Metal Powder Market Size, Share, Trends and Forecast by Material, Technology, Application, and Region, 2026-2034

Metal Powder Market Size and Share:

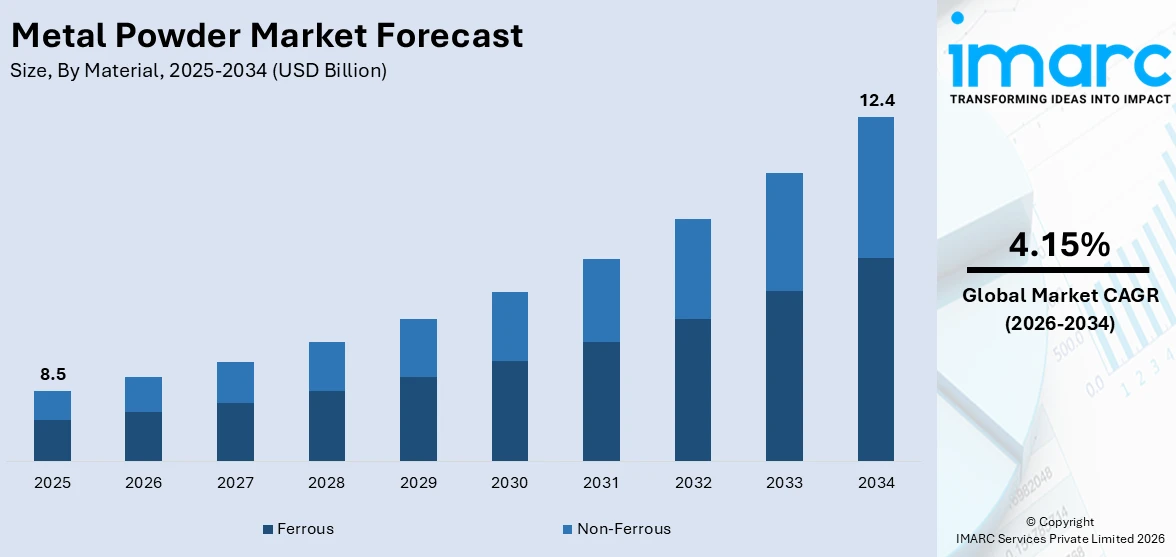

The global metal powder market size reached USD 8.5 Billion in 2025. The market is projected to reach USD 12.4 Billion by 2034, exhibiting a growth rate (CAGR) of 4.15% during 2026-2034. The market growth is attributed to growing demand for light components in the aerospace and automotive sectors, growing use of additive manufacturing, advances in powder metallurgy technologies, and requirements for cost-efficient, high-performance materials in different industrial applications.

Market Insights:

- Asia Pacific dominated the metal powder market in 2025.

- On the basis of material, the ferrous segment leads the market in 2025.

- Based on technology, the pressing and sintering segment leads the market in 2025.

