

- U.S. sustainability goals spur the adoption of renewable-integrated modular data solutions.

- Hybrid work model transitions boost demand for scalable data centers.

- Telecommunications growth requires low-latency, high-efficiency modular infrastructure deployments.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 36,796.6 Million |

| Market Forecast in 2034 | USD 108,484.0 Million |

| Market Growth Rate (2026-2034) | 12.38% |

The market is significantly influenced by the increasing adoption of AI-driven workloads and high-performance computing, which is fueling demand for modular data centers. Additionally, the growing environmental regulations are prompting enterprises to adopt energy-efficient data center solutions with advanced cooling technologies. According to an industry report, globally, there were more than 170 million new 5G connections in the third quarter of 2024, underscoring the rapid expansion of 5G networks. This surge, coupled with the growing adoption of edge computing, is intensifying the demand for decentralized infrastructure, driving the need for modular data centers. Also, rising cybersecurity concerns are encouraging the use of modular designs with enhanced security features, which is providing an impetus to the market. In addition to this, advancements in prefabrication techniques are improving cost-effectiveness, making modular data centers more viable for enterprises seeking operational efficiency. The growth data center modernization is an emerging modular data center market trend.

To get more information on this market Request Sample

The market in the United States is driven by the increasing adoption of government-backed digital infrastructure projects, which is accelerating the demand for modular data centers. In line with this, the growing need for resilient disaster recovery solutions is prompting enterprises to deploy modular facilities with enhanced redundancy. Besides this, the rising concerns over supply chain disruptions are propelling the demand for prefabricated, rapidly deployable data centers. Furthermore, the shift toward colocation services is further stimulating investments in modular solutions, which offer cost-effective scalability. According to industry reports, the United States targets to have zero net emissions by 2050 and focuses on reducing emissions by 50–52% below 2005 levels by 2030. Therefore, the growing emphasis on sustainability and carbon-neutral operations is encouraging enterprises to integrate modular units with renewable energy sources and efficient power management systems.

Modular Data Center Market Trends:

Expansion of Work-From-Home (WFH) and Hybrid Work Models

The shift towards remote and hybrid work models significantly increases demand for scalable, flexible, and cost-effective data infrastructure, which is enhancing the modular data center market outlook. The advent of the work-from-home (WFH) trend due to the onset of the COVID-19 pandemic resulted in the increasing demand for modular data centers for remote storage and access to organizational data. According to the IMF, remote work has increased fivefold since the pandemic. This shift has led to a 2% rise in prime-age female employment and added 2 Million disabled workers in the U.S. Office occupancy remains 50% below pre-pandemic levels. Enterprises require more distributed computing power to support remote employees, cloud-based applications, and video conferencing solutions. This trend has led to a rise in edge computing, where modular data centers play a crucial role in reducing latency and enhancing data processing capabilities closer to end users. Additionally, industries such as e-commerce, online education, and telehealth have seen rapid digital expansion, further driving the need for modular solutions that can be deployed quickly. Organizations are prioritizing decentralized IT strategies, leading to the adoption of smaller, modular units over traditional large-scale data centers. This demand is also accelerating advancements in pre-configured, prefabricated modular data centers, ensuring rapid deployment with minimal disruption.

Advancements in Telecommunications Infrastructure

The rollout of 5G networks, fiber-optic expansions, and improved satellite internet connectivity creates the need for high-performance, low-latency data processing solutions. Modular data centers are being deployed closer to telecom towers and network hubs to support the growing volume of real-time data traffic. In addition to this, the implementation of favorable government initiatives and increased investments in the telecom sector fuels the modular data center market growth. As per the IBEF, the Indian government approved an INR 12,195 Crore (USD 1.65 Billion) PLI scheme for telecom products. By December 2022, 42 companies committed INR 4,115 Crore (about USD 502.95 Million). The 2024-25 telecom budget is INR 116,342 Crore (about USD 13.98 Billion), and FDI inflows reached USD 39.32 Billion (April 2000–March 2024). Telecom providers are leveraging modular solutions to expand network capacity efficiently. Additionally, the increasing deployment of IoT devices, smart cities, and AI-driven applications has necessitated robust and adaptable data infrastructure. Enhanced telecommunication networks allow modular data centers to function as efficient edge computing nodes, reducing dependence on centralized cloud facilities. The demand for mobile and containerized data centers is also increasing, allowing telecom operators to rapidly scale operations in urban and rural areas while maintaining cost efficiency.

