Mobile Gamma Cameras Market Size, Share, Trends and Forecast by Product, Application, End User, and Region, 2025-2033

Mobile Gamma Cameras Market Size and Share:

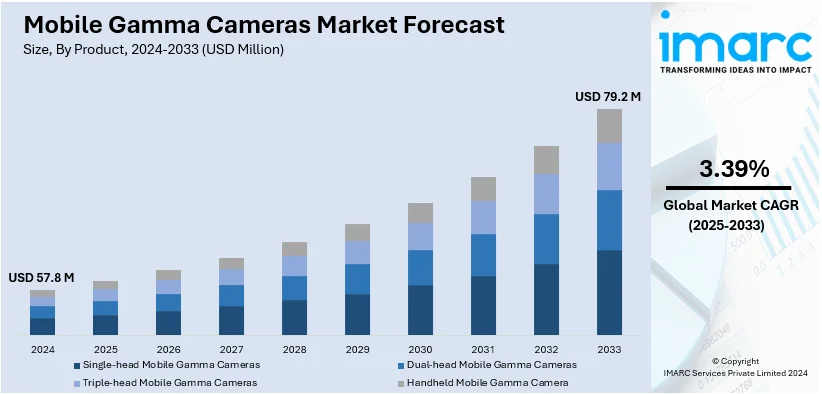

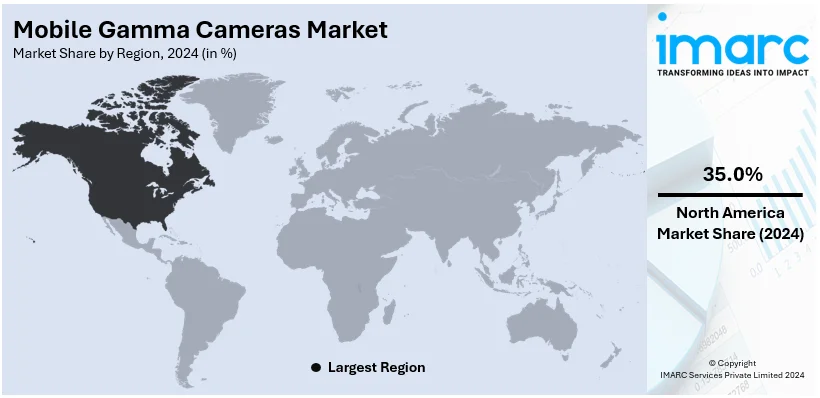

The global mobile gamma cameras market size was valued at USD 57.8 Million in 2024. Looking forward, IMARC Group estimates the market to reach USD 79.2 Million by 2033, exhibiting a CAGR of 3.39% from 2025-2033. North America currently dominates the market, holding a market share of over 35.0% in 2024. The advancements in medical imaging technology, rising prevalence of chronic diseases, increasing demand for portable diagnostic devices, growing adoption in oncology and cardiology applications, and supportive government healthcare initiatives are some of the factors driving the market in North America.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2024

|

|

Forecast Years

|

2025-2033

|

|

Historical Years

|

2019-2024

|

| Market Size in 2024 | USD 57.8 Million |

| Market Forecast in 2033 | USD 79.2 Million |

| Market Growth Rate (2025-2033) | 3.39% |

The market for mobile gamma cameras is supported by the growing incidence of cancer and cardiovascular disease. The increased demand for these devices is increasing as they are portable for use in an outpatient facility or a centralized site at the health care center. It is also more flexible than traditional gamma cameras for providing service in different clinical settings.

To get more information on this market, Request Sample

Improvements in imaging modalities have an important role, such as improvements in spatial resolution and integrating the imaging modalities with digital systems. Moreover, the increase in the elderly population, which is known as a high-risk group for developing chronic disease conditions, encourages the demand for efficient and simply available diagnostics.

The United States has emerged as a key region for mobile gamma cameras. The increasing prevalence of chronic diseases, such as cancer and cardiovascular disorders, that require an early and accurate diagnosis for better management, is increasing the use of portable gamma cameras. It will give them mobility and ease of handling to be used in different types of healthcare facilities, including outpatient and emergency departments. Another factor is the recognized potential of nuclear medicine with regard to diagnosis, alongside advances such as higher resolution and software integration. Moreover, the elderly population of the U.S. drives high demand for mobile gamma cameras due to their vulnerability to chronic diseases. The nature of the technology has made it possible for government and health service providers to focus on cost-effective diagnostic measures while further driving the pushes into advanced medical imaging technologies by government initiatives, which are essential boosts in the favor of the market.