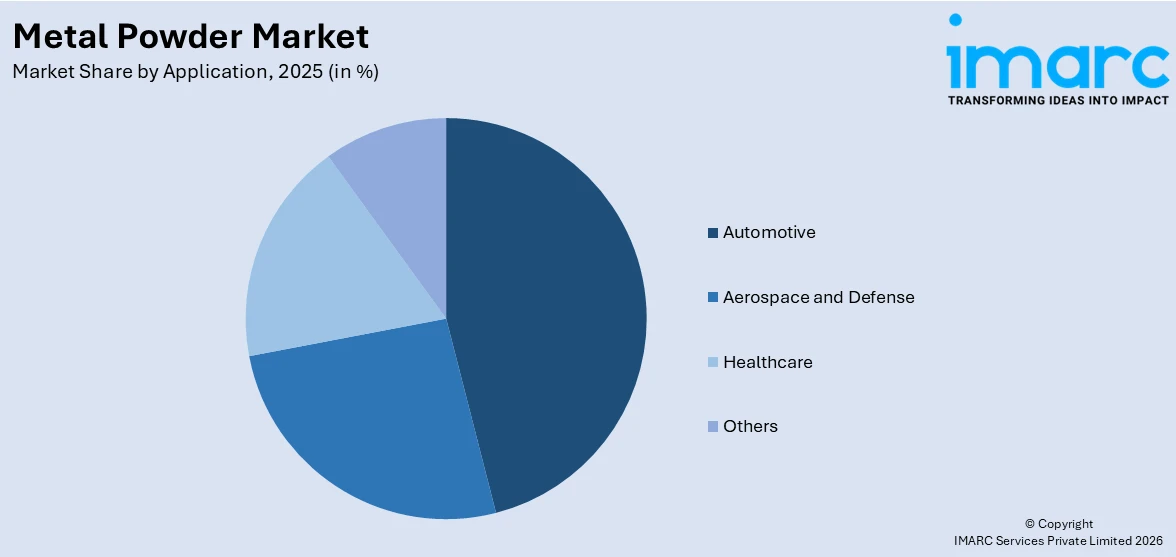

- On the basis of application, the automotive segment leads the market in 2025.

Market Size & Forecast:

- 2025 Market Size: USD 8.5 Billion

- 2034 Projected Market Size: USD 12.4 Billion

- CAGR (2026-2034): 4.15%

- Asia Pacific: Largest market in 2025

Metal powders are alloys of metals that are processed into a fine and grain-like powder through several processes, such as atomization, chemical, electrolysis, and solid-state reduction. They are manufactured from stainless steel, brass, copper, iron, and bronze to achieve the desired material properties and characteristics for a particular application. They consume less energy, improve material utilization, and contain fewer steps during the manufacturing process. They are used to produce complex geometries, such as irregular curves, radial projections, keyways, splines, counterbores, bosses, and axial projections. They are also employed in powder metallurgy to make metal parts and components by heating compacted powdered metals below the melting point. They offer reduced manufacturing time, cost efficiency, high volume capability, minimal wastage, and enhanced recyclability. As a result, metal powders find applications in chemical processes, food supplements and additions, friction materials, magnetic composites, polymer filtration, printing, surface coatings, and welding.

To get more information on this market Request Sample

The market is dominated significantly by the ever-growing demand for high-strength and lightweight materials in the aerospace and automotive industries, which has fueled the growth of metal powder adoption. In addition, growing interest in reducing energy consumption and material wastage in production processes increases the attractiveness of metal powders due to their low wastage and recyclability. According to industry reports, in many high-income countries, approximately 80% of the public resides in urban areas. Moreover, upper-middle-income nations have urban dwellers, making up between 50% and 80%. Urbanization and industrialization at a high rate in emerging markets fuel demand for sophisticated metal-based products used in construction and heavy equipment. Despite favorable growth opportunities, there are significant challenges confronting the market. One of the key concerns is the excessive cost of producing advanced metal powders, especially those applied in additive manufacturing and aerospace industries. This discourages their use in price-sensitive industries. Nevertheless, as per metal powder market analysis, constant improvements in manufacturing technologies, including plasma atomization and gas atomization, are proving to minimize the cost of manufacturing while optimizing powder quality. Thus, making metal powders more affordable in various applications across industries.

Metal Powder Market Trends:

At present, there is a rise in the utilization of metal powders to manufacture gears, shock absorbers, anti-lock braking systems (ABS), exhaust systems, chassis components, variable valve timing systems, exhaust gas recirculation (EGR) systems, and turbochargers. This, along with the increasing demand for metal powders to produce lightweight parts in the automotive industry, represents one of the key factors supporting the growth of the market. In addition, the growing employment of iron powder for making brake pads and magnetic products to lower brake weight, minimize noise, and reduce material usage is positively influencing the market. Besides this, the escalating demand for metal powders to improve the bulk properties of complex components, such as reactivity, flow ability, compressibility, porosity, and hardenability, is propelling the growth of the market. Moreover, there is an increase in the demand for structural components in various applications, such as agriculture machinery, motorcycles, and home appliances, around the world. This, coupled with the growing demand for lighter and thinner components with higher dimensional precision, sintering, and thermal processing, is offering a favorable market outlook. Apart from this, the increasing application of metal powders in electronic devices, such as electric car batteries and electronic gadgets, is strengthening the growth of the market. Additionally, the rising demand for metal powders in the healthcare industry to produce connecting and blacking plates, surgery blades, forceps, graspers, and blacking hooks is bolstering the growth of the market.