Growing Focus on Energy Efficiency and Sustainability

Rising concerns about data center energy consumption and environmental impact are pushing the industry toward a greener solution, which is increasing the modular data center market demand. According to an industry report, the yearly electricity usage of data centers worldwide is around half that of domestic IT gadgets, such as computers, phones, and televisions, and they contribute approximately 1% of the world's total electricity use. As demand for scalable and rapidly deployable data solutions grows, modular data centers are emerging as a key strategy for improving energy efficiency. Modern cooling systems, efficient power distribution, and integration with renewable energy sources are all features that reduce the environmental effect of these prefabricated units. Hyperscale cloud providers and enterprises are increasingly adopting prefabricated modular units with energy-efficient components, reducing overall power consumption. Many organizations are also incorporating AI-driven energy management systems that optimize power distribution and cooling in real-time. Governments and regulatory bodies are implementing stricter carbon emission regulations, prompting data center operators to shift toward sustainable infrastructure. Additionally, modular designs support power usage effectiveness (PUE) improvements, ensuring efficient energy distribution. Companies are also investing in circular economy strategies, repurposing old hardware, and integrating carbon-neutral power sources such as wind and solar energy into modular data center operations.

Modular Data Center Market Opportunities:

The modular data center market holds big opportunities since worldwide demand for scalable, efficient, and rapidly deployable IT infrastructure keeps on rising. The most promising of these is the increasing deployment of edge computing, causing the demand for localized data processing capacity. Modular data centers provide a scalable solution that can facilitate fast deployment in remote or underserved locations, and hence such solutions are extremely appealing to sectors such as telecom, energy, and healthcare. Furthermore, the growth of cloud services, AI workloads, and IoT applications is further amplifying the demand for cost-effective, agile data centers. Organizations also place greater emphasis on sustainability, and modular configurations tend to have energy-efficient infrastructure that harmonizes with green IT initiatives. Also, positive investments from private and public sectors, particularly in emerging economies, offer a rich soil for expansion. All these factors combined create opportunities for innovation and expansion in a market standing at the juncture of digital revolution.

Modular Data Center Market Challenges:

Notwithstanding its growth trend, the modular data center market has some significant challenges. A main issue is the hefty upfront capital expense involved, which could deter take-up in smaller companies or in fiscally restrained environments. Complexity in integrating with established legacy infrastructure can also interfere with effortless deployment, particularly in organizations that have not yet fully converted to modular architecture. In addition, maintaining uniform regulatory compliance across various regions compounds complexity, especially when deploying units internationally. Cybersecurity is also a critical issue, since modular units tend to be used in distributed environments, which can enhance risk if not well controlled. Moreover, the requirement for specialized technical talent in design, setup, and maintenance may pose challenges for organizations without such staff. Adoption by the market could also be hindered in areas where established brick-and-mortar data centers prevail through familiarity or previous investments. Managing these issues with effective strategies will be critical to realizing the maximum potential of modular data centers across the world.

Modular Data Center Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global modular data center market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on component, data center size, application, and industry vertical.

Analysis by Component:

- Solutions

- All-in-One Module

- Individual Module

- Services

- Design and Consulting

- Integration and Deployment

- Support and Maintenance

Solutions leads the market with around 83.8% of market share in 2025. Solutions involve the combination of essential infrastructure components such as power, cooling, management software, and security systems into pre-engineered, expandable modules. These solutions make deployment easier, minimize operational intricacies, and improve efficiency through pre-configured, tested, and optimized systems that can be deployed quickly. They are significant in making modular data centers fulfill changing enterprise requirements, accommodating high-density loads, edge computing, and disaster recovery use cases. The solutions offer end-to-end capabilities, solving issues of energy efficiency, space utilization, and quick scalability. Specialized management software further optimizes real-time monitoring, proactive maintenance, and automated resource distribution, improving performance and reliability even further. As businesses and hyperscale providers are looking for flexible, high-performance infrastructure, solution-based modular data centers are increasingly in demand, fueled by digital transformation, 5G rollout, and increasing demand for cloud and AI-based workloads.