Mobile Gamma Cameras Market Trends:

Increasing prevalence of chronic diseases

The market is driven by the increasing prevalence of chronic diseases. According to the WHO, noncommunicable diseases (NCDs) are responsible for 41 Million deaths annually, accounting for 74% of all global fatalities. Besides this, the growing incidences of cancer and a considerable rise in the requirement for gamma camera devices during radio-guided surgery are driving the product demand on the global level. As per the WHO, cancer ranks among the leading causes of death globally, claiming approximately 10 Million lives in 2020, which is about 1 in every 6 deaths. In line with this, continual technological advancements in medical imaging options, such as nuclear imaging and the emergence of solid-state technology, are positively impacting the market. The growing trend of miniaturization of medical devices is acting as another significant growth-inducing factor for the market. The market is further driven by the increasing healthcare expenditure across the globe. Some of the other factors that are providing an impetus to the mobile gamma cameras market growth include the inflating disposable incomes of the masses, the rising product awareness, significant improvements in the healthcare sector and extensive research and development (R&D) activities conducted by key players.

Technological advancements

Advancements in imaging technology have proven to be instrumental in driving the market for mobile gamma cameras. Modern gamma cameras offer enhanced resolution, the ability to carry them from one point to another, and sophisticated data processing that helps produce precise diagnostic imaging. Innovative technologies like solid-state detectors, high-energy collimators, software integration have revolutionized the field with their promises of better image quality and rapid results. All of these things support the growing inclination toward minimally invasive diagnostic techniques, especially in oncology and cardiology, where early and accurate identification is imperative. Moreover, artificial intelligence and machine learning embedded into the system act as real-time interpreters of images to improve diagnosis accuracy. Healthcare service providers are increasingly embracing the technology to enhance operational efficiency and solve the health problems related to patient outcome improvement, diagnostic errors, and workflow management. With continued research and development efforts, technology remains the foundation for most growth within the mobile gamma cameras market as it takes advanced imaging technology to more healthcare option venues.

Shift toward portable and point-of-care solutions

The healthcare industry's shift toward portable and point-of-care diagnostic solutions is another key factor driving the mobile gamma cameras market. Traditional gamma cameras are often stationary and require dedicated imaging suites, limiting their accessibility. Mobile gamma cameras, however, offer flexibility, enabling imaging at the patient’s bedside, in outpatient settings, or in emergency scenarios. This mobility is particularly valuable in critical care units and for patients with mobility constraints. Moreover, the growing emphasis on reducing healthcare costs and improving operational efficiency is accelerating the adoption of portable imaging solutions. Mobile gamma cameras also support decentralized healthcare models by bringing advanced diagnostic capabilities closer to patients, especially in rural or resource-limited settings. The ability to perform real-time diagnostics without extensive infrastructure requirements aligns with current healthcare trends, making mobile gamma cameras an increasingly attractive choice for both developed and developing markets.

Mobile Gamma Cameras Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global mobile gamma cameras market, along with forecast at the global, regional, and country levels from 2025-2033. The market has been categorized based on product, application and end user.

Analysis by Product:

- Single-head Mobile Gamma Cameras

- Dual-head Mobile Gamma Cameras

- Triple-head Mobile Gamma Cameras

- Handheld Mobile Gamma Camera

Single-head mobile gamma cameras hold the largest mobile gamma cameras market share of 62.9% in 2024. This is due to their cost-effectiveness, versatility, and widespread adoption in various clinical applications. These systems are significantly less expensive than dual- or triple-head cameras, making them an economical choice for small to mid-sized healthcare facilities, especially in resource-constrained settings. The affordability of single-head units allows hospitals and diagnostic centers to invest in nuclear imaging technology without substantial capital expenditure. Moreover, single-head cameras are highly versatile, catering to a broad range of diagnostic needs, including thyroid scans, bone scintigraphy, renal imaging, and cardiac studies. Their portability and compact design make them ideal for point-of-care settings, enabling bedside imaging and use in outpatient clinics, emergency rooms, and rural healthcare centers.