Key Market Segmentation:

IMARC Group provides an analysis of the key trends in each sub-segment of the global metal powder market report, along with forecasts at the global, regional and country level from 2026-2034. Our report has categorized the market based on material, technology and application.

Material Insights:

- Ferrous

- Non-Ferrous

The report has provided a detailed breakup and analysis of the metal powder market based on the ferrous and non-ferrous. This includes ferrous and non-ferrous. According to the report, ferrous represented the largest segment.

Ferrous products are extensively used in industries, and it is known for their affordability. Constituting iron and its alloys, ferrous powders find widespread applications in powder metallurgy to produce vehicle parts, machinery elements, and structural parts because they have superior mechanical strength, wear resistance, and magnetic character. The motor vehicle sector, specifically, depends greatly on ferrous powders for manufacturing gears, bearings, and sintered components, aiding fuel efficiency and weight reduction programs. Additionally, the increasing use of additive manufacturing and 3D printing technology has further boosted the demand for high-quality ferrous powders, such as stainless steel and tool steel types. Their recyclability, ease of processability, and versatility to different fabrication methods also enhance their demand in various end-use applications. As industries tend towards greater emphasis on sustainability and cost savings, the role of ferrous materials grows even stronger, solidifying their leading position worldwide.

Technology Insights:

- Pressing and Sintering

- Metal Injection Molding

- Additive Manufacturing

- Others

A detailed breakup and analysis of the metal powder market based on the technology has also been provided in the report. This includes pressing and sintering, metal injection molding, additive manufacturing, and others. According to the report, pressing and sintering accounted for the largest market share.

Pressing and sintering technology is the key to the metal powder market; it is one of the most traditional and commonly used production methods. The process involves compacting the metal powders at high pressure into a shape (pressing) and then heating the compacted component below its melting temperature for bonding and densification (sintering). This process is particularly cherished for the creation of highly accurate, intricate parts with little wastage of material, as it is both cost-effective and eco-friendly. Pressing and sintering have wide applications in the automotive, aerospace, and machine industries for producing gears, bushings, filters, and structural components with high mechanical strength and accurate dimensions. It is also suitable for high-volume production with consistent quality, which is important for mass production. As demand for high-performance, lightweight parts continues to grow, especially in the automotive and electric vehicle industries, the importance of the segment remains strong.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Automotive

- Aerospace and Defense

- Healthcare

- Others

A detailed breakup and analysis of the metal powder market based on the application has also been provided in the report. This includes automotive, aerospace and defense, healthcare, and others. According to the report, automotive accounted for the largest market share.

The automotive industry is a significant segment in the market due to its ongoing need for light, strong, and cost-effective components. Metal powders find extensive applications in the manufacturing of sintered components like gears, bearings, bushings, and structural components, which are crucial for engine, transmission, and chassis systems. Powder metallurgy enables exact component production with minimal loss of material, enabling high-volume manufacture and decreased overall vehicle weight, a critical aspect in enhancing fuel economy and satisfying aggressive emission regulations. The growth of electric vehicles (EVs) has also added pressure on using advanced metal powder applications for motors, battery systems, and magnetic components. With the future of the auto industry shifting toward electrical and green technologies, metal powders become more imperative in facilitating next-generation, efficient manufacturing capabilities.

Regional Insights:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others) was the largest market for metal powder.

The market in the Asia Pacific region is propelled by industrialization, growing automotive manufacturing, and robust manufacturing capacity in key economies like China, India, Japan, and South Korea. The region relishes a vast and affordable labor pool, strong infrastructure, and rising investment in new-generation manufacturing technologies like additive manufacturing and powder metallurgy. Asia Pacific's automotive and electronics sectors are two of the world's largest, generating huge demand for non-ferrous and ferrous metal powders employed in sintered parts, electronic components, and structural uses. According to the metal powder market forecast, with increasing research and development (R&D) spending and growing industrial uses, the Asia Pacific region will remain dominant in the global market. On the other hand, increased emphasis on the use of lightweight materials, energy efficiency, and emissions control favors the use of metal powder-based solutions in different industries. Government policies encouraging domestic manufacturing, further support regional market expansion.