Analysis by Data Center Size:

- Small and Medium-sized Data Centers

- Large Data Centers

Large data centers lead the market with around 76.4% of market share in 2025. Large data centers provide high-capacity, scalable infrastructures to serve enterprise, hyperscale, and cloud computing requirements. These centers comprise several modular units to offer high levels of computing power, storage, and networking functions while being energy-efficient and operationally flexible. They are significant due to their capacity to support expanding data demands from AI, big data analytics, and cloud applications. Large modular data centers provide quick deployment, less construction time, and increased redundancy in comparison to conventional data centers, which makes them best for companies that need high availability and scalability. They are also designed to be power and cooling-efficient, facilitating the sustainability agenda and low cost of operations. As edge computing and 5G networks continue to gain popularity, large modular data centers deliver centralized processing capacity with distributed computing capabilities, further solidifying their position in the market.

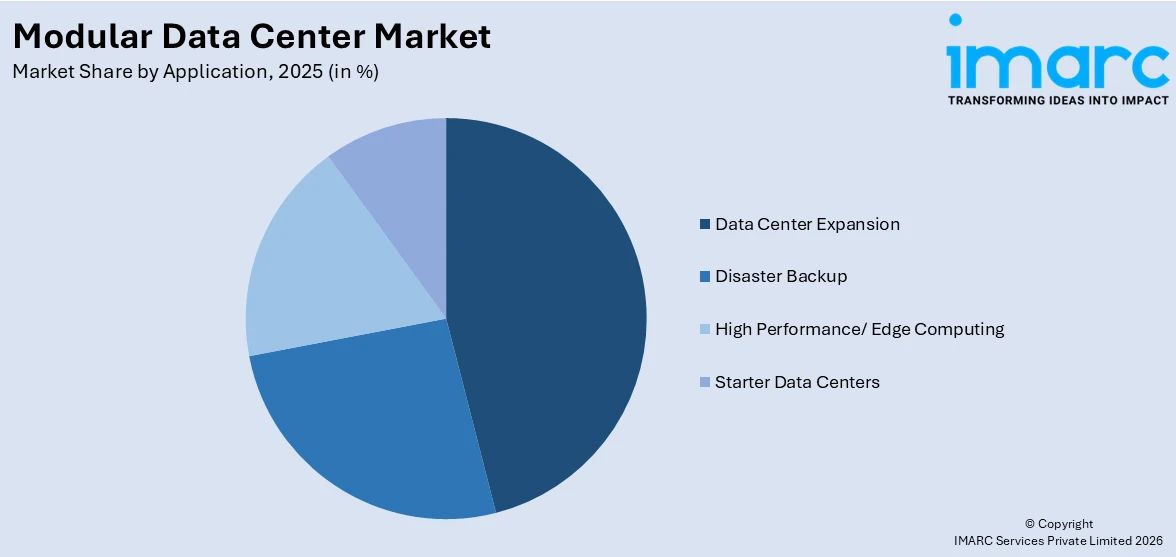

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Disaster Backup

- High Performance/ Edge Computing

- Data Center Expansion

- Starter Data Centers

Data center expansion leads the market in 2025. The segment reflects the increasing demand for highly performing, scale-up infrastructure for expanded data processing and storage capacity. Enterprises of various industries are tapping into modules to effectively double or upgrade existing data centers at a reduced time-to-market and cost, lower than deploying classic brick-and-mortar-type buildings. Modular data centers can allow businesses to extend capacity in phased steps with uninterrupted operation processes running on top of them. Their pre-engineered, standardized architecture enables quicker deployment, energy efficiency, and cost savings with high reliability. As cloud, AI, and big data workloads grow among enterprises and hyperscale operators, modular solutions enable flexible expansion to meet workload-specific requirements. They also enable sustainability initiatives by maximizing power usage effectiveness (PUE) and minimizing overall carbon footprints. With digital transformation speeding up and edge computing becoming more prominent, modular data center growth is still a key strategy for companies to upgrade their IT infrastructure with zero downtime.