Analysis by Application:

- Cardiac Imaging

- Breast Imaging

- Thyroid Scanning

- Kidney Scanning

- Intraoperative Imaging

- Brain Imaging

- Others

Thyroid scanning dominates the market due to its critical role in diagnosing and monitoring thyroid disorders, which are increasingly prevalent worldwide. Conditions such as hypothyroidism, hyperthyroidism, thyroid nodules, and thyroid cancer necessitate accurate imaging for effective management. Mobile gamma cameras, equipped with advanced nuclear imaging capabilities, provide precise visualization of thyroid gland function and structure by detecting the uptake of radioactive isotopes like iodine-123 or technetium-99m. The portability of these cameras enhances accessibility, making thyroid scanning feasible in outpatient settings, rural areas, and point-of-care environments. This is particularly crucial as thyroid disorders are often underdiagnosed, especially in regions with limited healthcare infrastructure. Furthermore, the non-invasive and cost-effective nature of thyroid scans aligns with the increasing demand for affordable diagnostic solutions.

Analysis by End User:

- Hospitals

- Ambulatory Surgical Centers

- Research Centers

- Imaging Centers and Clinics

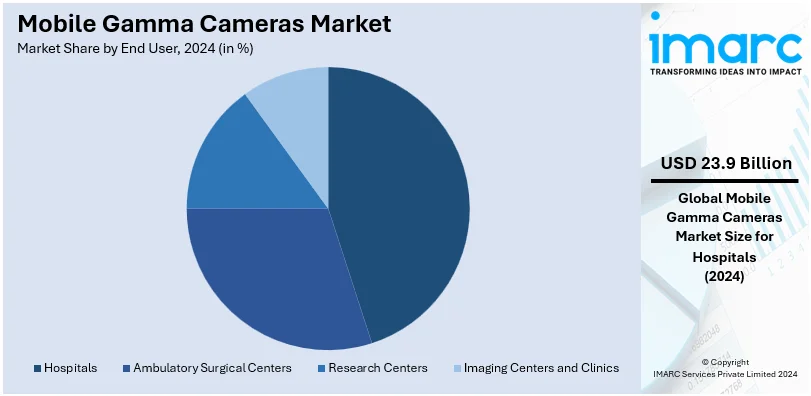

In 2024, hospitals hold the largest market share with 41.3% share due to their extensive infrastructure, large patient volume, and diverse diagnostic requirements. As primary centers for healthcare delivery, hospitals frequently manage complex and critical cases, including oncology, cardiology, and neurology, where gamma imaging is crucial for diagnosis, treatment planning, and monitoring. The availability of skilled professionals, such as nuclear medicine specialists and radiologists, further supports the widespread use of these devices in hospital settings. Moreover, hospitals often have greater financial capacity to invest in advanced diagnostic equipment like mobile gamma cameras.

Regional Analysis:

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2024 North America leads the market with 35.0% share. Some of the factors include advanced health care infrastructure, increased health care expenditure, and the speedy adoption of modern medical technologies. The well-established hospitals and diagnostic centers in the region are equipped with state-of-the-art imaging facilities to provide accurate treatment and diagnosis, hence creating a great need to acquire mobile gamma cameras. North America has the highest prevalence of chronic diseases, for instance, cancer and cardiovascular disorders, which compels the need for new advanced diagnostic tools like gamma cameras. The aging population of the region also necessitates the increased use of these portable imaging solutions for elderly patients who undergo frequent routine diagnostic assessments but may find it difficult to go to a hospital or facility.

Key Regional Takeaways:

United States Mobile Gamma Cameras Market Analysis

In 2024, the United States accounts for 83.9% of mobile gamma cameras market in North America. The market in the United States is driven by the increasing prevalence of chronic diseases, with an estimated 129 Million people affected by at least one major chronic condition, such as heart disease, cancer, diabetes, obesity, or hypertension, as defined by the US Department of Health and Human Services. This growing burden of disease has led to higher demand for advanced diagnostic imaging technologies. Mobile gamma cameras offer the flexibility to be used across various healthcare settings, including hospitals, clinics, and remote locations, improving access to diagnostic services for patients. Additionally, technological advancements in mobile gamma cameras, such as improved image resolution and faster scanning capabilities, are contributing to market growth. The push for cost-effective healthcare solutions further drives the adoption of mobile imaging systems, as they reduce the need for expensive fixed infrastructure. Favorable reimbursement policies for nuclear medicine procedures and the growing awareness of early disease detection and personalized treatment are also expected to support market expansion. Furthermore, the demand for mobile gamma cameras is anticipated to rise as early diagnosis and treatment of chronic conditions become increasingly prioritized in healthcare systems.