Competitive Landscape:

The report has also provided a comprehensive analysis of the competitive landscape in the global metal powder market. Competitive analysis such as market structure, market share by key players, player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided. Some of the companies covered include:

- Advanced Technology & Materials Co., Ltd.

- ATI Inc.

- Carpenter Additive (Carpenter Technology Corporation)

- Continuum Powders

- GKN Powder Metallurgy

- H.C. Starck Tungsten GmbH

- Höganäs AB

- JSC POLEMA

- Kymera International

- Linde PLC

- Rio Tinto

- Sandvik AB

Kindly note that this only represents a partial list of companies, and the complete list has been provided in the report.

Latest News and Developments:

- On May 29, 2025, PyroGenesis Inc. announced that its Ti-6Al-4V (Ti64) coarse metal powder has been added to Boeing's qualified list of additive manufacturing materials. This certification recognizes PyroGenesis as an approved supplier and highlights the performance of its NexGen™ plasma atomization technology. The development marks a significant step forward for the company's integration into the aerospace supply chain, reinforcing its position in the high-specification metal powder market.

- On April 2, 2025, Epson Atmix Corporation, a subsidiary of Seiko Epson, announced the establishment of a new sales office in Munich, Germany, in collaboration with Epson Europe Electronics GmbH. The office aims to enhance the company's presence in the European market for metal powders and metal injection molding products. This strategic move is intended to improve delivery times, offer localized technical support, and meet growing regional demand, particularly from the additive manufacturing and 3D printing industries.

- On March 26, 2025, U.S.-based Metal Powder Works announced its merger with Australian welding technology company K-TIG, with the combined entity now trading on the Australian Securities Exchange under the name Metal Powder Works (ASX: MPW). The company successfully raised AUD 10 Million (about USD 6.517 Million) through a public offering, resulting in a market capitalization of approximately AUD 27.9 Million (about USD 18.174 Million). The merger aims to create an integrated manufacturing solution by combining metal powder production with advanced welding systems, targeting key industries such as defense, aerospace, and nuclear energy.

- On March 6, 2025, EOS GmbH announced the expansion of its laser powder bed fusion metal powder portfolio with two new nickel-based materials: EOS NickelAlloy IN718 API for demanding oil & gas applications and EOS Nickel NiCP tailored for the semiconductor industry. The IN718 API alloy meets API 6ACRA standards, delivering high-impact toughness, corrosion resistance, and tensile strength of 878 MPa—ideal for critical downhole and injection components.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Material, Technology, Application, Region |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Advanced Technology & Materials Co., Ltd., ATI Inc., Carpenter Additive (Carpenter Technology Corporation), Continuum Powders, GKN Powder Metallurgy, H.C. Starck Tungsten GmbH, Höganäs AB, JSC POLEMA, Kymera International, Linde PLC, Rio Tinto, Sandvik AB, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the metal powder market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global metal powder market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the metal powder industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Key Questions Answered in This Report

We expect the global metal powder market to exhibit a CAGR of 4.15% during 2026-2034.

The increasing utilization of metal powder, such as high-strength steel, aluminum, magnesium alloys, etc., to aid in manufacturing lightweight automobile components is primarily driving the global metal powder market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary closure of numerous end-use industries for metal powder.

Based on the material, the global metal powder market can be segmented into ferrous and non-ferrous. Currently, ferrous holds the majority of the total market share.

Based on the technology, the global metal powder market has been divided into pressing and sintering, metal injection molding, additive manufacturing, and others. Among these, pressing and sintering currently exhibits a clear dominance in the market.

Based on the application, the global metal powder market can be categorized into automotive, aerospace and defense, healthcare, and others. Currently, the automotive industry accounts for the largest market share.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global metal powder market include Advanced Technology & Materials Co., Ltd., ATI Inc., Carpenter Additive (Carpenter Technology Corporation), Continuum Powders, GKN Powder Metallurgy, H.C. Starck Tungsten GmbH, Höganäs AB, JSC POLEMA, Kymera International, Linde PLC, Rio Tinto, and Sandvik AB.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)