Analysis by Industry Vertical:

- BFSI

- IT and Telecom

- Retail and Manufacturing

- Healthcare

- Energy

- Media and Entertainment

- Government and Defense

- Others

IT and telecom lead the market with around 27.1% of market share in 2025. The sector needs extremely scalable, reliable, and efficient infrastructure to support cloud computing, 5G networks, and data-intensive applications. Modular data centers are capable of instant deployment and flexibility, which enable telecom and IT companies to increase capacity in a short time as a reaction to growing data traffic and connectivity requirements. Prefabricated and pre-engineered, these solutions integrate smoothly with existing infrastructure while maximizing power and cooling efficiency and minimizing the cost of operation. Telecom operators utilize modular data centers to improve network coverage, facilitate edge computing, and facilitate real-time data processing for applications like IoT and AI. IT businesses also depend on these solutions to accommodate cloud services, bolster cybersecurity platforms, and handle massive computing workloads. With digital transformation speeding up and worldwide connectivity increasing, the use of modular data centers in the telecom and IT industry is increasing further, fueling innovation and infrastructure strength.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 41.0% due to swift digital transformation, cloud migration, and the growing need for scalable IT infrastructure. The region hosts leading hyperscale cloud vendors, colocation data centers, and enterprises needing high-performance computing solutions. Increased adoption of 5G networks, AI-based applications, and edge computing also increase the pace of modular data center adoption with the benefits of fast deployment, energy efficiency, and economical scalability. Green data center initiatives by the government and rigorous data security compliance further drive market growth. The U.S. dominates the region with a high level of investment in cloud infrastructure, followed by Canada which is witnessing surging demand for modular data centers as a measure to meet increased data localization mandates. With firms focusing on speed and efficiency while expanding data centers, North America continues to be a prime region in the market.

Key Regional Takeaways:

United States Modular Data Center Market Analysis

The United States holds a substantial share of the North America modular data center market with 85.40% of market share in 2025. The market in the United States is significantly driven by the rapid expansion of hyperscale cloud providers, AI-driven workloads, and edge computing demands. Major players are increasingly adopting modular data center solutions to accelerate construction timelines while ensuring energy efficiency and sustainability. The U.S. government’s initiatives promoting clean energy and carbon neutrality are further fueling market growth, with companies integrating liquid cooling and prefabricated modular units to optimize power consumption and reduce operational costs. Strong investments in 5G infrastructure and enterprise digital transformation are increasing the need for scalable, pre-built data center modules. For instance, on May 20, 2024, Ericsson announced a USD 50 Million expansion of its 5G Smart Factory in Lewisville, Texas, following its USD 100 Million investment since 2020. The 300,000 sq. ft. facility, employing 500+ workers, will accelerate 5G infrastructure production, including Massive MIMO radios and RAN Compute. This expansion aligns with the Build America, Buy America Act (BABAA) and strengthens U.S. 5G leadership amid growing connectivity demands. Additionally, rising data security concerns and localized processing needs are driving edge computing, supporting modular data center demand. Moreover, AI and machine learning adoption further expand the sector, requiring scalable, efficient, high-performance infrastructure.

Europe Modular Data Center Market Analysis

The European market is experiencing strong growth, propelled by stringent environmental regulations, energy efficiency mandates, and rising AI adoption. As per reports, in 2024, 13.5% of EU enterprises (10+ employees) used AI technologies, marking a 5.5 percentage point increase from 8.0% in 2023. Similarly, AI usage increased across all EU nations, reinforcing the demand for scalable, high-performance infrastructure. Countries such as Germany, the UK, France, and the Netherlands are leading modular data center deployments, integrating sustainable solutions, liquid cooling, and heat reuse. The European Green Deal and climate neutrality targets are accelerating the shift towards low carbon, prefabricated modular infrastructure, which enhances energy efficiency and reduces construction time. The rise of colocation providers and cloud expansion is further fueling demand for cost-effective solutions that optimize operational costs. Furthermore, the expanding 5G networks in Europe drive localized data processing, boosting modular edge data center adoption in telecom, finance, and healthcare. As AI workloads grow, the demand for high-density, power-efficient modular data centers will continue to rise.