Asia Pacific Mobile Gamma Cameras Market Analysis

The mobile gamma cameras market in the Asia Pacific (APAC) region is experiencing growth due to the rising prevalence of chronic diseases and respiratory infections. According to PubMed Central, respiratory infections alone account for 475,000 deaths, representing 16.8% of total deaths in the region. Chronic conditions such as cancer, cardiovascular diseases, and diabetes are also on the rise, particularly in countries like China, India, and Japan. Mobile gamma cameras offer a vital solution, providing flexible diagnostic options in hospitals, outpatient clinics, and remote areas where healthcare access is limited. Government investments in healthcare infrastructure and increasing awareness of the benefits of early disease detection are expected to drive the demand for these mobile systems. Furthermore, advancements in technology, making mobile gamma cameras more affordable and efficient, contribute to their growing adoption across APAC.

Europe Mobile Gamma Cameras Market Analysis

In Europe, the mobile gamma cameras market is growing due to the rising prevalence of chronic diseases, which are becoming more prominent in an aging population. As of January, 2023, the EU population was estimated at 448.8 Million, with more than one-fifth (21.3%) aged 65 years and over, according to Eurostat. This demographic shift is leading to an increase in age-related chronic conditions such as cancer, cardiovascular diseases, and neurological disorders, which drive the demand for advanced diagnostic tools. Mobile gamma cameras provide flexible solutions for hospitals, outpatient clinics, and remote healthcare facilities, especially in rural areas where access to fixed imaging infrastructure is limited. The ability to conduct imaging on-site offers cost-effective healthcare alternatives, which is particularly important in light of Europe's strained healthcare budgets. Moreover, advancements in technology, including improved image resolution and faster scanning capabilities, further boost market growth. With increasing government investments in healthcare infrastructure and the push for personalized medicine, mobile gamma cameras are becoming an essential tool in early disease detection and monitoring across the region.

Latin America Mobile Gamma Cameras Market Analysis

The mobile gamma cameras market in Latin America is expanding due to the increasing burden of chronic diseases, with Brazil estimating 928,000 deaths annually from chronic conditions such as heart disease, diabetes, and cancer, according to PubMed Central. This rising mortality rate drives the need for advanced diagnostic tools. Additionally, limited access to healthcare in rural areas creates demand for portable imaging solutions. Government efforts to improve healthcare infrastructure, along with the growing adoption of mobile health technologies, further support market growth. Mobile gamma cameras offer a cost-effective and accessible alternative for early disease detection in the region.

Middle East and Africa Mobile Gamma Cameras Market Analysis

The mobile gamma cameras market in the Middle East and Africa is growing due to the increasing demand for advanced healthcare solutions, particularly in the UAE, Saudi Arabia, and South Africa. These regions have strong investments in healthcare infrastructure, and mobile gamma cameras offer a flexible and scalable solution to expand diagnostic services. For instance, according to the World Economic Forum, healthcare expenditure in the Gulf Cooperation Council (GCC) is predicted to reach USD 135.5 Billion by 2027. Mobile gamma cameras provide portable, cost-effective alternatives to traditional imaging methods, improving access to healthcare in remote areas. Government efforts to expand healthcare infrastructure further support market growth in the region.

Competitive Landscape:

Key players are focusing on developing innovative and advanced mobile gamma cameras to meet the growing demand for precision and portability in diagnostic imaging. They are incorporating features such as solid-state detectors, improved energy resolution, and artificial intelligence (AI)-powered imaging software to improve diagnostic efficiency and accuracy . Companies are also designing compact, lightweight, and user-friendly models to cater to point-of-care applications, ensuring wider adoption across diverse healthcare settings. These advancements allow market leaders to differentiate their products and appeal to a broader customer base. Moreover, collaborations with hospitals, research institutions, and nuclear medicine centers are enabling key players to expand their market presence and access new opportunities. Partnerships with technology providers help integrate cutting-edge software and data analytics capabilities into gamma camera systems. Additionally, collaborations with healthcare providers foster trust and brand loyalty, ensuring a steady demand for their products.