Asia Pacific Modular Data Center Market Analysis

The modular data center market in Asia-Pacific (APAC) is witnessing growth due to the rapid digitalization, cloud services rise, and government infrastructure initiatives. China, India, Japan, and South Korea lead investments in prefabricated modular data centers to meet rising demand for AI computing, 5G networks, and edge processing. The booming e-commerce and fintech sectors require low-latency, high-density computing solutions, making modular designs increasingly attractive. According to an industry report, India's fintech sector ranked second globally in Q3 2024 funding, attracting USD 778 Million (+66% YoY). Alternative lending led with USD 517 Million, followed by investment tech (USD 109 Million) and payments (USD 93 Million). India hosts 12,894 fintech firms, valued at USD 125 Billion, with 1 decacorn, 25 unicorns, and 87 soonicorns. UPI transactions reached USD 15.04 billion (INR 20.64T) in September 2024. China’s dual-carbon goals and India’s data localization policies are accelerating adoption of energy-efficient, scalable data center solutions. With AI-driven applications and gaming industry expansion, modular data centers must scale rapidly, supporting growth in urban tech hubs and Tier 2 cities.

Latin America Modular Data Center Market Analysis

The Latin American market is growing steadily, fueled by cloud computing, AI, and digital transformation investments. Brazil, Mexico, and Chile lead in hyperscale and colocation expansion to meet rising digital service demands. Similarly, 5G deployment and regulatory compliance are accelerating modular data center adoption, particularly in finance, e-commerce, and telecom. According to 5G Americas, 5G connections in Latin America reached 67 Million in Q3 2024, with 11 Million new connections (+19%), while 4G LTE remains dominant, serving 592 Million users (74% of total wireless connections). The region’s susceptibility to natural disasters makes modular, resilient infrastructure essential for disaster recovery. Startups and tech-driven businesses are increasing demand for scalable, cost-efficient solutions, though power supply issues and rural connectivity gaps remain challenges. North American and European investments are expected to further drive market expansion.

Middle East and Africa Modular Data Center Market Analysis

The Middle East and Africa (MEA) modular data center market is growing due to cloud computing, AI, and smart city projects. The UAE, Saudi Arabia, and South Africa lead demand, driven by Saudi Vision 2030 and UAE’s artificial intelligence (AI) strategy. As per the International Trade Administration, Saudi Arabia’s Information and Communications Technology (ICT) sector was valued at USD 40.94 Billion (2023), contributing 4.1% of GDP, with USD 24.8 Billion invested in digital infrastructure, achieving 99% internet penetration and 215 Mbps mobile speeds. The region’s harsh climate makes modular data centers attractive for energy-efficient cooling and extreme temperature adaptability. Africa’s rising internet penetration and mobile payments sector further drive modular adoption, offering scalability and cost-efficiency in emerging markets. Microsoft and AWS are expanding their hyperscale presence across key urban and tech hubs, accelerating regional data center investments.

Competitive Landscape:

The market for modular data centers is competitive, fueled by ongoing innovation in design, cooling systems, and energy efficiency. Players in the market are interested in creating prefabricated, scalable, and deployable solutions quickly to address increasing demand from different industries such as IT, BFSI, healthcare, and telecom. Developments in liquid cooling, artificial intelligence (AI)-based automation, and integration with renewable energy sources are defining competition. Firms invest in mergers, acquisitions, and strategic partnerships to increase market reach and technology capabilities. The market also experiences robust research and development (R&D) activities to make modular architectures better suited for edge computing and high-density workload purposes. Pricing models, customization, and data security compliance standards also separate players in this dynamic landscape, where speed, efficiency, and sustainability are key drivers for the market.

The report provides a comprehensive analysis of the competitive landscape in the modular data center market with detailed profiles of all major companies, including:

- BASELAYER Technology LLC (Intermountain Electronics Inc.)

- Cannon Technologies Ltd

- Dell Technologies Inc.

- Eaton Corporation plc

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co. Ltd.

- International Business Machines Corporation

- Rittal GmbH & Co. KG

- Schneider Electric SE

- Vertiv Group Corp.

Latest News and Developments:

- December 2024: Siemens and Compass Datacenters signed a five-year agreement to deliver 1,500 modular medium-voltage skid units, accelerating data center construction and reducing costs. The first deployment will be at Compass' Chicago campus in late 2025, enhancing efficiency, scalability, and sustainability for hyperscale and cloud customers.

- July 2024: Vertiv launched the MegaMod CoolChip, a high-density prefabricated modular AI data center with liquid cooling, reducing deployment time by 50%. It supports hundreds of kW per row, integrates Vertiv power and cooling technologies, and enhances energy efficiency for AI-ready infrastructure worldwide.

- June 2024: HPE and Danfoss launched a modular data center with heat recovery, cutting energy use by 20% and cooling needs by 30%. With a PUE of 1.14, it reuses excess heat for buildings, enabling faster AI deployments and decarbonization through efficient liquid cooling and energy recycling.

- March 2024: Nautilus Data Technologies launched EcoCore, a 2.5MW modular data center with liquid cooling and high-density support. The first deployment will be at Start Campus in Portugal, enhancing data hall cooling. The system features N+1 redundancy and 833kW heat rejection per CDU unit, ensuring efficiency and sustainability.

- March 2024: Eaton launched SmartRack, a modular data center with 150kW capacity, designed for AI and edge computing. It supports rapid deployment in days, offers 13 standard configurations, integrates pre-built cooling, and includes Eaton’s PDUs, UPSs, and remote monitoring software for efficient power management.

Modular Data Center Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Data Center Sizes Covered | Small and Medium-sized Data Centers, Large Data Centers |

| Applications Covered | Disaster Backup, High Performance/ Edge Computing, Data Center Expansion, Starter Data Centers |

| Industry Verticals Covered | BFSI, IT and Telecom, Retail and Manufacturing, Healthcare, Energy, Media and Entertainment, Government and Defense, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | BASELAYER Technology LLC (Intermountain Electronics Inc.), Cannon Technologies Ltd, Dell Technologies Inc., Eaton Corporation plc, Hewlett Packard Enterprise Development LP, Huawei Technologies Co. Ltd., International Business Machines Corporation, Rittal GmbH & Co. KG, Schneider Electric SE, Vertiv Group Corp., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the modular data center market from 2020-2034.

- The modular data center market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the modular data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Modular Data Center Market Report

The modular data center market was valued at USD 36,796.6 Million in 2025.

The modular data center market is projected to exhibit a CAGR of 12.38% during 2026-2034, reaching a value of USD 108,484.0 Million by 2034.

The market is driven by increasing demand for scalable and energy-efficient data centers, rising adoption of cloud computing and edge computing, rapid digital transformation, and stringent regulatory standards for data security. Growing investments in AI, IoT, and 5G infrastructure further boost modular data center adoption, ensuring flexibility, speed, and cost-effectiveness in deployment.

North America currently dominates the modular data center market, accounting for a share of 41.0% in 2025. The dominance is fueled by strong cloud adoption, rising AI-driven workloads, increased hyperscale data center deployments, and government initiatives supporting green data centers. The presence of leading tech firms and high internet penetration further contribute to market expansion.

Some of the major players in the modular data center market include BASELAYER Technology LLC (Intermountain Electronics Inc.), Cannon Technologies Ltd, Dell Technologies Inc., Eaton Corporation plc, Hewlett Packard Enterprise Development LP, Huawei Technologies Co. Ltd., International Business Machines Corporation, Rittal GmbH & Co. KG, Schneider Electric SE and Vertiv Group Corp., among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)