The report provides a comprehensive analysis of the competitive landscape in the mobile gamma cameras market with detailed profiles of all major companies, including:

- CMR Naviscan Corporation

- Crystal Photonics GmbH

- Mediso Ltd.

- MiE GmbH

- NUVIATech Instruments

- Oncovision

- Southern Scientific Ltd.

- Spectrum Dynamics Medical

- TTG Imaging Solutions

Latest News and Developments:

- October 2024: Serac Imaging Systems announced that the University of Malaya Medical Centre has presented initial findings on the clinical feasibility of Seracam®, a portable gamma-optical camera, for sentinel lymph node imaging in breast cancer. The results, shared at IPET 2024 in Vienna, highlight Seracam®'s advantage over standard gamma probes by providing visual imaging alongside gamma radiation detection, addressing limitations such as the lack of anatomical context and precision in node localization.

- August 2024: Royal Shrewsbury Hospital has launched a new gamma camera, part of a EUR 3.6 Million (USD 4 Million) investment by the Shrewsbury and Telford NHS Trust to enhance cancer and acute condition diagnostics. The advanced camera improves image quality, reduces waiting times, and supports expanded imaging services. Operated by a specialized Nuclear Medicine team, the facility aims to improve patient care and attract skilled professionals, securing the future of diagnostic services in the region.

- February 2024: M3D, Inc., a Michigan-based company, has received investment from Michigan Rise Pre-Seed Fund III to advance its gamma radiation detection cameras. The company is developing two products: a radiation detection camera for safety and compliance, and an intraoperative surgical camera. The investment will help finalize the design and conduct field testing, with the safety camera expected to be ready for commercial release by mid-2024.

Mobile Gamma Cameras Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2024 |

| Historical Period | 2019-2024 |

| Forecast Period | 2025-2033 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Single-head Mobile Gamma Cameras, Dual-head Mobile Gamma Cameras, Triple-head Mobile Gamma Cameras, Handheld Mobile Gamma Camera |

| Applications Covered | Cardiac Imaging, Breast Imaging, Thyroid Scanning, Kidney Scanning, Intraoperative Imaging, Brain Imaging, Others |

| End Users Covered | Hospitals, Ambulatory Surgical Centers, Research Centers, Imaging Centers and Clinics |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | CMR Naviscan Corporation, Crystal Photonics GmbH, Mediso Ltd., MiE GmbH, NUVIATech Instruments, Oncovision, Southern Scientific Ltd., Spectrum Dynamics Medical, TTG Imaging Solutions, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the mobile gamma cameras market from 2019-2033.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global mobile gamma cameras market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the mobile gamma cameras industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

Mobile gamma cameras are portable imaging devices used in nuclear medicine to capture gamma radiation emitted by radioactive tracers administered to patients. These cameras are designed for convenience and mobility, enabling their use in various clinical settings, including operating rooms, emergency departments, and bedside procedures. They are particularly valuable for on-the-spot diagnostics or when transporting patients to fixed imaging facilities is impractical.

The mobile gamma cameras market was valued at USD 57.8 Million in 2024.

IMARC estimates the global mobile gamma cameras market to exhibit a CAGR of 3.39% during 2025-2033.

The market is primarily driven by advancements in medical imaging technology, rising prevalence of chronic diseases, increasing demand for portable diagnostic devices, growing adoption in oncology and cardiology applications, and supportive government healthcare initiatives.

In 2024, single-head mobile gamma cameras represented the largest segment driven by their cost-effectiveness, versatility, and widespread adoption in various clinical applications.

Thyroid scanning leads the market owing to its critical role in diagnosing and monitoring thyroid disorders, which are increasingly prevalent worldwide.

Hospitals are the leading segment due to their extensive infrastructure, large patient volume, and diverse diagnostic requirements.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein North America currently dominates the global market.

Some of the major players in the global mobile gamma cameras market include CMR Naviscan Corporation, Crystal Photonics GmbH, Mediso Ltd., MiE GmbH, NUVIATech Instruments, Oncovision, Southern Scientific Ltd., Spectrum Dynamics Medical, TTG Imaging Solutions, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)